All Swiss Shares Part 3 – Nr. 21-30

Another week, another 10 randomly selected Swiss stocks. This time, two of them made it onto my watch list.

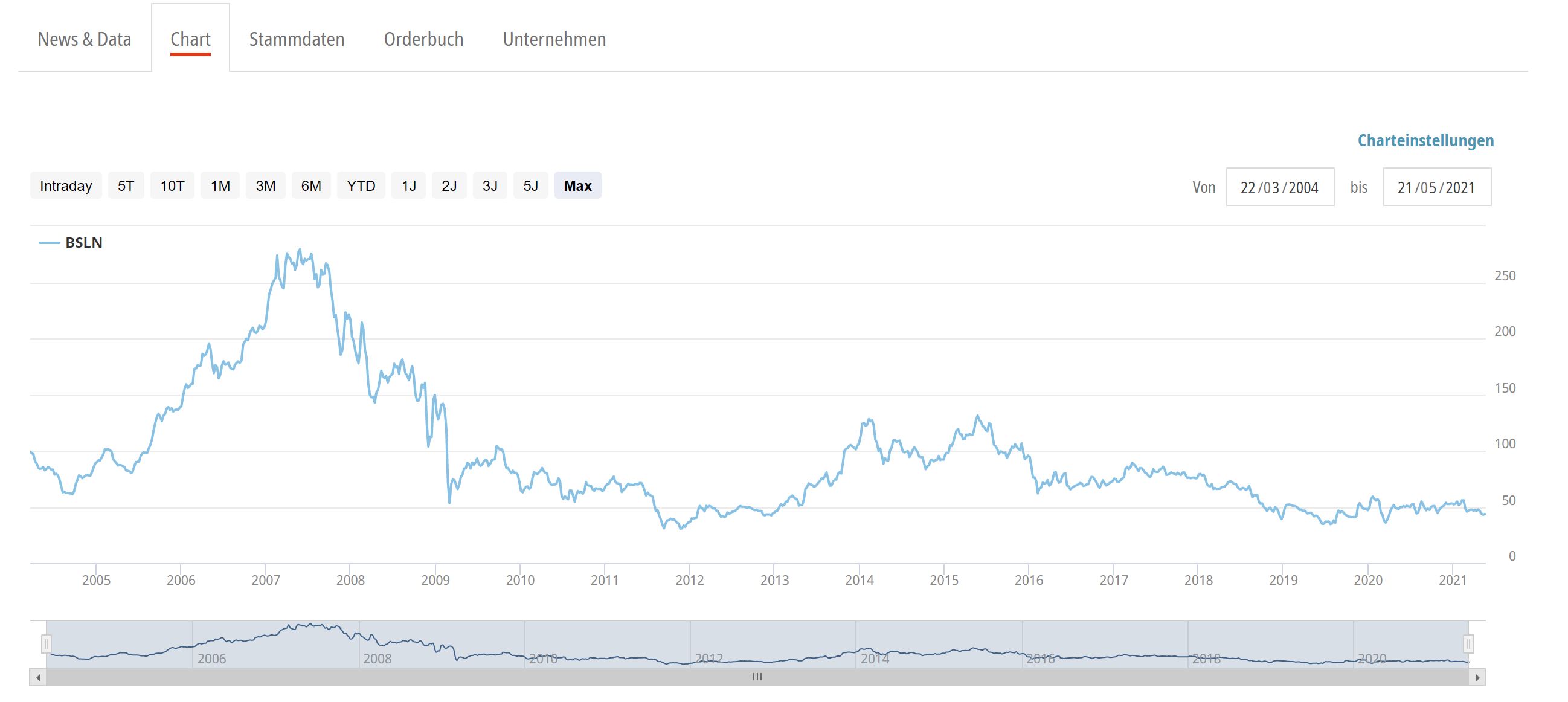

21. Basilea AG

Basilea AG is a 569 mn CHF “biopharma” company that was spun off in 2000 from Roche. Other than for instance Actelion, Basilea doesn’t seem to be a big success when looking at the share price:

According to their annual report, they do have two developed pharmaceuticals which create real revenue and allows them to almost break even. One of them is an “Antifungal” pill which could be interesting, however I have no way to judge the potential of a pill.

Currently, there is little observable growth and I am also not able to judge if the remaining pipeline is good or not. Therefore I’ll “pass”.

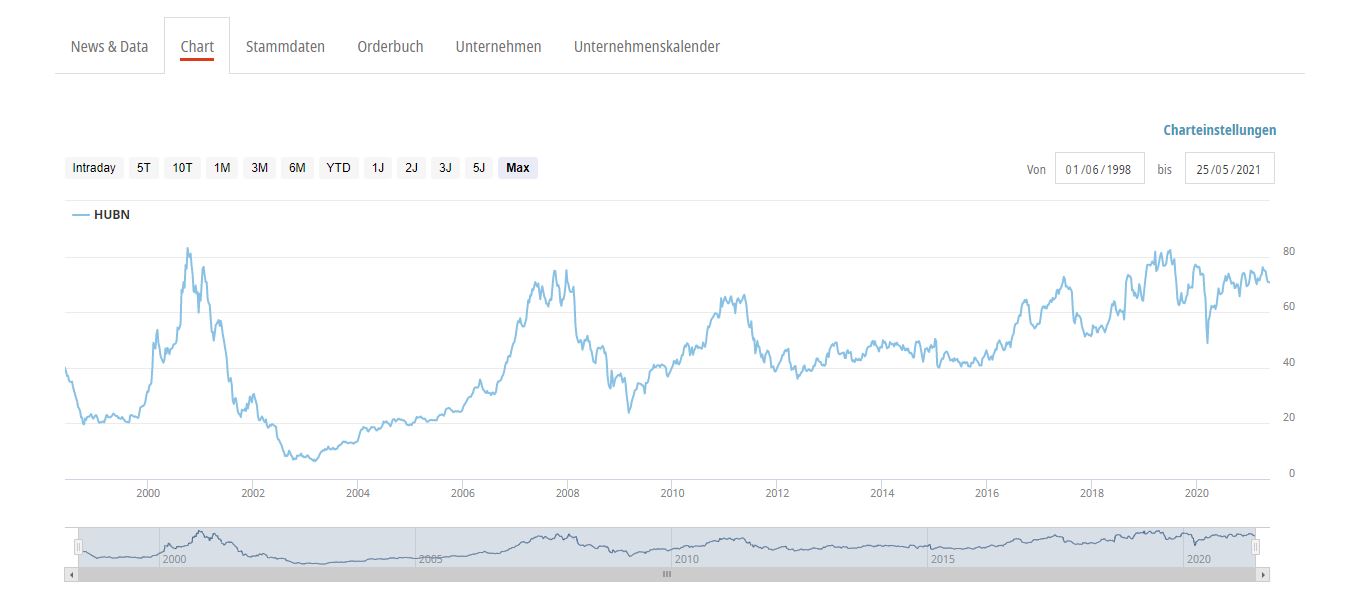

22. Huber + Suhner AG

Huber + Suhner is a 1,43 bn CHF market cap company that specializes in components for radar technology, fiber optics technology and a segment they call “low frequency”.

Business has suffered due to Covid 19 with sales down -11%, however they seem to have a good control on costs as net income only declined by -16%.

The company has significant net cash and has bought back shares in the past. The stock price has been volatile in the past but one can see a long term upwards trend since the early 2000s:

For 2021, the company envisages single digit growth and a a move back into their target EBIT margin corridor of 8-10%.

This is a unspectacular company that I want to learn more about if time allows, so I’ll put them on “watch”.

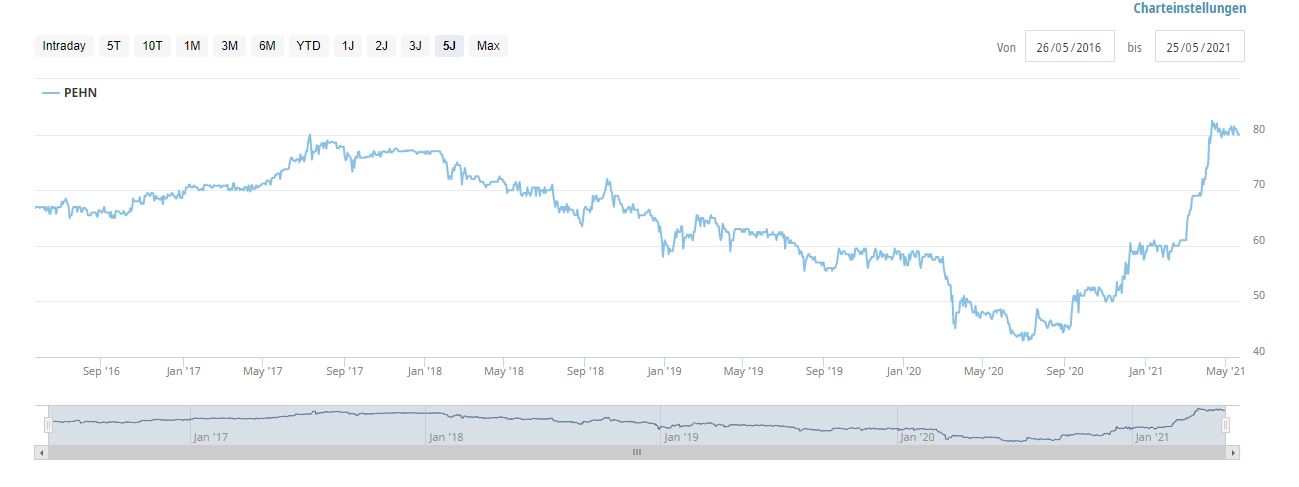

23. Private Equity Holding AG

Private Equity Holding AG is a 205mn CHF company that ture to its name invests in Private equity and Venture capital. According to the web site, the NAV per 30.04.2021 has been rported at 133 CHF which means that at currently 80 CHF, the stock trades at a discount.

The chart looks very interesting: A long decline from 2017 and then since a few months a relatively rapid increase in share price:

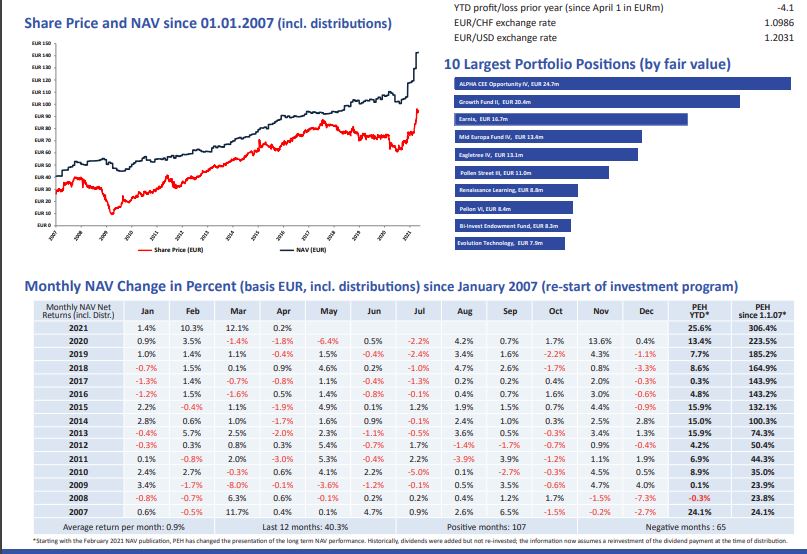

This seem to be driven by a corresponding increase in underlying NAV as the fact sheet indicates:

Nevertheless, investing into a listed, fund-of-fund PE vehicle does not make much sense for me, therefore I’ll “pass”.

24. Novartis AG

Novartis is one of the biggest global pharmaceutical companies with a market cap of 200 bn CHF. The company has not manged to grow a lot in the past few years and the stock price hasn’t done much over the last 5 years.

As I do not see how to get any “edge” on such a big company, I’ll just “pass”.

25. Airesis AG

Airesis is a small, 47 mn CHF company that is active in sports equipment, mainly under the brand “Le Coq Sportive”. The business was already loss making in 2019 and things did get worse in 2020. According to the annual report, the company is struggling for some time:

In addition, the company has negative equity and significant debt. As I am not interested in turn-around stories, I’ll “Pass”.

26. Lalique Group

Lalique Group is a 252 mn CHF market company that is active in the luxury area, comprising fragrances, interior design, Whiskey and other items. The company went public in 2018 and looking at the stock price little progress has been made.

Sales were hit hard by Covid-19 but seem to have recovered late in early 2021. Sales are very Europe centric and other than for instance the big guys like Richemont and LVMH they could not compensate with sales in China.

I do think that the luxury business requires some scale and that Lalique seems to be pretty far away from any kind of scale. Their target of 10% EBIT margin is quite low for a luxury player.

Compared to Richemont, I see very little reason to dig deeper here, therefore “pass”.

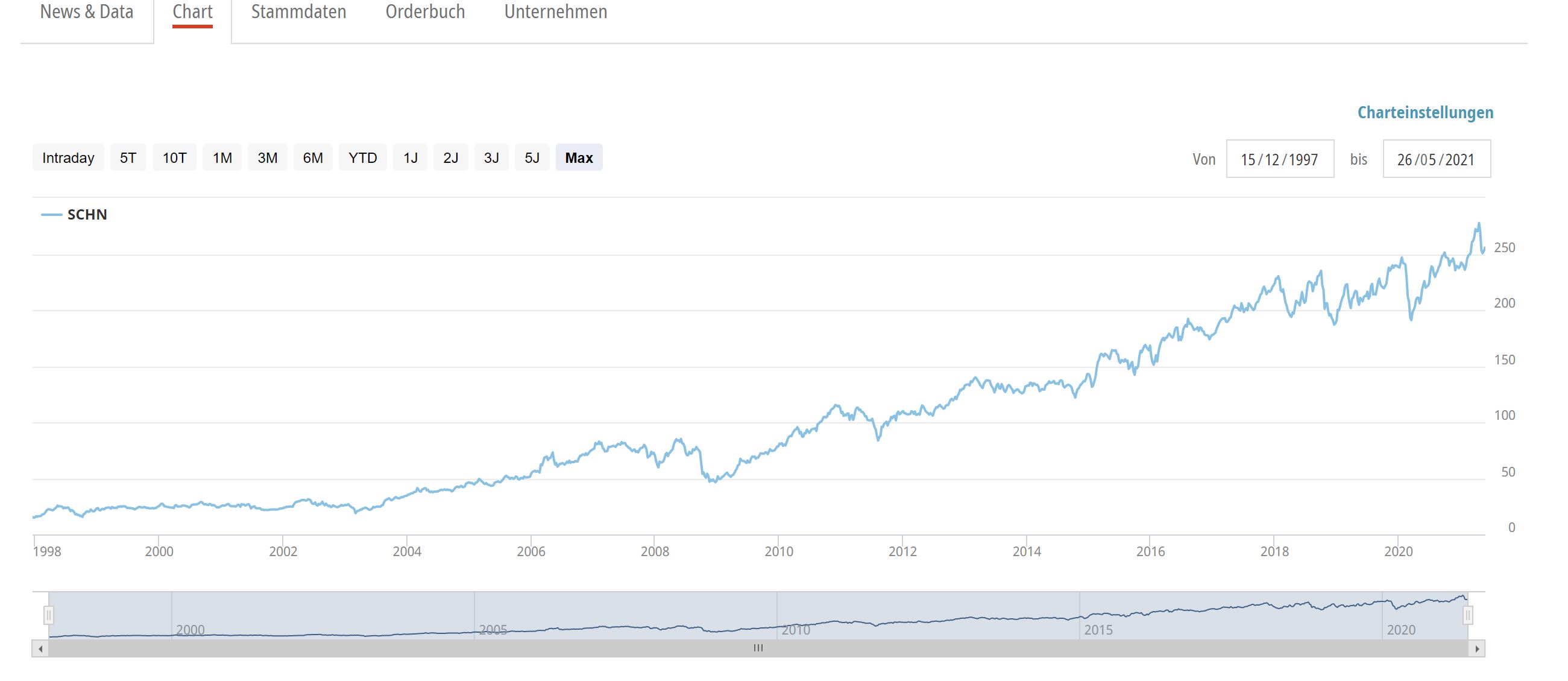

27. Schindler Holding

Schindler is a 28 bn CHF market cap company that is one of the leaders in elevators, escalators and miving walkways globally. Especially elevators have been a growth business for many years which is reflected inth elong term share price:

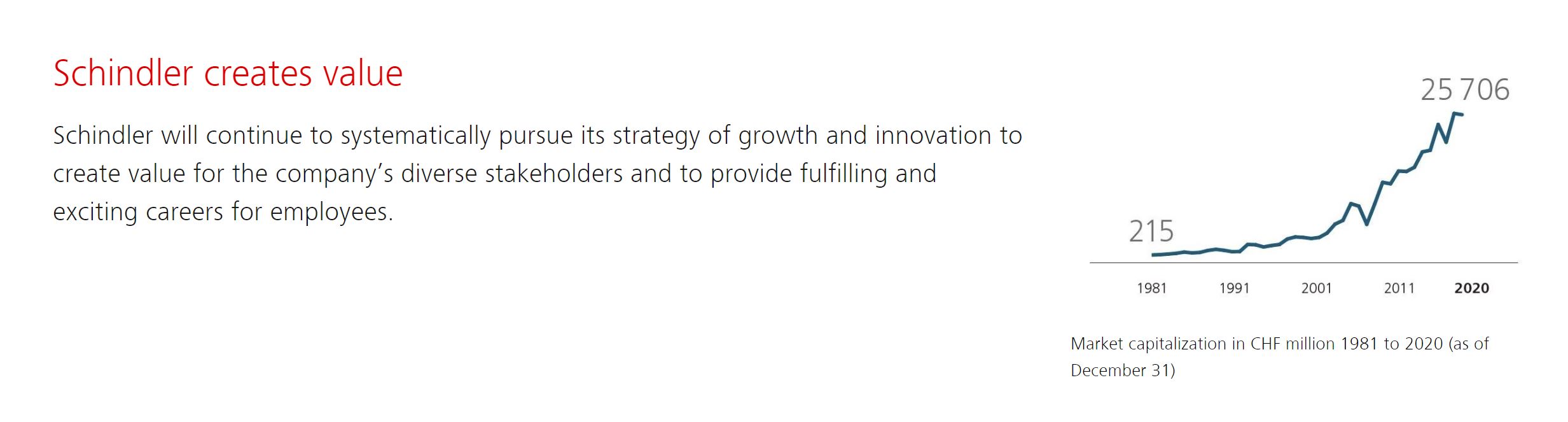

They have a great chart on their web site that they have increased their market cap by 100x since 1981:

Profitability is very solid for an engineering company, with EBIT margins in a range of 10-12%. ROEs have been historically between 25-30% p.a. which is remarkable for an unlevered company.

Unfortunately, all these qualities are reflected in a high valuation at around 28x peak earnings or ~30x 2021 earnings. Some years ago, I would be nervous above a P/E of 10, these days my threshold is at a P/E of 20. Maybe I need to move my threshold even more but so far a P/E of 30 is clearly outside my area of comfort even for a high quality company like Schindler. Therefore I have to “pass”.

28. Medacta AG

Medacta is a 2,5 bn CHF market cap “MedTech” company specialized in the design and production of innovative orthopaedic products and the development of minimal invasive surgical techniques for joint replacement, spine surgery and sports medicine.

The company was IPOed in 2019. The stock price has seen some volatility with a stron increase in the past few months above its IPO price:

The company managed to keep sales almost stable in 2020 depsite Covid with EBITDA margins of ~30% and an EBIT Margin of 16%. With a trailing P/E of 60, the stock is clearly expensive. As it is a still rather small company with 300 mn in sales, the question is clearly how much they can grow from here. The company plans to grow 10-15% in 2021.

70% of the shares are held by the founding Siccardi family, with a lot of Siccardis in the Board and executive team.

Although the stock looks very expensive, I will put them onto my “watch” list in order to learn more about the company if time allows.

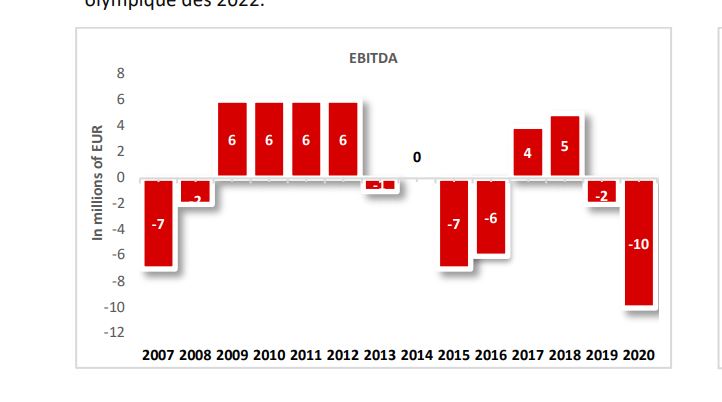

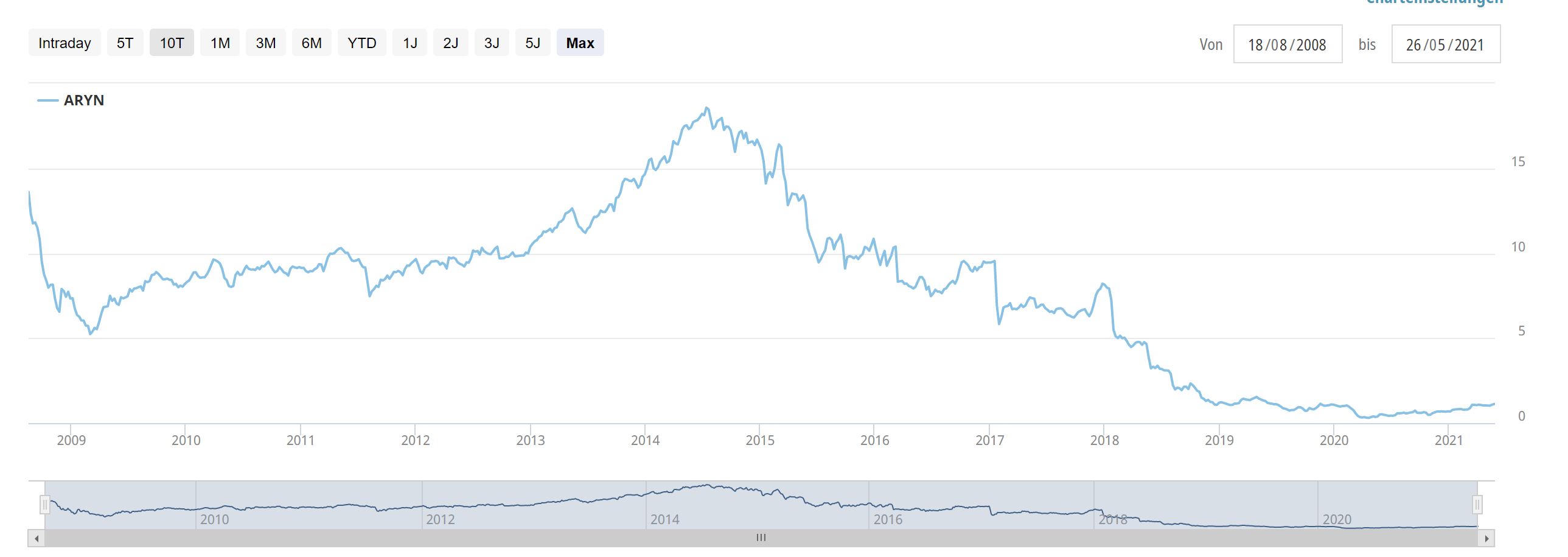

29. Aryzta AG

Aryzta is a 1.13 bn CHF market cap company that produces froen bakery items mostly for B2B use. The company has been struggling for some time, culminating in a big capital raise in 2018.

Business is still shrinking and the company employs significant leverage (4xEBITDA). They seem to have sold a large part of their north American activities. Long term, the company managed to destroy a siginficant amount of capital over the last 10 years:

As I do not consider myself a good turn around investor, I’ll “pass” on Aryzta.

As I do not consider myself a good turn around investor, I’ll “pass” on Aryzta.

30. Highlight Event & Entertainment AG

Highlight is a 236 mn CHF market company that is active in the movie/television business and in sports media. The company onws, among others the German film studio Constantin Film as well as Sport1, a sports chanel. The company made a loss in 2020 and in general, the stock did very little over the last 20 years with the exception of 2020 pre Covid:

The company is famous for complex relationships, among other with the German listed company Highlight Communications AG. As I am not an expert on media stocks, I’ll “pass”.

Aryzta is well known in the spanish investors community because some star value investor (Paramés) had invested in it (as much as 10% of his fund), and lost 90% on this value so far.

I never see any competitive advantage in this company.

Spain is also well know in Europe for its crony capitalism, and for jailing political leaders that protest peacefully.