All Swiss Shares part 18 – Nr. 191-200

With 200 out of 215 stocks now covered, this will be the penultimate post in this series covering single stocks. My goal is to conclude this in 2021 and it almost looks like I’ll succeed.

This time, two stocks look like worth watching further. At the very end of this series I will need to consolidate my watchlist and concentrate on the top 20 (or so) stocks to watch going forward.

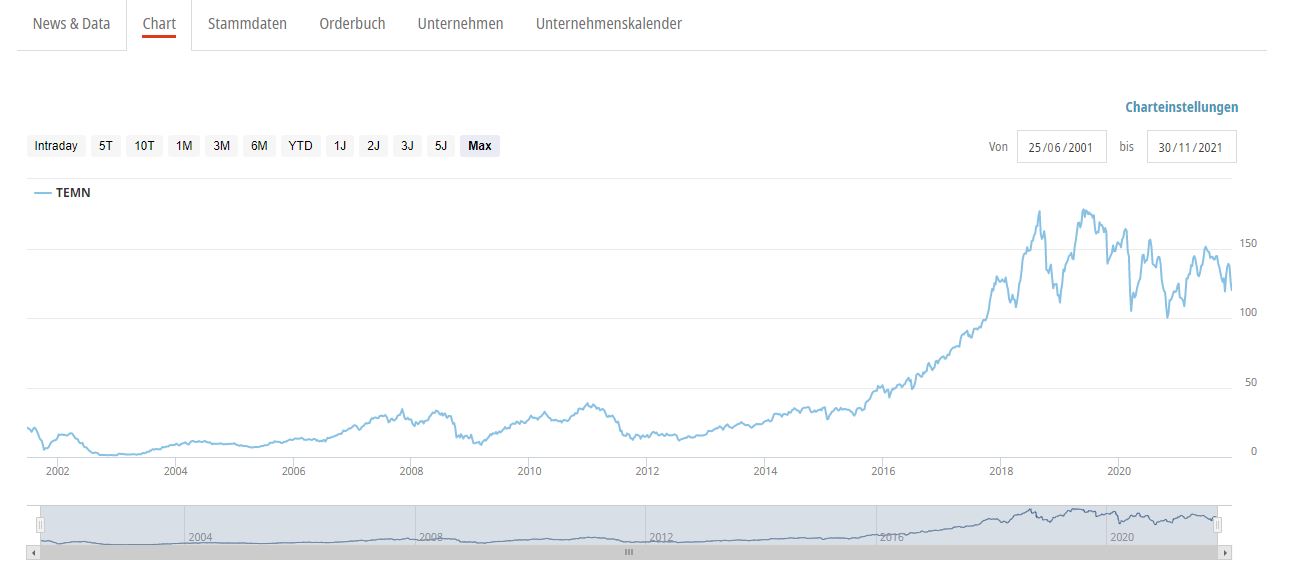

191. Temenos

Temenos is a 9 bn CHF market cap software company that specializes on Software for banks and financial institutions. Looking at the chart one can see a very nice run up until 2018, since then the stock trades sideways under significant volatility:

The company as such is highly profitable, with EBIT margins of > 30%. In 2020, sales declined by -8%, but EPS remained more or less constant. As many other “traditional” Software companies, Temenos seems to be transitioning right now from a licence + maintenance model to a SaaS model.

Valuation wise, the company currently trades at around 11x EV/revenue and at ~35x 2021 (non-IFRS) Earnings. So this is clearly outside what I feel comfortable, however I would nevertheless put them on “Watch” as at its core they seem to do something very good by achieving these margins. An area of some concern is that they use a lot of non-GAAP metrics and it is hard to find out about GAAP numbers. Also the company carries net debt of around 0.9 bn CHF.

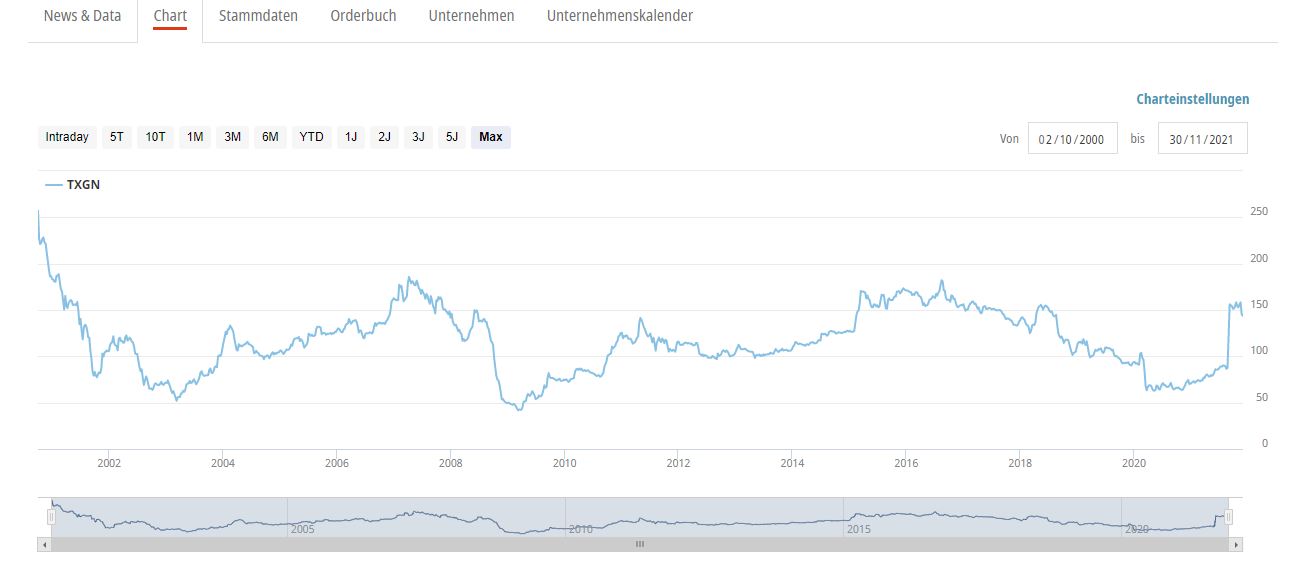

192. TX Group Ag

TX Group (formerly Tamedia) is a 1,5 bn CHF market cap media company, owning a variety of Swiss media outlets, mostly newspapers. After big losses in 2020, 2021 seems to be a lot better. The company also was able to merge its digital part with the digital activities of Ringier which seems to explain the big jump in the share price in August 2021:

However, as it can clearly be seen in the chart, there was little shareholder value creation over the last 20 years. Based on 6M 2021, the shares trade now somewhere between 15-20 EV/EBIT which doesn’t look cheap. “Pass”.

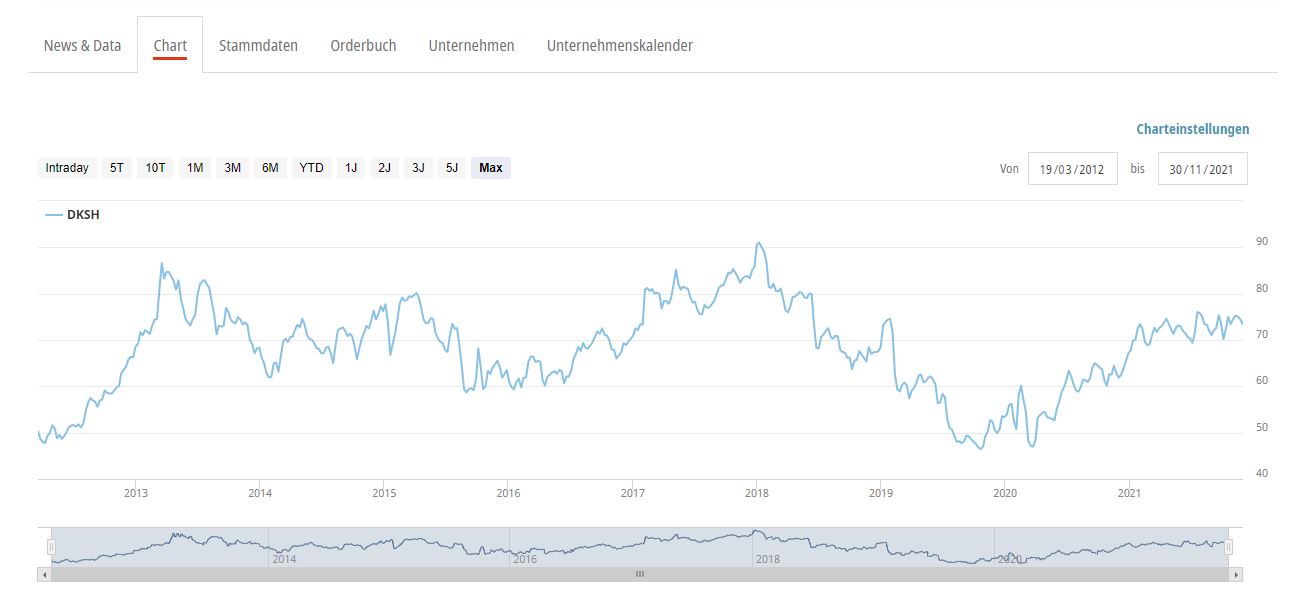

193. DKSH Holding AG

DKSH is a 4,7 bn CHF market cap company that seems to be mostly active in Asia in health care, consumer product distribution as well as chemicals. Overall it looks like an extremely diversified conglomerate. Since its IPO in 2021, the Stock has basically traded sideways:

With a P/E for the current year of around 30, the stock doesn’t look cheap and from the outside it looks like very hard to really understand, although the company as such looks quite interesting.Maybe I am missing something, but I’ll “pass”.

194. IVF Hartmann AG

IVF Hartmann is a 310 mn CHF market cap majority owned (~2/3) subsidiary of Paul Hartmann AG, a German healthcare supplier that I actually had invested in some time ago.

IVF had significantly outperformed the parent for a long time as we can see in the chart:

Interestingly, profits declined from 2016 to 2019 before jumping significantly in 2020, driven by the demand for their infection management products. However, 6M 2021 already looks a lot wors and profits are below 2019, which explains the weak share price.

Overall, the investors of Paul Hartmann clearly have no particular interest to see a high share price, neither for the parent, nor for the subsidiary. Therefore “I’ll “pass”.

195. Valartis AG

Valartis is a 47 mn CHF market cap company that is active in banking and asset management. There seem to be some Russian activities. At first sight, the stock seems to be very cheap at a P/B of ~0,5 but results seem to be very random. Maybe interesting for a “deep value” investor but not for me. “Pass”.

196. Orior AG

Orior is a 590 mn CHF market cap company that specializes in food and beverages and is active mostly in Switzerland but also in Germany and Belgium.

The business is rather low margin, with net margins in the range of 3-6 % in the past, ROCE looks Ok in a range of 10-15%. The stock is not that expensive (measured by Swiss standards) based on pre-Covid profits, on the other hand I don’t see that much upside, especially as their offers look quite “sausage centric”. “Pass”.

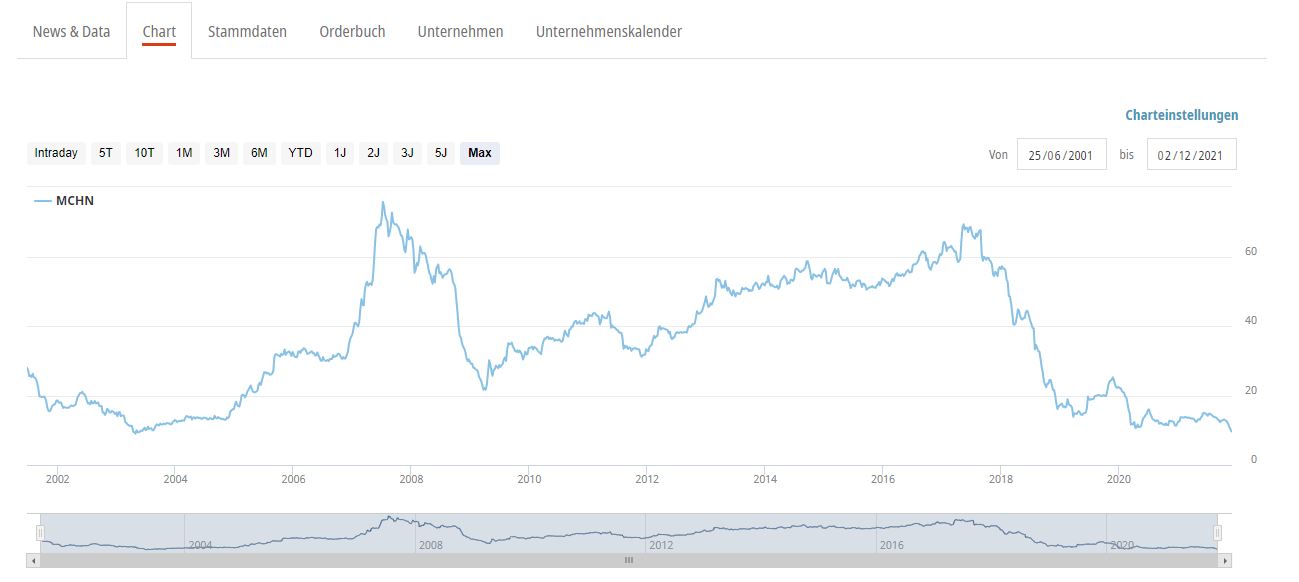

197. MCH Group AG

MCH Group is a 141 mn CHF market cap “fallen angel” company that had problems already before Covid-19 hit. as we can see in the chart:

MCH is a company specialising in exhibits and expositions, among them Art Basel as well as the biggest watch esposition Baselworld. Covid-19 clearly was not good for business but the problems started earlier, with Baselword basically dissolving in 2018 due to a lack of enthusiasm from the big watch companies, especially Swatch Group. MCH had built a huge exhibition building in Basel which because of this had to be written down by a third digit mn CHF amount.

Following Covid-19, MCH had to be rescued by James Murdoch, who now owns ~1/3, however with some problems around the capital raise.

From the outside, this looks very messy. Per 6M 2021, the company is still bleeding money and as for now it doesn’t look like things might change soon. In addition the company has recently suffered a cyber attack which, 4 weeks after the attacks, still hasn’t been resolved.

Overall, this looks like a real “hard core trun around case” which is not really my specialty, therefore I’ll “pass”.

198. Metall Zug

Metall Zug is a 491 mn CHF market cap diversified group active in infection control, wire processing and medical devices. Metall Zug spun-off V-Zug which has now almost 2x the market cap of its parent.

The remaining business looks rather low margin, although the stock looks quite cheap, with an annualized valuation of arounf 10x EV/EBIT based on 6M 2021.

Within the conglomerate, the medical device business looks most interesting with single double digit margins. The biggest segment, Wire processing seems to be mostly an automobile supplier with potentially some positive exposure to EVs.

The chart looks uninspiring:

The company has significant net cash. Overall it might not be a stellar performer, but I would want deeper into this company at some point in time. “Watch”

199. Spice Private Equity AG

Spice is a 89 mn CHF market cap listed PE company. Based on their reports, the stock seems to trade at around 50% NAV which seems to be cheap, but a first look at the portfolio shows a quite unsystematic collection of assets such as a US based Italian estaurant chain. Despite its spicy name, the share price development has not been very spicy. Not my cup of tea, “pass”.

200. CICOR Technologies AG

CICOR is a 151 mn CHF market company that is manufacturing electronic components. At first sight it looks like a low margin, capital intensive business. The stock is relatively cheap but has been going sideways for the last 20 years under some volatility. I do not see the upside here. “Pass”.

Damn, I should have applied for that management position at Temenos – almost $1bn extracted (if the shortseller has calculated correctly).

https://www.shadowfall.com/blog/2020/01/13/bravado-buys-and-unremitting-sales/

Thx, off the watch list they go….

Thanks a lot for your work again! Is lastminute.com also part of your Swiss screening universe or will they not be included given Dutch ISIN? In any case, would be very curious to hear your current view, in case you still follow them and recently looked at them? Thank you! 🙂

Swiss market seems as boring as their unhabitants… :-s