All German Shares Part 29 (Nr. 626-650)

Another week, another 25 randomly selected German shares. This time, I only found 3 of them to be interesting, however one stock became the biggest position in my German basket yet.

626.Pommersche Provinzial-Zuckersiederei AG

Pommersche is a 2.3 mn market cap company that is very illiquid and only releases very intransparent information. “Pass”.

627. Netfonds AG

Netfonds AG is a 63 mn EUR market cap company that could describe itself as a “Fintech” if they wanted. The company listed directly (no IPO) in 2018 and at first struggled:

The company has a somehow similar business model to JDC which I already added to my “German Basket”. Whereas JDC mostly focuses on back office solutions for insurance brokers, Netfonds also offers solutions for investment and wealth advisors. This is not yet a big market in Germany but is growing.

Netfonds has been growing at a pace of 15% p.a. over the last few years. Profitability looks low, with stated EBITDA margins in the low single digits, but if they would apply “fintech” measures and split between GMV and “net sales”, hings look much better. I also liked their 2019 annual report very much where they nicely explain their business model. At the current valuation, Netfonds trades north of 25xEV/EBITDA (2019), but I think that EBITDA can grow quicker than top line and that they have some runway for growth.

Other positives are that the founder still runs the company and the founders (incl. family) own more than 50%. By coincidence, just today the highly recommended Blog “Preis und Wert” released a detailed write-up on Netfonds (German), nicely explaining the business.

Therefore I do not only “watch” Netfonds but actually initiate a 2,5% position for my German basket at around 29,80 EUR/share. I will follow up with a more detailed post soon.

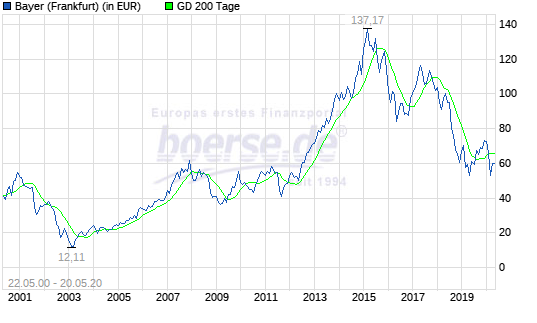

628. Bayer AG

Bayer, a 58 bn EUR market cap company, is one of the big traditional chemical/pharmaceutical companies of Germany with a long, sometimes controversial, but overall successful history.

The long upward trend was stopped by the current CEO and a the very controversial acquisition of Monsanto in 2016:

At the time of writing, Bayer just gained 8% as a settlement for the Monsanto litigation seems to be in reach. The company had a good start into 2020 with EPS up ~10% yoy driven mainly by Crop Science. The 32 bn net debt clearly is an issue-

Bayer had to go through a lot of self-inflicted pain but to me it looks like that they might be only underprportionally effected by Covid-19. Therefore Bayer is a candidate to “watch”.

629. Wasgau Produktions & Handels AG

Wasgua is a 115 mn EUR market cap regional grocery retailer and whole seller. The company was near bancruptcy in the early 2000s but then performed quite well:

The free float is relatively small, the biggest shareholder with 51% is a holding company where grocery giant Rewe is the controlling shareholder, but 25% also belong to competitor Edeka.

The big increase in 2017 seems to have been driven by rumours of a delisting/offer to minorities that didn’t happen. Technically the company looks quite expensive these days. MAybe it could be a real estate play but I’ll “pass”.

630. Wallstreet Online AG

WO is one of the oldest investor communities in Germany with a 95 mn EUR market cap. I used to read and write there a lot some 10+ years ago as it was the best platform for German small cap. Over time however, the quality decreased in my opinion and the interface became almost unbearable.

The stock chart looks “Interesting”:

So after the GFC, the stock did nothing for 8 years or so before exploding by 20-25 times in 2017.

This seems to be a reflection on a change in strategy from 2018 on when WO started to acquire other portals and even move into fund distribution and online brokerage. I think this alos explains the quick bounce back after the Covid-19 crisis.

Based on their H1 2019 numbers, the business seem to do quite well, decent growth and quite high profitability and the big move seems to be the entry into the brokerage market. The company is majority owned by the founder Andre Kolbinger who bought back the shares from Springer after the GFC.

Despite my dislike of the W:O portal, the company is one to “watch”.

631. Solvesta AG

Insolvent zombie stock. “Pass”.

632. Beiersdorf AG

Beiersdorf is a 29 bn EUR market cap company that is mostly famous for its iconic “Nivea” skin care brand plus the “Tesa” brand. The company has been on a long term growth path, but I always considered it as “too expensive”:

However in the last 4 years or so the stock price pretty much stagnated. In Q1 2020 sales actually declined by around -4% indicating that Beiersdorf is not immune to COvid-19.

But even in 2019, results already stagnated which is not good for a company trading at a P/E of around 30. As the company is majority owned by the Billionaire Herz family (Tchibo), there wil lbe no activist investors pushing the company to grow more.

For the time being, despite being a good company with great products, I’ll “Pass”.

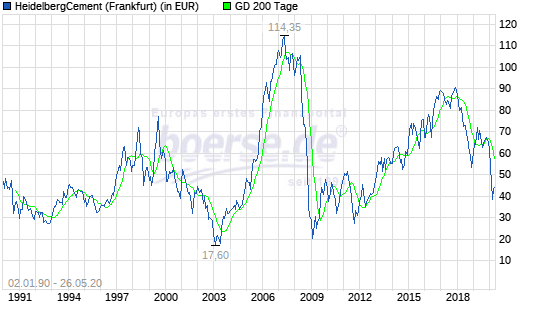

633. HeidelbergCement AG

Heidelberg Cement is one of the big global player in the cement market. After a “Near death” experience following the GFC, inflicted by expensive M&A transactions and high debt, the company has stabilized. However a look to the stock chart shows that long term, little value has been created for shareholders:

It rather seem to be a stock where one needs to time the cycles coreectly in order to make money. Structurally, the business has some issues due to the CO2 footprint, on the other hand, with a P/E of 8 the stock looks cheap. However a “pass” for me.

634. Delignit AG

Delignit AG is a 33 mn EUR market cap stock that went public in 2007. The company is a subsidiary of listed “PE” company MBB. The stock has seen better times:

The company specializes in wood based chemical products predominantly to the automobile sector. Although the company managed to grow top line by almost 10% in 2019, bottom line declined by -50%. Overall, the company doesn’t look interesting to me. “Pass”.

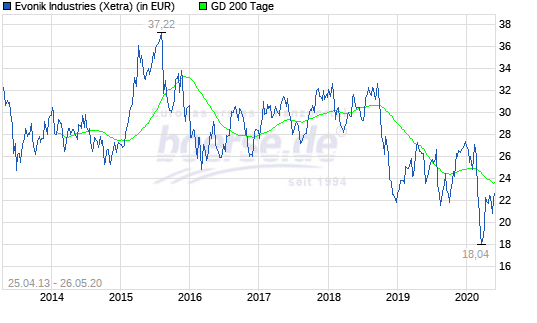

635. Evonik AG

Evonik is an interesting company. The 10.6 bn market cap company was one of the biggest IPOs in Germany ever in 2013. The specialty chemicals company had been created from the remains of the former coal monopoly company RAG. 59% of Evonik are owned by the RAG foundation which needs to manage the long term liabilities of the coal mining operations.

Looking at the chart, it is clear that the IPO was not a big success

The year before 2019, Evonil traded more like a bond than a stock for whatever reason.

The problem is clearly that EBIT in 219 is ~10% lower than it was in 2013. Net debt has increased since then despite a sale of a significant business in 2019. The company has a signifcant pension liability. All in all nothing to see, “pass”.

636. Deutsche Börse AG

Deutsche Börse is as its name says the company running most German exchanges. The company has a market cap of 28,5 bn EUR. As a quasi monoplist, the company enjoys great margins with EBITDA magrins of ~58%. The biggest profit pools are however not the stock exchanges but the mandatory derivative clearing and securities clearing where Deutsche Börse is one of the dominating European players.

Although the company botched a merger with LSE, the stock price has done quite well and recovered quickly from the Covid 19 crisis to a recent ATH which is very different to what happened after the GFC:

Compared to other “High quality” business models, the 25x PE ratio doesn’t look too expensive. However I do not understand enough of this business, therfore I’ll “Pass”.

637. Signature AG

1.4 mn market cap company with frequent name changes. “Pass”.

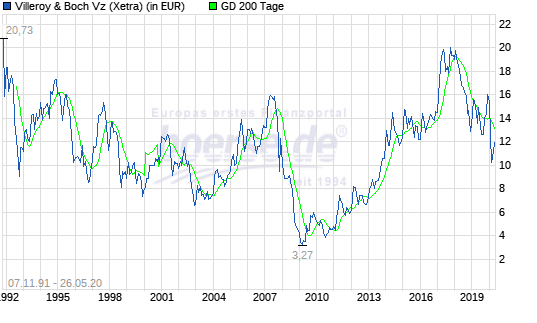

638. Villeroy & Boch AG

Villeroy & Boch is a 330 mn market cap company with a long history active in ceramic tableware and bathroom equipment.

The long term stock chart shows that not much value has been created as luxury table ware is clearly not a growth industry:

In 2019, top line decreased slightly, however profits more than doubled. What happened ? This increase was driven by a sale of real estate which clearly is of “Non recurring” character. The traded shares are nonvoting shares, all voting shares belong to the heirs of the founding family. The company has a rather large pension liability and the business is quite capital intensive. overall for me a “pass”.

639. Ekotechnika AG

Ekotechnika is a 22mn market cap company that makes its money by selling agricultural equipment(Tractors etc.) in Russia.

The company seems to be the exclusive partner for John Deere in Russia. On paper the company looks super cheap, however the “IPO” in 2015 was a result of a debt restructuring.

One of my mental models is to stay away from everything that has to do with Russia, so “pass”.

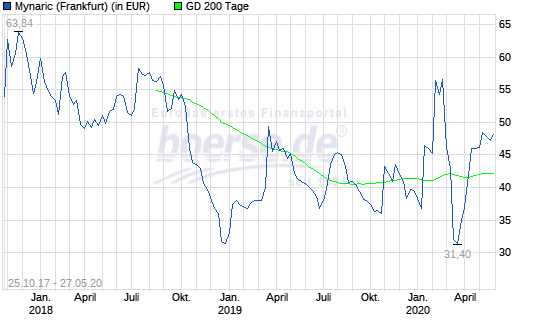

640. Mynaric AG

Mynaric is another company I never heard about, despite haveing a 153 mn EUR market cap. The company IPOed in 2017 at a price of 54 EUR/Share but struggled to keep that level since then:

Myanic develops laser communciation for (military) aircraft and satellites, which sound quite High-tech. This sounds great, but unfortunately, the company showed only 400k in sales in 2019 after 1.4 mn in 2018. A lot of the costs are capitalized but the company still managed to lose 8 mn EUR in 2019 and burned ~2x that amount.

To compensate, the company raises capital frequently. The stock clearly has “venture character” but I cannot judge if what they do is interesting or not, therefore I’ll “pass”.

641. Brilliant AG

Brilliant is a 15 mn EUR market cap company producing lighting fixtures for interior and exterior purposes. 85% of the shares are owned by UK based National Lighting Company Ltd, the stock is thinly traded. Interestingly the company had to issue a profit warning already before Covid-19 hit them. “pass”.

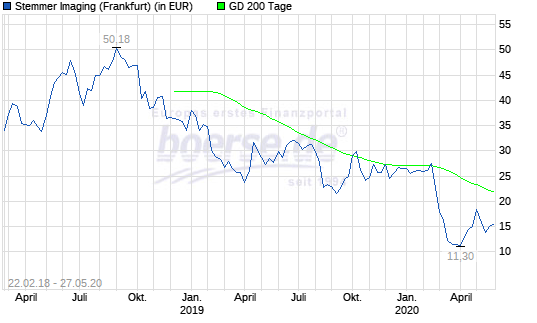

642. Stemmer Imaging AG

Stemmer is a 100 mn market cap company that went public in 2018. As many IPOs from that period, the stock has been struggling since then:

The company is active in “digital imaging” and “smart data” whatever that means. The accounts are hard to read because for whatever reason they had a shortened financial year in 2019. For me this doesn’t look very inspiring, “pass”.

643. Allerthal-Werke AG

Allerthal is a 23.5 mn EUR holding company that is active in the German small cap market and especially in Squeeze-out situations. Unfortunately, the reporting is quite intransparent and the company is run by a single person. “pass”-

644. Dierig Holding AG

Dierig Holding is a 53 mn ER market cap company that has its roots in textile manufacturing. These days the company owns a shrinking textile segment and a growing property business. The property portfolio is concentrated around the company headquarters in Augsburg. The textile business had a bad year in 2019 with significant write offs. The company is majority owned (70%) and run by the Dierig family. With more time this could maybe be an interesting target to look for “value”, but at the moment it is a “pass”.

645. Mic AG

Mic AG is a 2,7 mn EUR market cap loss making holding company that recently had to do a capital increase. “pass”.

646. Bechtle AG

Bechtle is a 6.6 bn EUR market cap IT service company with a greattrack record of growth as we can see in the stock chart:

Initially the stock got hammered by COvid-19 but then recovered quickly to new ATH. The company has doubled its sales from 2015-2019 as well as profits. On the minus side, margins are quite low (EBIT Margin ~4,5%) but stable. The Schick family owns 35% of the company but doesn’t have any active role.

A significant part of the growth seems to have come from M&A as Bechtle was rolling up smaller player in the IT service business. Another minus is cash conversion which is not so good. The final minus is however the valuation. At a current PE of >35, a lot of future growth seems to be priced in already. Therefore I’ll “pass”.

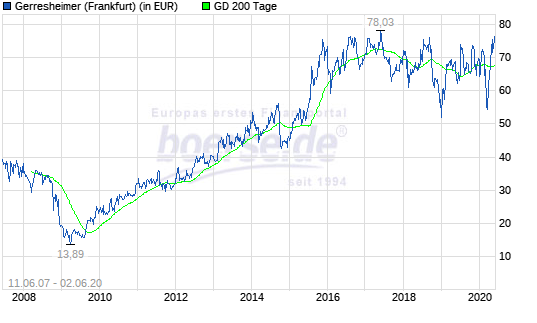

647. Gerresheimer AG

Gerresheimer is a 2.36 bn EUR market cap company that produces specialty glass/plastics packaging. The stock looks quite boring and is more or less flat since a few years:

As a company that had been owned by a PE bfore its IPO, it is no surprise that they employ some leverage. Margins and Returns on capital look quite OK on an adjusted basis, but the company shows hardly any growth for the last 4-5 years which explains the stagnating share price.

On a non-adjusted basis, things look actually quite bad. Overall there is nothng at first sight that makes this attractive, therefore I’ll “pass”.

648. Stada AG

Stada, a pharmaceutical company, is a company that was subject to one of the most spectacular “activist” campaigns in Germany. At the end of the day, the CEo who ran the company like its own without owning shares was kicked out and PEs took over the majority of the shares after a bidding contest.

. The “Lucky winners” were Bain and Cinven. I actually “played” that special situation as well, however selling much to early at around 65 EZR per share.

Stada is a painful reminder that timing is not exactly my strength. These days, Bain and CInven have establishe a domination and p&L transfer agreement, so the remaining Stada sahreholders are only entitled to a guaranteed dividend of 3,54EUR/share. “Pass”.

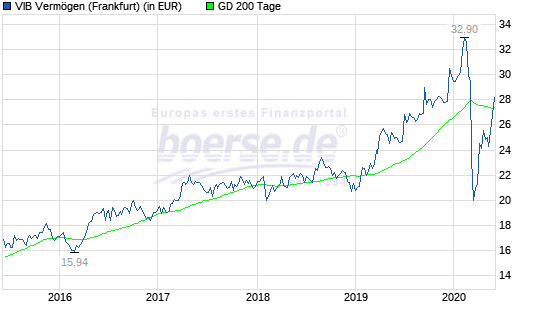

649. VIB Vermögen AG

VIB Vermögen is one of the more interesting real estate companies that are listed on the GErman Exchanges. The company specializes on logistics projects and has only little exposure to more problematic sectors.

With 760 mn EUR market cap, the company is actually not that small anymore and has offered its shareholders a nice long term growth story as we can see in the chart:

The stock has been hit hard by Covid-19 but recovered quickly as the market seems to assume little impact on their portfolio. Interestingly the market pays a premium on top of their disclosed EPRA NAV of 22,68 EUR per share at the end of Q1.

However, as I am not a fan of normal listed Real Estate in general, I will “pass” in VIB.

650. Borussia Dortmund GmbH & Co. Kommanditgesellschaft auf Aktien

The Business model of Borussia Dortmund doesn’t need a lot of explanation: It is basically Germany’s second famous football club after Bayern Munich.

As a (medium intense) football fan one has to concede that Dortmund, despite losing out to Bayern in most of the last years has done a pretty good job to attract talents and play attractive football.

In the past, Dortmund had big issues with debt and at one point in time had to be bailed out by Bayern Muenchen with a loan but hese times seem to be over. The stock has done very well over the last few years:

Even Covid-19 didn’t really kill the stock. At 600 mn EUR market cap, the club doesn’t seem to be extremely expensive compared for instance with the 3 bn market cap of Manchester United, however I am not 100% sure how football clubs really want to earn money in the long term as they are always depending on expensive individuals.

I know that some very smart investors are quite bullish on sports rights in general, but I don’t know enough here so I’ll “pass”.

Irgendwie kommt mir die Netfondsbilanz 2019 spanisch vor: Die als Umlaufvermögen angegebenen 27.911 T€ kann ich rechnerisch nicht nachvollziehen. Auch sonst wirkt die Bilanz schlampig erstellt. Tausenderpunkte fehlen teilweise und die Summe der immateriellen Vermögensgegenstände ist irreführend fett gedruckt.

In der Tat scheint die Summe beim Umlaufvermögen 2019 nicht die Grundstücke einzubeziehen. Die Gesamtsumme Aktiva stimmt aber.

Für mich ist das eine etwas größere “Beobachtungsposition”. Das Geschäft und die handelnden Personen finde ich gut, aber beim Reporting würde in der Tat etwas mehr Sorgfalt nicht schaden.

Netfonds with immpressive 6M numbers:

Click to access Netfonds-AG-Halbjahreszahlen-2020.pdf

It looks like COvid-19 did not happen for them.

I think one of the issue is that “Listed Germany” is pretty much all “old economy” or crap. There is little in between. Also, the good ones seem to be fairly priced. This can change however, so let’s not be to pessimistic 😉

Your review so far seems to indicate that the German stock market is not the most exciting one. Maybe because stock market rules in DE are not fit for modern financial markets, as you (&others) mentioned already. Big part of it due to cronyism that we criticise on Trump.

Problem is that other European stock markets are worst (PIGS are the flagship of cronyism & corruption).

Your review is great by all means in exposing this issue. So that when we invest in DE (or EU) we are aware of all things behind.