Re-underwriting Sixt AG: Family owned & run long term compounder with a great US growth story at a “bonkers bargain” price

DISCLAIMER: This is not investment advice. The Author is known for making lots of mistakes in his write-ups and will frontrun you whenever possible. DO YOUR OWN RESEARCH !!!!

As always in my longer write-up, this post only contains selected sections of the write-up- A full pdf is embedded below.

- Management Summary

Sixt AG, a family-owned and -run Car rental company from Munich, has been compounding profits and shareholder returns at a double digit CAGR for the last 20 years. Following Covid, they accelerated their organic growth in the US which now represents ⅓ of their business and is growing rapidly at 20% plus p.a..

As most of their competitors (Hertz, AVIS, Europcar) are overleveraged, they will continue to take market share from them in the coming years. The recent (temporary) issues with residual (EV) car values depressed valuation multiples so that Sixt trades at a very low P/E for 2025 (~8 times for the Prefs, 11x for the common) for what I consider a high quality company resulting in an attractive risk return profile.

- Background

Sixt is a company I owned several times in my investment career, unfortunately never long enough. During the initial Covid panic, I bought a “half” position as a part of a wider Covid basket” without any deep fundamental research at that time. Initially, this turned out to be a brilliant investment and almost tripled until the end of 2021, however since then, the stock struggled.

When the Pref Shares hit 50 EUR I tweeted that I couldn’t believe how cheap the stock is.

Following that Tweet, I thought it’s a good time to dive a little bit more into the rental car industry and see if I should “re-underwrite” Sixt or not.

3. Sixt History & some KPIs

3.1. Company history

Sixt was founded in 1912 and so technically is the oldest of the large car rental companies. However, only with Erich Sixt, who became CEO in 1969, Sixt started to expand significantly. Sixt went public in 1986 and opened the first US Branch in 2011. In 2021, Erich Sixt after 42 years finally passed to lead over to his two sons who now run Sixt as Co-CEOs in the 4th generation.

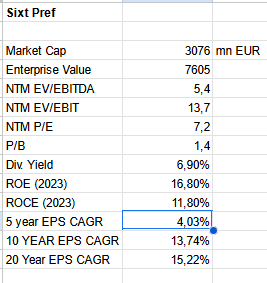

3.2. Some KPIs

We can see that over 10 and 20 years (based on 2023), Sixt has been a great compounder. Only over the last 5 years (EPS 2018 adjusted for DriveNow one off gain), EPS growth slowed. But one has to remember that this time period includes a beginning recession (2019), Covid, interest rate increases etc.

It’s also worth mentioning that all that growth was achieved organically. To my knowledge, Sixt never acquired another company.

Full PDF:

10. Why is the stock cheap ?

As always, when a stock is cheap, the question is: Are there any perfectly good reasons for the stock being so cheap ?

Despite the general weakness in European small and midcaps, these factors might play a role:

- A common theme I hear is that the rental car business is a shitty one. I think this is mainly due to the fact that the problems of AVIS, Hertz and Europcar are very public, but the success of Enterprise is not. On a P/E basis, both Hertz and Avis have traded at similar multiples (but with a lot more debt). As Enterprise is not publicly traded, some analysts might look at Sixt and decide that it is even “expensive” compared to Hertz and Avis.

- Falling residual values for cars have impacted Sixt in 2024. Initially, an EBT of 400-520 mn had been forecasted. After Q1, where they had to book a loss because of unexpected depreciation, they had to cut the guidance again with the Q2 results in May to 350-450 mn EUR. In Q2 once again they again reduced the outlook to 340-390 mn EUR. So investors might be afraid that Q3 might contain more negative surprises.

- Investors might still not fully trust the two sons to continue what Erich has achieved over more than 40 years. I have to admit that I am also not 100% convinced. Only time will tell.

- Sixt is clearly also exposed to the overall economic situation. A deepening recession in Europe might soften the demand, both for vacation rentals and business customers. Or customers might trade down from Sixt’s premium offer to a cheaper competitor.

11. Summary & conclusion

The initial question that I asked myself before writing this post was: Should I re-underwrite Sixt despite the quite disappointing performance over the past months ?

Thea answer after this exercise for me is clearly YES.

Sixt is a stock that offers an interesting growth story, a strong track record for a very low valuation which in my opinion creates a very attractive risk-return profile on a mid-term time horizon.

There are clearly some risks, as mentioned my main concern is how the sons will perform once Erich is not around anymore.

In any case, I decided not only to “re-underwrite” the stock but to increase my exposure by buying an additional 1% of the portfolio of Common shares.

I might add further, both to the Prefs and the Commons in the future if no negative surprises happen. The date for the release of Q3 earnings is November 11th.