Knorr Bremse AG: German Mittelstand”Hidden Champion” with a few issues

Intro:

Knorr is a company I have been looking into now for some time. It is one of those “hidden Champions” that Germany is famous for. As I drive by their HQ on a regular basis, I decided to have a deeper look into them.

History:

![]()

Knorr Bremse has a very interesting history. The company was founded in 1905 in Berlin and for a few years, BMW (in its original form) was actually a subsidiary of Knorr. In 1985, Karl Herrmann Thiele, who initially joined the company in 1969, took over the majority from the Knorr family and developed the company into a Global Player. The company is now headquartered in Munich and only went public for 80 EUR/share in October 2018.

Karl-Herrmann Thiele

Thiele died quite surprisingly in early 2021, the heirs still own around 59% of the shares via a foundation.

Thiele was a typical “Patriarch” and clearly had issues to cede control.

His son, who was groomed as successor left the company in 2015, his daughter had a position at Knorr but little managerial responsibility. At the time of his death, Thiele’s net worth was estimated to be close to 20 bn EUR.

Based on his will, the 59% share holding in Knorr is supposed to move into a foundation, however it looks like this is still work in progress. To me it is not clear, if and how the family currently influences things at Knorr.

Management issues

Knorr Bremse at the moment does not have a “real” CEO, currently the CFO is running the shop after the previous CEO had been fired in March 2022 after around one year. Among other things, he unsuccessfully tried to bid for Auto supplier Hella which for most observers did not make a lot of sense.

Even before, many CEOs had only very short tenures at Knorr. Michael Buscher had the job from 2013-2014, his successor Klaus Deller lasted 5 years. His Successor, Bernd Eulitz lasted only one year.

The previous Head of the supervisory board, Klaus Mangold also had a quite mixed reputation. According to many rumors, Thiele still basically managed the company although hew was only “Deputy Head” of the Supervisory board. He also seemed to have been quite erratic in his later years.

On the plus side, the current Chairman of the board, Reinhard Ploss, the former CEO of Infineon, is considered to be one of the better managers in Germany. As of the time of writing, Knorr still hasn’t found a CEO, but overall, I do think that things can only get better from here.

The business:

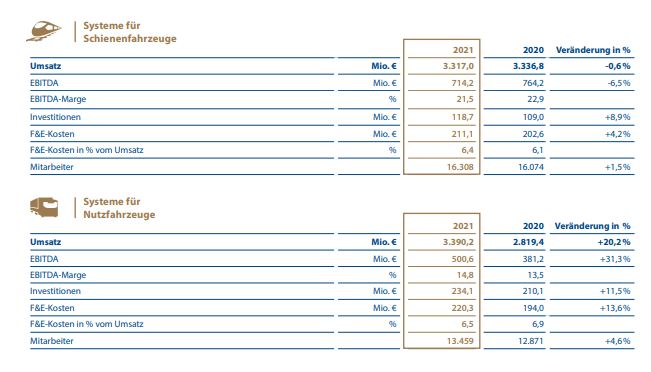

Knorr specializes mostly in complex braking systems both, for trucks and trains. The train and truck segments were more or less equal in sales in 2021, but profitability in the train sector is significantly higher:

Even in the difficult year 2021, the rail segment showed an EBIT margin of 19% whereas the truck segment “Only” made ~8% EBIT margin. ROIC is quite high, before Covid the return was around 30%.

Knorr also tries to become a key player for automated driving systems in the truck segment.

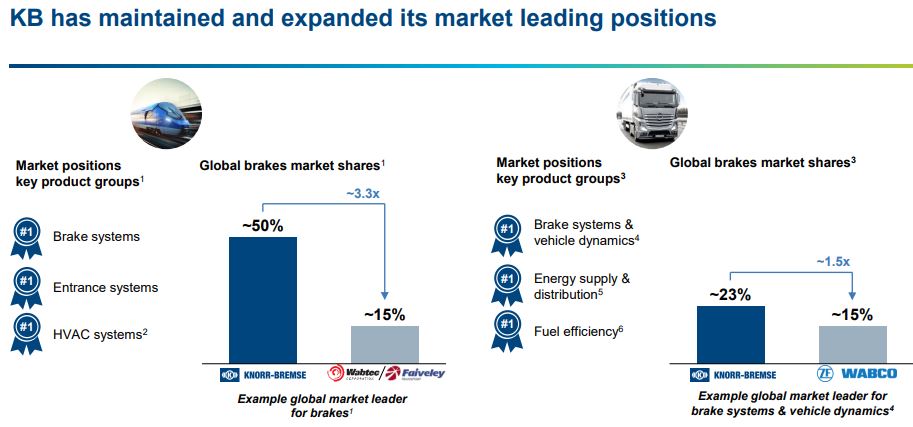

Aftermarket sales are at around 30-40%, with a higher percentage in the rail business compared to the truck business. This might also explain part of the higher profitability as well as the global market share of Knorr in both segments (according to the Knorr IR presentation).

As Knorr has dominating market shares in its core product categories already, growth will come mostly from growth of the overall segment and potential “horizontal” growth into new products for the same customers.

My explanation for the high margins in the rail business is a combination of a high “aftermarket” share in sales, i.e. spare parts (currently 40%, up from 33% in 2017) and a certain level regulation especially in the rail sector. This seems to resemble to a certain extent the Aerospace sectors, where the regulation provides significant barriers to entry.

Knorr seems to have created something like a standardized production system, that ensures the same quality across its ~60 international production sites. From what I understand, the ability to produce locally at a high quality standard is also one of their competitive advantages.

Fake Knorr Bremse:

There is an interesting story on the website that someone created a complete fake Knorr Bremse outlet in Hongkong:

After months of painstaking work, “Knorr-Bremse Limited” turns out to be an entire counterfeiting ring. Not content to simply sell their own products locally under the name of the global market leader, the companies involved have hatched a radical plan to basically copy everything humanly possible: the company name in large letters at the factory entrance, the product including the Knorr-Bremse logo, outer packaging to match the original. Even the websites have confusingly similar URLs, and the firms have their own entries in the commercial register. Mattusch: “Evidently they wanted to make the business fully official at home and were planning to go international. Anyone who registers 40 brand names worldwide is looking to expand on a grand scale. Production capacities of around 2.5 million brake pads per year are another clear indication that they wanted to play on the international stage.” Apparently these product pirates don’t like to do things by halves, even if their methods are quite shameless.

Employee attractiveness

Both, in Glassdoor and Kununu, reviews are mixed. Interestingly, Knorr requires a 42 hour work week, which is quite unique. Overall, the employees seem to be very friendly and helpful to each other, whereas Management is seen quite critical, which might have to do with many changes.

Salaries seem to be a problem, too, especially adjusted for the 42 hour workweek.

2022 not looking good so far

The 6M presentation clearly shows that KB is struggling. Both, the Russia sanctions and the slow down in China have hit the company. Overall EBIT margins declined to ~10% and even the EBIT margins of the rail business only reached 14%.

One remark: With regard to the European energy crisis going on, I guess Knorr might be somehow less impacted. The company produces globally for local markets, so in contrast to some other players their competitiveness in local markets should not be hurt that much by the current turmoil. Of course they do have increase in input costs, but I assume that after some months they can pass on this to clients.

China Exposure:

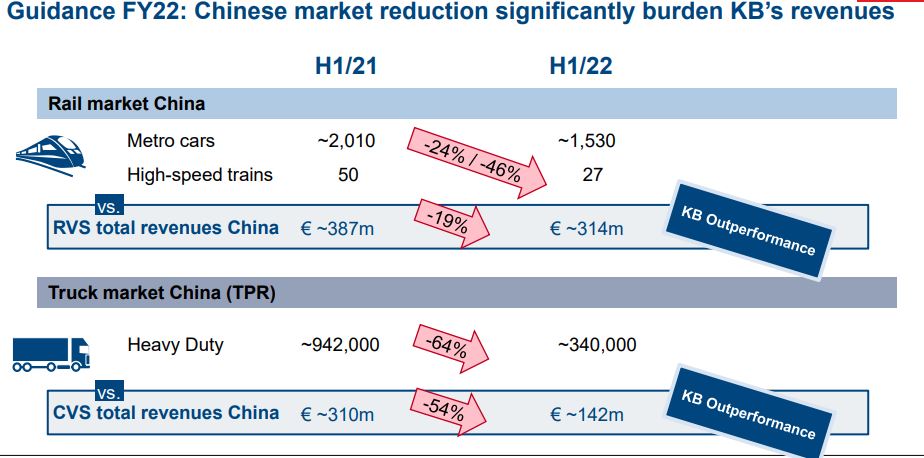

Around 30% of Knorr’s sales come from Asia, about half of this is China. Knorr has been an early entrant in China and has 3 different companies operating and producing locally. As with other German companies, my guess is that the share in profitability of the China business is much higher. China has been stagnating already in the first 6M 2022 how this chart shows from their 6M presentation:

It also shows how dramatic the current slow down in China is in these sectors.

Share price:

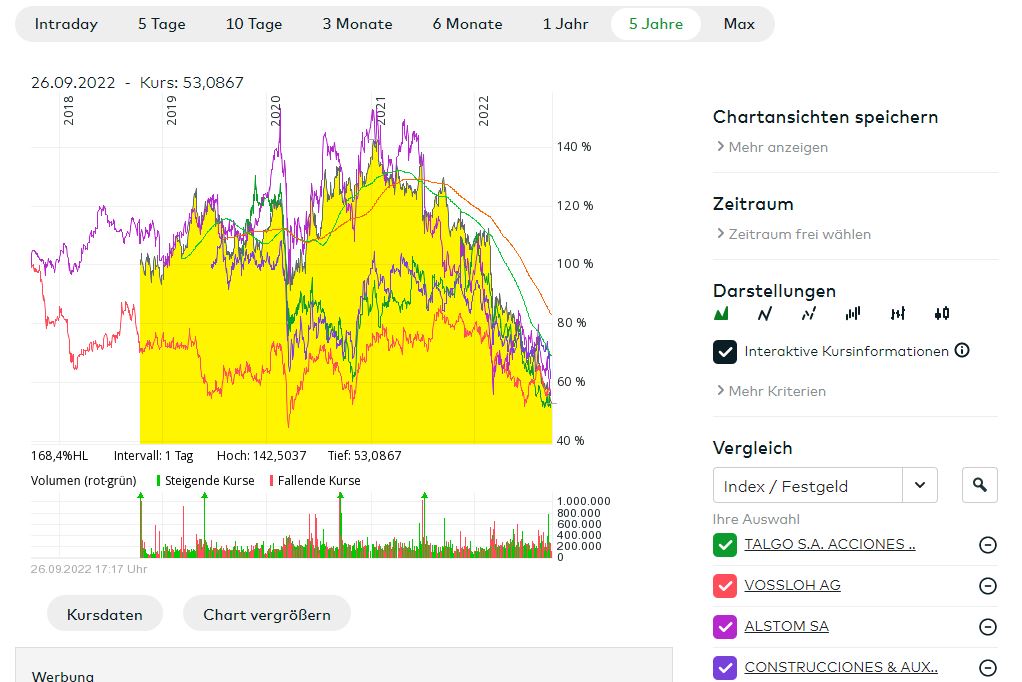

I guess both, the uncertainty with regard to the leadership and also the issues in the first 6M have taken their toll on Knorr Bremse as one can see in the share price which has lost ~60% since the last 12 months:

However, also other European rail related manufacturers are struggling as this chart shows:

Both Spanish train makers, CAF and Talgo are struggling, as well as Alstom, only Vossloh, where Thiele personally held a majority stake, is doing better.So there are clearly overall headwinds in the rail industry at the moment and I hae no idea if and when this cycle will turn.

Valuation:

At the current share price, Knorr has a market cap of 7,1 bn and an EV of 8,7 bn EUR. Knorr ist guiding for 6,9-7,2 bn in sales in 2022 and an EBIT margin (after all effects) of 10,5-12%.

This result in a predicted range for EBIT from 725 mn EUR to 864 mn EUR or a midpoint of around ~800 mn EUR, which would translates into ~11x EV/EBITDA.

“Reversion to the mean” potential

Knorr Bremse could be a potentially interesting “mean reversal” story. The big question is, what is the mean profitability for Knorr Bremse ? Looking at historical numbers via TIKR, from 2007 to 2021, Knorr’s average EBIT margin has been 12,7%, so compared to 2022 estimated 11,3% there is some upside.

The bigger “mean reversion” potential would be with regard to valuation. 11 EV/EBIT is a quite low valuation for “top tier” industrial companies. This is a small comparison where looked at some peers:

| Peers | 2021 | |||

| EBIT Margin | Return on capital | 2021 Growth | EV/EBITDA | |

| Burckhardt | 9,20% | 15,50% | 4,60% | 15,8 |

| Atlas Copco | 20,50% | 24,50% | 11,10% | 15,9 |

| Honeywell | 21,70% | 17,70% | 5,40% | 13,5 |

| Wabco | 13,10% | 7,10% | 3,50% | 16,8 |

| Ingersol Rand | 13,20% | 5,90% | 29,70% | 18.7 |

| Avg | 15,54% | 14,14% | 10,86% | 16,1 |

| Knorr Bremse | 13,20% | 22,50% | 8,90% | 11,0 |

So looking at the peers, we can see that currently, a “High quality” industrial is trading somewhere at around 16x EV/EBIT, which would indicate significant upside for Knorr in case they go back to be seen as a high quality industrial.

So combining the avg, EBIT margin with current sales and assuming a target EV/EBIT of 16x, Knorr could trade at around 80 EUR per share or 83% higher than the current share price.

However, and this is a big however, Knorr at the moment clearly deserves some kind of discount due to the uncertainties around ownership, management and geopolitical issues. My gut feeling is that at least a discount of 20-30% would be justified.

Pro’s and Con’s

So let’s look at this stage at the Pro’s and Con’s of Knorr so far:

+”hidden Champion” with high margins and High market share and some clear competitive advantages

+ very interesting business area rail, regulation is a barrier to entry

+ high aftersale share, increasing share in total shares

+ Global standardized production system as another competitive advantage

+ KPIs like ROCE, FCF etc. easily available, very limited use of “adjusted numbers”

+ cheap in relative terms to its Peers, some mean reversion potential

+ especially rail segment with potentially good long term tailwinds

+ first insider buys from executive team

+ Company seems to be “underfollowed”

+/- Acquisition history /capital allocation not bad but not great

+/- employee job satisfaction ok, but not great

- founder died, many CEO changes, currently leadership and shareholder influence unclear

- 2022 is very challenging for Knorr and other players in the field

- Significant China Exposure, market share in the US is relatively low (Wabco)

- Truck segment is significantly more competitive than the rail segment

- Management & Supervisory board very German

- high dividend pay outs limit flexibility in the future

- High market share limits growth in core area

- Rail cycle on a downwards trend

- Working capital issues in the first &;

- time lag in passing through price increases

Summary:

Overall, I find Knorr Bremse a very interesting company, however I cannot motivate myself to invest at this time.

The main issues are as described above, that there seems to be “leadership vacuum” which, combined with the current sector specific and overall downturn (plus geopolitical risk) creates the risk that the business might suffer and might not be in a position to make the required adjustments quickly.

I’ll therefore remain in a “watch” mode to see how especially the leadership topic develops.

New CEO has been found. Never heard of that guy:

https://www.faz.net/aktuell/wirtschaft/unternehmen/marc-llistosella-zu-knorr-bremse-18384905.html

Hi, interesting post. Thank you 🙂

A couple of questions if I may.

1. With energy prices skyrocketing especially in Europe and Knorr-Bremse using a lot of commodities in their products, how to you see their potential to pass on price increases?

2. Will international competition take market share from Knorr-Bremse as they have lower energy costs and can thus are able to offer products (even with longer and thus more expensive transport) cheaper?

3. What was so special about Thiele, why is it still so difficult to replace him, what happens to the stake of the family and what do you mean it can only get better from here?

Would be great to here your opinion on that.

Thank you! : )

Ignaz,

thank you for the comment.

With regard to 1) and 2): As mentioned in the post, to my understanding, Knorr Bremse mostly produces local, i.e. no exports from Europe to Asie etc. So in theory they should not be disadvantaged vis-a-vis the competition.

With regard to Thile: He actually created the company as it is now and seems to have made all the decisions. This is not so easy to replace, especially as he didn’t groom a successor.

mmi

Thank you for looking into this share.

I am a little more optimistic than you and have started a first purchase at 45. Especially with the strong position in Rail, and also a strongly growing service and aftermarket segment, this should be a safe bet.

Concerning leadership: I prefer the current constellation with established and respected leaders of segments and resorts from within the company, and no CEO. It seems to work quite well.

Thanks for another insightful study. I was surprised to see Wabco mentioned as a peer though. WABCO made air brakes for trucks but it was acquired by ZF Friedrichshafen in 2020.

Another company, WABTECH (publicly traded as WAB) is active in the rail business. It started as a sister co of WABCO and was originally active in the business of brakes for trains. It then acquired Faively and a part of GE. Its ROE is only around 5%. Interesting contrast with the more profitable Knorr rail business.

Thanks, I might have mixed them up.

WAB performs good, especially related to Knorr. I think Thiele was responsible for the success of the Company, he was brilliant. After his death, the situation at Knorr is similar to the situation when he started as owner.

Thank you for the post.

I’ve only been here for a short time, but hats off to the whole fund you’ve put together here. 🙂

I would have probably already been convinced by your arguments and would have invested at least a part in the stock already. By the time the uncertainties around management and ownership have cleared, it’s probably “already too late”.

How long do you usually take to analyze a stock before deciding to invest?

What I often miss is the historical background of a stock or why the share price has developed the way it has in the past years. How do you approach an unknown stock?

Thanks

KR

FIL

hi, thanks for the comment. It depends, somehow I decide rather quickly for instance for special situations. Sometimes it takes many years until I feel comfortable to invest.

I approach most stocks with a high level overview of the numbers and then I try to move directly to annual reports if I find the company interesting.

Hope that helps.