Italmobiliare (ISIN IT0005253205) – Buying “Italy’s Finest” for only 50 Cents on the Euro ?

Disclaimer: This is not investment advice. PLEASE DO YOUR OWN RESEARCH !!!!

What better day to publish a post about an Italian company than Ferragosto, the Italian Public Holiday where virtually any Italian family is somewhere close to a beach and Italian offices only are staffed with the most junior person to take up the telefone in order to say: “No one here, please call next week/next month”.

With Italmobiliare, I fell deeply into a rabbit hole, which lead to a quite extensive analysis. Due to some problems with the WordPress editor, I wrote it with a different Editor and have attached the PDF with the full version. In the blog post I’ll focus on the executive summary, the Pro’s and Con’s and the return expectations. The rest of the gory details can be read in the attached PDF document.

Executive summary:

Italmobiliare (IM) is an Italian Holding company with a market cap of ~1 bn EUR that underwent 2 pivots in its 40 year history as a listed company. The first pivot, in the 1990s, from conglomerate to Cement (Italcementi) and then once again in 2017 after a 2 bn sale to Heidelberger into an Italy focused, “Quality-growth small/mid cap PE” style investment company.

What makes the company very attractive to me, is a very interesting portfolio (including at least two potential “Super Star” holdings), decent value creation, good strategy/transparency and especially a 50% Discount to NAV.

In my opinion, the main reason for the discount is that the story and the quality of the portfolio is not well known and Italian Holdco’s are maybe not the most popular investments right now.

On the other hand, this potentially represents an attractive return/risk profile for the patient investor even without the presence of a “hard” near term catalyst.

Potential Catalysts

Overall, there is clearly no hard catalyst. “Soft” catalysts would be a continuous good or even great performance of the flagship companies and maybe a larger exit in the next 2-3 years. An IPO or even a sale of Caffe Borbone for instance could make a big difference. Or if Santa Maria grows 30-50% p.a. for some, investors might notice as well.

If, and this is a big IF, a share buy backhappens, even a smaller one could compress the discount, but I would not bet on it. The biggest hope would be that the other employees, who also are incentivized based on NAV, keep pressuring their boss who maybe has a much longer time horizon.

Another possibility could be of course once again an activist investor, but I would have no idea who this could be. The absence of such a catalyst might be part of the explanation for the high discount and why Italmobiliare is not very well known.

Valuation/Return expectations

Italmobiliare is not a Serial Acquirer but a “buy and sell” Investor. Therefore, in my opinion, the NAV is the best valuation metric. A consolidated “look through” EV/EBIT valuation or similar does not make a lot of sense due to the heterogeneity of the portfolio. This is also one of the reasons why the stock doesn’t screen well. Screeners only show book values, not NAV.

Based on this, the return expectation has two main parameters: NAV growth and assumed discount to NAV. If the discount remains 50% and they manage to increase the NAV with 8% p.a. (incl. dividends) then the return will be 8%. If however the discount narrows, then returns could be Turbocharged.

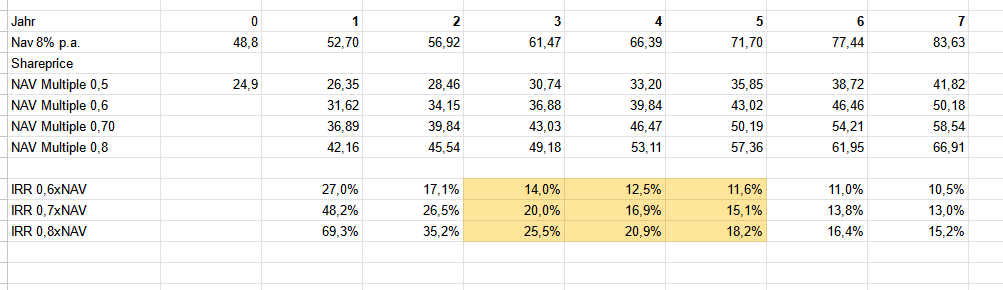

The following table shows the IRRs based on an 8% NAV growth, a share price of 60-80% of NAV along the time axis.

The orange box is the area that I think is realistic. In the low case, it takes 5 years to reach 60% of NAV which will return 11,6% p.a. (incl. dividends). In the best case, I will double my money after 3 years if the share price reaches 80% of NAV in this time. Of course , returns could be better or word, but I think that the “expected” return is something like 15-17% p.a. over 3-5 years. Which I think is attractive.

Pros/Cons

As always, even after a quite excessive deep dive, time for a Pro/Con list:

+ Significant discount to NAV

+ No holding debt (only at participation level) or other structural issues

+ good reporting

+ interesting portfolio with some potential “Star Companies” (Caffé Borbone, Prof. Santa Maria)

+ does not screen well

+ story is not well known

+ Family owned, owner operated, aligned incentives

+/- pretty OK NAV track record (8% p.a.)

– partial “Family office” character

– Holding cost + taxes

– No “hard” catalyst

Summary

Overall, I do think that Italmobiliare is a very interesting case. The current transformation doesn’t seem to be well known, but in my opinion, Italmobiliare is a very interesting “family investment” vehicle run by a very smart owner operator.

Their portfolio looks interesting and has good growth potential. The only disadvantage is the absence of a “hard catalyst”. This however is compensated by a more than comfortable discount of 50% to the NAV.

For the patient investor, this creates a great opportunity over a time horizon of at least 3-5 years. Therefore I allocated 3,3% of the Portfolio into Italmobiliare at 24,20 EUR per share.

The family (via Cemital Privital Aureliana) sells 550.000 shares for 27,5 EUR per share. Maybe that’s the reason for the current weakness of the share…

https://www.soldionline.it/notizie/azioni-italia/italmobiliare-collocamento-azioni-12-giugno-2024

Thanks for your great post, mmi. As usually really interesting. What’s your opinion about the recent sale of AGN Energia?. I think that the sale unblocks value, even not reaching your estimation in your sum-of-parts calculation (100 vs 142 mEur)

The sale as such is neutral for e. the resulting 3 EUR dividend seems to be seen very positive.

Hi Andi, thank you for the great writeup! I’m currently looking into the company and am a bit lost by the connection of H1 and FY results. E.g. for FY 2022 they posted Total revenue and income of 137 Mio. EUR, but for H1 2022 255 Mio. EUR? Why are the FY results half of the half-year results? I would be really thankful if you could clear this confusion.

Not sure which numbers you are referring to. Screenshots would be helpful. As mentioned in my post, looking at aggregated numbers is not so useful for a PE style vehicle like ITM.

Sure, here the tables I’m referring to:

https://ibb.co/44pcg1w

https://ibb.co/K5t0HkJ

I know aggregated numbers are not perfect, but they would help me get a better feeling for the company.

Not sure where thte 2022 Table is from On page A12 of the 2022 Anuual report you see the annual consolidated revenue whioch was 483 mn EUR. Maybe your number is from the Holdco statement ?

yea my FY numbers were from the holdco…sorry 😀

Thank you for this amazing analysis. I made a couple of days ago the same investment decision albeit I wasn’t aware of this article! Have you considered or researched before Peugeot Invest (former FFP)?

Thanks for sharing this interesting idea!

Most business of Caffè Borbone consists of pods for third-party coffee-machines, like Nespresso, Nescafè Dolce Gusto and Lavazza A-Modo-Mio. These machine makers prefer to sell their own branded pods and do not welcome third-party pods like Borbone. They warn consumers not to use such pods and there have been legal actions against pod makers.

So far, it has been relatively simple to design a pod that works with a specific machine. However, Nespresso introduced the VertuoLine, where the pod has to present a valid barcode to the machine in order for the brewing process to start. Nespresso does not tell third-party pod makers how to generate a valid barcode. As a next step, it is not hard to imagine a coffee machine, connected to the internet, which identifies every authorized pod uniquely. This will be nearly impossible to break for pod makers like Borbone. If they even wanted to attempt that, because it would basically make them hackers.

Could this be a threat to Borbone in the mid- to long term as such advanced coffee machines replace the current generation? Borbone’s pods might be blocked or they will be forced to sign a license agreement with the machine maker, which will likely be extremely expensive.

Thanks for the comment, good point. To my knowledge, Nestle tried this already once but failed but it is something to keep in mind.

However, if you look for instance to the Printer market, there seems to be always a way around these restrictions.

Could definitely be a threat at least in terms of market sentiment, but it’s a bit like Epson “warning” customers not to use compatible ink cartridges. And imagine the backlash if people learned that they have to connect your coffee machine to the internet to make a coffee. People would literally go apeshit in Italy, for instance.

I don’t see it as a big deal at least in the next 10 years. The IoT “applied” to appliances is mostly gigantic BS.

I have been your reader for many years. I follow four investments blog (IB) around the world (one American, one Hungarian, one Swedish and yours.) There are thousand and one IB, but only a few of them have real value for investors. It is very difficult to decide, wich is valueable and wich is not, like wich stocks are buyable and wich are not. I think, your calls and wrintings are good, realy good. Thanks for sharing your investment ideas, you have helped a lot to learn, think and invest. I hope you continue to blog for many years.

I would appreciate it if you could share with us wich investment blogs you follow regulary and wich you think are really good.

One potential reason for the absence of Exor in their 5-year total shareholder comparison chart could be relatively straightforward. Given Exor’s relocation to the Netherlands, price history data spanning more than 2 years presents a significant challenge. Despite my attempts, I was unable to access such information, even during my previous access to Bloomberg or when utilizing tools like TIKR.

I like your comprehensive analysis of Italmobiliare, and I also like how ITM manages and invests its assets in a manner reminiscent of a family office style. Nevertheless, my personal inclination leans towards other predominantly family-owned holding companies such as Odet or Exor, as opposed to Italmobiliare. That being said, I may allocate a minor portion of my portfolio to ITM, as it complements my other mentioned names quite nicely….thanks for your good work (and congratulations on your Schaffner holding) 🙂

Mr. Pesenti started buying shares personally one day after this was released.

Click to access 20230817_136049.pdf

I guess it is a coincidence, but still remarkable.

what’s the difference between nav and book value? # noob question

I noticed we bought keys made by one of their companies iseo recently

No worries. Book value is, especially for the larger participations “at cost”, NAV is at assumed market values.

My home keys are Iseo’s as well. 🙂

DISCLAIMER: the author of this paper is the same that went all-in to the nonsense LK-99 (luftballon-konduktor-99) investment. Quality of the fundamental analyses assumed the same

Exactly where did I go all-in for Lk-99 ? Because I mentioned it twice in the links ? Which investment ? I guess you mistake me for someone else maybe ?

Have to comment on this one.

I’m a long term reader and never since experienced such an Harakiri Investment. All shown on this blog is build up slowly, reasonable and transperent. Also mistakes are openly commented.

Must be someone else.

If you know other harakiri investments that returned 12% CAGR over the last 10 years, with little to no volatility, CEO buying back shares every month, that pay a decent dividend (sometimes extra ones) and continue to acquire solid businesses at a discount, please call me.

My best guess is you will receive an 8% annual return out of this investment and dilute your overall solid portfolio return. Mildly sad.

Do you want to substantiate this cleaim or just throw this out without any real arguments ?

Tyvm for the great investment case MMI !

One question re. 7.6 Tecnica: their hy-figures 2023 show a 4 % decline y-o-y. In absolute terms this is much less than half of 2022 revenues. Am I right in assuming they have a very seasonal business ? ( Skis, winter boots )

Cheers, Robert

Very seasonal. H2 should do much better.

It’s quite seasonal, Hiking boots and skiing equipement mostly sells in Q4, before Chrsitmas.