All German Shares Part 23 (Nr. 476-500)

We are getting close to having covered 2/3 of the German stock universe. Among these 25 randomly selected stocks, I have identified 7 which are at least worth watching, although none with high priority.

476. E.On AG

E.on has changed a lot over the last years.I had written about the company in 2013 and luckily I never invested.

They spun-off the ugly legacy business Uniper, and took over the good part of RWE (Innogy). That makes their numbers very hard to read. Overall at the moment it doesn’t look super attractive as the company still has many problems (UK etc.). Therefore a “pass”.

477. uptech AG

uptech AG is a 2.7 mn EUR Nanocap with frequent name changes that does something with Crypto/Blockchain/Distributed ledgers. “pass”.

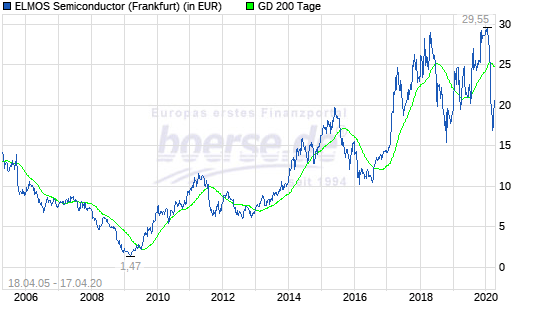

478. Elmos Semiconductor AG

Elmos is a 403 mn EUR market cap company that is active in the Semiconductor industry. As far as I understand, they mostly produce for the automobile sector which might be an issue. Compared to other automobile suppliers, the company still grew in 2019 and has double digit EBIT margins. Elmos sold subsidiary SMI late last year which netted them 95 mn USD. As a consequence, the company has net cash.

The stock price has been hit quite hard by the crisis and only partially recovered:

Depending on how to to treat restructuring expenses, the company trades at around 9xEV/EBIT based on the continuing part of the business. At first sight this looks interesting, therefore “watch”.

479. Altech Advanced Materials

1.3 mn EUR market cap stock which is the “reincarnation” of a fraudulent German-Chines eStock (Youbisheng Green Paper). “Pass”.

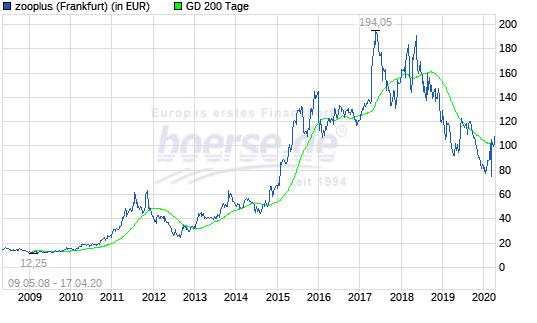

480. Zooplus AG

Zooplus is a 825 mn Market cap company specializing in E-Commerce for pets. The company has grown into 1 .5 bn sales company despite the continuing threat of Amazon. In 2019, the company grew around 15%. The company does around 3/4 of the business in Germany, the rest in Europe.

Looking at the stock price, we can see that Zooplus has seen already better days:

Nevertheless, they could increase gross margins in 2019 to around 30%. What I found interesting is that they show in their annual report target prices of sell side analysts which range from 52 EUR to 185 EUR which is a very unusual wide range.

On the other hand, EBITDA margins are still super low and I do not know how and if they can scale logistics enough to make the business interesting. But still a candidate to “watch”.

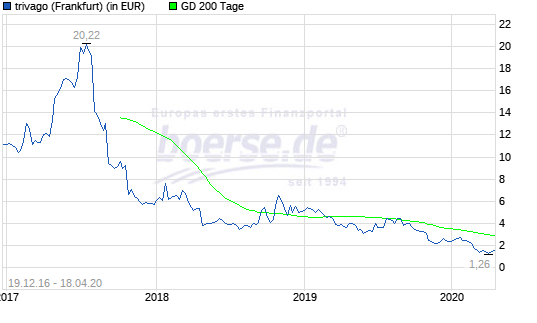

481. Trivago NV

Trivago is a 540 mn EUR market cap travel aggregator which I looked into in detail during my “Travel series” 3 years ago. Since then the stock has lost more than -90% with a really ugly stock chart:

The business ran already in trouble some time ago when Booking and Expedia (which is still majority shareholder) decided to pay less to Trivago. As in many comparable cases, the opening of their fancy new headquarters in December 2018 indicated the end of the success. At year end 2019, Trivago had ~220 mn EUR cash left on the balance sheet and the next months will be brutal. To me it is not clear if they will survive this and the founder/CEO left at the end of 2019. As I have a soft spot for travel stocks, I wil put them still on “watch”.

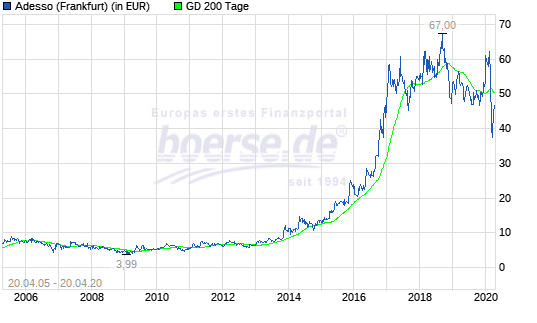

482. adesso AG

Adesso is a 286 mn EUR IT software/sytems integration company. The company grew top line in 2019 by 20%, EBITDA by +46%, however without IFRS 16%, EBITDA grew only 10%. Nevertheless, with 12x EV/EBIT the stock is not expensive. The stock chart shows that for a long time the stock did nothing and then “exploded” from 2015-2018.

Adesso’s main client groups are banks and Insurance companies. Whereas for banks there seems to be some kind of stagnation (+1%), the insurance part grows very fast (+37%). The former founders own ~45% of the company, but ownership of the current management is relatively small. Nevertheless one to “watch”.

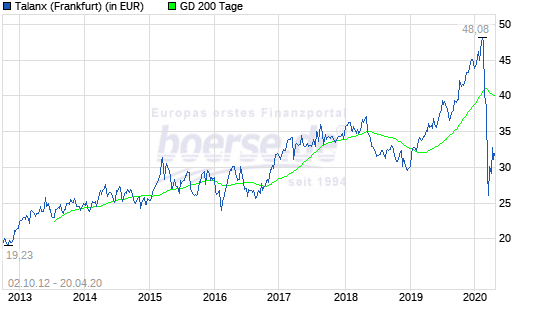

483. Talanx AG

Talanx is a 8 bn market cap insurance company active in the insurance and Reinsurance business. Talanx owns 50,2% of Hannover Re which is the 4th (?) largest Reinsurer globally. The freefloat of Talanx is however relatively small, as 79% are owned by HDI, a Mutual Insurance entity.

What I find interesting at first sight is, that the insurance result has been negative over the last 5 years and investment returns are the sole profit source for the company. This is partially driven by life insurance but also the P&C part itself is not really profitable. The “realized” return on investments is 3,5% which in my opinion is not a sustainable level based on their asset allocation (97% fixed income).

The stock got hammered by the crisis but had a great run before:

So basically, the stock is now back on the level of the year before. As I have a soft spot for insurance companies, I’ll put them on “watch” although with low priority..

484. Blockchain Infrastructure Group AG

A 2.2 mn market cap company with no business but lofty ambitions. “pass”.

485. Heliad Equity Partners AG

Heliad is a 49 mn EUR market cap listed investment holding that invests into Fintech and other “Innovative” businesses. The main asset is a participation in the listed FinTech Group AG. Helöiad itself again is owned ~45% by listed FinLab AG. Overall a pretty complicated picture plus the typical “KGaA” structure lead to a clear “pass”.

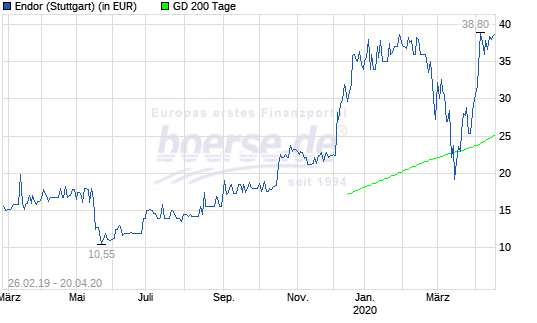

486. Endor AG

Endor is a really interesting company. The 68 mn EUR market cap firm produces and sells gear for virtual car racing. As such, the company has gotten a little hyped as “E-Sports” pure play and the stock chart looks “Exciting”:

During the crisis, the stock lost -50% but recovered quickly to new ATH as staying at home in theory might push their business further. For the first quarter 2020, even before Corona, the company saw a sales increase of +90% yoy after growing ~80% in 2019.

The company trades at a P/E of ~17, which is not cheap, but if they continue gorwing like this it would be Ok. A clear candidate to “Watch”.

487. Panamax AG

0.5 mn EUR market cap “Zombie”. “Pass”.

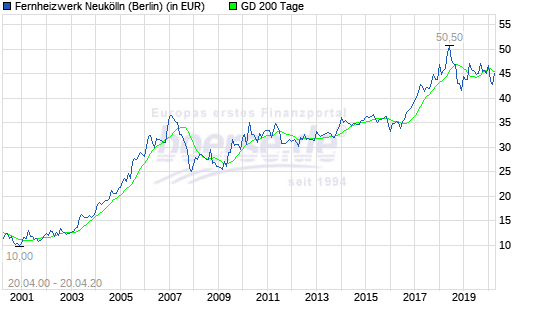

488. Fernheizwerk Neukölln

Fernheizwerk is a 105 mn EUR market cap local utility company in Berlin. The company is pretty boring but the stock has moved steadily upwards over many years:

80% of the shares belong to Swedish Vattenfalll. 2019 9M didn’t look too good. For me the company is not so interesting, therefore I’ll “pass”.

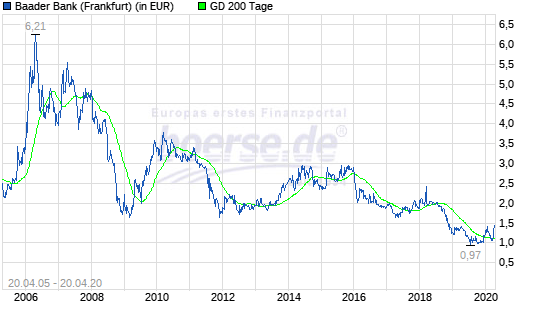

489. Baader Bank

Baader Bank is a 65 mn EUR market cap bank that is active in securities trading and related services. The company made a big loss in 2018. 2019 is better but they are still loss making. The stock is on a downward trend for a long time:

Life is too short for these kind of stocks, therefore “pass”.

490. Daldrup & Soehne

Daldrup is a 15 mn EURmarket cap company that offers drilling services for water wells etc. The company went public in 2007 and was hyped as a “geothermic” alternative nergy play, but the stock price is on a long decline since then. The company is loss making, the CEO from the founding family retired and the head of the supervisory board is a former politician. “Pass”.

491. Beteiligung im Baltikum AG

0.9 mn EUR market cap holding company that has seen better days. The last report is from 2016 and they seem to have issues with law enforcement. “Pass”

492. Commerzbank AG

Commerzbank is Germany’s second largest bank with a market cap of 4 bn EUR. The bank is struggling since the GFC where they we so “smart” to buy Dresdner Bank. The stock looks dirt cheap but they have structural problems like a much too high cost base and no clear business model. Profit declined by -25% in 2019 and Covid-19 doesn’t make things that much better.

Comprehensive income was even lower, as well as in 2018. The high book value per share (22 EUR) doesn’t help if they are not able to generate any meaningful returns. Covid-19 will show how resilient the bank is, but I don’t want to find this out as a shareholder. “Pass”.

493. Zapf Creation AG

Zapf Creation is a 150mn EUR market cap manufacturer of branded baby and children toys with a very interesting history.

Zapf IPOed in 1999 and was a shooting star, expanding quickly international. However in 2006 there was a big scandal and the company got close to bankruptcy.

After some back and forth, the owner of US toy company MGA Entertainment went for Zapf and is now owning the majority. Zapf has been delisted from regulated markets in 2018 and since then is only publishing regulatory required information. I guess Zapf could be interesting for “insiders” and patient special situation guys, but for me it is to cumbersome to dig into this one. “Pass”.

494. Verallia Deutschland AG

Verallia is a 482 mn market cap glass producer. It used to belong to the St. Gobain group but the whole division was sold to Apollo a few years ago. Apollo owns ~97% and has exercised a profit transfer agreement with the company. Verallia Shareholders “only” are entitled to a 17,06 EUR per share dividend which translates into a dividend yield of ~3,5%. Could be interesting for someone looking for a relatively safe yield, for me it is a “pass”.

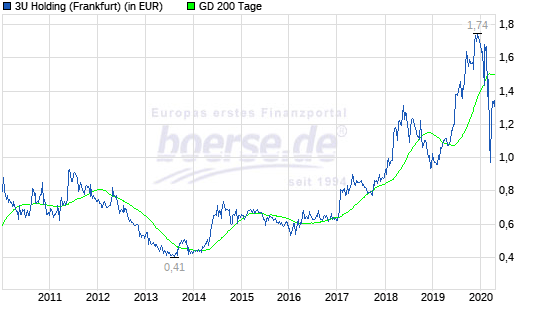

495. 3U Holding AG

3U Holding is a 48 mn company that I had looked at in the past (outside the blog). The company originally was active in the TelCo business but then sold the main operating entity. They then decided to become an investment holding and invested in all kind of assets like renewables and cloud computing.

What looked pretty stupid back then looks a lot better now, even with the recent drop:

In 2019 they could increase top line by 10% and doubled their profits. However the profit increase was only driven by selling their own real estate, operationally not much happened. Interestingly they show the result of the property sale in EBITDA which is “a little bit” misleading. Nothing to see here for me at this stage, “Pass”.

496. GWB Immobilien AG

Insolvent Real Estate company. “Pass”.

497. Intertainment AG

A 4.5 mn EUR market cap company that trades media rights. No observable business, negative equity, “pass”.

498. aap implantate AG

15 mn market cap “med tech” company with a long history of losses and no observable improvement. “Pass”.

499. Deutsche Beteiligungs AG

DBAG is one of the “original” listed PE companies in Germany with a market cap of 438 mn EUR. As a specialty, the company both, invests from its own balance sheet as well as runs PE funds for 3rd party investors. The company has a decent track record, has returned a lot of cash to investors in th past and, according to their annual report, has outperformed the DAX and SDAX over 1, 3,5 and 10 years.

They have raised a new 1 bn fund by the end of 2019 which should give them a lot of firepower to do deals in the coming months.

This is one of the very few German listed PE companies that looks interesting, therefore “Watch”.

500. 4SC AG

4SC is a 80 mn EUR market cap Biotech company that develops pharmaceuticals against cancer. The company has some sales but, as other Biotech companies, is burning money. the company is able to raise money though, the largest shareholder is Santo Holding, which is the vehicle of the Hexal founders and billionaires, the Strüngmann twin brother. As I do not understand these kind of businesses, I’ll “pass”.

500 mark! Phew! Good job. I’ve been enjoying the series thoroughly.

Regarding Baader: did you factor in that the bank sits on a windpark in Croatia which blows 4 million Euros profit (!) each year into the bank’s balance sheet? It’s in their statutory publications but not particularly highlighted. IF they would decide to sell this asset, this could mean almost the whole current market cap in cash on top of the marketcap.

Haven’t heard about that one. Than ks.

Do you know what the ticker in google finance for Endor is?

Thanks for this work!

Thanks for the next batch!

“watch although with low priority” reminds me of an new acquaintance who said “let’s stay in touch loosely”. Of course, I never heard from him again.

Haha

Good one indeed. I would say: Stocks to look at when I am really bored….