Protector Forsikring ASA – The Scandinavian “Baby Markel/Berkshire” ?

The company:

Protector Forsikring ASA is a name that came up more often in my “stream”. It is a Norwegian “Challenger” Insurance company founded in 2007 (and IPOed in 2008) that has been growing nicely over the past years and doesn’t look expensive.

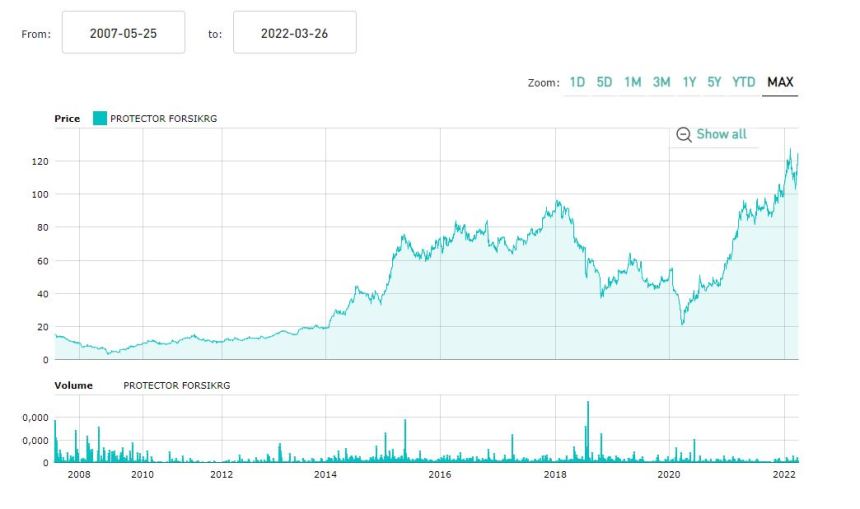

The stock price has been quite volatile but recently the stock has reached new highs and long time shareholders should be quite happy:

The high level financial indicators look very attractive: A relatively Ok valuation with an impressive ROE:

Market cap: 10.200 mn NOK

EV/Revenues: 2,1x

Price/book: 2,8x

Price/tangible book: 2,9x

ROE 2021: 35%

P/Earnings 2021: 9,6

The business:

Protector focuses on Property & Casualty insurance in the Nordics and the UK. One specialty is that they only sell via the broker channel. They also focus on commercial business as well as insurance for public institutions but not individuals.

Another specialty is that they try to emulate the Berkshire/Markel model by investing a significant amount of money into a rather concentrated stock portfolio.

The Danish Fund manager Symmetry has published an interesting write-up on Protector in 2020, which looking back clearly was exceptional timing. Their thesis centers around the following points:

- Protector has a cost advantage (being lowest cost provider)

- Protector has superior investment skills, especially for their equity portfolio

- Back then, Protector was cheap both, historically as well as in comparison to Nordic peers which trade at significant higher multiples

Nordic insurance is very special: For some reason, the big Nordic players (Trygg, TopDanmark, Sampo etc.) managed to keep the large Global/ European players out and seem to have managed to form a “friendly oligopoly”, allowing very decent returns for everyone. This is very different to the rest of the P&C world where competition is fierce.

What needs to be taken into account also is that Protector accounts full “mark-to market” for its financial investments, which means that 2021 comprise a very good year for equities (more than 30% return) which clearly cannot be assumed for each and every year. In addition, insurance technical results were good as no major Cat risks realized.

“Normalized” Profit potential:

As mentioned in other posts on insurance companies, a “normalized” return consists of two main items: “Underwriting profit” from the insurance side and financial returns from the investment portfolios. Year on year, these results can jump around a lot, but long term they should average out on realistic assumptions.

For Protector, I would calculate this as follows:

Premium Income 6 bn NOK , Target CR 90-92% –> 550-600 mn NOK “operating” insurance profit

Total Investments: 14.3 bn NOK, thereof 2 bn NOK in shares

Normalized return Fixed Income: 12,3 bn * 2% =~ 250 mn NOK normalized profit for bonds

Normalized return Stocks. 2 bn * 10% = ~200 mn NOK normalized profit for stocks

In total, this would mean ~1000- 1050 mn NOK of “operating profit” minus -60 mn NOK of interest expenses, which leaves us at 940-990 mn NOK Operating profit, minus 15% tax results in around 800-840 mn NOK of net income on a normalized 2021 basis.

This in turn would mean a “normalized” P/E ~12-13x. Still cheap for the Nordics where the competitors trade at P/Es of 16-22x (trailing) but maybe “OK” for the UK.

In the UK, commercial insurers like Beazley trade at a P/E of ~10.

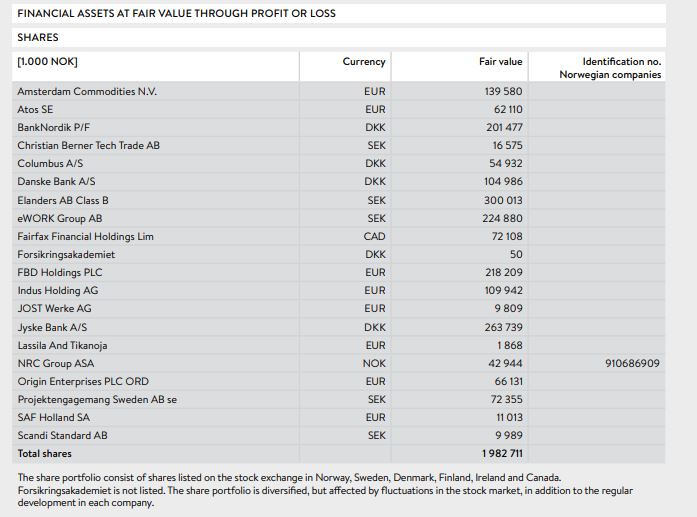

Share portfolio

As a potential “Baby Berkey”, it is of course interesting to look at their investment portfolio which performed very well, both in 2020 and 2021 which looks as follows:

The portfolio is quite a concentrated portfolio with a significant share in (cheap) financials, mostly in the Nordics and neighbouring countries. The big positions are clearly “value” stocks that look technically cheap and pay rather high dividends. With the size of Protector’s position, they also would not be able to liquidate the shares quickly. I have analyzed a few of them myself (FBD, Acomo).

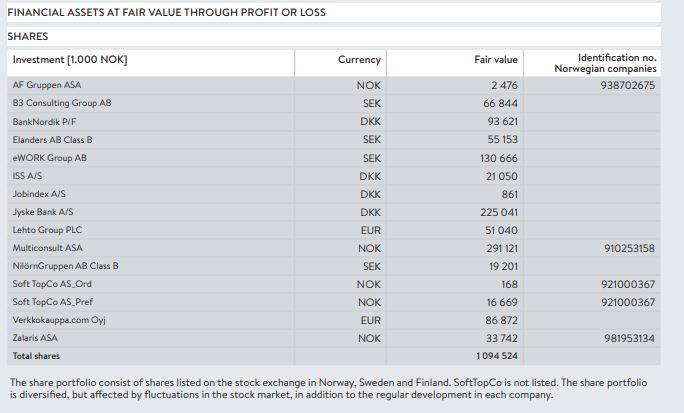

Looking at the 2019 portfolio, one can also see that the portfolio has changed significantly over the last 2 years:

Only 4 stocks from 2019 are in the portfolio in 2021. So overall this looks like a more “opportunistic value” strategy than a Berkshire/Markell type long term “Quality GARP” strategy. Overall, I honestly would not hold that portfolio myself but that doesn’t mean anything. Symmetry actually did an interview with the CIO and he sees to be a nice and thoughtful guy and he definitely has his own style.

Pros/cons

Some Pros/cons at this stage:

+ low cost ratio (gross around 10-11% vs. 14-15% for Nordic peers)

+ partially founder run (Supervisory board)

+ good growth track record historically

+ good Investment track record

+ short tail, SME focused P&C business is relatively easy to manage

+ Nordic insurance market is potentially very attractive

- potentially volatile P&L because of fair value accounting with full P&L effect of equity investment valuation

- Protector’s second biggest market and main growth engine is the UK in 2021 and UK is a much harder market as seen by the negative technical results in 2021, growth stalled overall in the Nordics

- reserving is not so conservative (from 2015-2019, reserve development was negative)

- Founder’s share in the company is quite low, founder CEO retired in 2021

- quality of bond portfolio is difficult to assess as ~50% is not rated

- Business model is geared towards brokers which itself is a channel that is not growing

- Business model dependent on intermediaries

Preliminary conclusions:

Protector is clearly an interesting company and at the time of the pitch from Symmetry, the stock was clearly as close to a “no-brainer” as it gets.

Right now, I do think that the case is not so clear. The valuation is mostly in line with historical values. It is still relatively cheap compared to Nordic peers but not cheap compared to UK peers where they currently grow the most.

Their cost advantage is most likely the result on focusing on the broker channel, where a lot of services are provided by the broker. This means however, that they cannot just compete with players in the direct space because they lack the capabilities to do so. They are restricted to this specific business segment, which, depending on the country, might be larger or relatively small.

Personally, I do think the Insurance industry will face a tough time if inflation persists, as usually there are time lags between claims inflation and premium adjustments.

From a strategic point of view, for me the big question is how much they can still grow in the broker channel in the attractive Nordics markets. In 2021, overall Nordics growth was almost flat and most growth came from the UK which is a very different market. From the experience of Handelsbanken in the banking sector, one should be cautious to extrapolate past profitability numbers from the Nordics and assume this for the UK as well.

Overall, competition in the SME area is increasing, especially from new direct players, so it needs to be seen how big the “niche” for Protector under their current business model actually is.

Finally, it needs to be seen how investor react if their volatile earnings swing back into a loss which I think could happen in 2022.

The big question mark for me is what the actual growth potential of Protector is going forward. If they would be able to grow double digits in the Nordics, a higher multiple wuld be justified. Growth in the UK is clearly less valuable. For the time being, I would be not comfortable to assume significant (and profitable) growth.

For me, Protector is clearly an interesting “watch” candidate, but not a buy at the current valuation. I might be biased here but in relative terms, Admiral to me seems to be the better value proposition.

In addition, I guess it also makes sense to watch their stock portfolio, as there is some overlap in what I am looking

Protector cost (excluding claims handling costs) but including ceding commission to reinsurer in Q1-Q3 2023 is 10,8%, while cost excluding ceding commission is 6,5%.

In UK, cost (excluding claims handling costs) excluding ceding commission went down in one year from 9% to 7.2%.

Protector is a cost leader by far in the Nordics but I don’t know whether there is an UK insurance company able to compete in terms of costs. The management said currently there is no serious competition in UK within the public sector (mostly housing associations and leasehold).

@memyselfandi007, I suppose if you know the UK insurance sector you should have some information?

About growth prospects: the UK market is much larger than the Nordics according to Protector and less competitive in term of costs. Seems like a no-brainer.

When Protector will have reached the critical scale in UK and started to be a dominant (no1 no2) player in its brokers markets, then Protector will move to Netherlands. Afterward, it will attack maybe Belgium.

Protector is simply the low-cost player, disrupting the market. Here you go with the growth plan for the next 10 years. Incumbents can’t compete on price with Protector because of their already existing structures. They would need to completely restructure their organization (-30% in technical costs maybe?) and lower their prices.

By the way, the previous CEO has repeated several times during his presentations that the Nordic market is very competitive because the players are very cost efficient. That’s why International Insurance companies couldn’t enter this market, look at the ratios.

On the opposite, in the UK the players are not “fit and lean” in their cost structures compared to the nordic ones. The current low result of Protector in the UK is just due to the fact that it has not yet reached the efficient size.

This is strange that in your analysis you are stating the opposite about those markets but maybe you have so facts that we ignore.

Also in UK, I thought the main opportunity for Protector was in the motor insurance segment not in the SME area (but I may be wrong on this one).

I have a very different view on that but we will see.

The Motor sector in the UK is by the way mostly direct, not via brokers. Will be interesting how they want to compete there.

Any comment about the astonishing growth of Protector in UK and its Combined Ratio? UK is already the first country for Protector. It seems that the growth comes mainly from the property side public/private.

Also the management is studying the opportunity to enter the French market.

This is indeed at least” astonishing”. I will wait for other UK players to release numbers for Q2 before making an assessment.

nice write-up, thank you. The broker-model has the advantage of low customer acquisition cost but also introduces an extra layer of cost. In our interactions with the company we discovered that the end-customer price is usually a low SD % cheaper than peers. That is in the Nordics.

What I don’t really understand: to my knowledge, broker fees at least in continental europe are normally somewhere between 10-20% of gross premium. Protector shows a lot lower commission cost. Any idea why this is so low ?

AFAIK compensation is often directly between the broker and the customer. So it does not show in Protector’s P&L

I though so. Is there any source where to find more information ? Because this skews the comparison compared to players who do dierct business.

a good starting point could be some of the larger brokers they work with, like Marsh or AON?

That was funny timing. I broadly came to the same conclusion (published today).

The broker distribution is currently a strength but might ultimately turn into a weakness.

The broker modell currently seems to work very well for cyber insurance (not enough underwriting capacity) but usual, boring P&C might see headwinds …

If they do not grow strongly in UK and/or enter continental Europe all the high ROEs are not that valuable

Let’s see if we can (i) buy it cheap during weakness and (ii) indeed have the guts to pull the trigger than…

Cheers

I think you draw the wrong conclusions about which markets are attractive or less so. The nordics is much more efficient or “ologopoly” than U.K or former choises like Netherlands. Also ofcourse the growth potential is much higher threre .

Sorry, I don’t see your point. The Nordic markets are a “friendly oligopoly” and allows for high ROEs.

The UK and the Netherlands are “red oceans”.

No, the opposit, the technical resault is much worse in uk or ex. Netherlands

Bad reply. From my understyrning is the cost advantage for Protector higher in UK and Netherlands than in the nordics relative to peers. That should be a good thing not a bad?