Special Situation Updates: Actelion/Idorsia, Gagfah, SAPEC & Stada

A lot has happened over the last few weeks for my 4 largest special situation investments:

Actelion / Idorsia

The original Actelion idea was very simple: Buy an M&A target at a small discount which is relatively safe and get something (the Idorsia spin-off) extra which no one seemed to have noticed.

Although the case played out exactly as I thought and Idorsia even seems to be worth more than I assumed, I only made around +4% on it. Not bad for around 5 months but not great either.

Looking back I think I made 3 mistakes:

- I bought the first “batch” too early. As in many similar cases, the stock price dropped after the first announcement when some rumors came up that the deal could blow up because of a problem in France. It’s interesting that such rumors surface almost always. Although I am not a conspiracy theorist, I don’t think that this is pure coincidence. There was a high short interest in the stock before the announcements, so maybe short sellers try this to cover the stock more cheaply. Or specialist M&A arbitrage funds use this “instruments” to gain a cheap entry point.

- I sold Idorsia maybe too early. at CHF 15. As my defense I could argue that no one knows how to value this because at the moment, the 3 analysts covering the stock have price targets of 7,50 CHF, 12 CHF and 20 CHF. Interestingly the whole Actelion story doesn’t put a great light on the “professional” analysts. First, they did not attach any value to the spin-off and now they cannot agree what it’s worth.

- I didn’t hedge the USD. Back then I argued that I have no material FX exposure and I can therefore leave it unhedged. However as I compare myself against a EUR benchmark, I think I should have hedged FX exposures with a relatively short term fixed maturity in the future as there is no expected return for the risk I am taking. In this case the USD move cost me almost -5% which trasnformed the result from a potentially very good onr into an ok return.

Gagfah

2 years after my initial write-up, the Gagfah case seems now be come to an end. I could not attend the annual meeting but from what I heard, the proposal (0,57 Gagfah shares per Vonovia share) is more or less a done deal.

It clearly undervalues Gagfah by a wide margin (NAV would be rather at around 24 EUR or so) but from what I have heard there is not a lot that can be done about it. Other than in a Squeeze-out, the cross border merger seems to be a hole in the Luxembourg law and any challenge will require a lot of legal effort with a very uncertain outcome.

Looking back I could have sold at 22 EUR in late April to mid may but in any case overall it was a very nice transaction. I bought 60% of the position at ~13,70 EUR 2 years ago and the remaining 40% at 19,70 EUR.

The only question is now if one should wait until one actually gets Vonovia shares or not. In a theoretical case that someone sues successfully a few years down the road, there might be a chance for more if one actually goes thorough the merger process. However for this to work all Gagfah shareholders should be the beneficiary of a positive verdict. The chance for this is rather low.

SAPEC

I have commented already a lot in the original post and the follow-up post. The investment was ultimately spectacularly succesful although it was kind of roller coaster ride, Especially when the reserved everything they could in their 2016 numbers, there was a chance that the outcome would be a lot lower than initially thought.

However then in the end they surprised everyone with the 60 EUR bid which moved the outcome close to what I hoped for in the beginning:

After the deal (which is very likely in my opinion), the company will have 230 EUR cash plus any other assets. The expected distribution might help to unlock some of the value. I think it would not be unreasonable that the stock price will be at ~200 EUR before the distribution, an upside of almost 50%.

In my “Virtual” portfolio I will book the claim towards the Belgium fiscal authority as a “receivable” which I will turn into available cash once I get the rebate in my private portfolio.

In the SAPEC case I made no obvious mistakes with the only exception that I should have bought more. I actually tried to buy even more the day before the dividend payment but by then it was already too late as the stock was suspended. On the positive side I did increase my position into an increasing share price once things became more certain which I wouldn’t have done a few years ago. On the day before the payment, SAPEC became briefly my largest position with ~10% of the portfolio.

I will strat to sell my position ast current prices in order to neutralize the taxes I have to pay on the other “exits” like Gagfah and to recoup taxes I have paid

Stada

Last but not least a brief recap on Stada. As I mentioned in the original post, Stada was never any easy case. This is what I wrote back then and which turned out to be very true:

One word of caution here: Stada is a relatively well-known name and the story is well published. So one should not assume that this is “easy” money. Rather this is a case of “swimming with the sharks” as one can assume that many professional players look into this and the discount really includes some kind of risk. I still think it is worth the risk but one should be aware that more “hiccups” are very likely. The price of Stada will most likely not go up in a straight line to 58,70 but go up and down depending on many rumours. If you can’t stand this (like some readers in the Actelion case), don’t do it.

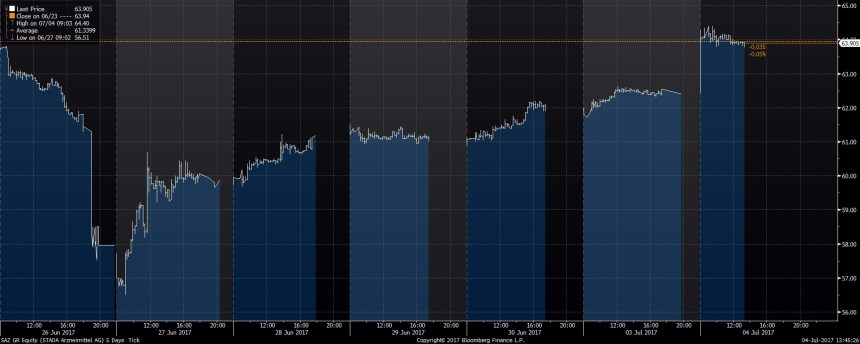

Luckily I think I was (mostly) mentally prepared for this. Even more lucky, I was on vacation when finally the news hit the wires that the bid failed so I could not do much (for my own safety I cannot trade via mobile phone). Some people obviously were not so well prepared as this chart shows:

Those who pulled the trigger fastest lost the most, selling at around 57-58 EUR. So much for “the faster the better….”.

So what happened ? I read a lot of interpretations, among others that index funds played a role etc. However my interpretation is slightly different (and maybe wrong, who knows ?).

It is pretty clear that Bain and Cinven want the deal. So why didn’t shareholders sell ? The issue in my opinion is the German mechanism for determining the price of the shares in an ultimate squeeze out.

Bain and Cinven will clearly try to squeeze out all minorities as quickly as possible in order to be able to do whatever they plan without asking minorities.

A Squeeze out in Germany roughly works like this: A company offers a price based on an average price before the squeeze out (Trailing x day average). This will be then used a s the price for pushing out minorities. Minorities then have the chance to go to court and ask for a verification of the price. The court will ask for a “3rd party fair valuation” based on more or less standardized valuation models. Those models often lead to a higher price and shareholders who have been squeezed out will get a compensation payout. In the past those “top ups” where sometimes quite significant.

With regard to the Stada offer there are 2 big issues for Stada shareholders (and the potential buyers):

- In order to participate in the Squeeze out procedure and any possible payout, one needs to keep the shares. Those shares which are tendered in the initial buy out offer to not participate in the ultimate squeeze out proceeds

- Squeeze out valuation: I have briefly discussed the case with a “squeeze out specialist”. Based on his remarks (and without verification from my side), the expected squeeze out price might be significantly higher than the offer take over price (mid to high 70ies vs 66 EUR). This is partly due to the surprising increased company guidance from early March. A squeeze out valuation always only refers to company plans, no matter how overoptimistic they might be.

So the current situation clearly look like an invitation for more adventurous hedge funds and specialists to “hold out” against the take over offer and either demand a higher offer or wait for the squeeze out. Bain and Cinven clearly could lower the acceptance threshold but then the overall purchase price would increase if they have to pay the higher squeeze out price to more shareholders.

Clearly this is only another theory but today’s firing of the CEO and CFO could hint that the buyers are clearly annoyed by all this.

Looking back, I think I also made 2 mistakes since I started the position:

- I should have sold when the rumour on a higher bid from the CHinese came up. As I mentioned in the comments, I found the rumour not to be trust worthy because it is relatively clear that Chinese buyers these days have issue in closing big deals.

- I should have sold when the initial activist AOC surprisingly sold their position early in mid June. I was surprised when they sold at a time when the price was below 65 EUR, leaving some (easy) money on the table. It felt somehow like you are in a club dancing and the DJ leaves early. This is something to remember in the future that those guys might not wait until the end.

Where does that leave us with the investment itself ?

I think the current situation is clearly more tricky than back in March. The situation reminds me of a typical “Prisoner’s dilemma” situation and I am not really able to get an idea how the odds look like at the moment. The price of the stock is higher than I initially thought. I do not think that there is much upside with regard to a (likely) new offer. Maybe one EUR more but not that much.

I haven’t made up my mind yet but I think I might start to sell rather sooner than later and then maybe go again for the Squeeze out once the offer goes through.

But again please remind: This is not investment advice. DO YOUR OWN RESEARCH !!!

Domination agreement with a 74.40 EUR compansation price announced and the share price is already >88 EUR.

For clarification, that’s for STADA. The legend gets confirmed…. timing….

Yesterday, full exit of CVonovia at around 34,6 EUR/sahre

Fuklly sold Stada, avg. price 65,25 EUR/share.

At Stada it will be close again. Get the popcorn ready…

Full exit of Sapec shares, on average at 59,10 EUR.

new stada offer at 66,25 EUR (+0,25 EUR). I am starting to sell now. This time I do not wait for the last 1%….

I also contemplated selling but I turned the last 1% into 3% by writing covered call options. I got 1.25 EUR per share with a strike price of 66 EUR (September expiration). If some crazy bidder comes around offering above 67.25 EUR, I will leave money on the table. Expected return is 3% (67.25/65.25-1) for little more than 2 months assuming it closes end of September. Of course, I have no downside protection other than reducing my entry price by the 1.25 EUR.

Smart idea. I damit that I am also a little bit nrevous because of the Elliott engagement. I try to stay away from them if possible.

Interesting: Elliott joins the Stada Party

http://www.manager-magazin.de/unternehmen/artikel/stada-hedgefonds-elliott-steigt-ein-a-1156330.html

I was expecting that the Idorsia share price would decline due to selling by funds, etc. Any thoughts on why, on the contrary, it went up 100% in the first two weeks? Was it completely incorrect to think it was an “unwanted unloved spinoff”? Also anyone know why it was priced at $10CHF at the onset (seemed low)? Thanks

The Actelion CEO (who is now the IDorsia CEO) has been buying massively Idorsia shares:

https://www.nzz.ch/wirtschaft/hohe-beteiligung-an-idorsia-was-plant-das-ehepaar-clozel-ld.1304368

I guesss many people interpret this very positively.

Speaking of special situations:

I am currently researching the 28$ tender offer for the Qiwi plc shares/ADS (current price 23,9$) – looks very interesting on first sight. Have you looked into that one by chance?

#Liza,

one word of advice here: YOu should only invest into such situations if you full yunderstand the mechanics and the players involved and especially, why there is a discount. Based on a very quick research, the 28$ tender odder is not for 100% but for 55% only. So at the current stage it is not clear how much shareholders will be able to tender at that price which most likely explains the discount. On top of that you have the issue that the bidder is from Russia.

mmi

Another M&A emerging today is Axis Capital offer for Novae.

Thanks to your article I bought Idorsia shares after the spinoff (wish I had bought more and woken up at 3am NYC time when it first started trading…). Buying Actelion beforehand didn’t make sense to me given what a small percentage Idorsia was of the its parent.

“Buying Actelion beforehand didn’t make sense to me given what a small percentage Idorsia was of the its parent.” ….That’s exactly why Actelion was such a nice “special situation” 😉

Thx for the update and the lessons your are providing. How is your stance about Metro and it’s spinoff? Are sou interested?

I am watching 😉

I hope you will let us know, if you are investing. I got some Metro stocks and see a potential in the spin-off. It is far from a buy and hold business, but MediaSaturn and Metro should be worth more, if they are separated. From my research I am seeing a market for MediaSaturn. They improved their service and modernized their markets and structure.

Very satisfactory thoughts. Although over the long pull of arbitrage transactions, short term fx moves can’t be hedged in such a way that cumulative hedging costs (forward points) would be less than taking the hit unhedged, unless a currency pair is permanently impaired in one direction. In other words, these types of hedge, although funds claim them to be directionless, effectively involve taking a stance (i.e. direction).

I second that point.

Idorsia wurde in Schweizer Wirtschaftsmedien einmal in einem Artikel analysiert, worin Branchenanalysten die Wahrscheinlichkeit der momentanen Forschung analisierten, später marktreife Medikamente zu generieren. Diese waren im besten Fall bei 30 Prozent und die anderen darunter, wenn ich richtig erinnere. Was allerdings täglich vermeldet wurde, war die Beteiligungserhöhung von den Clozels. Von einem Einstieg Paul Singers habe ich auch etwas gelesen, allerdings alles von mir ungeprüft übermittelt, da ich nicht an dem Wert interessiert bin. Ich denke, das ist eine Art Goldgräberstimmung, welche durch den Erfolgsweg von Clozels bisheriger Lebensleistung auf die Zukunft von Idorsia prognostiziert wird.

30% Erfolgswahrscheinlichkeit multipliziert mit einem entsprechenden Marktpotential gibt schon einen ziemlich “satten” Erwartungswert.

Da mein Beitrag doch etwas ungenau war, habe ich den Artikel eben gesucht, hier der Link. Uebrigens, der Hedgefond war der von Paulson, nicht von Singer.https://www.nzz.ch/wirtschaft/nach-der-uebernahme-durch-jj-so-viel-wert-ist-das-actelion-baby-ld.143649

Seems like this (Clozels buy) is still a story in 2018

Mark Lampert (BVF Partners): Long Idorsia (IDIA-CH), spin-off from Actelion done in conjunction with Actelion’s sale to Johnson & Johnson. Founders/owners of co are exemplary scientists and business operators. Invested $525 million into Idorsia, more open market purchases recently. Insider purchases stand out as among biggest in industry. Thesis is to co-invest with the Clozels, the founders.

Read more: https://www.marketfolly.com/#ixzz5VDZlLX6w

I am new to your blog and Sapec. If you think it is worth 200 and trading at roughly 60 shouldn’t it be buy recognizing how illiquid it is buying stock looks challenging. Also, looks like it is being taken private. So if you purchase the shares now would the investor be a involved in a private company once the transaction closes.. Would appreciate your thoughts. Thanks.

Thanks for the comment but the stock price (and the offer) now at 60 EUR does not include the 150 EUR dividend paid a few days ago 😉

First of all nice article regarding Idorsia. Before the first trading day there was an article on cash.ch , which was written in a similar way: risk of selloff and in that case a massive buying opportunity. I also thought about that case and my conclusion is: the influence and intentions of the founder of Actelion werent accounted for that much. In hindsight it looks logical , but already while he negotated with J&J he showed his intentions : to repeat his success with Actelion from the scratch and to put more time in R&D instead of managing things. To protect this goal he bought many shares in the first days to reach a portion of Idorsia which put him in the position to be involved in every decision which regards a majority of shares. Your arcticle gave me the opportunity to take notice of that chance and i didnt thought it through to the end. Regarding contingent value rights Tobira/Allergan was an interesting example: if i remind it right after the takeover news Tobira didnt reached the full takeover price which gave you the opportunity to get real options for a real cheap price. I have to follow that example to get more knowledge of CRVs to take the next opportunity.