All Danish Shares part 13 – Nr. 121-130

Slowly we are reaching the end of my Journey through Denmark. Another 10 randomly selected stocks, this time yielding two “watch” candidates. Only 48 now outstanding. Enjoy !!!

121. Strategic Investments A/S

Strategic Investments is a 52 mn EUR market cap investment vehicle that invests into securities, private equity and real estate. Investor relations is in Danish only. Looking at the share price, there doesn’t seem to happen a lot of value creation here. “Pass”.

122. Copyright Agent

Copyright Agent is a 2 mn EUR market company that “is a legal-tech company that helps professional content creators to ensure their original work against misuse by other companies.” This 2021 IPO is actually growing quite fast, but losses are growing faster with an EBIT margin of -50%. Cash at June 30th at the current burn rate only lasts until year end 2022, so capital increase will be coming soon (or bankruptcy). “Pass”.

123. Gyldendal

Gyldendal is a 125 mn EUR market cap book publisher and operator of book stores. After doing nothing for 20 years, the Stock saw some interesting price action in 2021 which has now mostly reversed:

I have no idea why that happened. The stock looks expensive from any angle and they showed losses for the first 6M 2022. Maybe it is an real estate play but for me it is a “pass”.

124. Dataproces Group A/S

Dataproces (with one s only) is a 10 mn EUR market cap IT consultant that went public in 2021. They do have revenues but are burning cash and don’t seem to have that much cash left which seems to explain the share price development. “Pass”.

125. NKT A/S

NKT, the 2,2 bn EUR market cap cable manufacturer is already an “old friend” of the blog. I invested into them as one of my first attempts to develop the electrification theme. I invested into NKT in June 2021 but sold them in early February 2022 for risk management reasons.

The stock has actually performed very well over the past months, especially relative to the market:

This was supported by very solid 6M numbers, especially the backlog increased a lot. Renewable energy requires a lot of electricity cables and NKT seems to be able to take its share. Their recent investor day yielded an interesting presentation on how they see the future. Overall NKT is clearly a stock to “watch”.

126. Brdr. A & O Johansen

A&O Johansen is a 211 mn EUR market cap distribution company that distributes supplies for the construction industry, mainly to craftsman like plumbers and construction companies.

A&O saw a rapid increase in its shareprice from the start of the pandemic until end of 2021, going up almost 4x:

Similar to Solar, the stock looks cheap, with a P/E of ~7 and an EV/EBIT of 6x. The issue clearly will be, how severely they will be hit by the expected slow down in the overall construction sector in the coming months / years.

As for Solar, the first 6M 2022 have been very good and A&O was quite optimistic about the full year. The only negative, as for Solar was that they had significantly into inventory.

Being a competitor to Solar, A&O is clearly one to “watch” closely.

127. Odico A/S

Odico is an 8 mn EUR market cap company that seems to be somehow active in robotics. The company does have sales, which are increasing (~2 mn EUR), but losses are also increasing. “Pass”.

128. Fynske Bank

Fynske is yet another small, 130 mn EUR market cap bank. The stock did surprisingly well in 2021. At first sight, this doesn’t look attractive. “Pass”.

129. Lundbeck AS

Lundbeck is a 3,4 bn EUR market cap biopharmaceutical company that “engages in the research, development, production, and sale of pharmaceuticals for the treatment of psychiatric and neurological disorders”. They seem to offer medication agains depression, schizophrenia and other mental illnesses.

Lundbeck has seen better days, with the shares down -75% against their 2018 peak.

In the first 6M 2022, business has been growing again, thanks to a new product that treats chronic migraine. At currently 12xEV/EBIT, the company doesn’t seem to be expensive, however as I have zero competence in assessing the portfolio and pipeline of a pharmaceutical company, I’ll “pass”.

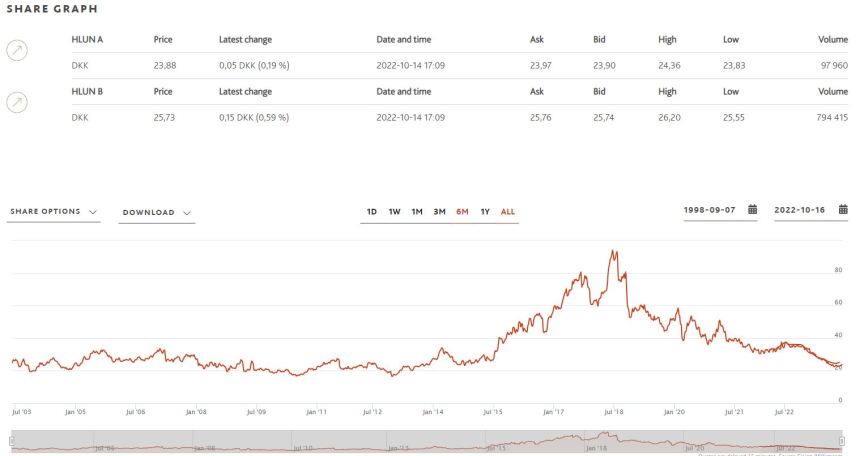

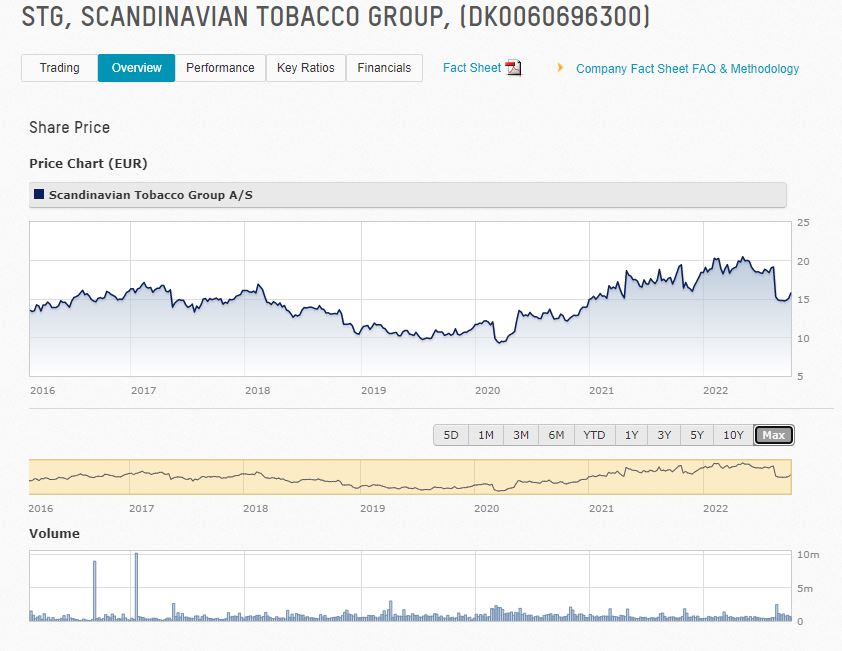

130. Scandinavian Tobacco Group

Scandinavian Tobacco is a 1,5 bn EUR market cap company, that as the name indicates, sells tobacco products in Scandinavia and other countries. The company seems to focus mostly on Cigars and Tobacco as such, less on cigarettes.

The stock didn’t do much over the past 10 years:

From a valuation perspective, the stock looks cheap with a P/E of 8 and a decent dividend yield. Profits have actually doubled over the past 10 years although the first 6M 2022 look a little bit weak. As many Tobacco companies, they enjoy very nice margins (20% EBIT, 15% ROCE). They also seem to play the “combustible hemp” market in North America.

For investors who have an appetite for “sin stocks” this could be interesting. For me it is a “pass” as I prefer to stay “out of trouble” .

A&O Johansen raises its outlook for this year’s revenue and profit.

Click to access upward-adjustment-october-2022.pdf

Hi, thanks for all the work you do – really helpful.

Was curious if you’ve looked at Mister Spex, a German eyewear retailer? 150m of cash and 100m market cap. Even if you deduct 60m of lease liabilities, still leaves you at roughly zero EV.