Paul Hartmann AG (DE0007474041) – Back to my (boring) roots

The company:

Paul Hartmann AG is a 200 year old German company active in the healthcare sector, This is how they describe themselves:

The HARTMANN GROUP is a global company operating in the field of medical and care products. The core of the product portfolio offered under the HARTMANN brand is formed by professional system solutions in the areas of wound management, incontinence hygiene, and infection protection. Complementary products and supplementary services round out the range for medicine and hygiene.

The focus is on products and services for professional users in hospitals, doctors’ practices, nursing homes, and for home-care services. HARTMANN offers innovative all-in-one solutions made up of user-friendly products and fit-to-purpose services – helping in this way to make everyday work to enhance patients’ wellbeing

that bit more efficient and cost-effective. The company also offers consumer product ranges sold at pharmacies and specialist medical stores.

Back to my roots:

I owned Hartmann long time again and sold it in 2010 just before I started the blog. I sold it at that time because the stock price went up a lot in short time and I started to move from my “core center of competence” German small caps to more international targets.

Facts & Figures:

Market Cap: 1,2 bn EUR

PE (2017): 13,4

Dividend yield 2,1%

EV/EBITDA (2017) ~6,5 (including pensions)

Debt: Net cash

Free float: Unknown (below 50%)

The company is not covered by any analysts. The stock is traded at a very lightly regulated segment of the German stock market. therefore information requirements are limited, for instance only sharholder transactions above 10% have to be notified.

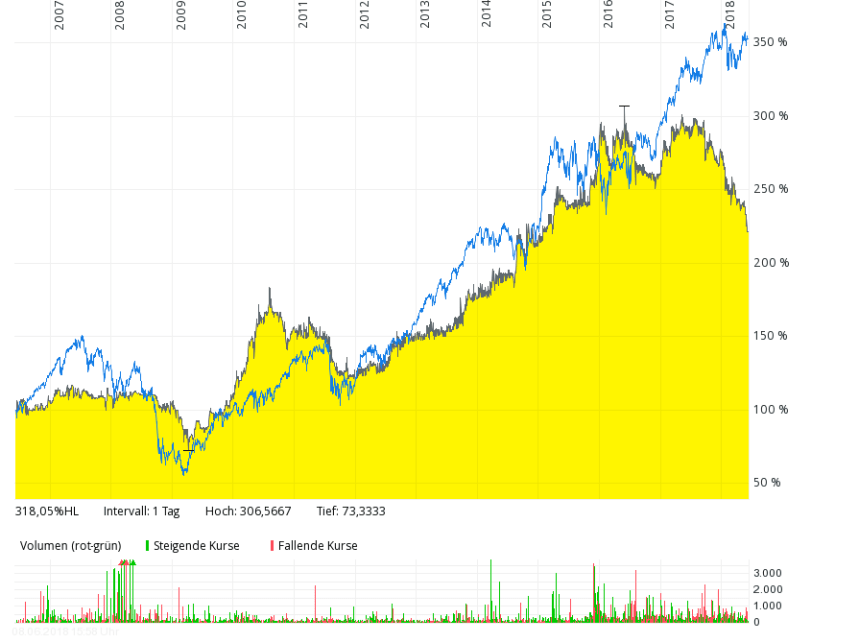

Stock Chart

Looking at the stock chart we can clearly see that things looked Ok until 2017 (compared to the MDAX) but than the stock started dropping and has lost more than 30% over the last 12 months.

This is mostly the result of a profit warning from September 2017, where the company said that this is mainly due to the new European Medical Device Regulation (MDR) that leads to extra cost. I haven’t been aware of this new regulation but this E&Y report confirms that this is “for real”:

The costs associated with compliance may force some companies putting themselves up for sale. The aftermath of the shake- up will be a stronger, more accountable medtech industry that may look substantially different from today’ s. Many medtech companies have begun to look at how they should address compliance, and realized that the extent of the changes requires a company- wide approach. These companies have grasped that the EU MDR represents not just a compliance

challenge, but an opportunity to add value to the business at the same time.

In regulated industries, an increase in regulation often has two effects on the existing players: Yes, it increase cost but also in the long run it often makes it more difficult for others to enter the space. It will be interesting to see how this plays out for Hartmann, but at the moment it looks like the costs are significant.

In Q1 2018, EBITDA dropped yoy by -8%, EBIT by -16% and net income even by -17,5%. As Hartmann is only listed in a very lightly regulated segment of the German stock market, no detailed numbers are available to really understand the drop in profit. The language in the report says however that they expect a “Moderate drop” in EBIT for 2018.

The company is really boring:

A German stock blog writer for instance sold the stock last year (well-timed by the way) among other reasons that the company was “snoring”. In the same posts a commentator argued that he didn’t like the stock as the majority shareholder (Schwenk family) is not interested in more aggressive strategies as they like Hartmann to be defensive in order to compensate for their main cyclical Cement/building material.

What I like about the company:

+ the company is run conservatively: Net cash, few M&A transactions. long-term orientation

+ the company is in a stable sector with long-term growth

+ the current weakness seems to be triggered by an industry wide issue

+ despite its size it is mostly unknown (no index member etc.)

+ very moderately valued

– the industry is really hard and regulated (cost saving pressure at main clients)

– mediocre returns on capital

– relatively large pension reserves

– no short-term catalysts

Some historical numbers:

This is for instance the development of net debt since 2011:

| 2017 | 2016 | 2015 | 2014 | 2013 | 2012 | 2011 | |

|---|---|---|---|---|---|---|---|

| Cash | 73.7 | 109 | 90.5 | 89.1 | 56.8 | 48.2 | 44.7 |

| Financial debt | 22.1 | 38.2 | 58.9 | 92.7 | 137 | 146 | 202.9 |

| Net debt | 51.6 | 70.8 | 31.6 | -3.6 | -80.2 | -97.8 | -158.2 |

| Pension | 172.4 | 170.5 | 152.6 | 142.2 | 102.1 | 106.1 | 88.9 |

| Net debt incl. pension | -120.8 | -99.7 | -121 | -145.8 | -182.3 | -203.9 | -247.1 |

| Acquisitions (net) | -129.9 | 4 | 1 | -2 | -5.4 | -16.8 |

It is easy to see that Paul Hartmann “delivered” the company over the past 8 years until last year when Net cash went slightly down after their first larger acquisition for a long time. The acquisition was a Spanish decision of P&G specialized in producing and selling incontinency products via pharmacies. Although the acquisition looks expensive compared to Hartmann’s own valuation, from a strategic point of view it looks ok, as this is clearly within the core market of Hartmann.

A Private Equity owner would have done most likely the exact opposite It would have been relatively easy to obtain low yielding debt and either buy back shares or buy higher margin businesses. This often works in the short run, but creates problems in the long run makes companies vulnerable.

IVF Hartmann

Interestingly, Hartmann’s Swiss subsidiary has its stock listed on the Swiss stock exchange.

IVF has a market cap of 440 mn CHF and trades on much higher multiples that the German Holdco:

P/E 2017: 27,4

P/S : 3,3

However, IVF Hartmann is also much more profitable. EBIT margins are on average 14% or 2x that of Paul Hartmann. I honestly do not know why. Maybe the Swiss market is more regulated and margins therefore higher ?

Valuation

As always, I try to keep it simple. At the current stock price the earnings yield is around 6-7%. Free cashflow yield is even a little bit higher.

Assuming a long-term growth rate of 3-5% p.a. I would estimate at the current share price a potential long-term return of between 9-12% p.a. This doesn’t sound much, but in relation to the “antifragile” business model I do thin this is attractive from a risk return perspective.

I have therefore allocated ~2% of my portfolio into Paul Hartmann shares as a starter position at ~334 EUR/share and I plan to add slowly over the coming months.

https://www.onvista.de/news/dgap-adhoc-paul-hartmann-ag-paul-hartmann-ag-isin-de0007474041-hebt-aufgrund-temporaerer-effekte-der-corona-pandemie-die-prognose-fuer-das-geschaeftsjahr-2020-an-deutsch-386747525

Paul Hartmann AG with a raised guidance

Absolutely sick quarterly figures reported by Paul Hartmann today, wow!

Does “sick” mean good or bad ?

Sick meaning very good here:

EBITDA grew by 35%+, they must have had a free cash flow of about 50 Mio € in Q1 – probably with heavy tailwinds of working capital reduction and the Sanimed sale

Covid-19 could be a short-term catalyst here, I’m very surprised about the current share price for this defensive, even antifragile business. Sterillium is now the bestseller in many medical categories on Amazon, and I’ve noticed a big surge in prices, also even for rather plain surgerical masks.

Interesting to me as well, that the Swiss subsidery IVF Hartmann gained about 20% since mid-December – with no material effect on Paul Hartmanns share price, which is very strange.

There seems to be a large seller @290€ on the trading plattform tradegate, almost like an iceberg order – I’ve noticed this for weeks now. Interesting to see what happens once he is done.

yes, this could be a small short term bump. Zur Rose is actually also doing quite well.

It seems to me that Germany withholds 15% of dividends in tax from foreign investors.

Did I understand this correctly?

Ballpark yes.

added a small amount (0,3% of portfolio) to my Hartmann position at 298 EUR/Share

Dear MMI, one thing that would worry me with Hartman is Coloplasts ambition to take share in the wound care market.

E.g. check this presentation https://www.coloplast.com/Documents/Investor%20Relations/CMD/Wound%20and%20Skin%20Care.pdf

that shows that they successfully gained share – currently still from a low base of ca. € 275m sales (so it will not be felt immediately given Hartmann is much bigger – but should they accomplish to double their business I would expect Hartmann growing below mkt.).

Kindly Sascha

thank you for the comment. However what I am struggling with is the following: Coloplast has currently net margins of ~20%, Hartmann less than 5%. I don’t think that Denmark based Coloplast is a lower cost manufacturer so I really don’t see them competing in Hartmann’s market. I am not a Wound care expert but i guess they are most likely targeting a different segment. I would be interesting to see if Hartmann could target this segment too and improve margins ?

Dear MMI sadly I never spoke to Hartmann but from my meeting notes with Coloplast I noted that CP predominantly sells to Hospitals and later on Elderly Homes – whereas Hartmann is strong in “conventional wound care” which is less critical product probably often sold via the pharmacy / “Sanitätshaus” saleschannel.

There’s an old Mölnlycke presentation mentioning Hartmann a few times here: https://www.investorab.com/media/1194/presentation_q3_2013.pdf see esp slide 33

interesting Sascha. Do you have an investment blog as well?

Coloplast is among the picks of one of the best buffet-like funds in the nordics.

Until recently, Switzerland has been the place where health spending per capita was highest in absolute terms. I guess margins can be FAT in these circumstances.

Do they have operations in Turkey and Russia ?

Yes.

Welcome aboard, memyselfandi007:

https://www.covacoro.de/2018/05/06/read-in-may-and-stay/

Pingback: Kleine Presseschau vom 21. Juni 2018 | marktEINBLICKE

2% ain’t small. Why now and not later?

2% for me is a starter position. A normal size position would be 6%….why now ? Why not ?

No catalyst, no inflection, top of the cycle, etc….

But I understand that you aer averaging down (making the EUR 334 irrelevant). How do you usually do that (without material changes)? double up with every pully back of 5% or so?

No catalyst and no inflection are actually strong indicators FOR an investment under my philoSophy…

what about the averaging down question? is there a philosophy or just whimsical?

I am not planning to average down but to buy mechanically every quarter.

Thanks for sharing with us your thesis.

Just for information, according to the 4-traders company information free float would be below 33%.

I assume they can grow in line (or slightly above including small scale M&A) with healthcare expenses, which grow clearly above normal inflation.

Makes sense, thanks.

Looks reasonably priced. Why do you think the company can grow substantially higher than the inflation rate for the foreseeable future?