All Norwegian Stocks Part 4 – Nr. 46-60

It is still January and I have managed to look at already 60 Norwegian companies, so this is good progress. This time, 6 companies made it onto the watxh list, although I would not consider any of them a strong candidate. Let’s go:

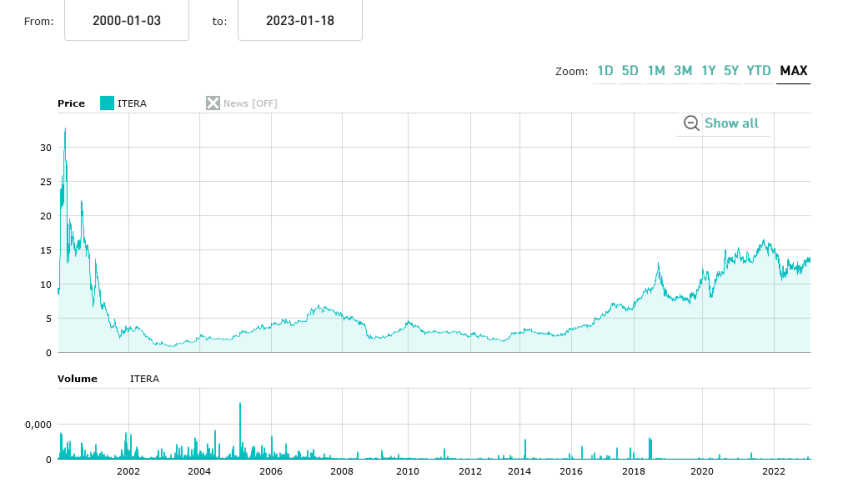

46. Itera

Itera is a 108 mn EUR market cap IT consulting company. The company has managed to grow topline consistently which is reflected in a relatively high valuation with a P/E in the mid 20s.

If I understand the business model correctly, a sinificant part is “near-shoring” IT employees in Eastern Europe.

The company was IPOed in the heydays of the dotcom boom and needed many years to regain the share prcie level from back then as we can see in the chart:

Unfortunately, in Q3 2022, the company saw a drop of around -50% in operating margins and the book to bill ratio dropped significantly. As a potential small competitor to Bouvet, I’ll put them on “watch” nevertheless.

47. SmartCraft

Smartcraft is a 300 mn EUR market cap SaaS Software company that provids solutions for Craftsmen and the construction sector. The company IPOed in June 2021, but other than many IPO peer from that vintage, the stock has done OK, trading around the IPO price.

That might have to do with the fact that the company is actually profitable with decent margins (20% net margins). However, the stock ios quite expensive, at around 40x trailing earnungs and 9x sales. This is pretty far outside my comoft zone, therefore I’ll “pass”.

48. Hynion

Hynion is a 6 mn EUR market cap nano cop that IPOed in 2021 and has lost 3/4 of its value since then. The company is running a few Hydrogen fueling stations in Norway and Sweden. Little revenue, large losses and a recent capital increase. “Pass”.

49. Bergen Carbon Sol

Bergen Carbon is a 32 mn EUR market company that is active in the “production of carbon nanofibers using CO2 and hydroelectricity and based on electrolysis process technology. Carbon nanofibers are a material with applications ranging from energy storage, protective clothing, flame retardant to oil spill remediation.”

Again an 2021 Vintage IPO that has lost money, but only 1/3. The company seems to be “pre commercial scale” without revenues but claims that they are on a good way to produce input material for batteries via a novel, energy efficient process.

For some reason, the got a new CEO in January 2023. Although it sounds kind of interesting, this seems early stage venture. “Pass”.

50. AEGA

AEGA is a 6 mn EUR market cap company is owning a couple of small solar assets. They do have revenues but bottom line they are making increasing losses. “Pass”.

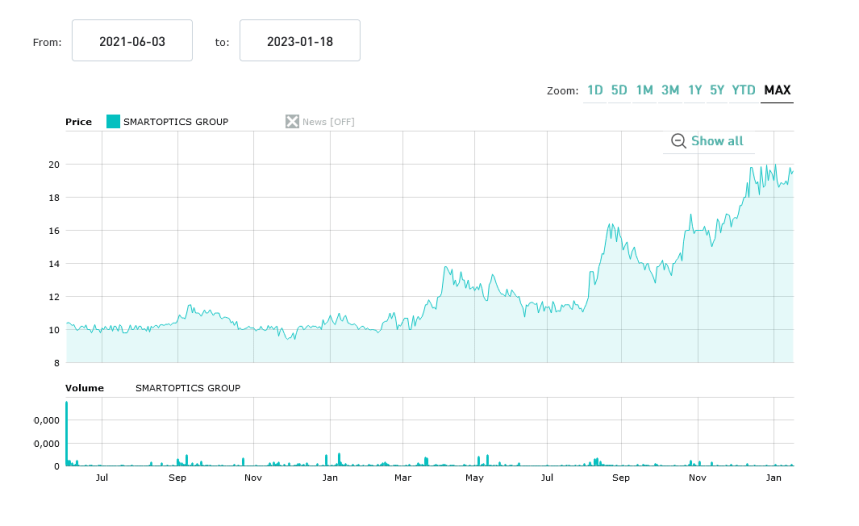

51. Smartoptics Group

Smartoptics is a 180 mn EUR market cap company that is offering “innovative optical networking solutions and devices for the new era of open networking”. Again a 2021 IPO, however this time the stock almost doubled:

The company is growing and profitable. They are guiding for “long-term revenue ambition of USD 100 million by 2025/2026 and an EBITDA margin of 17-20%.”. The stock is not cheap but also nut super expensive. I have little exeprience in this area but it sounds interesting enough to “watch”.

52. Nortel

Nortel is a 33 mn EUR market cap specialised TelCo catering to businesses. Again a 2021 IPO, but one that roughly trades around its IPO price. The company is a young business, founded in 2019. Gross margins turned posiive in 2021. In 2022, the company growed for the first 9M by 2,5x and there seems to be some scale effect and in Q3 even EBITDA turned positive.

Unfortunately the company only reports in Norwegian, but somehow I find it interesting. “Watch”.

53. Sunndal Sparebank

Sunndal is a ~25 mn EUR market cap local savings company that seems to offer a really juicy dividend yield. Business seems to be going quite well. The company seems to have IPOed in 2018. However, as I am not keen on local savings bank, I’ll “pass” again here as well.

54. IDEX Biometrics

IDEX is a 100 mn EUR market cap company that “engages in the design, development, and sale of fingerprint authentication solutions in Europe, the Middle East, Africa, the Americas, and the Asia-Pacific regions”. The company has very little in sales, is making losses and share count increases quickly. “Pass”.

55. Pioneer Property

Pioneer is a 43 mn EUR market cap property company that owns property in Norway, Sweden, Poland and the Netherland. For the last 5 years, the stock traded in a band between 95-105 NOKs per share through every crisis which is very strange. Not my area of competence, “pass”.

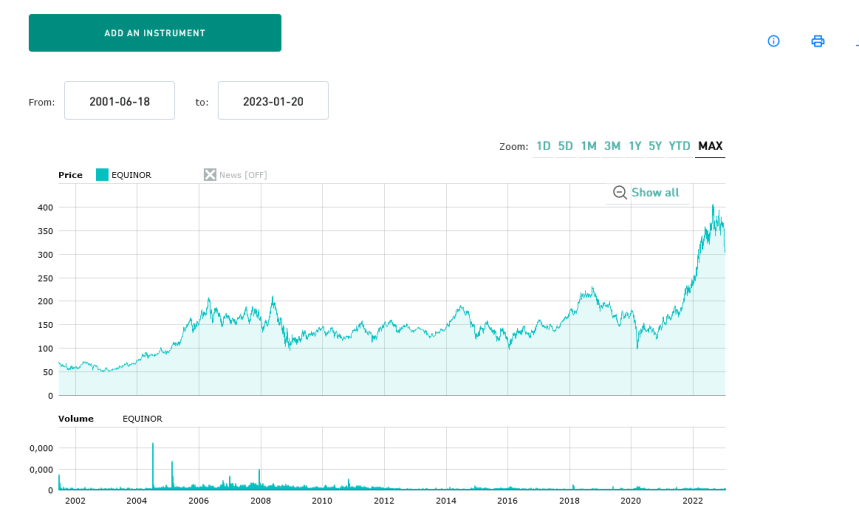

56. Equinor

Equinor is a 97 bn EUR market cap Energy juggernaut that at first sight looks ridiculously cheap at around 1x EV/EBITDA and ~5x P/E.

However, one very important thing to mention here is that every mutliple before tax is pretty meaningless, because Equinor, despite 70% Government owned, is subject to an addtional “petroleum tax” on top of the normal income tax which adds up to around 60-70% taxes.

Equinor is really one of the main beneficieries of the Russia/Ukraine war, as Norway is the obvious player to fill part of the gaps for nazural gas at very high prices. A look at the chart shows that some of that is clearly included in the share price as the stock trippled over the last 12 monhts:

Equinor seems to have a quite conservative dividend policy, so shareholders should not expect to directly participate in the windfall profits. They seem to have started buying back shares. Interestingly, number of shares have been increasing from 2015 to 2020.

I am not a big fan of investing into this kind of “boom time” situation, but I think it clearly makes sense to “watch” equinor as they provide really good inforamtaion to investors about the energy markets.

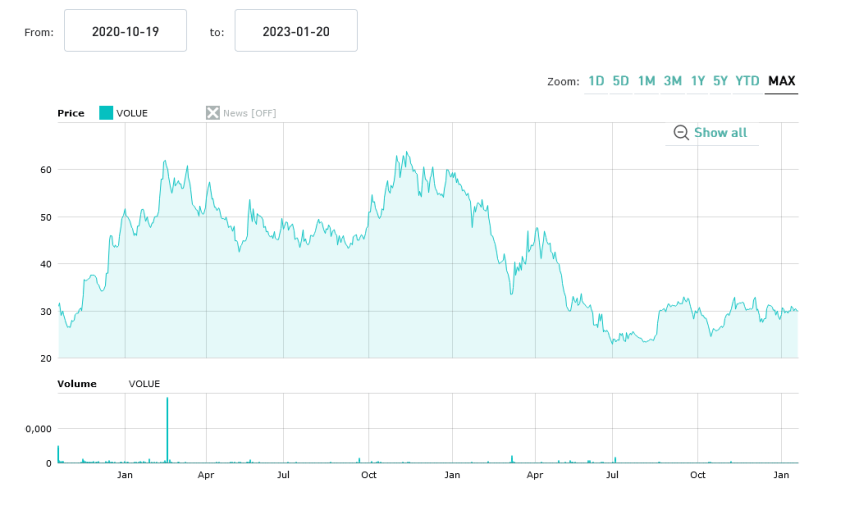

57. Volue

Volue is a 407 mn EUR market cap “international provider of business-critical software and technology services for the energy, power grid and infrastructure markets”. That sounds interesting. The company went public in 2020 and now trades around the IPO price:

As many software businesses, Volue is not real value (excuse the obvious wordply) at an P/E of around 37x for 2023. Volue seems to be the result of a merger of 4 companies. They seem to transform towards a SaaS model and have ambitious targets:

60% of the company is owned by a puclic listed investment company called Arendals Fossekompani.

Despite the high valuation, I think this is one to “watch”.

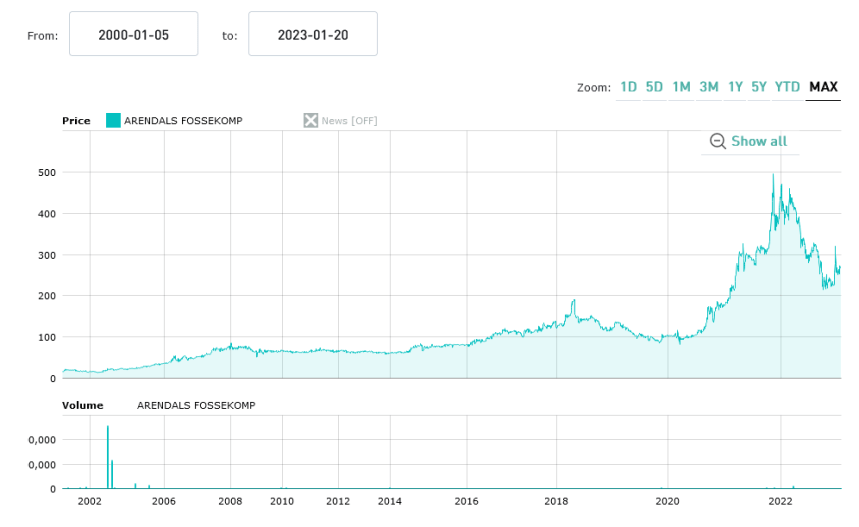

58. Arendals Fossekompani

I have overruled the random stock selector and chosen Volues (Nr. 37) majority shareholder as next target manually, as long as my memory remains fresh.

As mentioned above, Arendals owns 60% of Volue and has itself a market cap of 1,4 bn EUR. The company is active in very divergent areas, among other they seem to run hydro power plants, 3D Printing and other stuff.

The stock chart looks interesting:

They also own 71% of another listed company called Tekna. In principle, it sounds very interesting what they are doing, but it also looks like really hard to value. They seem to have a good track record in value creation, but for instance the Tekna subsidiary lost -75% in value since their IPO 1 year ago. The previous CEO has jsut resigned after only 3 years which is not 100% positive. Nevertheless, I give them the benefit of doubt and put them on “watch”.

59. Tekna Holding

While I am at it, I overrule the random gsnerator a second time and move on directly to Tekna, the other Holding of Arendals (71%). Tekna is a 70 mn market cap company that was Ipoed in 2021 but has lost almost -75% since then. Tekna claims to be a “a leading supplier of advanced micro- and nanomaterials for 3D printing, as well as the electronics and battery industry.” This sounds sexy but is yet not profitable.

Growth is relatively slow, around +6% in Q3 2022 and the company indicates that they need addtional financing in 2023. So maybe the technology is interesting, but so far this doesn’t look like a slam dunk. “Pass”.

60. PCI Biotech

As the name says, this 11 mn EUR market cap company that is “focusing on development and commercialisation of novel therapies for the treatment of cancer through its innovative photochemical internalisation”. I have no clue what that means. What I do understand is that the company has very little revenue but significant and consistent losses. “Pass”.

In the meantime, Smartoptics interestingly has topped some 50% above what you considered neither cheap nor expensive and is back at the same level as before. It may have shaken out some short-term traders and now be ready for longer-term investment.

Regarding #47. 40 Earnings for a SaaS Company looks like a steal to me.