All German Shares part 28 (Nr. 601-625)

Another 25 randomly selected German stocks. This time, there is only one “watchlist candidate” among them.

601. Elbstein AG

Elbstein AG is a 29 mn EUR market cap holding company that is majority owned (75%) by the billionaire Ehlerding family. The company invests among others in listed German companies. The stock price is flat over the last 5 years or so which might indicate that the investment success is limited. Nothing to see for me, “Pass”.

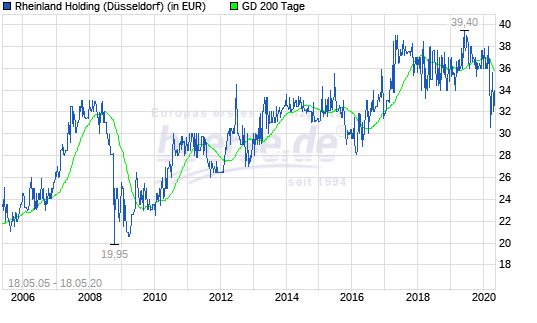

602. Rheinland Holding AG

Rheinland Holding is a small German Insurance company with a market cap of 119 mn EUR. The stock chart is “super boring”, although with a small long term uptrend that one rarely sees with insurance companies over this period:

As many other insurers, the stock looks cheap with a trailing single-digit P/E and a P/B of 0.6. The company is majority owned by the billionaire family Werhahn.

What I don’t like is that one of their businesses is insuring loans against unemployment/disability and that they only issue reports according to HGB which is extremely non-transparent, even for the standards of insurance. All in all a “pass” for me.

603. Hyrican AG

A long time ago (2003), Hyrican was a shooting star producing cheap PCs and notebooks. Since then, the share price is on a long and painful downtrend. The current market cap is 15 mn EUR and the company has gone pretty “dark”, issuing only a minimum of information. “Pass”.

604. Diebold-Nixdorf AG

Diebold-Nixdorf is a very interesting case. The 324 mn EUR market cap company used to be a part of the Siemens Group but bought in 1999 by KKR. KKR listed the business in 2004 and fully exited the company soon thereafter. In 2015, US group Diebold took over the majority and then merged the company into the new Diebold Nixodrf” AG.

Looking at the share price, the new entity doesn’t look like a huge success (yet):

Sales in 2019 have declined a second time in a row and the company showed a substantial loss. Diebold-Nixdorf’s main product are ATMs, additionally they also offer solutions for retailers. Both product groups were already in trouble before Covid-19 and will clearly not belong to the long term winners.

Cashflow is an issue and the company has (too much) debt. In sum a clear “Pass”.

605. MediNavi AG

0.3 mn EUR Nonocap. “Pass”.

606. ProSiebenSat1 Media AG

ProSieben with a market cap of ~2.6 bn is one of the market leaders of private “free TV” in Germany. Private TV in Germany had always the issue that TV viewers are obliged to pay for the state owned channels. Therefore ad financed FreeTV was more dominant than US style “cable TV”.

ProSieben has a very volatile history as we can see in the stock chart:

The company got IPOed in 1997, fell hard after the dot.com crash. The US based investorHaim Saban took over the majority cheap but sold out with a nice profit to KKR and Permira in late 2006. Permira and KKR exited in 2013 with a decent profit.

The stock price peaked in 2016. Profits in 2016 were higher than now, meaning that in the last 3 years, ProSieben failed to create much value.

In general I think there is clearly an issue with both, streaming offerings as well as more efficient advertising over the internet compared to “hard to measure” TV ads. ProSieben expanded significantly into E-Commerce but there are doubts how successful that push really is. A few weeks ago, the controversial CEO had to leave.

I am not sure if ProSieben is “good value” but it is still an interesting case and a stock worth to “Watch”.

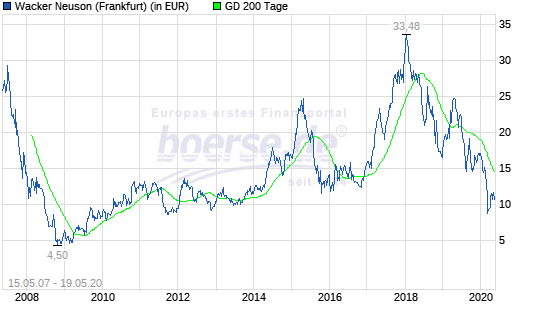

607. Wacker Neuson SE

Wacker Neuson is a 818 mn EUR market cap company that produces equipment for the construction industry. The company was IPOed in 2007 and 2/3 of the shares are still family owned. The stock price shows that as of now, the stock price is below the IPO price however with some spectacular rallies in between:

The stock looks cheap based on “traditional” metrics like P/B (0,6) and P/E (~9), margins in 2019 were Ok despite already retreating compared to 2018. However cashflows look bad both in 2018 and 2019 and ROCE really bad.The problem seems that they have huge working capital requirements. Overall nothing that excites me at this stage, “pass”.

608. Co.don AG

Co.don is a 30 mn EUR market cap “Biopharmaceutical” company that has sen better days. The company has little sales but rather large losses. Nothing to see for me here. “Pass”.

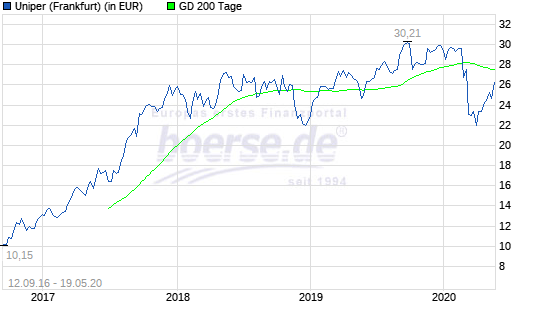

609. Uniper SE

Uniper is the “ugly child” of E.on that was spun-off in 2016 from E.On. I looked at Uniper back than and unfortunately did not invest. The stock since then developed nicely:

Part of that increase in share price is clearly driven by Finish utility Fortum who in the mean time owns 73,4% of E.on. It is pretty clear that Fortum will try to asume control of E.On at some point but I guess this is now more a “special situation” play. For me, for the time being a “pass”.

610. Stern Immobilien AG

Stern is a 30 mn EUR real estae company that buys, holds and sells real estate. Nothing of interest for me, “pass”.

611. Plan Optik AG

Plan Optik is a 7 mn EUR market cap company that soemhow develops and distributes technical items in the “Optoelectronic” area whatever that means. “Pass”.

612. UniDevice AG

UniDevice is a 20 mn EUR market cap B2B distributor of smartphones that somehow went public in 2018. The company has a operating margin of 1% and the balance sheet looks strange. “pass”.

613. artec technologies AG

artec does soemthing in the areas of video and “multi media”. The company has around 2-3 mn in sales and barely makes a profit. Not sure if teh 8 mn EUR market cap is “fair” or not, but I’ll “pass”.

614. Medion AG

Medion AG was a “red hot” growth stock in the early 2000s when the company provided Aldi with PCs, notebooks and other tech gadgets. When that business shrank, Medion didn’t really find a similar opportunity.

These days, the 673 mn EUR market cap company still distributes various gadgets under its brand, however the comapny has been taken over by Lenovo which implemented a P&L transfer agreement that entitles shareholders only to a guaranteed dividend. “Pass”.

615. Innogy SE

Innogy is the better part of former utility giant RWE which got overtaken by E.on.I “played” Innogy as a special situation a few months ago but didn’t make any money on it. For me, the 24.3 bn company is a “pass”.

616. Design Hotels AG

Design Hotel is a 32.5 mn EUR market cap hotel consulting company that is majority owned by Starwood Hotels. As far as I understood, there is also a Domination and profit transfer agreement in place which only entitles shareholders to a guaranteed dividends. “pass”.

617. NanoFocus AG

Nanofocus is a 5 mn EUR market cap company that is active in optical measurement technology. The companies’ stock is on a long decline and business is not really doing well. Plus reports are rare and not transparent. “pass”.

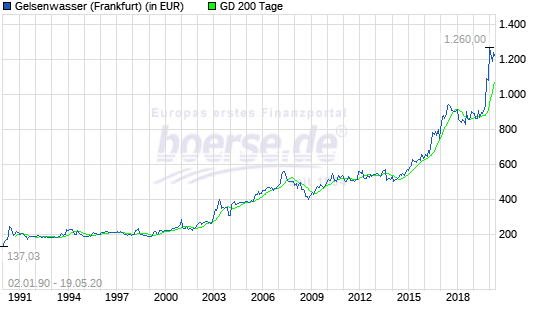

618. Gelsenwasser AG

Gelsenwasser is the largest regional water utility in Germany with a market cap of 4.2 bn EUR and is owned with 92% by the municipalities of Bochum and Dortmund. Looking at the chart I might need to drop my avoidance of Government owned stocks:

Operationally, although 2019 was a good year, the development in the last 5-6 years was OK but not that good to justify sich an increase in value. The company is conservatively financed and a good proof that local utility business can be profitable, but I am not sure why this should be worth 35x earnings. Maybe I am missing something but it is a “pass”.

619.Value Management & Research AG

VMR is a 7,5 mn EUR market cap with some Fintech participations. The first impression is that this is nothing special. “Pass”.

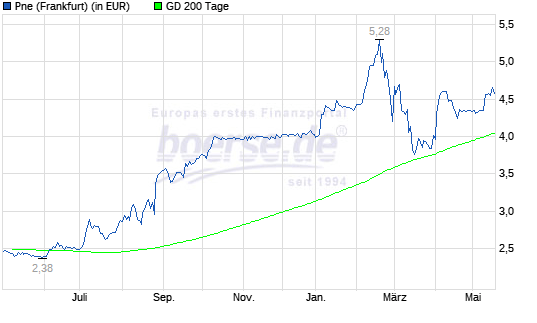

620. PNE Wind AG

PNE is a 357 mn EUR Windpark developer which I had covered briefly as special situation. Morgan Stanley did make a bid for 4 ER per share put only recieved 40% of the shares. The Covid-19 crisis had only a short impact on the share price:

Looking back it would have been a good “pseical situation” investment. Going forward I believe that the upside is limited. “Pass”.

621. TUI AG

TUI, the 1.93 bn EUR market cap company is clearly, together with Lufthansa, the company being hit hardest by Covid-19 in the German Mid/Large Cap space.

The stock price somehow indicates “rock bottom”:

On the other hand, TUI clearly is in existential problems. TUI is clearly one of these companies that not just have “a bad quarter or two”. Already the 6 months up to March with only one month of “full Covid” created an additional loss of -1 ER per share which is similar to the max EPS per year in the last few years and net debt has increased dramatically from -1,9 bn to -4,9bn.

For me this is clearly “too hard”. Maybe they survive and current prices represent a bargain but I would prefer less capital intensive models in travel. “pass”.

622. U.C.A. Aktiengesellschaft

UCA is a 10 mn EUR market cap Holding / advisory company that invests somehow in VC like companies. It looks pretty much like a one man show with 60% of the shares owned by the CEO and another family. Reporting is surprisingly transparent However is does not look very successful, as the company didn’t manage to increase the NAV over the last few years. “Pass”.

623. Pongs & Zahn AG

Insolvent 0.3 mn market cap Zombie. “Pass”.

624. Travel24.com

Travel24.com is a 3 mn EUR market cap online travel company. The company made operating losses even before Covid-19, no no real reason for me to look into this. “Pass”.

625. artnet AG

artnet AG is a 20 mn EUR market cap online art auctioning service with a colorful history. IPOed into the dot.com boom, since then the company showed little structural growth despite having potentially interesting “assets” such as a pricing database etc.

Competitor Weng Fine Art bought shares last years and is now the second largest shareholder after the founder. However, art auctions are not my circle of competence and the stock doesn’t look interesting enough to dig into. “Pass”.

Besten Dank für Deine Arbeit und Deine Website. Darf ich fragen, wie Du bei so einer Übersicht vorgehst? Bloomberg Kennziffern und die dann als Kennzahl heranziehen beziehungsweise zueinander stellen? Oder nimmst Du die Bilanzen der Firmen und errechnest die Zahlen selbst? Vielen Dank und entschuldige die fast indiskrete Frage.

Mangels Zugang zu Bloomberg errechne ich alles selber.

Vielen Dank für Deine Antwort.Wenn ich noch anfügen darf, mich, als nicht fundamental orientierter Investor, interessiert sehr das “wie”. Also der Analyseprozess. Etwa wie viele Jahre schaust Du in einer ersten Einschätzung zurück und wieviele dann vor einem Kaufentscheid? Gewichtest Du bei bestimmten Branchen Kennzahlen unterschiedlich? Welche Konstellation löst eine Investition aus und solche Themen. Eventuell würde ein Artikel in diese Richtung auch andere Leser Deines Blogs interessieren.

Ehrlich gesagt lege ich immer weniger Gewicht auf die Analyse der Vergangenheit. Das ist ein “Nice to have” aber bei weitem nicht ausreichend. Für mich ist es mittlerweile sehr viel wichtiger das Geschäftsmodell zu verstehen und die Motivation der handelnden Personen.

Mittlerweile sind soviele Branchen einem strukturellen Wandel unterworfen dass der Blick in den Rückspiegel nur einen sehr bedingten Mehrwert bringt, insbesondere bei fast allen Unternehmen die “Optisch” billig aussehen.

really appreciate this series and your work in general! thanks a lot

Reg 609: Uniper

Fortum owns 70% of Uniper not of EOn.

I finally sold my tiny legacy position