All German Shares Part 21 (Nr. 426-450)

And the next batch of (mostly) randomly selected German stocks. The only exception I do make for my selection is when one company owns a big stake or is related closely to another listed company. Then I’ll try to look at them in sequence. This time, 5 stocks made it onto the watch list.

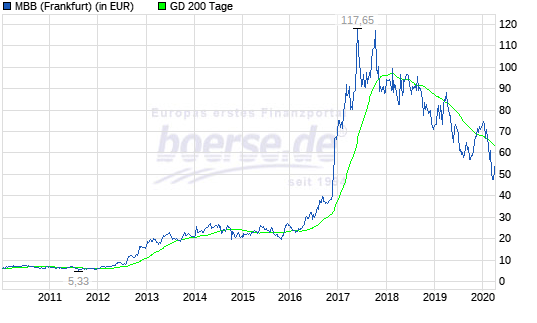

426. MBB SE

Another listed “Mittelstands” holding company with a 317 mn EUR market cap. Looking at the stock chart we can see, that between 2015 and 2017 the stock price went up significantly, Since then the stock is on a downward trend, despite share repurchases:

The company has significant net liquidity, however the underlying businesses are low margin. The drop in value might be the result of the drop in value of their most successful participation, Aumann AG. As I am not a big fan of this “Mittelstand” Holding Cos, I’ll “pass”.

427. Aumann AG

Aumann AG is a 131 mn EUR market cap machinery company that was IPOed in 2017 as a “pioneer” to enable E-mobility by its former owner MBB (see above).

The stock chart shows that this seems to have been a quite successful “pump and dump” IPO, as now the stock trades only at a fraction of the IPO price and the stock declined long before the current crisis:

In 2018, Aumann reported solid numbers with very impressive growth (top line and Net income +40% yoy), although margins (EBIT margin ~9%) were not too impressive.

However already the 4th quarter seems to have been quite week as growth and EBIT margins for the first 9 months 2018 had been a lot better. Then 2019 started to look ugly, with a weak first quarter, followed by even worse half year numbers and 9M numbers. Order entry more or less cratered, top line and bottom line shrank even more.

On the plus side, the company still has net cash, but cash has been shrinking fast in the last few months. Overall I do think Aumann is one of the better positioned automobile suppliers but still is in for a very hard time. “Pass”.

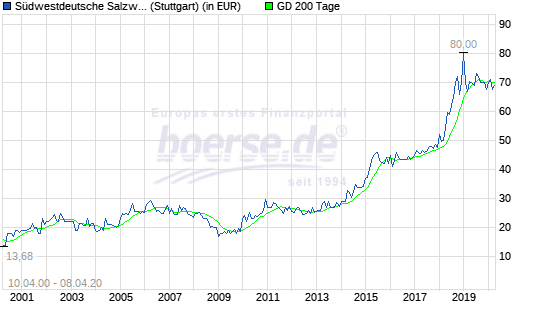

428. Südwestdeutsche Salzwerke Aktiengesellschaft

Südwestdeutsche Salzwerke is as the name says, a 725 mn EUR salt mining/producer. The company is pretty “boring” which I normally like and the stock price is quite unspectacular but has increased nicely over the past few years:

The company showed a loss in 2019 but this seems to have been a one time effect. Both the core salt business and the second segment “disposal” are quite profitable with double digit EBIT Margins. Disposal, which seems to be a second use for salt mines even has EBIT margins of 20%. However, free float of the stock is only 2% and 98% are owned by Government entities which for me is a direct reason to “pass”.

429. HCI Hammonia Shipping AG

A 3.7 mn EUR nano cap investing in container ship projects. Very thin reporting, “Pass”.

430. Pulsion SE

Pulsion is A med-tech company that has been majority acquired by Swedish competitor Getinge in 2013/2014 at EUR 16,90. The 170 mn EUR market cap company is traded very thinly on the “Pink sheets”. As part of a Profit and loss transfer agreement, minority shareholders do not have the right to participate in any profits but are compensated with a guaranteed dividend of 0,86 EUR per share. Again, this is something for specialists, for me it is a “pass”.

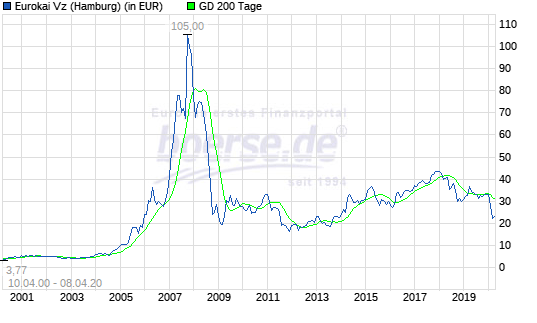

431. Eurokai AG

Eurokai is a company that I had owned at least 2 times in the last 20 years. The 337 mn EUR market cap port operator owns (partially) a wide network of ports and should in theory be a nice and boring “infrastructure” investment. Looking at the stock chart we can see however that the stock price looks more like a tech stock, esp. the spike before the GFC:

The majority of the operated ports are in northern Germany, however they also have some activities in Italy as well as in Algiers and Cyprus. The YTD 2019 numbers look very positive, however there is a one-off gain form a disposal included. In general, due to a lot of minority interests, the accounts are not easy to understand and one really needs to see the annual report to guess how business is really going. The company is dominated by the Eckelmann family which controls 75% of the voting rights. Clearly the business is cyclical, but for me it is worth to “watch” and revisit at a later stage.

432. EcoUnion AG

Insolvent “zombie” stock. “pass”.

433. Aurelius Equity Opportunities SE

Aurelius is one of the larger “listed PE” holding companies in Germany with a market cap of currently 508 mn EUR. To say that the company and its CEIO is “controversial” is an understatement. Several international short sellers attacked the stock which was a growth star for the earlier part of last decade. He was part of the quite “infamous” Arques AG which in the early 2000s created the business model of buying 1 EUR companies and show the badwill as profit which he seems to have perfected with Aurelius. This is a stock I wouldn’t touch even with a 100 foot pole. “pass”.

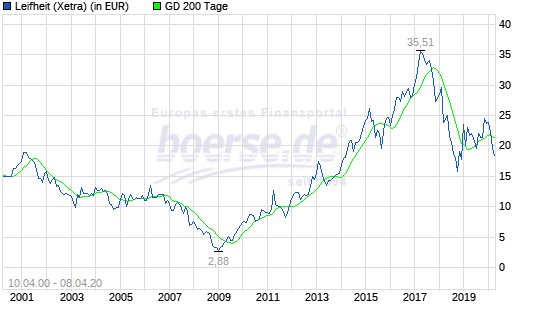

434. Leifheit AG

Leifheit, a 184 mn market company is also a company that I owned at least once during the last 20 years or so. It is a well known German brand for all kind of household “helpers”. In 2019, the business of Leifheit stagnated and profits declined. The company has significant net cash, (50 mn), however also significant pension liabilities. The business itself is quite low margin. They intend to invest more in advertising but it needs to be seen how effective this is.

For some reason, the stock price went up like crazy in 2017 but since then has lost almost -50% from the top:

There has been some movement in Managment and SUpervisory board, but overall I do not see that Leifheit is an interesting stock at this level, so I’ll “pass”.

435. MVV Energie AG

MVV is a 1.8 bn EUR market cap regional utility company. The company has only a very small free float (~5%). In a very interesting move, two shareholders decided to sell their 45% stake to a UK infrastructure fund. However, the city of Mannheim still owns 50,1%. As I don’t like stocks with the Government as shareholder, I’ll pass on MVV.

436. TAG Immobilien AG

TAG is a 2,8 bn market cap real estate company specializing on residential real estate in northern and eastern Germany, mainly in the lower end of the market. The company has a very interesting part, starting out as a local railway company in the Bavarian mountains and then transforming itself into a real estate company from the year 2000. TAG was run for some time by the Rolf Elgeti, one of the more controversial persons in the German capital market scene. Elgeti is still Head of the supervisory board.

Optically, TAG looks quite cheap, however the majority of the results are revaluation gains. This leads to the fact that the “EPRA NAV” used to be actually lower than the market cap which is quite unusual. The ongoing revaluation for me is not a good sign as it indicates a very aggressive accounting behavior.

As I am not a fan of real estate companies in general, TAG Immobilien is a clear “pass”.

437. Konsortium AG

Konsortium AG is a 1 mn market cap holding company that belongs to a very shady group of players (Reich family) in the German small cap space. “Pass”.

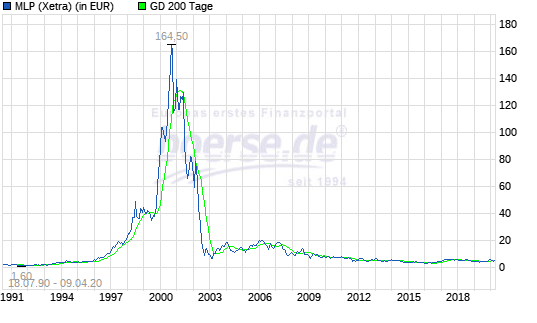

438. MLP AG

MLP AG is a 550 EUR market cap financial company that distributes all kind of financial services via an advisor network. The chart shows the quite interesting history:

In the late 90s, early 00s, MLP was “THE” hot financial growth stocks. However the dotcom bust took its toll and the company never fully recovered.

Looking at their 2019 report, it is quite remarkable that for the last 3 or 4 years thay manged to grow steadily again. However, they seem to actually run a banking business now on top of the core advisory business and the stock has recovered quite quickly. A candidate to “watch”.

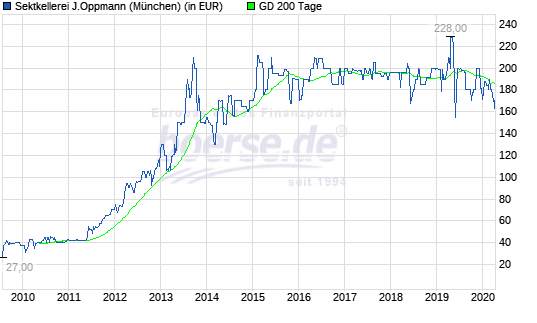

439. Sektkellerei J. Oppmann AG

J. Oppmann is a sparkling wine producer with a 5.6 mn market cap. The company has a strange stock chart:

The stock increased 6x from 2010 to 2013 and then…nothing. Looking back into my blog, I actually had covered them a long timein 2011 ago as a quite well performing spin-off. However the company doesn’t publish any reports online and I guess this is only something for “Liebhaber”. For me it is a “pass”.

440. Euromicron AG

Euromicron is a company that I had looked at in the past and always found their accounting extremely questionable. The company survived longer than I though tbu then went bankrupt in late 2019. “Pass”.

441. Voxeljet AG

Voxeljet AG was one of the big high flyers of the 3D printing craze in early 2014. The company went public in the US and had a market cap of over 1bn USD. These days, the stock has lost more than -96% and the market cap is around 20 mn USD.

The company which produces large, industrial sized 3D printers. However business does not look too good. They broke the loan covenants of an EIB loan which then has been waved according to an SEC filing.

However the company has never made and profit and sales are very lumpy. Nevertheless I’ll put them on “watch” as I like 3D printing.

442. Adler Modemärkte AG

Adler is a 65 mn market cap clothes retailer specializing on the very cheap end of the market and on people aged 55 and above. However, even before Covid-19 this was a brutal business. Somehow, Adler managed to squeeze out a higher profits in 2019 despite lower top line sales. For a retailer, the balance sheet looks relatively solid, but still the whole sector is for me structurally unattractive. “Pass”.

443. DNI Beteiligungen AG

A 2.2 mn EUR market cap holding company. The company invests in listed securities but reports very infrequently. “pass”

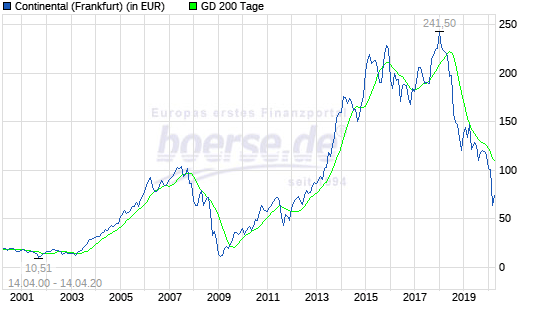

444. Continental AG

Continental is one of the largest global automobile suppliers globally with a current market cap of around 14.8 bn EUR. As the chart shows, Conti’s problems started long before Covid-19 arrived:

The main reason despite the general weakness of the car industry seems to be that Conti is focused to a large extent on classical combustion engines and is hit by the shift to EVs. Conti tried to IPO their most vulnerable part called “Vitesco” but then decided to go for a spin-off in late 2019. Conti is vulnerable because the largest shareholder Schaeffler is in deep trouble itself, so there is little chance of support there. Schaeffler is significantly indebted after the failed take over attempt in 2008/2009.

2019 was already an ugly year for Conti with stagnating sales and negative EBIT plus a significant increase in net debt to 4 bn EUR from 1.6 bn (driven by lease accounting). The loss itself was driven by a significant Goodwill impairment.

Conti still plans to pay a 1 bn dividend which in my opinion is a really bad idea but I guess the main shareholder Schaeffler desperately needs the money. Another interesting aspect is that the boss of the Supervisory board, Wolfgang Reitzle is famous for his gigantic mergers (Linde, Lafarge).

Overall I do think that Conti has a lot of substance (especially the tire business) but I am afraid that the worst is yet to come. Nevertheless it is a stock to “watch”:

445. Clockchain AG (former Uhr.de)

Something with online and watches. 0.1 mn EUR market cap. “Pass”.

446. Dr. Bock Industries AG (listed in Vienna)

Dr. Bock is a men’s clothes producer that I have never heard of and, which despite being in Germany is only listed in Vienna and in theory has a market cap of 72 mn EUR which seems some kind of insider joke when looking at their 2 mn sales in 2018. However I could not see any trading for the last 18 months or so. “pass”.

447. Haemato AG

Haemato is a 45 mn EUR market cap pharmaceutical company that seems to specialize in “grey market” imports of pills within Europe. They seem to have some problems as topline was shrinking dramatically in 2019 and the company went into a loss position. “Pass”.

448. Heidelberg Pharma AG

Heidelberg Pharma AG is a Biotech company with a 147 mn EUR market cap specializing in cancer treatments. The company actually does have sales (7mn), but as most Biotechs is burning money at a current rate of 8-9 mn ER a year.

Interestingly, the stock price jumped in March. The company, backed by SAP Founder Hopp seams to be somehow linked to developing a Covid-19 vaccine/treatment. Not my area of expertise though, “pass”.

449. Renk AG

Renk AG is a 728 mn EUR market cap supplier that was long majority held by Volkswagen. In a surprise move, Volkswagen sold the company in early 2020 to PE investor Triton. Triton had to make an offer to minority shareholders which at teh moment would be a little bit above the current share price (106 vs. 104). Plus there could be a chance of a higher price for a subsequent squeeze out. Soemthing for the “special sit” pocket but not a long term watch, rather a “pass” at his stage.

450. Nordwest Handel AG

Nordwest is a 60 mn market cap trading company that wholesales construction equipment and tools to smaller shops. The company is majority held by the Rothenberger Holding, a German/Austrian family company. The company has been doing quite well in the last few years, riding the construction boom in Germany. it will need to be seen how the business is hit by the crisis. Technically, the company looks quite cheap and the first quarter doesn’t seem to be impacted by Covid. “Watch”.

A freindly reader sent me this comment via Email that I am allowed to post here:

MBB: CEO Nesemeier führt das Unternehmen seit Beginn an (25 Jahre) zusammen mit seinem non-executive Mitgründer Freymuth als “Familienunternehmen” wie er es nennt. Man muss ihm lassen, dass er ein sehr guter Capital Allocator ist. Book Value per Share Zuwächse sind um die 20% seit dem Listing in 2006, und dies schon vor dem Aumann IPO. Seine Philosophie ist – a la Buffett – Beteiligungen kaufen und behalten. Das ist anders als bei Aurelius et al. Bei Aumann hat er trotz des Elektro-Hypes versucht, den Gruppenzusammenhalt zu bewahren und gleichzeitig für MBB einen enormen Capital Gain Cash-wirksam zu realisieren. Das Ergebnis ist, dass er nun (wieder) zum richtigen Krisen-Zeitpunkt bei MBB und auch bei Aumann enorme Cash-Bestände, und Möglichkeiten zu Zukäufen hat. Er könnte also wieder genau das Richtige gemacht haben. Mir gefällt vieles an der Kultur dieses Beteiligungsunternehmens, u.a. dass er stets versucht, die Minderheits-Aktionäre fair und klug zu bedienen: (i) Dividend Raise Policy (er möchte MBB im Dividendenadel halten – d.h. keep or raise), (ii) auch wenn er schon lange kein Geld mehr vom Kapitalmarkt benötigt macht er in Maßen IR weil er die IPO-Aktionäre und deren Nachfolger fair behandeln möchte nachdem sie ihm die Möglichkeit für die MBB-Investments gegeben haben und (iii) Dutch Auction style Buybacks. Er kauft seine Beteiligungen günstig ein. Was mir nicht so gut gefällt war der Managment-Compensation Windfall der sich durch den Aumann-IPO ergab (2-stellige EUR Mio-Beträge), wobei das Incentive System seither gedeckelt wurde. Allerdings ist der Chief Investment Officer nach dem Windfall dann auch seiner Wege gegangen – dessen Nachfolger ist sehr jung, eher PE-Fonds-style. Außerdem ist das parallele Listing von Aumann und Delignit auf die Dauer nicht sinnvoll bzw. verursacht es unnötige Kosten und Management Distraction. Sicher gibt es auch ein Key Man Risiko.

Das liest ein wenig wie i-i.net?