The Social Chain Cash Flow Shenanigan- Could that one have been spotted ?

Disclaimer: This is not investment advice, just a tiny little bit of “forensic analysis”.

The Social Chain, an initially hot, but now busted “Social Media DTC” company was recently subject to an intervention from German regulator BAFIN, claiming the 2021 accounts contained a material error in the Cashflow statement.

In essence, BAFIN said that The Social Chain’s Operating Cashflow did contain ~60 mn EUR of non-operating cashflow items that should have classified either as Financing and Investing Cashflow.

Why is that important ? Many investors (myself included) consider “Free Cashflow” as a very important metric. Free cashflow consists of Operating Cashflow minus Capex and is generally considered to be less easily manipulated than accounting numbers (“Adjusted EBITDA before costs to build the product”).

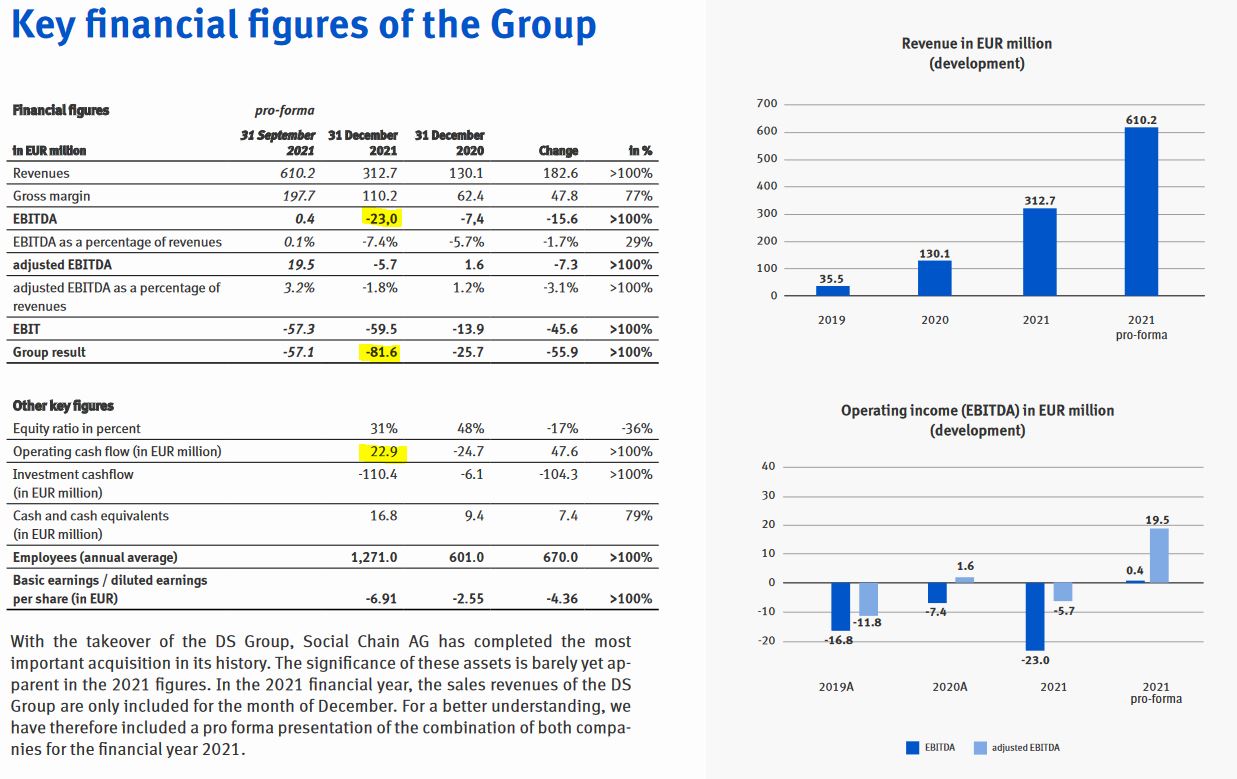

Looking at the headline numbers from the 2021 annual report, we can see that despite the “adjusted pro-forma” numbers, the +22 mn Operating cashflow compares to -23mn EUR in EBITDA and -82 mn EUR Net income and seems to generate the impression that the underlying business is cash generating, as the investment cashflow was mostly M&A:

At the time of the release of the report, The stock was already well below its peak but still 10x higher than it is today, most likely supported by this quite positive Operating Cashflow:

Whenever something like this happens, I ask myself: Could one have seen this just by looking at the numbers in the Annual Report that something was not “kosher” ?

Spoiler: In the case of Social Chain I would say yes and this despite a pretty messy balance sheet due to a debt financed, significant acquisition of a company called DS Produkte, run by this friendly Gentleman who is part of the Cast of Germany’s version of “Shark Tank”:

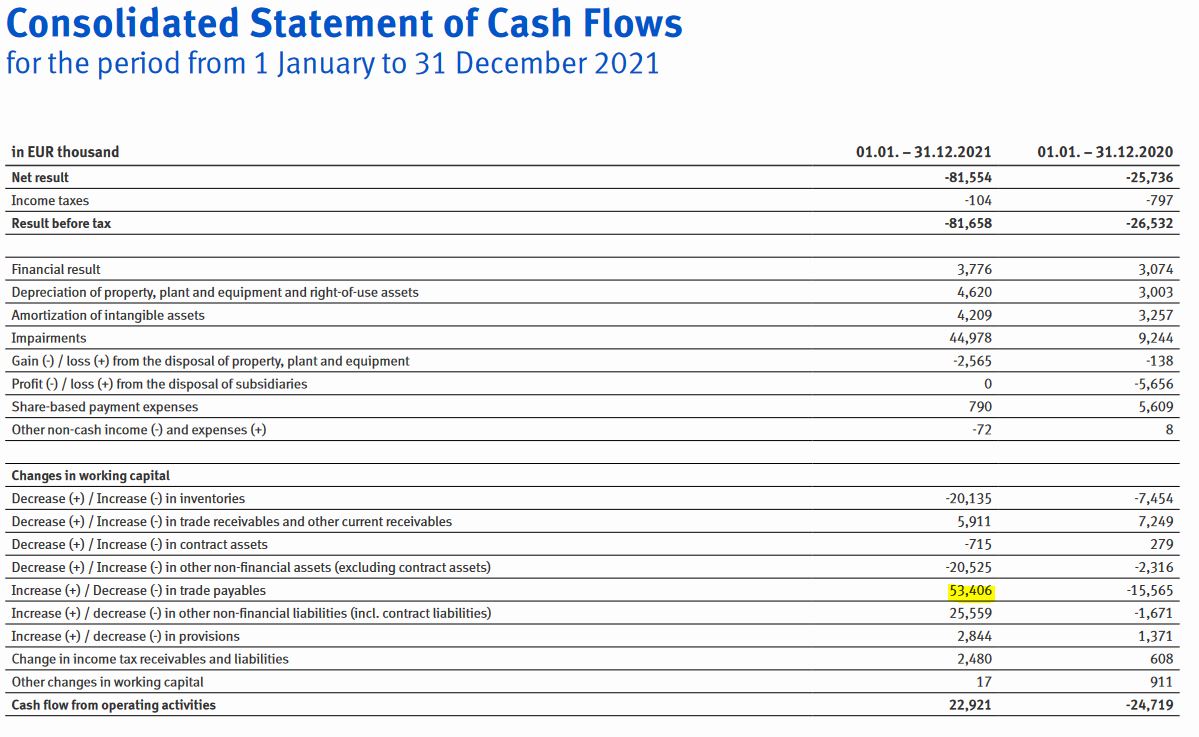

Back to the numbers. This is how the Social Chain’s 2021 CF statement looks like:

I have marked the biggest single Item that tturns the -80 mn net income into 22 mn positice Operating Cashflow, which is in this case a massive, 53 mn EUR increase in Trade payables.

A big increase in trade liabilities as such is always warning sign as such, as just squeezing suppliers is not a very sustainable strategy.

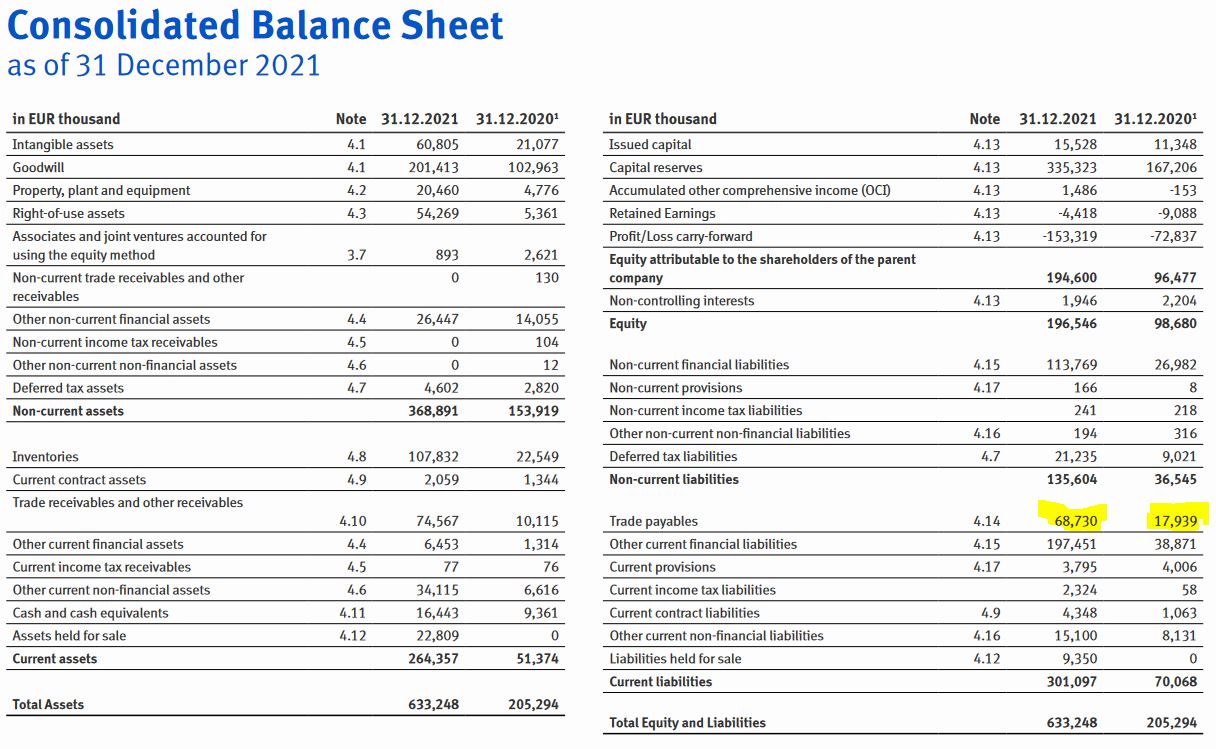

The first check one should always make is to check a suspicious CF statement against the balance sheet. And indeed, the number as such looks (almost) correct as the difference between End of 2020 end 2021:

Strangely enough, the balance sheet would indicate an increase of 50,7 mn EUR and not 53,4 mn but it’s close enough.

Now however comes the big issue: We know that The Social Chain acquired DS Produkte and that DS Produkte has been consolidated in 2021 but not in 2020 ansd it was a significant acquisition

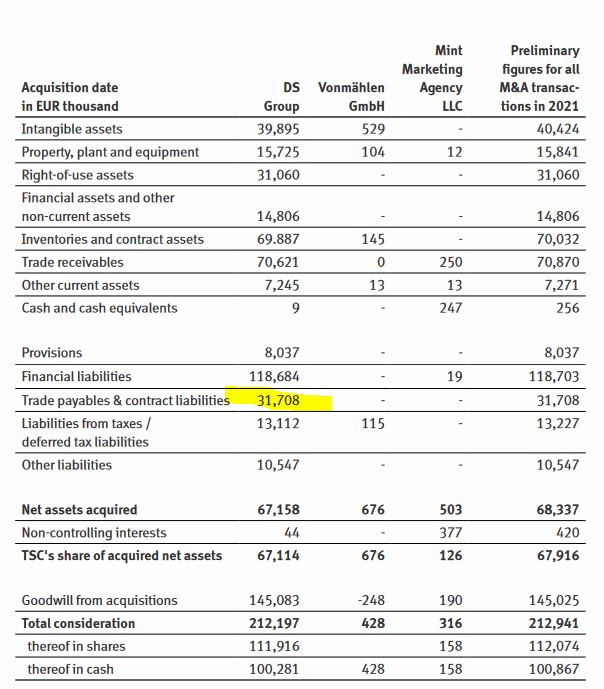

Thanks to IFRS notes, The Social Chain has to report the major balance sheet items of DS Produkte per the first day of consolidation as of November 1st 2021 in the notes under “Business combinations”:

I have marked the most interesting number in Yellow: When The Social Chain consolidated DS Produkte, their trade payables position increased by almost 32 mn EUR.

This increase in trade paybles clearly does not generate any operating cash as is purely a consolidation effect. So basically 32 of the 50 mn increase of accounts payables should not be recorded in the CF statement.

This mistake alone would push the operating Cashflow already to -10 mn instead of +22 mn EUR. To be honest, I have little motivation to go through all the other positions in the CF statement (for such a Shitco), but it is pretty clear that The Social Chain did not correctly show the effect of the acquisition in the Cashflow statement.

What can we learn from this:

- A relatively easy sanity check could have shown that something is wrong with the operating cash flow statement

- Large acquisitions and consolidation makes it easier to “fudge” especially cash flow numbers

- Shifting between different categories of the cash flow statement is the easiest way to artificially create Operating and Free cashflow

- The cashflow statement as such can also be quite easily manipulated without the auditors finding out

Some open questions remain, for instance why the auditors didn’t perform that relatively simple sanity check.

In any case, especially the fans of so called “serial acquiriers” should take cash flow statements with a big grain of salt. If you want to fudge numebrs in the cash flow statement, continuous acquisitions provide many opportunities to make the cashflow stament look much better than they actually are. So make sure to make these sanity checks for very acquisitive companies.

Well timed post! Great blog and thanks for all the effort put in over the years!

Berlin, 24. Juli 2023 – Der Vorstand der The Social Chain AG (“Gesellschaft”) (ISIN DE000A1YC996 / WKN A1YC99) ist heute nach eingehender Prüfung zu dem Ergebnis gekommen, dass für die Gesellschaft keine positive Fortbestehensprognose mehr besteht. Der Vorstand hat daher beschlossen, unverzüglich Antrag auf Eröffnung eines Insolvenzverfahrens zu stellen.

https://www.finanznachrichten.de/nachrichten-2023-07/59646044-eqs-adhoc-the-social-chain-ag-wegfall-der-positiven-fortbestehensprognose-anstehende-insolvenzantragstellung-mit-antrag-auf-eigenverwaltung-022.htm

Thanks. But to be honest, that was pure coincidence from the timing perspective.

Looking at other similar situations, the share price should go up. german speculators like insolvent stocks.

In hindsight the fairly sudden departure of the CFO Christian Senitz at the time is a clear red flag as well, wouldn’t you agree?

It pays to look into each line item when analyzing companies, and this shows why. Studying failures/fraudulent companies is a great way to instill a proper bs-filter!

While I agree that one should relatively easily be able to note the odd fluctuation in, i.e. payables, and thus start to ask questions, I do not think it is as easy as simply looking at the change in the balance sheet and see if it matches. More often than not one will not be able to reconcile reported changes in working capital on the cash flow statement with that apparent on the balance sheet.

I would disagree with your last statement. Reconciling the cash flwo statement with the balance sheet makes always sense because for the indirect method under iFRS, this is exactly how the cash flow statment is build up.

Your reconciliation exercise is complicated by at least three factors:

1. change in consolidation scope (investments/divestments)

2. Foreign exchange

3. valuation changes/allowance adjustments

Those and some I probably missed, are distorting the balances. It is simply to easy (or flawed) to look at cash flow items and expect the effect to be clearly visible in the BS.

Not sure if we are talking about the same here.

The issue was exactly that Social Chain ignored the change in consolidation scope when reporting CF from increase in payables. That was easy to spot and to reconcile with the “Business combination” disclosure.

I still think that starting with a CF Statment vs Balance Sheet reconcilliation ist the best way to identify inconsistencies. But it is clearly only the starting point.

Nice find! But what exactly ist the connection to the BaFin claim?

The connection is the following: That single item that I looked at, moves the Operating Cash flow from +20 mn to -10 mn. I am pretty sure if I would have dug deeper, I would find more. In order to still get to +22 Operating cashflow, they therefore “assigned” Financing cashflow items and Investing Cashflow itmes to Operating cashflow. According to Bafin, the total amount was ~60 mn EUR.

However I have little motivation to dig deeper into this pile of Beetle dung.