All German Shares Part 19 (Nr. 376-400)

Halftime !!! I covered now more than 50% of the German stock universe which is around 800 shares. In this post you’ll see still some entries that I have written pre-crisis that I then had to update significantly. Overall these 25 stocks resulted in 6 watch list candidates which is clearly above average.

376. Instant IPO Holding AG

2.1 mn market cap micro cap with very frequent name changes. “Pass”.

377. OTRS AG

16,3 mn EUR market cap IT/Software company. Although top line seems to have grown by more than 10% in the first 6M 2019, the company shows little profitability. Without capitalizing costs, the company would actually make losses. “Pass”-

378. Mologen AG

Old-time Biotech “pump and dump” stock that finally filed for insolvency in December 2019. 2 mn market cap remaining. “pass”.

379. Manz AG

Manz AG is a 168 mn EUR market cap equipment/machinery manufacturer that produces equipment for plants that themselves produce solar modules. The once high flying company is struggling, with top line decreasing and making significant losses. They do have a Chinese investor but these days the money in Solar is made by putting solar cells onto an empty field, cashing in subsidies and seling stocks/funds to investors, not in producing solar cells. “Pass”.

380. Hamburger Getreide Lagerhaus AG

1.8 mn EUR market cap nano cap with no real business. “Pass”.

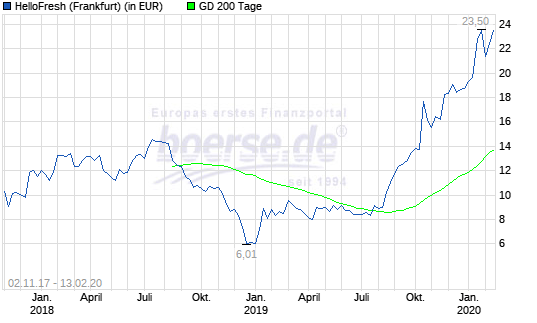

381. Hello Fresh AG

Hello Fresh, which has been IPOed in November 2017, is with a market cap of 4,5 bn EUR one of the most successful startup stories in Germany. The business model is quite simple: The company delivers boxes with groceries to their customers that are tailored for certain dishes (“meal kits”). The customer saves itself the walk to the super market and can directly start cooking with the recipes provided by Hello Fresh. The model is a subscription model, where the customer can chose how many boxes a week are delivered (min. 3 boxes). Since its IPO, the stock price has done surprisingly well, especially in the last few months, almost quadrupling from a low in early 2019:

Growth is still good: +40% in customers and sales yoy in Q3 2019. Structurally, however, the business doesn’t look too attractive. “Contribution margin”, which is the pure gross margin of sales minus cost of ingredients minus shipping costs is currently ~27,5%. Marketing costs are eating up this margin almost completely, but yes, the company is growing and adjusted profitability is growing.

However in my opinion there are not that many opportunities for HelloFresh to improve their margins from a structural basis and to me it is open, how sustainable their business model really is. “pass”.

COVID-19 Update: It turned out that meal kits are a pretty good idea these days.

382. Bet-at-home AG

Bet-at-home is as the name says, an online sports betting and gambling company, valued at 339 mn EUR market cap. In the first 9 Months 2019, the company had generated EBIT of 26 mn, but had to pay significant back taxes so that net income in total was only a single digit million number, Personally, I do have an issue with the whole online gambling sector, so I “pass”.

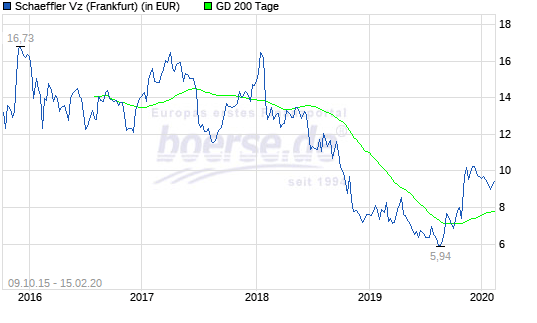

383. Schaeffler AG

Schaeffler is a 1.0 bn EUR market cap supplier to the automobile industry that went public in September 2015 at a price of 13,5 EUR per share. Schaeffler is still majority owned by the family and became famous for trying to take over bigger rival Continental in 2018 and almost going bankrupt in that process. At the time of writing, the family still owns 46% of Continental.

Looking at the stock chart we can see that Schaeffler got hit in 2018, but somehow recovered from the lows in 2019 recently:

Based on 9M numbers, top line is stagnating, EbIT has decreased by -40% yoy. Schaeffler pointed out that Greater China was one of their brights spots in 2019, which might be an issue now. Schaeffler has around 2,8 bn in debt, the holding company that owns the Continental stake has another 3,5 bn in debt. To me this construct is extremely vulnerable, especially with Conti also having lost more than 50% of its value over the last months. “pass”.

COVID-19 Update: The crisis hit Schaeffler hard and the stock is now trading at or below the lows of 2019. They are clearly in trouble.

384. Beate Uhse AG

Bankrupt shell company. “pass”.

385. AGIV Real Estate AG

0,3 mn EUR market cap shell company. “Pass”.

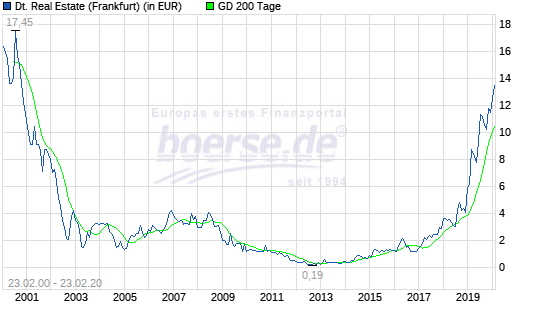

386. Deutsche Real Estate AG

278 mn EUR market cap company that is active in ….Real Estate of course. The long term stock chart shows that the stock has done nothing for a long time but then went up like a rocket over the last 2 years (who needs tech stocks if you have German RE):

AT first sight, the company aggressively values its properties upwards. Nothing to see for me, “pass”.

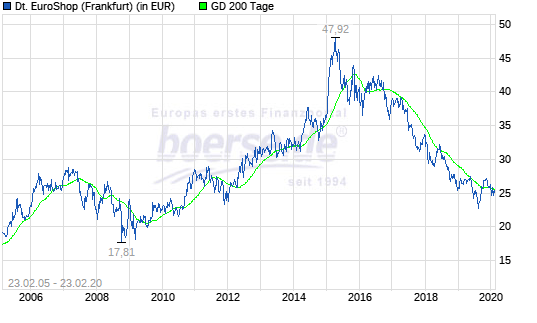

387. Deutsche Euroshop AG

Deutsche Euroshop AG is not a “1 Euro Shop” company but a real estate company that has specialized in Shopping malls with a market cap of around 0.8 bn EUR. Other than most Real Estate stocks, Dt. Euroshop’s stock is on a tailspin since a few years, most likely because of the perceived threat through online shopping:

Interestingly, current 9M numbers are not so bad. Dt. Euroshop is trading at ~2/3 of book value. This is actually a real estate stock that I out on “watch”.

COVID-19 Update: With all the shopping centers closed, Dt. Euroshop has been hit hard. Although the stock slightly recovered, the stock lost another -50%. For me it is not clear how to value these assets. But still a “watch”.

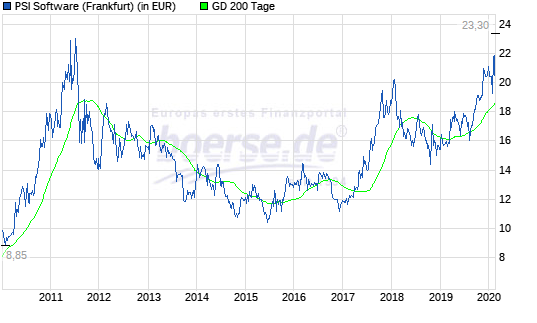

388. PSI AG

PSI is a 274 mn market cap software company. In comparison to other software stocks, PSI’s stock performance has been a “dud” over the last 10 years:

However, Growth also has been low single digits over the last few years and margins are quite low for a software company. Recently top line has been picking up with double digit growth, bottom line however is lagging. Still a candidate to “watch”.

389. Dahlbusch AG

Thinly traded 488 mn EUR market cap company with little free float. The company used to be a coal mine but this days only operates real estate. Reports are very thin. Maybe they have some hidden value to hide, but for me it is a “pass”.

390. Affimed NV

A 165 mn EUR market cap company doing something with immuno/Cancer. The company has some revenues (mostly milestone payments) but burns around 2 mn EUR per month. “Pass”.

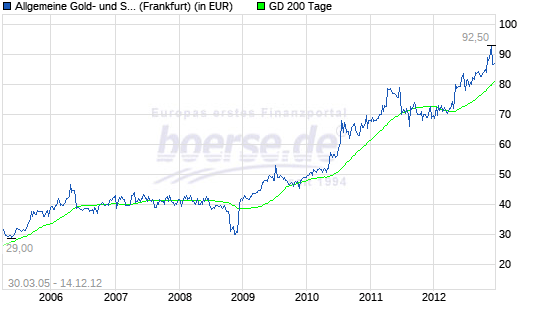

391. Allgmeine Gold und Silberscheideanstalt AG

“Agosi” is a 91% subsidiary of Belgian recycling giant Umicore with a market cap of 472 mn EUR. The stock shows a very good recent performance and was mostly unaffected by the Covid-19 turbulence as the chart shows:

With results stagnating or even decreasing over the last 5 years, I do not fully understand what justifes a valuation of around 30x Earnings. Therefore a “Pass” for me.

392. Edel SE

Edel SE is a 33 mn market cap company that mostly represents an independent music label. The company has had a “Mixed” 2019 with net income dropping significantly, although sales remained stable.

However the company has significant bank debt and low operating margins (~3% EBIT margin). Also the company is a KgaA, a German legal construction that restricts the rights of the shareholders significantly. “Pass”.

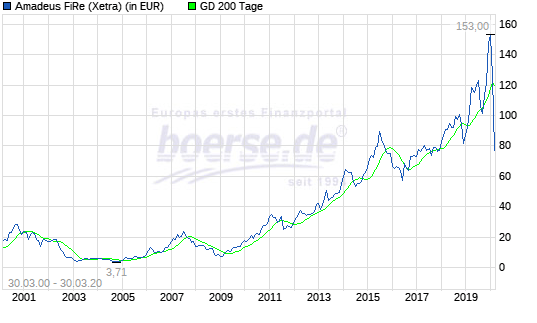

393. Amadeus Fire AG

Amadeus Fire is a 400 mn EUR market cap temporary work agency with a long successful track record and a focus on Germany. However the Covid-19 crisis hit the company hard, losing >50% from the February top.

At the current valuation, the company trades at ~15xPE. The recent annual report shows a nice growing top line, however a lower increase in the bottom line for 2019. Amadeus was very successful because they specialized in the IT and finance area, which are areas that showed a significant demand over the last 10 years.

At the end of 2019, Amadeus Fire made a relatively large acquisition with a company called ComCave thta offers trainign for areas like tax accountants. This acquisition seems to have driven the significant increase in the stock price until the beginning of the crisis. The purchase price seems to have been 200 mn EUR, financed by existing cash and a 170 mn EUR bridge financing. This represents around 13xEV/EBITDA according to German news articles.

Going into the crisis with 170 mn of shrot term debt is of course bad luck. The company cancelled the dividend which I think was a wise decision.

With ~40 mn pre acquisiton/crisis EBITDA and no previous debt, this won’t kill Amadeus Fire, but it needs to be seen how their business is impacted by the crisis.

In any case, it is an interesting case and a stock to “watch” more closely.

394. CompuGroup Medical SE

Compugroup Medical SE is 2.8 bn EUR market cap Software company specializing in the Healthcare sector. The company has been performing well and is one of Germany#s few software success stories. The CEO still owns 33% and controls with other related parties slightly more than 50% of the share capital.

As with other software companies, the valuation is quite high (15xEBITDA) but despite some acquisition, business has been stagnating in 2019 with slightly negative organic growth but significantly increased debt. EBIT and Net income decreased significantly, due to partly an impressive EUR 16 mn “broken deal” charge for a M&A transaction that didn’t materialize.

The COvid-19 crisis had little impact on the shareprice, but in my opinion the non-existing organic growth does not justify the valuation. “Pass”.

395. BBI Buergerliches Brauhaus Immobilien AG

BBI is a 124 mn EUR market cap commercial real estate company, owned itself (95%) by another listed company, VIB AG. The company has a profit and loss transfer agreement with VIB, therefore shareholders, so the 0,54 EUR per share guaranteed dividend is the maximum that a shareholder can expect. “pass”

396. centrotherm International AG

Centrotherm is a 52 mn market cap photovoltaic machinery company. The business seems to be very cyclical and not very profitable. The company was deep in the red for the first 6M 2019. “pass”.

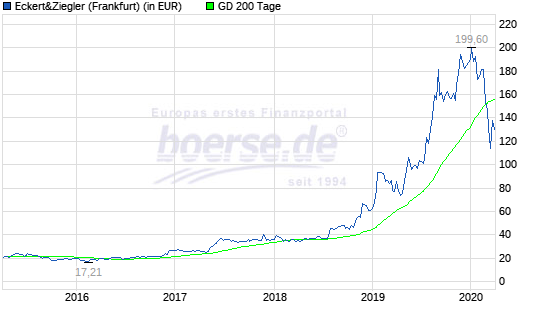

397. Eckert & Ziegler AG

Eckert & Ziegler is 688 mn EUR market cap company that according to the web site does the following:

The Eckert & Ziegler Group is one of the world’s largest providers of isotope technology for medical, scientific and industrial use. The core businesses of the Group are: cancer therapy, industrial radiometry and nuclear-medical imaging. The three business segments are: Medical and Isotope Products.

The stock price went up five fold from 2017 to 2020:

The question is clearly:why ? Looking at their key financials. they were able to more than double EPS from 2016 to 2019. Top line has been growing slower, but EBIT margins has been increasing von 11% to 18% in 2019. The company has net cash.

Nevertheless, a trailing P/E of around 34x is quite steep, but still it is a company to “watch” and dig deeper at some point in time in the future.

398. SNP Schneider-Neureither & Partner

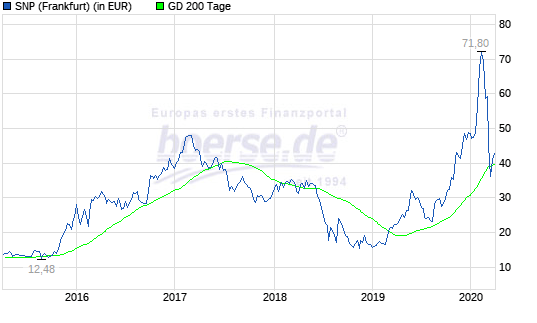

SNP is a 292 mn EUR market cap software / systems integration company. The company has been growing double digit in 2019, with software sales increasing very strongly (+50%). With 15 mn EBITDA, the company trades even after the crisis at around 24 times EV/EBITDA which assumes significant further growth.

As far as I understand it, they are active in the SAP environment, however offering own software tools to automate certain processes.

The stock price has been on a really wild ride recently:

For me it is a stock to “watch”, however at the current valuation with limited priority.

399. Scout24 Group

Scout24 is the leading German/European online classifieds player. Up until recently, Scout ran two segments: Auto classifieds and Real Estate. However just a few days ago, the sale auf Autoscout24 to former PE owner Hellmann & Friedman closed.

Scout24 is selling Autoscout24 for 2.84 bn EUR. 700 mn will be used to repay debt and ~1.7 bn to repurchase shares.

Based on their 2019 preliminary numbers, ~210 mn EBITDA remain with Scout24. The company has total debt of around 800 mn and a market cap of 5.8 bn ER.

So including the cash received, the “stub” is valued 3.8 bn EUR. Compared to Righmove in the UK, which trades currently at 18xEV/EBITDA, this looks like a fair valuation. The business as such is to a certain extent counter cyclical, as real estate agents need to put more efforts in promotion when no one wants to buy.

I will put them on “watch” to see if there might be a lower entry point in the future.

400. Murphy & Spitz Green Capital Aktiengesellschaft

Murphy & Spitz is a 6 mn EUR nano cap that specializes in managing “green and sustainable” investments. For the 6 mn market cap, inevstors get ea nice story, 80k sales and 80k losses. “Pass”

M&S: for 6m Marketcap, you get >20 MW of generating capacity that is valued around 1mn/MW at peers. M&S is a takeover story, 7C already bought up 10% per last year and probably has even more now (one big holder from Turkey has been selling his stake late last year which can be seen in the stock market volumes).

The valuation multiple Price per MW only makes sense if production costs are very similar to peers, right? Are they?

of course they are. It’s the same asset (solar and wind parks). The major differences are feed-in tariffs (determining CF) that differ according to the vintage of the park, but that mainly smoothes out in a diversified portfolio. Look at page 8 of this slide deck: http://solarparken.de/PPT/Plan%203Y%20FINAL%20FOR%20WEBSITE%20-%20Checked%20SDP%20on%2008.12.2019.pdf

M&S is clearly the cheapest of the bunch. Management is entrenched and sold a stake to a “friendly” investor, but I’m confident the 7C guys will squeeze them.