Inflation vs. Pricing Power for Chemical companies & Nabaltec follow up (ADD)

Disclaimer: This is not investment advice. PLEASE DO YOUR OWN RESEARCH !!!!

Inflation & Pricing power

One of the obvious strategies for for investors in an inflationary environment is to pick companies that have “Pricing power”. Pricing power means that companies should be able to raise prices at least as quickly as costs rise.

Now one could try to do some deep thinking if and how different business models react to inflation. As I am a more “hands on” guy, my solution is to look at actual numbers and then try to draw my conclusion.

For any company that is producing material goods, the best indicator for pricing power in my opinion is Gross profit, i.e. the difference between selling price of a product minus the direct costs to produce them.

A company with pricing power should keep the gross margin or ideally even improve gross margins in an inflationary environment.

The Chemical industry

For this exercise, I use the chemical industry as an example. Why ? Because I have one company in my portfolio (Nabaltec) that is/could be severely impacted plus I have a couple of others on my watchlist.

Chemical companies have direct exposure to rising prices for Oil & Gas in two ways: Directly, as feedstock in most “petrochemical” processes as well as energy cost for all chemical companies.

In order to find out how things look for Chemical companies, I defined a Group of mostly EUropean chemical companies that report quarterly P&L and compared the gross margins achieved in Q1 2021 with those achieved in Q2 2022. The result of this group looks like this:

| Company | Sales yoy | GM Q1 2021 | GM Q1 2022 | GM Delta |

| Covestro | 41.61% | 31.63% | 25.33% | -6.30% |

| AKZO | 11.63% | 44.08% | 38.85% | -5.22% |

| Yara | 88.61% | 30.65% | 25.48% | -5.17% |

| Hexpol | 35.77% | 23.86% | 19.43% | -4.43% |

| Fuchs | 15.78% | 36.59% | 32.34% | -4.24% |

| Solvay | 41.82% | 28.23% | 24.07% | -4.15% |

| H&R | 49.88% | 21.75% | 19.24% | -2.51% |

| Lanxess | 43.12% | 25.22% | 23.40% | -1.82% |

| BASF | 18.98% | 26.28% | 26.00% | -0.28% |

| Nabaltec | 25.23% | 50.00% | 52.45% | +2.45% |

| Bayer | 18.75% | 61.89% | 64.64% | +2.75% |

| OCI | 95.45% | 28.56% | 37.09% | +8.53% |

| Mosaic | 70.74% | 18.94% | 36.69% | +17.75% |

Out of these 13 chemical companies, only 4 were able to increase gross margins (Nabaltec, Bayer, OCI and Mosaic), one could more or less keep gross margins (BASF) and the others saw there gross margins decimated by -2% or more, despite all of them growing at least double digits yoy.

Mosaic, as a US based fertilizer company is a pretty obvious winner here, as US input prices have clearly risen less than prices for the end products. Bayer also might benefit (finally) from their US acquisition. OCI is also producing fertilizers and methanol and, in direct comparison to Yara from Norway, seems to be better able to pass on cost increases.

Now a second step is to look how these companies have done YTD so far which is what the next table shows:

| Company | GM Delta | YTD Return |

| Coverstro | -6.30% | -19.20% |

| AKZO | -5.22% | -16.40% |

| Yara | -5.17% | +12.20% |

| Hexpol | -4.43% | -23.60% |

| Fuchs | -4.24% | -27.80% |

| Solvay | -4.15% | -8.70% |

| H&R | -2.51% | -19.10% |

| Lanxess | -1.82% | -16.90% |

| BASF | -0.28% | -15.00% |

| Nabaltec | 2.45% | -19.40% |

| Bayer | 2.75% | +40.70% |

| OCI | 8.53% | +49.90% |

| Mosaic | 17.75% | +51.90% |

Not totally surprising, those players that managed to increase gross margins have done very well this year with the one exception being Nabaltec. The only company with a positive share price performance and a negative Gross margin development is Yara. Maybe people are speculating that Yara will benefit long term from a boycott of the Russian fertilizer companies.

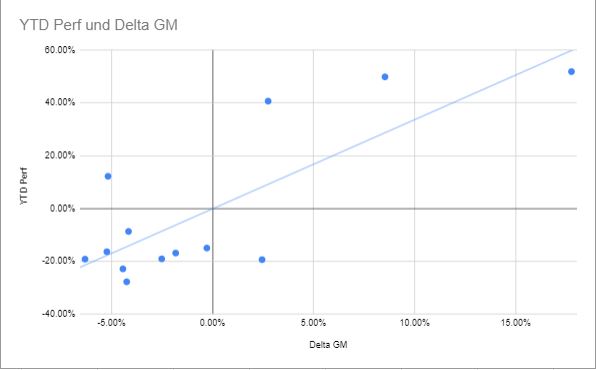

This is how this looks like in a scatter plot:

It is clearly not a perfect match but it clearly shows the direction: Chemical companies that can improve or keep gross margins are doing (much) better than those guys who can’t.

Of course, one quarter doesn’t tell the full story but it might be a good indication for this phase of the market.

Nabaltec follow up – ADD

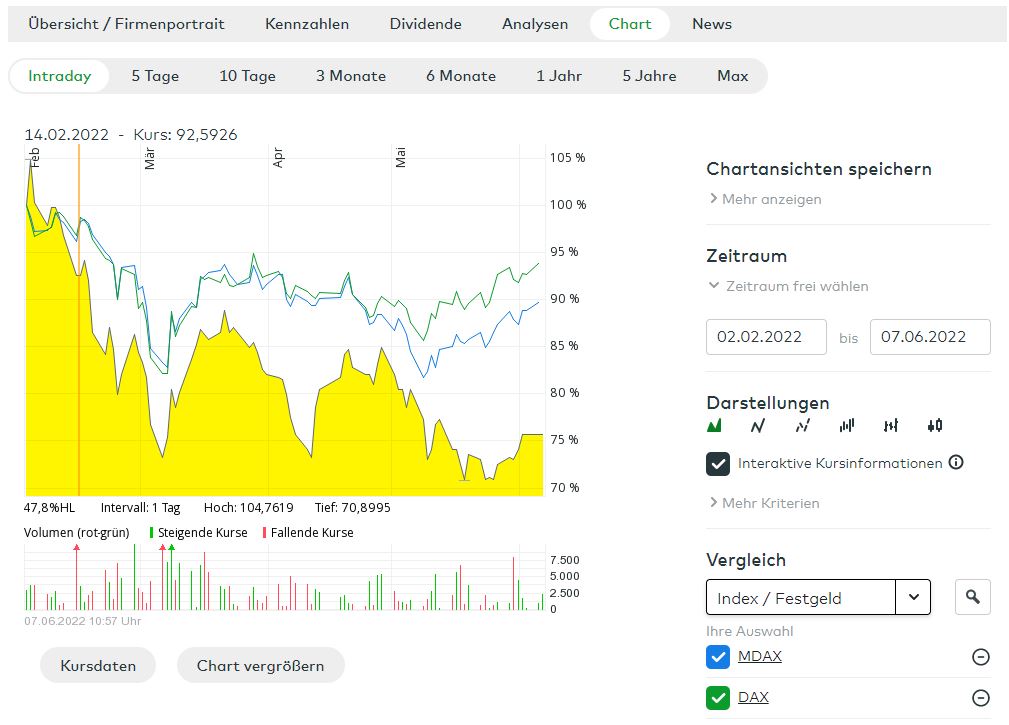

Nabaltec is a German specialty chemical stock that I introduced in early February 2022, just a few weeks before the Russian attack on Ukraine. As an energy intensive company that needs (a lot of) Natural gas as energy for its products, it is not a big surprise that the stock did not so good since then:

What is interesting, that since then, both the 2021 numbers as well as the first quarter 2022 were much better than expected. Nabaltec was guiding for 10-12% sales growth for 2022 and 10-12% EBIT margins. However Q1 showed a sales growth of +19% and an EBIT margin of 12,9%. As mentioned above, Gross Margins even increased, showing (so far) some decent pricing power.

This positive result was to a certain extent surprising, as Boehmit sales in Q1 have been -30% vs. Q1 2021 due to supply chain issues for the main clients (car OEMs). However, the “others” segment really performed well (+30% sales increase yoy).

The question I asked myself is: Why is Nabaltec able to increase margins despite its highest margin product Boehmite being -30% below last year ?

One explanation is that for now, they might still benefit from low gas prices they have locked in and this lasts as long Russian gas is flowing and maybe some competitors have to pay higher spot prices. In addition, their feedstock “only” has to be dug up from the ground and does not require any additional oil or gas (despite energy).

Based on what I heard from a company conference however the main driver have been the demand for their ceramic products for steel plants that are currently booming. Russia has been responsible for ~20% of EU steel imports. Other big exporters like China and India will have issues shipping the stuff, so it looks like that capacity expansion in Europe is on its way, which is good for Nabaltec.

In addition, I “found” another opportunity that I had overlooked in my analysis so far: Granalox is one of the products they sell in their “others” segment. According to Nabaltec’s website it has the following use cases:

Our ceramic bodies (GRANALOX®) are based on our own aluminum oxides. The selection of the aluminum oxide raw materials for each individual GRANALOX® quality is carried out on the basis of Nabaltec’s longstanding experience. Through a precise dosing of the synthetic raw materials with the necessary mineral components, the ceramic bodies for the respective applications can be optimized and designed for the different forming processes.

GRANALOX® is used in classical engineering ceramics e.g. in various machine components. In addition, GRANALOX® is also used in ballistic ceramics, e.g. for vehicle protection and in bullet-proof vests.

I haven’t verified this with Nabaltec yet, but I could imagine that especially the “ballistic ceramics” use case is now in high demand and might lead to more positive surprises down the road. This product also seems to be very profitable (20% EBIT margins).

On the negative side, they seem to have communicated that they are not building the new plant for Boehmite but are trying to expand the existing facilities. This will take longer than the initially communicated plan with the additional capacity going online only in 2024 compared to 2022/2023.

This effect lowers my price target from 72 EUR in 2025 to around 64 EUR, pretty much the decline we saw in the share price so far. This negative effect would be fully compensated if I would assume a 10% growth rate for the “non-Boehmite” business until 2025 (instead of previously 5%) which would not be totally unrealistic. (1% of increase in growth is around +1,5 EUR per share in price target).

Overall I do think that the “negative” news on Boehmit is at least compensated by the unexpected upside of the other business, with the main difference that the shares are actually around 20% lower compared to when I first bought them.

Normally, I tend not to buy when the price goes down but in this case, I do think the the mid term outlook is at least as good as I though in February and the long term outlook is even better than when i first looked at Nabaltec. The company, on top of Boehmite seems to be able to offer more “upside surprises” than “downside surprises” which is something I like very much.

In addition, I think it is good capital allocation that based on the significantly changed environment, they didn’t blindly followed their initial plan of building an expensive new facility, but adjusted quickly to a less risky pathway,

So after adding a little in Mid-May, I am adding “aggressively” from ~3,6% to 6% (full position) of portfolio weight at current prices (28,70 EUR/share).

Based on my usual timing skills, this will possible mean that the stock will go down a lot soon, but fundamentally, this looks like a very attractive stock to me.

Disclaimer: This is not investment advice. PLEASE DO YOUR OWN RESEARCH !!!!

Reduced my Nabaltec position by around 1,3%. Reason: risk management. Risk for escalation with regard to Gas freeze etc has increased.

ThX, isn’t the most important factor in the YTD yield the war in Ukrain and because of that fertilizers?

last days fertilizerprices go down and so are these companies.

https://www.kpluss.com/en-us/investor-relations/shares-bonds/ks-shares/

The price of fertilizer follows the price of Natgas because it’s a feedstock for Nittogen based fertilizers.

Mosaic still benefits from a hedging contract with CF Industries on 1/3 of its ammonia needs. However, the general point in the analysis above is still valid.

Hey MMI,

interesting insights into the chemical sector. I could not find the notification so far, where the building of the new facility was stopped. Could you share a Link here?

Nice to see how you adapt your investment case for the other product lines. Remember your intitial game plan was: „If for some reason the capacity extension doesn’t work out, I will sell.“ Do we have a hint, how much capacity is added by just expanding the old facilitiy for boehmite?

Good luck with this interesting investement and thanks for sharing your ideas!

I was indeed contemplating to sell as well. There was no notification as far as I know but it was communicated during an investor event.