All Swiss Shares Part 16 – Nr. 151-165

This time I spared no expenses and threw in another 5 randomly selected Swiss stocks to make it 15 “for free”. Among the 15, there is one stock that I already own and one that i find worth watching.

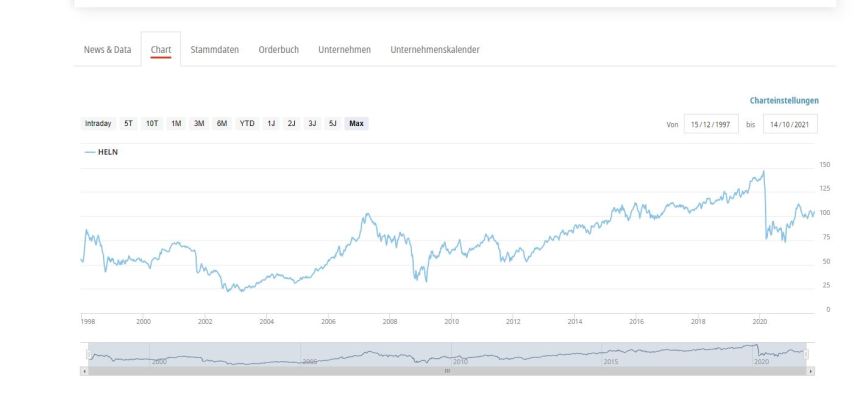

151. Helvetia Holding

Helvetia is “yet another” Swiss insurance company valued at 5,6 bn CHF. As with Baloise, the long term chart doesn’t look very interesting:

Helvetia trades slightly below book value and has a higher Non-life share than Baloise. However, the majority of the business is also done in Switzerland with around 1/3 in other European countries. All in all not very exciting, “pass”.

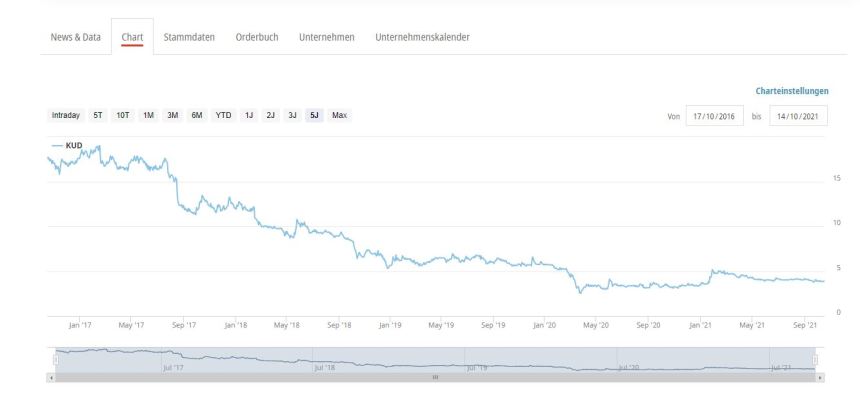

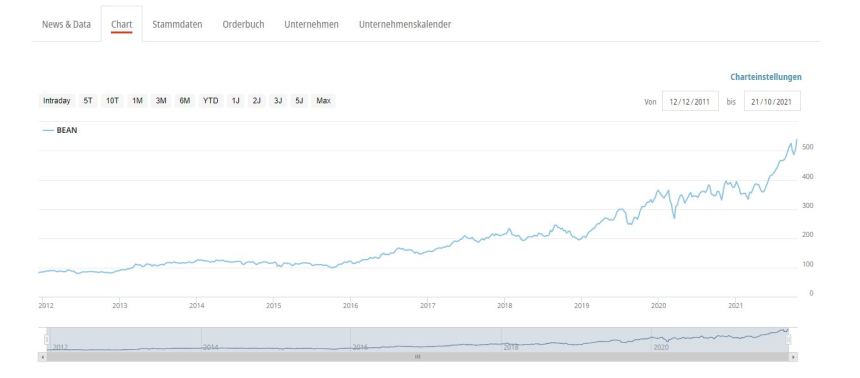

152. Kudelski AG

Kudelski is a 198 mn CHF market cap “Digital security” provider. This sounds exciting, but reality it seems to be a shrinking business. The company has been loss making fro the last few years and has a lot of debt. The chart speaks for itself:

“Pass”.

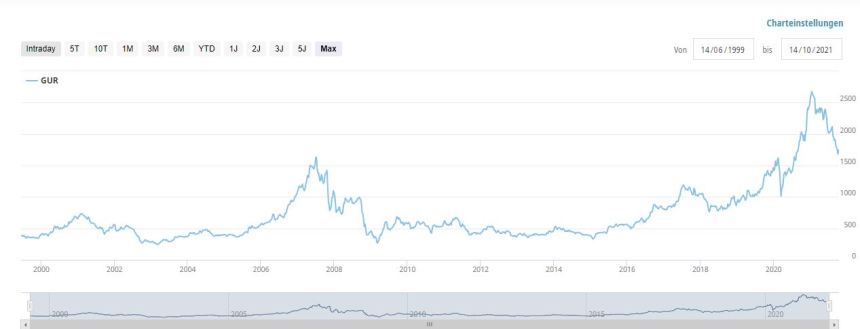

153. Gurit AG

Gurit AG is a 740 mn CHF market cap specialty plastics producer that , as many Swiss stocks, had a great run since Covid before consolidating in the last few weeks:

One of the reasons for the increase might have been that the company seems to be a supplier of composite materials for Windmill blades. On the other hand, Gurit had pretty awful 9M sales numbers which seem to indicate that the windblade business is not a sure home run and explains why the stock price has come down again. With an estimated op3erating p3rofit of ~25 mn CHF, the stock looks quite expensive. “Pass”.

154. SF Urban Properties

SF Urban Properties is a 266 mn CHF market cap property company that seems to ba active mostly in Switzerland. “Pass”.

155. Intershop Holding AG

Intershop is not an internet shopping company as the name might indicate, but another, Swiss focused Real Estate company with a 1,1 bn market cap. “Pass”.

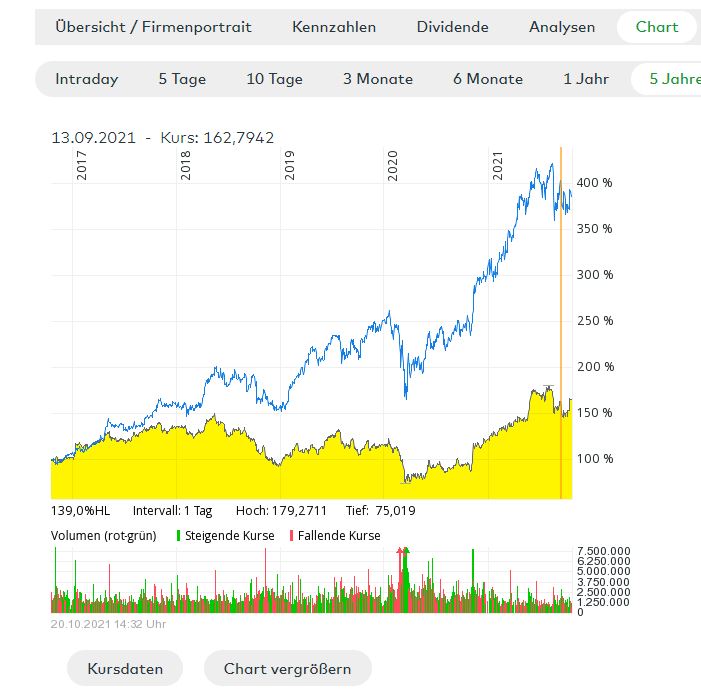

156. Richemont Holding AG

Richemont is a 57 bn CHF market cap luxury company that I had written about in 2016 but only bought during the Covid crash. Looking back, this was clearly one of my better ideas, even compared to LVMH (blue line).

However over 5 years, LVMH outperformed Richemont by a wide margin:

The company trades currently at slightly north of 40x P/E which for such a high quality business seems fair and the company is still run by owner/founder Johan Ruppert.. They have significant direct and indirect exposure to China which needs to be monitored. For the time being, it is a “hold”.

157. APG SGA

APG is a 640 mn CHF market cap company that is active in outdoor advertising. This sounds interesting at first, but a glance into the 6M report shows that the company seems to be in decline since a couple of years.

The company is active mostly in Switzerland but seems to be struggling for many years now. As I do not really undertand this industry, I’ll happily “pass”.

158. Autoneum AG

Autoneum is a 680 mn CHF market cap automobile supplier. They seem to specialize in thermal and accoustic insulation. The company made losses, both in 2020 and 2019, but so far in 2021 seems to be back on track for profits.

P§art of their product line seems to be specifically made for combustion engines which might not be the biggest growth market. Therefore I’ll “pass” .

159. INA Invest AG

INA Invest is a 161 mn CHF market cap holding company that seems to be a real estate developer. The company seems to have been some kind of spin off and was listed in 2020. So far with very limtied success. “Pass”.

160. EEII AG

EEII AG is a 8 mn CHF market cap company that claims to hold interests in Ukrainian utility companies. Outside my circle of competence and interestm therfore I’ll “pass”.

161. Swiss Steel Holding

Swiss Steel is a 1.1 bn CHF market cap “penny stock” that is an international steel producer. The largest market seems to be Germany. In 2019 and 2020, the comp3any burned a lot of money, the first 6M 2021 seems to have been profitable. I don’t see here any angle that interests me, therefore I’ll “pass”.

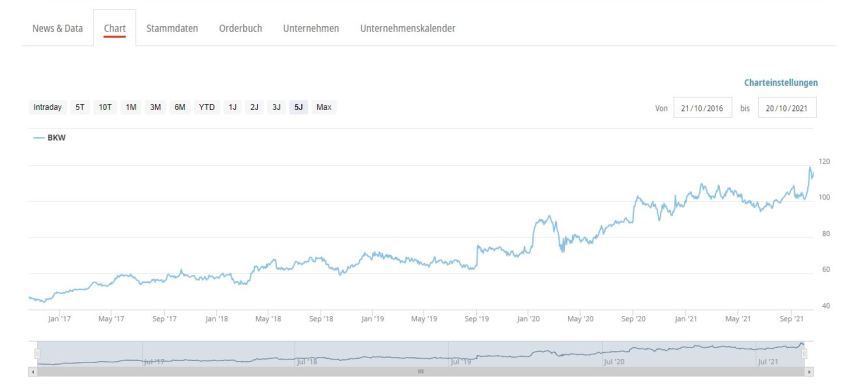

162. BKW AG

BKW AG is a 6.1 bn CHF market cap utility company that. according to a recent article on Brandeins, seems no trying to roll up3 the German Mittelstand. So far the shareholders seem to like the strategy as the stock price has been doing quite well over the past few years. Not bad for an utility company:

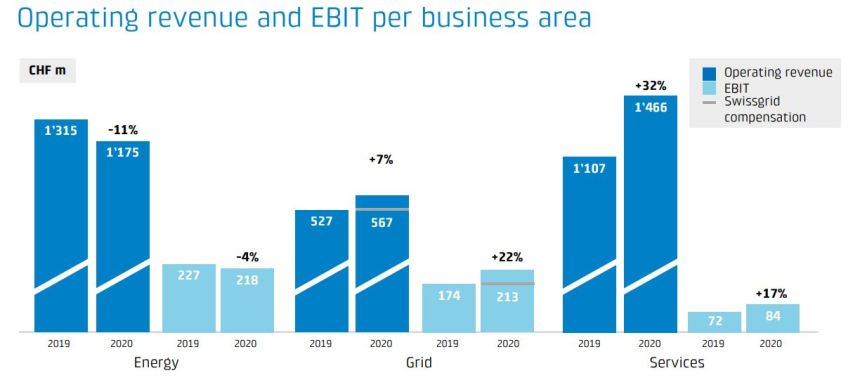

A quick look into the IR presentation shows that BKW is growing outside its core business but profitability is lacking:

Net debt is low (~1xEBITDA), so that is not a problem, but still this doesn’t look like a big value add strategy to me, buying low single digit EBIT margin businesses to comp3lement high EBIT margin divisions. Share buybacks would be the better way to create value.

However what really annoyed me is a really unprofessional website where it was impossible to find the 6M report. “Pass”.

163. Peach Property AG

Peach is a 935 mn CHF market cap property company that for a change seems to invest in German residential real estate. They concentrate on B-cities and, looking at their share price, they seem to do this with some success in the last few years.

However this is not a target sector for me, therefore I’ll “pass” as always in these cases.

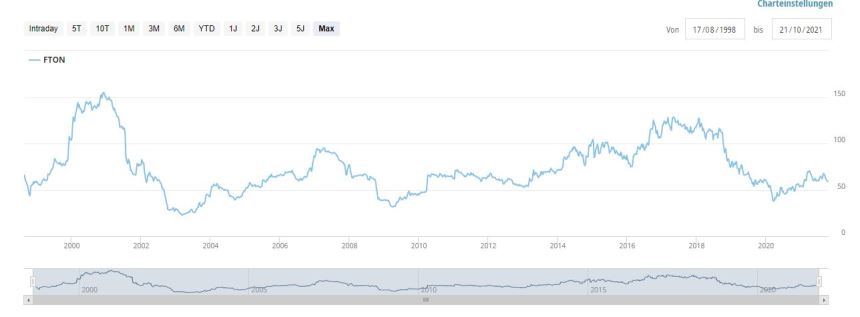

164. Feintool AG

Feintool is a 285 mn CHF market cap machinery company that according to the stock chart went nowhere over the last 20 years:

in the first 6M 2021, results came back strongly compared to 2020, but already 2019 was a very weak year. In good years, Finetool was able to make 20-30 mn CHF in profits, but they seem to have increased leverage lately, mostly due to very high Capex.

in the first 6M 2021, results came back strongly compared to 2020, but already 2019 was a very weak year. In good years, Finetool was able to make 20-30 mn CHF in profits, but they seem to have increased leverage lately, mostly due to very high Capex.

At a first glance, this could be a cyclical play, but as I am not looking for cyclical stocks, I’ll “pass” .

165. Belimo AG

Although the name sounds like real estate, Belimo is a 6,6 bn CHF market cap3 comp3any that manufactures all kind of building related, valves, sensors and other “gadgets”. Looking at the 10 year stock p3rice shows that with the stock up more than 5x, these gadgets seem to be interesting:

In the first 6, 2021, Belimo could increase sales by +15% and EBIT margins reached 19,7%. Traditionally, they achieved between 16-17% EBIT margins. 2020, sales declined by -5%, the years before, Belimo grew at 8-10% p3.a. and Returns on Capital looked equally healthy.

This clearly looks like a high quality business, on the other hand, at 10x sales and 50-60x 2021 earnings, investors seem to be aware of this. Nevertheless, this is one to “watch”.

Switzerland is a study case for many things, (oversized) finance industry in particular. To me it all goes down to trust, and its democratic fundamentals: you will place your savings where you trust they are safe, you will buy insurance where you trust they will pay if you face a loss. But the same goes to many other things. Also in life.

As always, thanks for the excellent research. I bought BKW on the occasion of and timed a week before the decommissioning of their Mühlenberg nuclear power plant End of 2019 and have been very pleased with the development since then.

The semi-annual report really only shows up on the homepage in the ‘About Us’ section if you select “Switzerland” as the location beforehand. However, even then the browser has to wait quite a lot of graphic gimmicks until you arrive at the pdf.

I own BKW shares but I don’t want to rank how the results compare to the others.

At least I expect an increasing overall performance in energy (last year was wind weak, additional wind farms commissioned), networks and transmission volumes develop well (end of Corona -Lockdown, EBIT increase despite 9 million one-time compensation in 2020, first entry into gas sales after at least partial liberalization in Switzerland) and personnel-intensive services have a very low return on sales (5% vs. 15-30% for energy and networks) but a high ROI (10-15%( according to investors conference in September 1st.

So this is no recommendation, just my personal summary. After your All-Swiss review, I will consider reviewing again whether I want to continue to hold the share or switch to another investment.

edit: 5% (Servises) vs. 15% (Energy) and 30% (Grid) is not return on sales, it is EBIT margin für HJ1 2021