Nabaltec AG – Boring Old Economy Dinosaur or “Hidden Champion” Electrification beneficiary ?

Disclaimer: This is not investment advice. PLEASE DO YOU OWN RESEARCH !!!!

The company:

![]()

Nabaltec is not a fancy Biotech company as the name might indicate, but a rather “old economy” Specialty Chemical company focusing on Aluminium-oxide based materials, located in the middle of nowhere in my home state Bavaria. This typical “German Mittelstand” company had its IPO in 2006, and was created 1996 as management buy-out of a production facility from VAW AG. The beginnings of the plant as such seems to have been built in 1938 and looks like this:

When I looked at Nabaltec during my all German Shares series, I already classified it as “Watch” candidate but didn’t dig deeper so far.

The Anti-Pitch:

This time I start with some reasons why one should maybe not invest into the company. Here are the major issues:

- The business is capital intensive, historical returns on capital have been Ok , but not great (6-16% ROE, 8%-11% ROCE in the past)

- The business is also energy intensive, it requires both, lots electricity and and natural gas. Prices for both inputs are rising strongly and Germany might not be the best country as a location

- The company had to write down a significant part of an US investment in 2020 in an amount of almost 24 mn USD. So far, their move into the US doesn’t look like a great success.

- The business relies mostly on short term contracts (order book year end is on avg. 2-3 months), some sensitivity to the overall economic cycle is clearly there, especially as the steel and automobile industry are major customers

- They have a 45 mn unfunded pension liability

- Their “star product” Boehmite which is used in EV battery packs might face more competition and might not be required in future battery technologies (solid state)

- The company is located in the middle of nowhere

- Free float is limited (300 mn market cap), no famous investors on board

- The stock is not cheap (2021 P/E of ~20, P/B 3,6x) and only pays a small dividend (1%)

- overall, the company looks quite boring

The Pitch:

Nabaltec in my opinion checks a couple of boxes why I would call it a “hidden Champion”:

- The company is still founder/owner-run (founders own > 50%)

- Decent long term growth track record: Since IPO, 2007-2021 +4,9% CAGR sales, +11,9% CAGR EPS.

- The main business of flame retardants seems to be a long term growth sector, some studies indicate that a 8% market growth over a longer time is realistic.

- Export share outside Germany: 75%. (This indicates that their products are competitive internationally)

- Operating profitability (Gross margins, Operating margins etc.) has been continuously expanding over the past years

- the company is conservatively financed, most likely there will be only little net debt at YE 2021 (10-20 mn EUR)

- Although the company sells globally, it sources most of its inputs locally and is not negatively affected by supply chain disruption which makes it a preferred partner for local businesses (Audi, BMW etc.)

- accounting is very conservative, no capitalization of expenses, no use of “alternative indicators”

- very “down to earth” management with clear operating focus

- decent pricing power, according to management, cost increases so far could have been passed to customers

So far so good, but not overly exciting considering the valuation.

The “Game changer”: Boehmite & Electric Vehicles

Now let’s look at something more exciting: Kryptonite ähh Boehmite.

Boehmite is technically a “Aluminium-Oxide-Hydroxide” and has been around for some time as part of their flame retardant product line. It’s main applications so far has been for instance in electronic circuit boards and as a base for other applications. Although it doesn’t sound very exciting , it became exciting for Nabaltec.

Over the past years however it has been “discovered” as a very interesting material to increase the power density of battery packs for Electric Vehicles. In short, in the current Li-Ion batteries, a plastic membrane is dividing the liquids. However, especially the larger batteries develop significant amount of heat which could destroy the membranes and damages the battery. A thin layer of a special Boehmite on the membrane however seems to dramatically improve the heat resistance of these batteries. The principle is actually described very nicely in the 2020 annual report, pages 11-14.

There are other materials that could do the same such as HPA (High Purity Aluminium Oxide) but these are more expensive by a factor 3-5x (15-18 k EUR/ton vs. 3-3,5k EUR/Ton for Boehmite).

According to the CEO, this development is like a Jackpot in a lottery for Nabaltec for several reasons.

First, It seems to be that it is not so easy to produce the quality of Boehmite that is required and Nabaltec seems to be one of the very few players being able to do so in the world. They claim that they can do this because they have a fully vertically integrated production process.

Second, they can charge a decent price which enables them to earn EBIT margins of 30% (!!!) on this product compared to their historical 10-11%. Why is this the case ? In my opinion it has to do with the fact that the EUR value of this material per battery/car is small, around 20-30 EUR per car. However the quality is critical: The battery is the most valuable part of an EV and the quality of the membrane is very important. This is a pattern that can be seen in many situations: the suppliers of a relatively small ticket but important item often can earn very good margins.

And just to be clear: This is not at R&D stage, Boehmite is already used for this application, so far mostly at the higher end of EVs. This is from the 2020 annual report:

Capacity increase: New facility

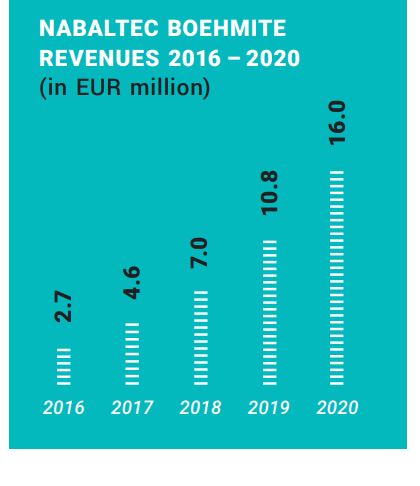

This clearly shows how Boehmite sales grow very dynamically. At a selling price of somewhere between 3000-3500 EUR per ton, Nabaltec has been most likely been producing around 5000 tons per year in 2020. According to some interviews (see links at the end), they have a current capacity of 10000 tons per annum in the current facility.

As EV production is just ramping up, it looks like that the existing capacity might be exhausted relatively soon. That’s why the board of Nabaltec has decided in December to build a new facility (next to the old one) that can produce an additional 15.000 tons. As this is not a “digital business”, they need to invest a “middle double digit” amount before the facility will begin production in the second half of 2023.

According to some rumours, they plan to spend around 35 mn EUR for the new plant, which however, at full capacity will have an EBITDA payback period of 2 years if the current pricing persits.

Assuming that the prices and margins remain the same, it is not difficult what this would mean for Nabaltec’s profits in the future: 15000x3250x30%= 14,6 mn additional EBIT p.a. Not bad for a company which has been doing 18 mn EBIT in 2019.

Solid state batteries & Wright’s law

As mentioned above, Boehmite is required for the current (liquid) Lithium Ion batteries and also likely for “semi solid state” batteries. however for fully “solid state” batteries, Boehmite is not required in larger quantities.

When I first heard about Boehmite, my first thought was: Well, nice windfall but this can be over pretty fast. Solid State batteries have been around for quite some time and one can hear news about some break through or another every few months or even weeks. In a recent announcement for instance Quantumscape, a SPACed Solid State battery company announced that their current prototype charges in 5-6 Minutes compared to 20-25 minutes for a Lithium Ion battery.

Speaking and hearing some experts, one could believe that these superior batteries will be available already in a few years (and at competitive costs). Quantumscape actually has a good paper on the basics of Solid State Batteries. However, these experts in my opinion miss one important point:

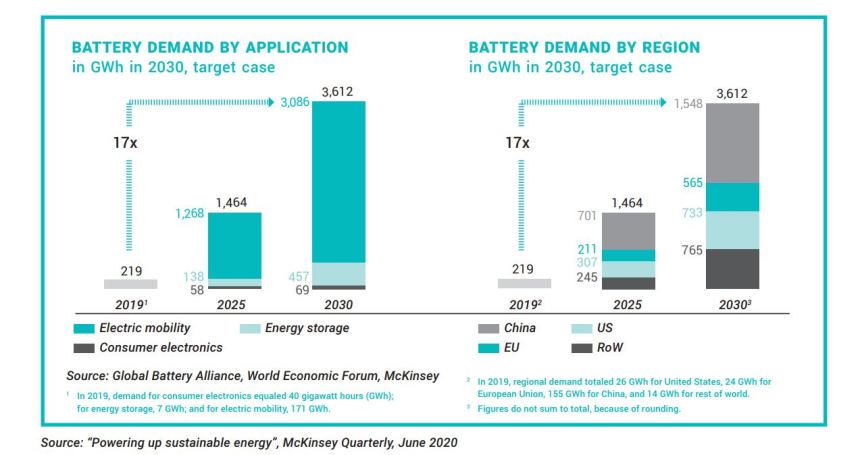

Lithium-Ion batteries in the mean-time will as well get better and cheaper. This is where Wright’s law or the experience curve is a relevant concept. It says that with each doubling of productions, cost per unit go down at a relatively constant percentage. There are a couple of estimates around, but in general, the learning rate seems to be somewhere between 15-25% per doubling of production capacity.

So let’s have a look again at a chart from Nabaltec’s annual report:

So to keep things simple, from let’s assume we are now at ~300 GWh per annum battery production capacity. Then we will see another 3,5 “doublings” in capacity until 2030 which in turn means a cost decrease of -90% for Lithium Ion batteries until then or -58% in 2025, assuming a 20% learning rate. Based on a Quantumscape presentation from August 2021, they expect a “commercialization” starting in 2025.

So any solid state battery coming onto the market in maybe 2025 needs to compete against a much better and much cheaper Lithium Ion batteries than today and the longer it takes, the cheaper and better Lithium Ion batteries will become.

This reminds me a little bit about thermal solar power vs. photovoltaic discussions 10-15 years ago, where many experts favoured thermal solar power as the superior technology, but photovoltaics just became cheaper and cheaper and won.

In my opinion, there is a significant probability that the runway for Lithium Ion batteries especially for EVs could be a lot longer than a lot of people, including OEM “experts” think. I might be totally wrong, but I guess this is also the major reason why the share price is not higher today, as a lot of investors do not want to have this kind of “certain uncertainty”.

It is difficult to get exact information about this topic, but the general consent at this stage seems to be that solid state batteries could become important in 2030 but might have a hard time to compete on price by then (emphasis mine):

Back in 2010, the cost per 1 kWh in lithium-ion batteries was over $1,000 and in the space of a decade, it has gone down nearly tenfold. It is predicted that the cost of lithium-ion batteries will keep going down and that by 2030, the average price per 1 kWh will dip below $60. It currently seems implausible that SSBs would drop so much in cost by then, but with the sheer number of companies actively working on this, a breakthrough that could allow it is not out of the question.

Share Price & valuation

Looking at the chart, we can see that Nabaltec underperformed the SDAX since its IPO but this was mostly because the IPO valuation just seems to have been too high before the GFC:

As for my return expectations, I build a very simple model:

I took the analyst estimate of ~2 EUR EPS for 2022 and let that grow by 5% p.a. Then I add the impact of the new Boehmite facility, assuming that it runs at 100% capacity in 2025. I also assume a flat selling price of 3500 EUR per ton and 30% EBIT margins.

This results in EPS of 2,61 EUR for 2023, 3,19 EUR for 2024 and 3,62 EUR for 2025. Assuming a PE of 20, this would result in a price target of ~72 EUR in 3-4 years or +100% compared to the share price of 36 EUR at the time of writing (plus dividends).

Interestingly, Nabaltec has not been discovered so far by many Cleantech/Electric mobility funds. Only one, the Belgian based Capricorn funds seems to have discovered them so far.

Overall this looks like an attractive risk/reward ratio to me. Therefore I decided to buy a 4% position at around 36 EUR per share for the portfolio.

Game plan:

The game plan is relatively easy: I will sit and wait how Nabaltec executes. I will also monitor progress on the solid state battery side. If Nabaltec reaches my fair value estimate earlier, i will most likely sell out as then the risk/return will look different. If the stock goes down because of an overall market decline, this would be one of the positions to increase. If for some reason the capacity extension doesn’t work out, I will sell.

Summary:

As I have tried to outline above, Nabaltec indeed looks like an extremely interesting opportunity that benefits from the mega trends towards electric vehicles.

There are of course a lot of risks, however at least for the next few years there is a very clear growth path and there might be other areas of upside as well, for instance the recovery of the US business and also the overall flame retardant business will benefit from the trend towards Electrification.

Overall, the company fits very well into my strategy focusing on small cap companies that look rather boring from the outside, are run conservatively for the long term and have some decent upside.

As mentioned above, I allocated 4% of the portfolio into Nabaltec at EUR 36 per share. In order to keep my cash allocation, I funded it partially through selling both, Euronext and ABB as mentioned in the comments.

Some more links/background

Supervisory Board :

https://www.br.de/nachrichten/bayern/strompreise-und-energiewende-energiesorgen-bei-nabaltec,SnceVh4

https://pegasussolutions.de/Boehmit

https://nanoinitiative-bayern.de/nano4emob/partner/nabaltec

Click to access Doc%20ATC%20HPA%20Market%20White%20Paper%20Final%20Mar%2020.pdf

Well, I expect 2023 to be the bottom… with Ebitda of 29 Mio and FCF of 19 Mio., the share is really cheap. Are you concerned about the prospects for 2024 or in general regarding growth/profitability?

There will be a post mortem soon….

For the record: Sold my Nabaltec position today in order to make space for another investment.

Now the share price can go up to infinity and beyond 😉

I respect your transparency. Did you find another gem worth taking the loss on nabaltec or is this out of frustration/dim view of nabaltec’s future?

I found another company that I like a lot. Nabaltec has become one of my “lowest conviction” positions. T

Funnily the stock indeed increased >5% over the last two days…

That happens every time I exit a stock. It’s part of my “Secret sauce” recipe 🤣

Extremely good numbers from Nabaltec and another increase for the expected 2022 earnings. Plus they almost seem to apologize for an extra Tax profit of 0,77 EUR per share:

https://www.eqs-news.com/news/corporate/nabaltec-ag-mit-fortgesetztem-umsatz-und-ertragswachstum-in-den-ersten-neun-monaten-2022/1698025

I added another 0,5% to the position at current prices.

Could not find anything about cash flows. Do you have information about Working Capital movements YTD?

Click to access DE000A0KPPR7-Q3-2022-EQ-E-00.pdf

Working capital has increased slightly, but a lot less compared to petrochemical companies. Operating cash flow equal to 2021 at 30 mn YTD. Here is the link to the full report.

Click to access DE000A0KPPR7-Q3-2022-EQ-E-00.pdf

Any news about Cash Flow and Working Capital. Could not find it in the press release 🙂

Added to Nabaltec today. 1% of Portfolio value at 20 EUR per share.

Sold some Nabaltec today at ~27,70 EUR (1% of portfolio). Reason: Risk Management. Winter is coming.

Good article with a very interesting angle. It may take time for solid-state batteries to take share from Li-Ion batteries, but have you looked into the risk of Li-Ion batteries being substituted by supercapacitors and hybrid supercapacitors? Thank you.

To be honest, I never heard of them being considered for ev. Any links here ?

It’s a relatively new concept for me as well. It’s unclear to me what the pros/cons and differentiating factors vs SSB are, but there seems to be some advantages over both Li-Ion and SSB (at least on paper). Here is a link that explains the concept at a very high level but there are more out there.

https://www.digitaltrends.com/cars/why-do-evs-charge-slowly/

I guess the technology is still in its very early stages but some people believe it take share from Li-Ion batteries. I was curious to know your take on how likely this is as it would potentially be a threat for Nabaltec (long-term)

added a little to Nabaltec today (around 0,45% of the portfolio) at 27,7 EUR. Reason: despite the obvious risks, i see an attractive risk/return profile at that valuation.

What about the current crash to 26€ per share? Worth buying the general dip or do you think there is something else behind it?

Difficult to say. In the long term, this all should work. In the short term they need a lot of natural gas to run the production. Iguess you see the problem….

Added ~0,5% Portfolio weight into Nabaltec at 32 EUR per share.

Here is another aspect to the battery puzzle.

Chinese EV manufacturers, BYD in particular, have been pushing hard for LFP (Lithium iron phosphate) batteries. Tesla’s Shanghai factory also uses that technology, and we can expect these batteries to become a larger part of the world market for EVs and battery storage.

LFP has a few advantages over lithium-ion:

+ cheaper

+ not toxic

+ not flamable

+ less degradation (completely charge and discharge without impacting cycle live)

+ no cobalt

Drawback:

+ lower energy density

For vehicles with large batteries, it still makes more sense to use lithium-ion. For most use-cases and stationary stoarge, LFP is superior and will probably also imporove on enrgy density measueres.

https://en.wikipedia.org/wiki/Lithium_iron_phosphate_battery

where did you get the 20-30€ per car ball park number? Too me this sounds high. And don’t forget – in automotive you have to deliver 2-3% yoy cost down 😉

Nabaltec Investor Relations. Yes, tere is cost pressure, however there are also not enough batteries 😉

ongoing cost pressure was also clearly behind the move from HPA to Boehmite.

good argument

Hello, many thanks for your write-up on this.

I have come across your blog just recently so excuses me if I am not fully familiar with the mechanics and details.

In the picture you used it says „Sponsored Post“ in the top left. Does this mean that the company is a sponsor of your website or that it has sponsored the generation of this article specifically? Thanks for showing transparently if indeed true, was just wondering how you think it impacts your content.

Regards Sebastian

Thanks for the comment. And no , no sponsoring on this blog. I did cut and paste this from a google search result which itself seems to have been a sponsordd post.

I actually pay for keeping the blog ad free.

Did some more cut & paste. Looks better now 😉

What I like about your analyses is the practical relevance with an analysis that is both economically and engineeringly comprehensible.

Dealing on regular basis with players along battery value chain, I see a very large gap between performance in the laboratory and in the car for solid state. There are good reasons why so many predictions on SSB have not materialized.. and as you say.. the productivity train through use in the field is rolling for LiIon.

You may also check upcoming battery exchange technologies.. this will come for sure as it is in everyone’s favor (automaker not having dependency on cell supplier, more attractive car prices, attractive biz model for changers). These guys would go for LiIon for sure.

I think biggest risk for your hypothesis is substitute for companies product. Here I am not convinced that there are no other / cheaper solutions.

Thanks for the insight. With regard to substitutes: This is clearly a risk, however at a cost point of 20-30 EUR per vehicle it might be just “good enough” for some time.

With regard to European OEMs, Nabaltec also has the advantage of being “local”.

I am not sure that your argument of being “local” accounts on this component level. The coating material is part of the cell and these are typically also sourced from big players (CATL, LG, SK, Panasonic). Automakers try to add value on the battery modul level (so putting these cells together into a system and doing assembly of course). Well, there is hope for European Battery Cell producers like Northvolt… but it is hard to kick the big players out (the from you mentioned productivity effects of course also account for these companies).

So it will probably not change that Nabaltec does a lot of biz in Asia.

What is promising is current adoption of boehmite as coating material – checked big selling vehicles in tear down data base a2mac1 for their coating material and AlOOH pops up regularly.

Why would these big cell supplier not integrate into AlOOH as well if this is so profitable?

Good point on local.

For the big players i guess the overall money value of the product is to small for the capex required.

SSB might not be a pressing threat as you analyzed. i did a simple search of this material in Chinese, doesn’t lead to any interesting/familiar EV batteries technology/company. Do you have checks on the customers/potential customers?

As far as I understand, they ship a significant amount of material to Asia. In the future, the European OEMs will be natural customers for the Boehmite.

thank you for this research, I have heard good things about them but never researched them myself because their website looked too difficult to understand what they do. I really like investing in companies that plan to build a new factory.

Hello memyselfandi007, this was a very interesting post. I suggest that quantumscape is not the place to look on solid state batteries though. Blue Solutions, a Bollore subsidiary, has product in use already, I think it is Daimler that is using them. Best,Steve