Panic Journal 5 – Ukraine/Russia edition: Is Europe really Toast, Energy Silver Bullets and the Weather

It’s time after exactly 3 months for some new ramblings on Energy, Europe and of course the weather and other stuff.

Bad news everywhere:

The last few weeks felt like a new catastrophe is happening every week or so. Italian elections, the British Pound trading like a Shitcoin, Putin threatening the West with Nuclear Weapons, Energy prices for retail customers skyrocketing, potential Blackouts being a real issue in Europe this winter, steel and fertilizer companies shutting down in Europe, creating supply chain issues down the chain and in addition, rumors about regime change in China and/or preparations for an attack on Taiwan are surfacing every day.

I have been listening to some US podcasts and there seems to be consensus on that Europe is Toast. Even a comparison to the “Arab Spring” was made with the dire prediction that Governments will topple like Domino tiles. I don’t want to sound arrogant but one word of advice to my American readers: European countries are actually all Democracies and if people don’t like their leaders they will elect new ones.

The FT was just running an article about the coming Deindustrialization of Germany with the example of BASF threatening to “leave” Germany and Billionaire Ray Dalio thinks that Europeans are not working hard enough.

Having we seen this movie before ?

Writing this blog now in my 12th year, the situation felt somehow similar to the Euro crisis and I actually found a post that reads eariely similar from February 2013:

If you follow the financial media, the world seems to be jump from one life threatening event to another. “Fiscal cliff”, vote in Italy, “the sequester”, speech of Japanese BOJ chief; Bernanke speech etc. etc. The media wants to promote the picture that the whole world is “walking on a tight rope” and if any one event goes wrong, doom is ensured. As a result, people are “glued” to their TV sets, Bloombergs etc. in order not to miss the one “big event” which will change it all.

I am clearly not saying that there aren’t any issues. there are many and as mentioned before, Natural gas scarcity will be a problem for some time and not only this winter.

“De-Industrialization” of Europe because of Natural Gas

Let’s start with this one: Yes, the current situation is difficult. Maybe a few things to clarify: Yes, it was clearly a strategic mistake not to diversify Natural Gas resources away into LNG and building LNG terminals as a back-up (as for instance the Baltic states have done). However, from a pure economic perspective, transporting natural gas via pipelines is always better and cheaper than to liquefy gas, put in onto a ship and to gasefy it again.

Europe will clearly pay the price for this strategic mistake, but in 2-3 years time this will normalize. What do I mean with normalize ? Very simple: LNG is a global commodity and more demand will mean higher prizes for everyone around the world. One can see this already right now. A curious example is the US region often called “New England” that for some reason is not connected to the American Gas grid but is importing all its gas via LNG.

So for those countries that rely on LNG (especially Asia), the European demand will increase prices for everyone. But also for instance in the US, where domestic gas is very cheap, gas producers will not be happy to sell their gas for a fraction of the price to local customers when there is a chance to sell it for a much higher price into the LNG market. So the current cost advantage will become (significantly) smaller over the next years and long term investors will factor this in.

Another argument that often pops up is that you can only run “real” industry if you also own the resources. Especially from the US side, “Energy independence” is being seen as a target in itself.

Interestingly, the reality says something different. Very few countries manage to use their own resources efficiently, most resource rich countries actually fall into the “resource curse” trap. The big industrial success stories are mostly resource poor countries like Japan, South Korea, Taiwan or Germany that became rich by concentrating on “value add” activities.

Instead of energy independence, in my opinion the story must be of an “energy diversity”, i.e. “spreading your bets” and not trying to rely on any one technology or source. The broader the better.

Another aspect to mention here is that due to inflation, the cost of setting up new plants etc. has risen a lot. So the case for a new chemical plant in an area with cheap gas prices is not as straight forward as the capex required is significant and has to compete with maintenance capex of a much cheaper existing production site.

So no, I don’t believe in ultimate full de-industrialization of Germany and Europe. Yes, there will be changes and some activities will shift more into other regions, but the truly “value add” activities cannot be shifted so easily because they depend much more on know how than on cheap input prices.

Energy: There are no silver bullets

These days you see newly minted experts coming out of their holes and claim that they have the ONE solution that solves all energy problems. Be it Nuclear Energy (takes a long time, is expensive, maintenance intensive – France), Fracking in Germany (no, Fracking is not so easy) or a direct 100% switch to Green Energy (obvious: the sun doesn’t shine at night and the wind doesn’t blow all the time and then there is “Dunkelflaute”).

The difficult reality is that the future will look a lot more complicated. In order to both, decarbonize and make a country like Germany more independent from fossil fuels, many technologies will play a role.

Renewable energy (solar Wind) clearly are important, but also for instance Heat that gets produced in industrial process should not be wasted but “coupled” with district heating systems. Fraunhofer Institute estimated for instance that almost 10% of the required energy for existing district heating systems could be generated by using excess industrial heat.

Another interesting technology is Geothermal. Fraunhofer again estimated that 25% of the energy required for heating in Germany could be produced via Geothermal energy, again in connection with district heating.

Again, this is not a silver bullet but a 10% reduction here and another 25% there and suddenly we are talking about a significantly reduced demand for fossil fuel through a mix of technologies that are already existing and cost competitive at scale.

Electricity demand need to become more elastic, existing fossil resources have to be used better. Renewable Natural Gas or Green fuels can play a role in areas that are hard to de-carbonize electrically (airplanes, ships).

This sounds complicated and it will be messy, but there is also a big chance: All these technologies, either existing ones that need to be scaled or new ones will not only work in ermany but could be also very valuable for other countries that face the same problems.

Therefore I also see a tremendous upside here in the medium to long term for those who develop and scale the required technologies.

Nuclear: Difficult but worth to develop further

Nuclear fission clearly has its own problems as our French neighbors can maybe explain better. The current technology that is used is neither cheap if one factors in all the real costs (Capex, Insurance) nor super reliable. It also takes ages to built a new reactor.

The biggest problem in my opinion is that the technology hasn’t been developed further for decades. Another problem is that in the future, big centralized plants are less effective than they are now.

On the other hand, for Germany, I think it would clearly make sense to run the existing reactors for more time instead of firing up coal plants.

I would be very happy if someone would figure out fusion technology in the near future but that is highly improbable. If society could agree on what will be done with the nuclear waste and the “real” costs would be allocated, than there might be a role for Nuclear in the future, but in my opinion it is clearly not the silver bullet that some claim it is.

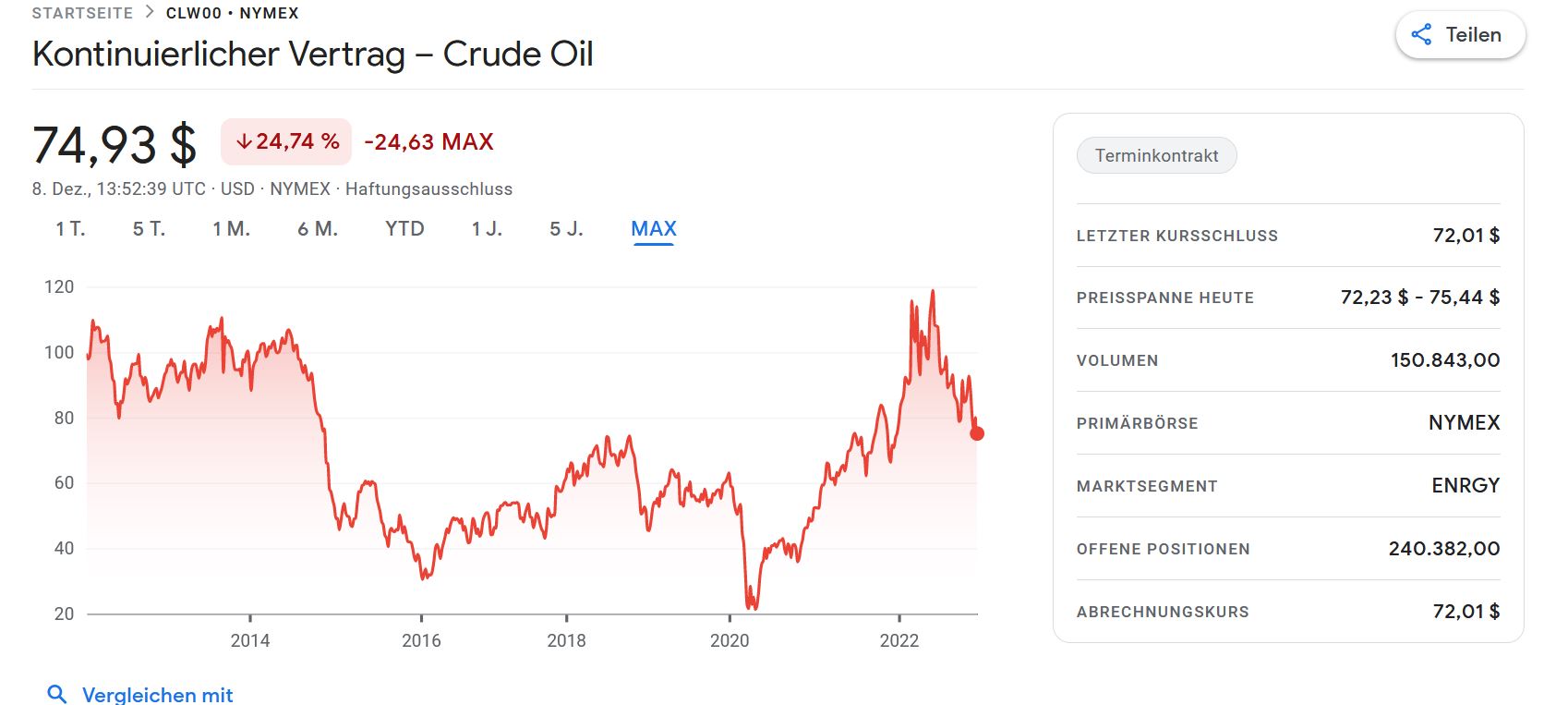

Oil & ESG Investing

The prices of oil and other commodities are notoriously hard to predict and trying to explain price actions by one factor is always a pretty stupid exercise. Nevertheless, as I wrote last year, David EInhorn and some other prominent investors blamed “ESG Investing” as the sole reason for increasing oil prices. With the war in Ukraine, oil looked like a “No brainer” one way bet to great returns. With oil prices now at around 70 USD the question is of course: Why is that ?

The amount of Assets managed under some kind of ESG mandate is still increasing so in theory oil should be more expensive. But the truth is that other factors are at least as important such as the recent easing of sanctions on Venezuela and a potential recession in 2023. The lesson at least for me is: Don’t ever believe in “single factor explanations” for any market price and try to separate ideology from your investment process.

Weather & German Gas consumption and storage

After a relatively mild November, where the required savings of -20% gas consumption were relatively easily achieved, December seems to become a cold month.

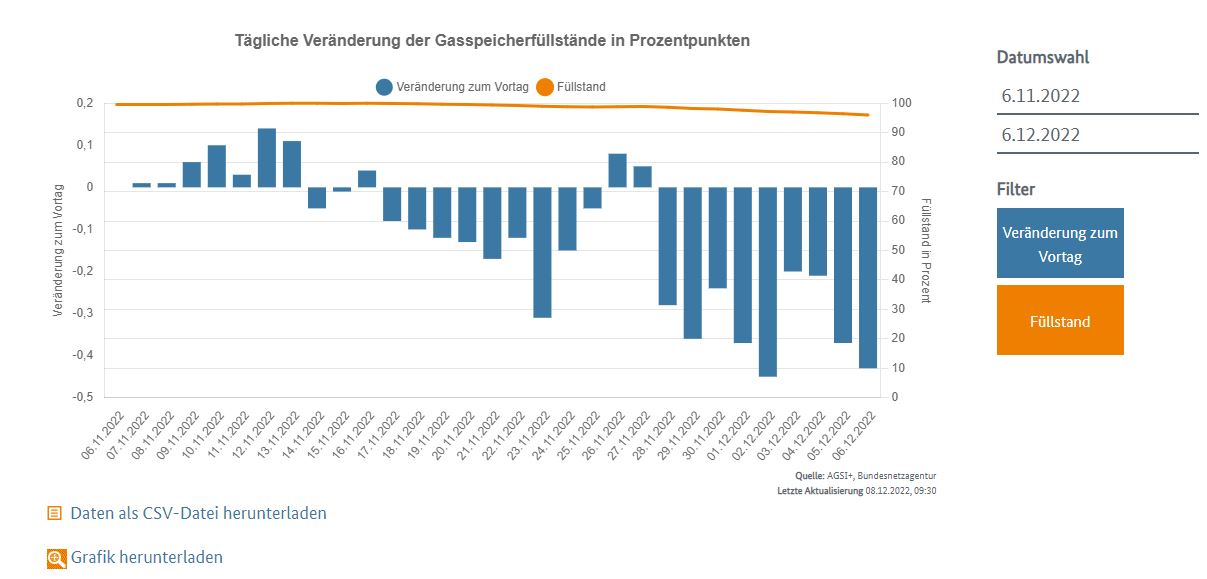

One positive surprise is that the “Deutsche Netzagentur” is coming up with new, quite useful statistics on their website. The most interesting one is in my opinion the daily statistic on how much in percentage points the storage gets depleted. This is the most recent version:

The orange line on top is the current percentage to what the storage is filled, the blue bars show the daily change. So on December 6th for instance, in order to satisfy consumption on that day, 0,45% of the stored Gas had to be taken out. Now December 6th was a cold day with temperatures around 1-3 degrees Celsius, but not a very cold day.

The last 2 days have been colder and next week might be even more cold according to the weather forecast.

It will be very interesting to see how storage will be depleted on a really cold day with -10 Celsius at night and maybe -3 to -5 during the day. Often, the weather gets warmer around Christmas and Industrial consumption might go down during the Christmas holidays but the problem remains: If gas reserves are sufficient or not is mostly depending on the weather.

Insulation Basket/Investments

After a recovery in the respective share prices, I have reduced my Insulation basket to only 3 shares: Sto, Rockwool and Recticel. The main reason was, that I underestimated the contraction in housing. All these shares have exposure to housing and if activity drops a lot, they will be negatively effected. I have kept the 3 positions as these seem to be the most conservatively financed ones and the cheapest names.

Nevertheless I do think that there are a lot of interesting opportunities in the energy efficiency and energy transition space. This will be one of my focus topics going forward.

Ukraine/Russia

Whenever people in Germany complain about a hard winter and high costs, they should maybe inform themselves what is going on in Ukraine and how a really hard winter looks like. Yes, Ukraine gained some ground back from Russia, but as retaliation, Russia is bombing the Ukrainian infrastructure and many Ukrainians will neither have heating nor electricity in a climate where winters are much colder than here in Germany.

As I have feared from the very beginning, there doesn’t seem to be a quick end to this conflict. I remember one podcast early in the year with Mario Papic from Clocktower who mentioned that most conflicts in the recent history didn’t end with either a clear victory or defeat but rather they stalled and faded out when the frontline stopped moving. So far it doesn’t look like that so therefore assuming a quick end of the conflict should not be a base scenario for next year.

Emerging Europe has a 25% earnings yield currently (see tweet). Best place in the world to look for bargains today. Russia cannot attack the whole of its nationwide western front since it can hardly beat Ukraine alone, and if it does decide to go nuclear then everyone in the EU has far, far bigger problems than falling stock and asset prices. Far bigger problems. So seems like a bit of a no-brainer in terms of places to go looking for value, IMHO.

Another great post. I think this is one of the best blogs and I enjoy reading all of your posts. Thank you for sharing your ideas with us.

“Deindustrialisation” is too strong a word, many manufacturing countries like Japan/Korea/Taiwan already rely on LNG instead of piped gas. Might get a 1-2 year recession adjusting too higher energy prices.

The geothermal paper is interesting, I guess if Germany does not have many mining & oil companies (for survey data and drilling), the government would have to take the lead.

>If society could agree on what will be done with the nuclear waste and the “real” costs would be allocated, than there might be a role for Nuclear in the future, but in my opinion it is clearly not the silver bullet that some claim it is.

There is a nuclear technology called thorium malten salt reactor. In theory: no meltdown possible, thorium is abundant, recycling of existing nuclear waste is possible in the reactor (energy potential from it for whole Germany approx. 270 years), 80% less nuclear waste (with max. radiation duration 300 years vs. 1-2 million so far).

In practice: China started up the first prototype plant a few months ago, with the aim of going into series production from 2030. India is also building a prototype. Germany is unfortunately missing the boat here, because of the idiological demonization of nuclear energy. The official reason is the corrosion of salt water, but there are 2 practical solutions for this: Either via an alloy or replacement of the small reactors (China/India are unfortunately keeping quiet about which path they have taken…).

Yes, I read about that in Bill Gates book. That sounds like a very interesting technology.

I don’t think Europe as a whole is done and certainly Germany would be the last to fall but consistently high energy prices are quite simply poison and will kill everything it touches quickly.

Here in Finland for example my electricity bill has increased almost 10 fold which is wholly untenable,ironically propably something to do with Fortum’s massive multi billion euro blunder in Germany with formerly owned Uniper and our citizens paying the bill for that as well,it gets very cold here in the winter.

Plus we have a ‘new’ French built nuclear power plant here which has been in construction for over 20 years and has broken down again after running a few weeks :).

Sorry to hear that. Not sure however if Uniper has to do something with this. Yes, Fortum shareholders have lost money, but the stock trades around the level where it traded the last 15-20 years.

Not speaking as a shareholder as i don’t care about that but as their electricity customer,they’re 50% state owned and the more than 6 billion euro loss they made with Uniper made it necessary to recoup that loss somehow both for the company and the state budget as well,the taxes and dividends the state gets from them is a large piece of it and as such our largest producer Fortum’s electricity and heating prices have soared and we need a lot of both during winters so the feeling here is our citizens as always in the end are made to pay for some corporate mistakes in the end.

We used to buy lot of our electricity from Russia lately as well as part of our ‘green’ transition