All Norwegian Part 5 – Nr. 61-75

And on we go relentlessly with another 15 randomly selected Norwegian Stocks. As this time, an “old friend of mine” is within the selection, maybe one interesting aspect:

When I bought my first Norwegian stock in 2014, the Exchange rate had been 8,21 NOK per Euro. These days, Norway is stronger then ever and Europe is limping along. Nevertheless, the exchange rate today is 10,92 NOK/EUR which means the the NOK lost -25% over 8 plus years. Quite a surprise if you just look at this from the outside. And maybe the Euro is not so weak after all.

61. Höegh Autoliners

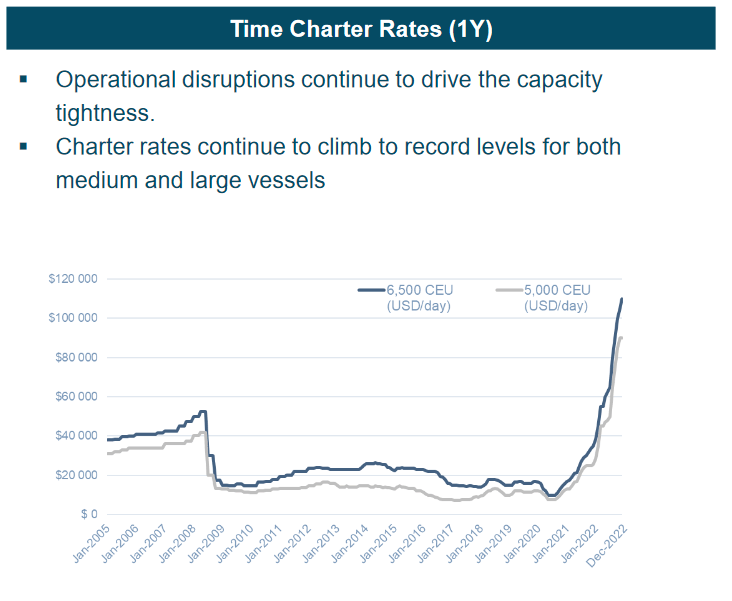

Höegh is a 1,15 bn EUR market cap “leading global provider of Roll On Roll Off transportation services, operating a fleet of around 40 Pure Car and Truck Carriers”. The company IPOed in late 202, but compared to other 2021 vintage IPO’s, Höegh investors are quite happy with the share price being up 3x since IPO.

The company seems to have a rather short financial history. Because of supply chain disruptions, charter rates are at mutli-decade highs. The market thinks that these rates are not so sustainable, otherwise the stock would not trade at a P/E of 3,5:

As I am not a nig fan of super cyclical businesses, I’ll “pass”

62. Gentian Diagnostic

Gentian is a 62 mn EUR that “researches, develops, and produces biochemical reagents for use in medical diagnostics and research in Europe, Asia, and the United States”. The company does have sales and a positive gross margins, but has never produced an operating profit. “Pass”.

63. Xplora Technology

Xplora is a 38 mn EUR market cap company that ” is a platform and services company and an industry leader in the market for children’s smartwatches. Xplora was founded to give children a safe onboarding to the digital life and a better balance between screen time and physical activity.”

As a 2020 IPO, the company first surged during the post-covid craze before trading now at around 50% of the IPO price. The company is still growing decently at around 20% y-o-y, but showing dis-economics of scale with increasingly negative margins. “Pass”.

64. Huddlestock Fintech

As the name indicates, this 30 mn EUR company is a Fintech that “develops unique software as a service solutions for digitizing work processes for custody banks, asset managers and retail trading venues”. From what I underatnd, their main products are white label stock trading apps for financial institutions.

This sounds interesting. Similar to other 2020 IPOs, the share shot up but is now at least trading at IPO level. In comparison to other Norwegian IPOs there seem to be some economies of scale at work, although the company is still loss making.

They have also acquired some business via an asset deal from a company that has now become the biggest investor. “Watch”.

65. Kyoto Group

Kyoto is another Norwegian Cleantech company with a 20 mn EUR market cap that “plans to operate and sell HeatCube thermal batteries, enabling industrial consumption of low-cost heat sourced from excess solar and wind energy”. As a hot 2021 IPO, the stock lost ~2/3 from their IPO price which indicates that things are not going as planned. They have a fancy investor presentation, 8 Chief something officers but no revenues. They seem to be trying to raise capital. Good luck, “pass”.

66. Norske Skog

Norske Skog is a 640 mn EUR market cap paper producer that focuses on newspaper and magazine paper and was IPOed in 2019. TIKR says the company is super cheap at 3,5x P/E and 4xEV/EBIT, but 2022 only seems to be the third year out of the past 6 that were profitale. They operate paper mills in Europe as well one in Tasmania (!!). They also seem to tranform one mill to containerboard production which has maybe a better future than newspapers and magazines. Overall, nt my cup of tea, “pass”.

67. DNO

DNO is a 1.1 bn EUR market cap oil company that has it’s main asset in the Kurdistan region if Iraq. DNO’s share price is quite volatile, from over 20 NOK pre Covid, down to 3 NOK in 2020 an now back to 13 NOks.

According to TIKR, the stock is very cheap at around 3x P/E. The company owns some oilwells near norway and seems to have bought assets in West Africa, but 80% of the production come from Kurdistan. As I am not an expert of Oil companies and even know less about the situation in Kurdistan, I’ll “pass” again.

68. Lifecare

Lifecare is a 28 mn EUR market cap company that seems to develop medical sensors for instance for Glucose levels. The company is public since the dot.com time and seems to get hyped everry 5 years or so. As far as I can see, they nver amde a profit and only little sales. “Pass”.

69. Arribatec

Arribatec is a 26 mn EUR market cap “Software & Consulting company headquartered in Oslo delivering Next Generation Postmodern ERP – Solution as a Service (SolaaS) globally.” The stock seems to ave had its year in the sun in 2007. Somehow they do have some sales but as expected the company is loss making and has raised capital in 2020 and 2022. “Pass”.

70. Bouvet ASA

Bouvet is a Norwegian IT consultancy that I accidently discovered in 2014 and own since then with the only regret that it started as a half position and I never filled it up to a full position.

The 560 mn EUR market cap company has since then more than 4x its EPS and at a current P/E of 20 is not cheap but alos not expensive for the quality on offer. Margins and returns have steadily increased and it seems that they can still grow organically. For me it’s clearly a “hold”.

71. Icelandic Salmon

Icelandic Salmon is a 440 mn EUR fish farmer and is majority owned by “larger fish” Salmar. Despit eing listed in Norway, the company is actually located in Iceland where they farm ….Salmon.

Interestingly, on its homepage, they still run under their old name Arnarlax which now is only the operating brand. Business is currently doing very well but I have to admit that I neither like Salmon nor that I undestand the KPIs of this business. From what I understand, margins are currently a lot higher than normal. “Pass”.

72. Elopak

Elopak is a 580 mn EUR market cap company that was IPOed in 2021 and offers “sustainable packaging”. These seem to be mainly paper based packagings for milk and other liquids. With a P/E of 13, the stock looks cheap, however growth has been week in the years before the IPO.

The share prcie is slightly below the IPO and margins have deteriorated in 2022, most likely due to high energy prices. Part of that is due to issues with a Russian subsidiary which they had to deconsolidate. their Q3 report contains some severe “chart crime”:

The company also carries quite some debt. Overall, doesn’t look too appealing, “Pass”.

73. Q-Free

Q-Free is a 61 mn EUR market cap “leading global supplier of ITS (Intelligent Transportation Systems) products and solutions”. The stock seemed to have its peak in 2005 and trading more or less sidewards down for the last 18 years.

The company is stagnating and barely profitable. “Pass”.

74. Komplett Bank

Komplett Bank is a 100 mn EUR market cap consumer bank that offer “unsecured financing to private individuals in the Norwegian, Finland, Sweden, and German markets. It offers deposit products, consumer loans, credit cards, and point of sale finance products.

The company made a significant loss in 2021 after having shown very high ROEs until 2018. not surprisingly, the share price lost -75% since 2018. There seem to have NPL problmes, a CEO change in further writedowns. “Pass”.

75. Panoro Energy

Panoro is a 300 mn EUR market cap “independent exploration and production company, engages in the exploration, development, and production of oil and gas in Africa. The company holds assets in the Equatorial Guinea, Gabon, Tunisia, South Africa, and Nigeria.”

According to TIKR, Panoro is equally cheap like DNO with a P/E of 3. The stock is around for some time and has recovered from its lows a few years agao but still at only 50% of the IPO price in 2010.

It seems to be that the main assets seem to have been puchased only in 2021. Maybe this is something for risk seeking oil experts, but I’ll “pass“.

Hey. I’d recommend to take a 2nd look at Xplora Technologies. The stock is bombed out, they have an amazing product in an interesting nice, very strong market position, good initial traction in the roll-out to several larger countries, improving margins, increasing share of recurring revenues, high insider ownership and low float. If their international expansion continues to go well, the stock is going to 5x at least.

Regarding Kyoto Group: Storing heat with molten salt is a proven technology from solar thermal power stations (for instance in Spain since ~2005). So I would not dismiss, that Kyoto has a point in their market approach and take things what they do seriously. Will see, how they perform with scaling up the technology this year and getting real business and not just demos. So for me, Kyoto is clearly a “watch” candidate, as industrial heat and energy storage are an important topic everywhere. That they dubbed it “thermal battery” is actually clever. 🙂

Thanks for pointing this out.

Servus Augustiner-Liebhaber. Concerning the paper-producer Norske Skog that you passed: any opinion on Mayr-Melnhof from Austria? Could only find a small comment from 2011 on your blog. Might be an interesting stock for your boring at a reasonable price-basket…

Servus back !! To be honest, for various reasons I am not a big fan of Austrian stocks. Maybe this is even irrational but MM is not in my target zone.

Thank you. I enjoy your stocks by country series very much.

You are very welcome !!