“Space is the place” – SpaceX IPO, OHB SE and a Rocket Internet update

DISCLAIMER: This is not Investment advice. PLEASE DO YOUR OWN RESEARCH !!!!

A lot has happened since I published my Rocket Internet write-up from the end of January. Just as a refresher: I found Rocket Internet interesting, despite some Governance issues as the “sum of the part” value was significantly higher than the share price back then and that it offered some relevant & discounted exposure to Elon’s SpaceX IPO.

But before we start, I would recommend to click on the following link and get David Bowie’s Space Oddity as a nice background sound for reading this post:

David Bowie – Space Oddity (Official Video)

As I write, SpaceX has just released its S-1 filing and plans to go public on June 10th. This is what I wrote back then:

My time horizon for this would be either the (Rocket) AGM or the actual SpaceX IPO. On Polymarket, the odds are 60% for an IPO before end of Q3 2026

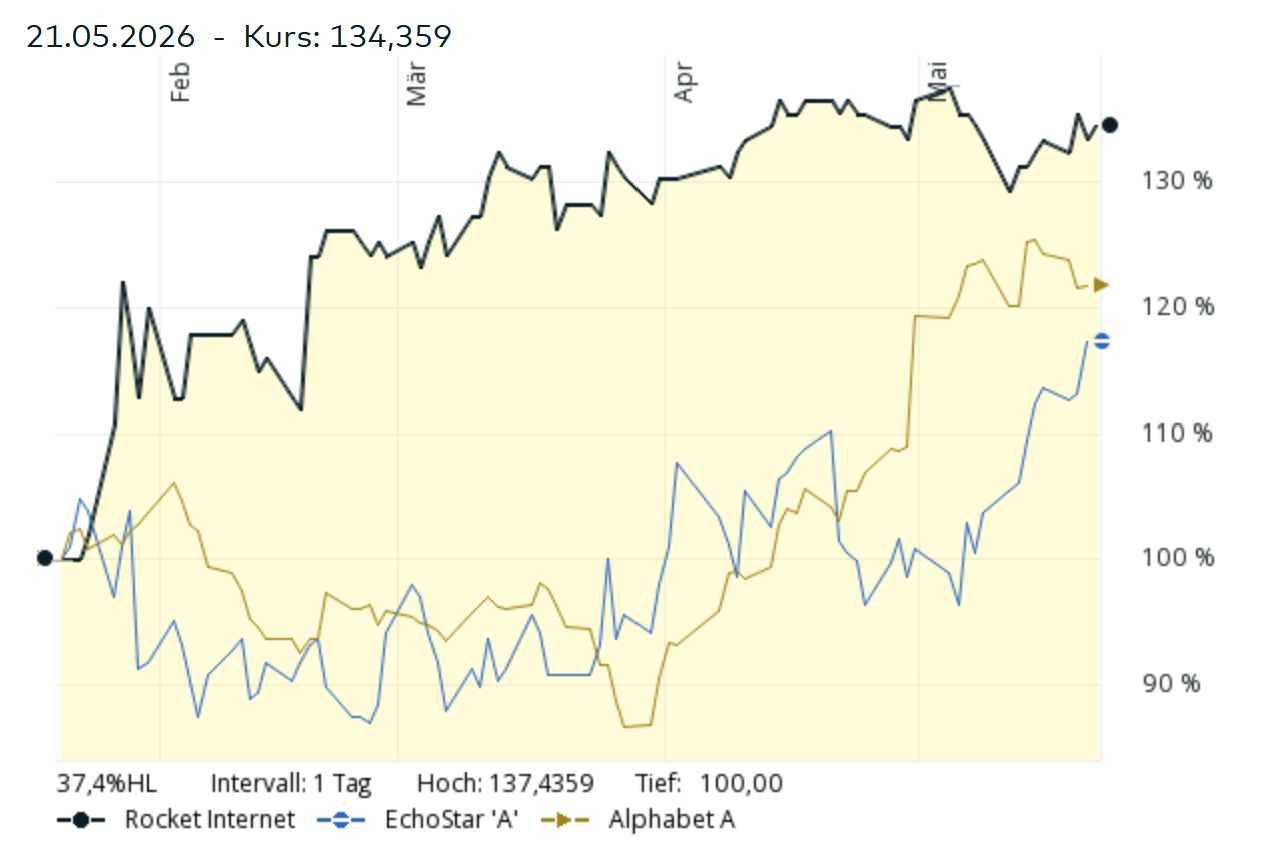

Compared with two other “SpaceX Proxies” that I mentioned, EchoStar & Alphabet, Rocket actually did quite OK if we look at the chart:

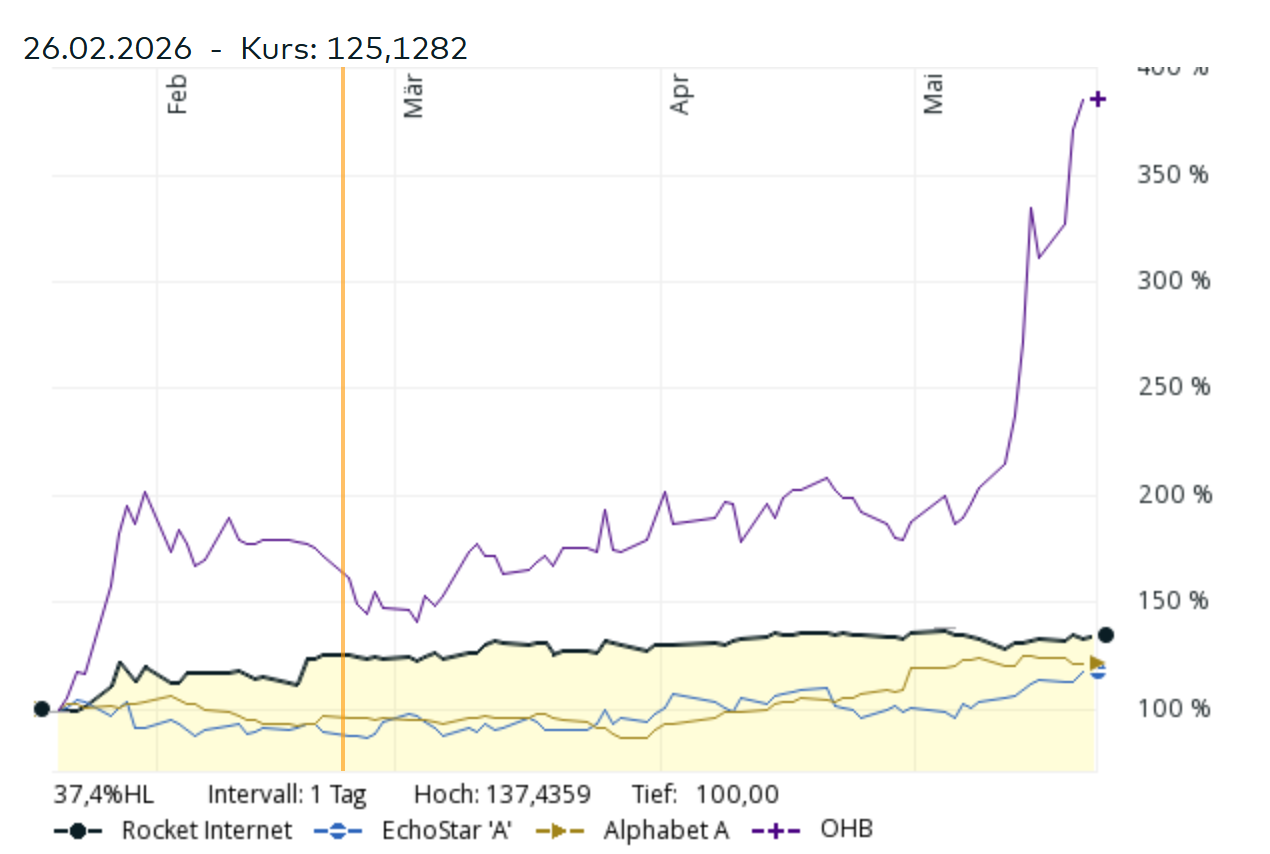

The real Space Superstar: OHB SE

However, the real “Performance Rocket” would have been another German stock called OHB:

OHB, a German/Bremen based Satellite manufacturer went parabolic despite having a really small free float after KKR acquired a significant portion of the minority free float at 44 EUR in 2023. Initially they wanted to delist but then kept the listing.

The main reason for this increase seems to be that OHB is included in a very popular ETF called Tema Space Innovators ETF with the great Ticker NASA.

This ETF is one of the fastest growing ETFs ever and currently has a 5% allocation in OHB. At around 1,4 bn AUM, that’s around 60 mn EUR in OHB. As most of the OHB shares are held by the founding Fuchs family and KKR (together ~94%) and some specialized “Squeeze out” players, there seems to be a pretty hard squeeze on the few remaining shares.

I also guess that you cannot short OHB shares. Operationally, OHB has been doing okayish, but nothing that would justify a 130x P/E.

In any case, this is a monster deal for KKR who (obviously) plan to exit while its “hot”. I am pretty sure that after that exit, OHB will be one of those “Christmas Tree” charts that we know from the Covid times.

Back to SpaceX

Elon seems to target a valuation of 1,75 tn USD, that would be the upper range of what I assumed in my January sum-of-the part valuation. However, “old” SpaceX shareholders from the beginning of the year have been diluted by ~20% after the “merger” of SpaceX with XAi, so we have to take this into account.

I am sure that Matt Levine will write and say much smarter things than I do about the SpaceX IPO, so here are just some observations:

- The S1 prospectus contains some really nice pictures of rockets

- There are already a lot of write-ups & observations about several aspects of SpaceX. A pretty good thread can be found for instance on Bluesky.

- Overall, SpaceX is clearly much more resembling a giant “Elon Venture Fund” than a normal company. I think I read this in one of Matt Levine’s newsletters about Tesla. Elon has assembled a relatively loosely connected group of companies (XA, Twitter, SpaceX, Starlink, maybe Cursor) with which he can more or less credibly jump on any new hype that will come his way.

Like the VC giants Sequoia or A16Z, he has two talents: To raise funding and to attract (a certain type) of tech people with which he can at least create the appearance of riding the next big thing.

If Ai hits a brick wall, Elon finds something else like maybe Quantum computing or he will merge Neuralink into SpaceX or become the Number 1 in obesity pills.

His hardcore fans are not looking for earnings but to ride the next hype - A lot has been already said about the “total Addressable Market” figures from the deck which equal the US GDP.

The great thing about both, the socalled “Space economy” and also AI is, that both at the moment seem to have indefinite TAMs. Mathematically, even a small slice of something indefinite is worth an indefinite amount of money.

So that’s clearly much better than something like earth bound EVs where there is a clear ceiling or humanoid robots that just don’t work and where the Chinese are obviously much better.

I am pretty sure, Cathy Wood or someone similar will come up with an “analysis” that SpaceX is worth 100X from wherever it is trading. - A nice contrarian take can be found at the “Wertegang” Substack with the nice title : SpaceX is a Zero. Here, my friend Dirk argues that the SciFi bestseller “The three body problem” clearly shows that reaching to the stars is pretty risky from a cosmic perspective (Dark Forrest theory). But I am pretty sure that if needed, Elon will also promise to manufacture Pocket Universes in one of his Gigafactories.

- What I am really curious about is, if Elon manages to really hype two companies, Tesla and SpaceX at the same time. Also, how will the typical “Elon retail hardcore supporter” react ? If he/she is a real Elon fan, he/she will have all of their money already in Tesla (plus maybe some more). But of course, they want to have SpaceX exposure, too. So will they sell their Tesla shares to get a 50/50 allocation ? I think this will be interesting to observe.

Anyway, the SpaceX IPO is great financial entertainment and might only be topped by an OpenAI IPO in autumn.

Rocket Internet Update

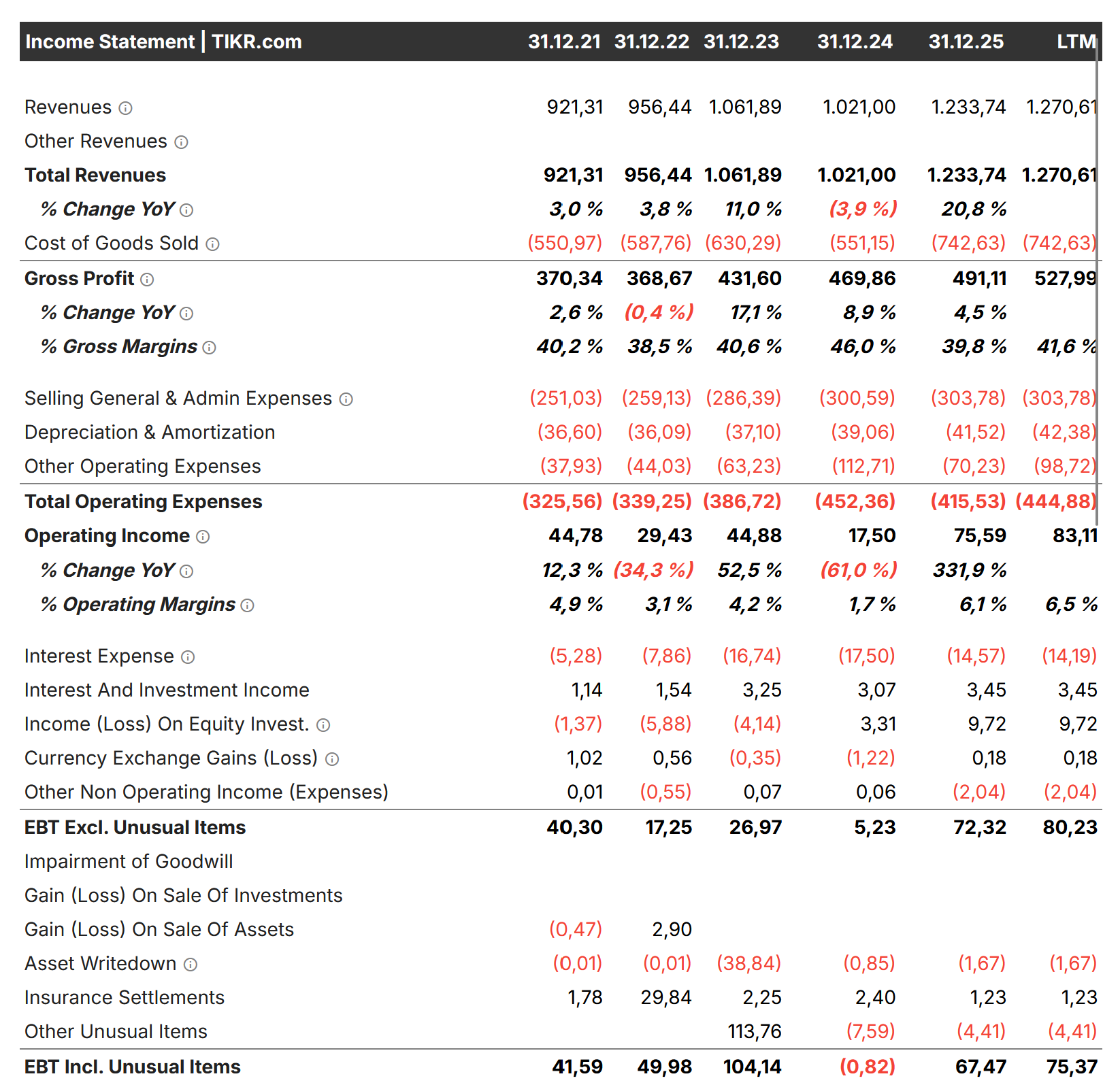

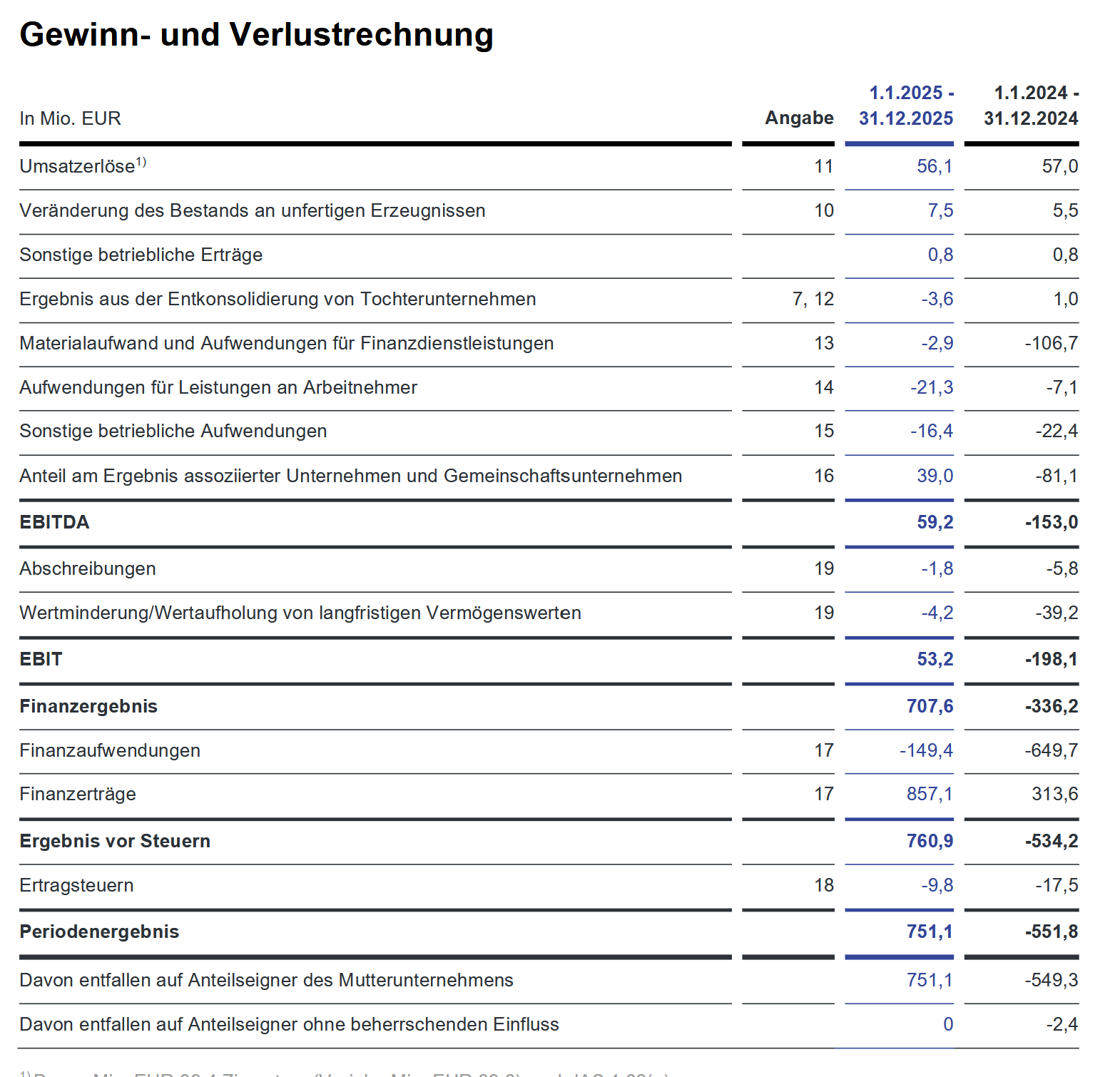

In the meantime, Rocket Internet has “published” its 2025 annual report. Interestingly they did revaulue their participations upwards to a certain extent. After a loss of -550 mn EUR in 2024, they now show a profit of 750 mn EUR. It seems that the letter from Scherzer AG to the auditors did have some effects.

If I would be in the Microcap Stock promotion game, I would maybe post something like: “Hidden Perfromance Rocket trading below NAV at 3x P/E ratio”, but economically the shown profit is pretty meaningless.

On the negative side, there will be no large cash distribution and Rocket seems to intend to make the company even less transparent going forward.

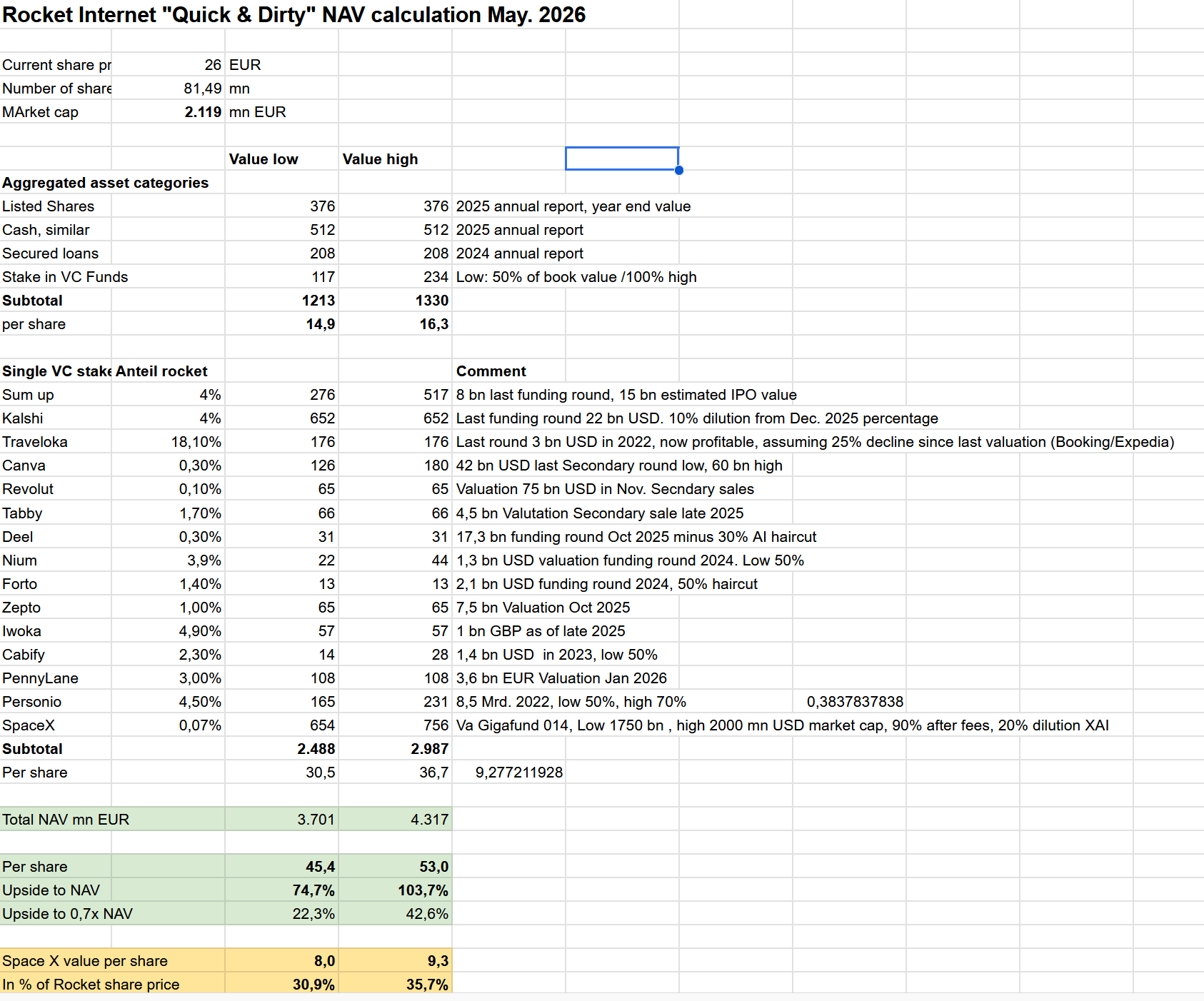

In any case, I updated my valuation sheet, including some “bug fixes”. Again, this is a quick and dirty exercise and definitely not investment advice !!!

Here is the new sheet:

The main changes that I made were some haircuts on Software companies andTraveloka and adjusting Kalshi and SpaceX for the most recent values. For SpaceX I incorporatedthe 20% dilution from XAi and a new range of 1750 to 2000 mn USD as valuation. For Kalshi I used the 22 bn valuation and implying a further dilution of 10% from the YE 2025 number.

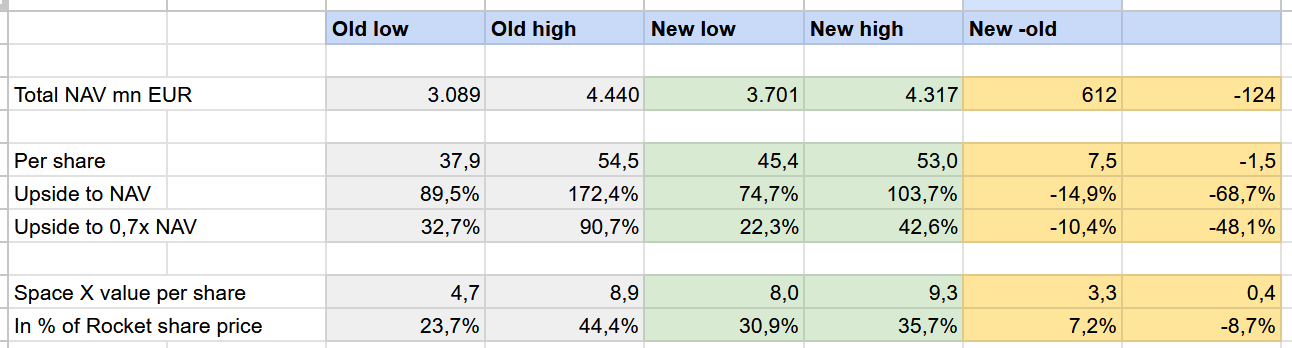

This is a quick comparison between my old and the new exercise:

We can see that the Upside NAV is more or less the same at 53 EUR per share vs. 54,5EUR despite the “haircuts” applied to Software, but the downside valuation is singinifcantly higher, mainly because of the expected valuation of SpaceX at theIPO and the recent Kalshi round which was only a rumour in January.

The upside to the NAV is of course lower, as the shares gained ~+30% since the write-up.

As mentioned in the beginning, I will keep the shares until the IPO hoping for some more irrational exuberance around the SpaceX IPO. Unless I’ll change my mind earlier 😉