Observations: Tesla, David Einhorn & Turkey

Tesla / Elon Musk

Elon Musk’s “Tesla is somehow going private” Tweet has triggered a lot of comments and discussions (good coverage on FT Alphaville).

For me the main take-away of this story is two fold:

One the one hand, listed equity markets are not the best place to raise equity capital once you are listed. It is OK to raise equity once when you IPO but after that, a company should only pay dividends and buy back stock. Part of the reason that Tesla is shorted so much is the expectation that they will need to raise equity which clearly shows the dilemma of public equity markets these days. Personally, I do think we will see more “Softbank style” large private vehicles which will specialize in providing capital to growing companies and save them the troubles of public equity markets until the company is mature enough. Unfortunately this will lead to the shift of a large part of value creation away from public markets and out of the reach of many “Normal” investors.

On the other hand, in my opinion Elon Musk has now crossed the line between genius CEO and simple stock promoter There are many examples of CEOs (Bezos, Buffett, Malone) who managed to run their companies in an unorthodox way and nevertheless “educate” investors to stick with them. Musk however in my opinion has failed. Of course he has his “fan boys” but I think he failed to nurture a long-term investor base that understands and supports his vision. Instead, he tries to push the stock up with Tweets. Let’s see how far this goes. I wouldn’t short the stock however, as this guy is so crazy that everything can happen.

David Einhorn

David Einhorn had some tough years. Maybe because of this, things between him and Elon Musk seem to get personal now which in my opinion is often a bad sign for a portfolio manager (divorces are bad signs, too). One should NEVER take things personal in my opinion with regards to investments and I am happy that I sold my Greenlight Re shares long ago.

As in the past, I was again surprised when I read the summary of his Brighthouse Financial analysis in his Q2 report. In short, he seems to have bought the stock because it showed a big discount against book value and was now surprised that the stock would go even lower.

What surprises me most is that he actually invests into the maybe most difficult sector in Insurance anyway (Variable annuities) after he obviously seems to have problems to run a reinsurance company profitable. In his report he states that they “have no idea why the stock went down further”. Well, as a starter, it might have to do with the fact that GAAP earnings were actually negative both in Q1 and Q2, i.e. the company is loss making. Plus, he should maybe try to better understand the balance sheet of a life insurance company. Half of BHF’s book value consists of “deferred acquisition costs”. These are capitalised costs which for instance could lead to large write offs if interest rates increase further an people start to cancel their policies earlier than expected. 50% of the book value to me seems a pretty fair price in this environment for such a company.

Turkey

A lot has been written in the internet about Turkey and its current currency crisis. I have no idea how this will play out, but in this case the problems for the Lira were easy and early to see. As some readers might remember, I invested in Turkish securities some years ago but pulled out completely in early 2016.

This is what I wrote back then:

When I look at the 3 points, I think the first 2 are at risk. With Turkish inflation running at close to 10%, the devalutation risk is clearly higher. Plus there is a risk that interest rates could actually increase which would be the normal course of action if inflation increases and negatively impact the price of the bond.

But obviously Mr. Erdogan is not a fan of interest rate increases and the Central bank is not acting:

“The longer Turkey’s central bank refrains from raising rates, the stronger the perception that its hand is being forced by Mr Erdogan’s economics team and the greater the strain on Turkish assets at a time when sentiment towards emerging markets is particularly bleak,” Spiro said.

Although I don’t think that this is a problem for Koc, I do think this could be a huge problem as a TRY bond holder. It clearly shows that Turkey is not that interested in a stable Lira which can easily wipe out any gains on the bond for the foreseeable future.

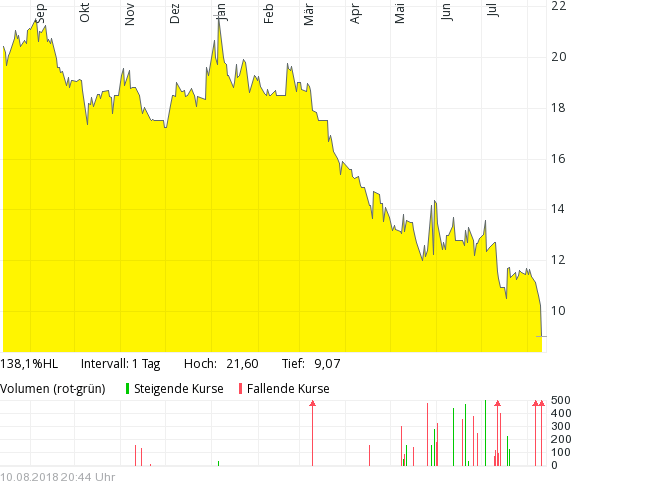

At the moment it looks like that even Koc Group seem to be badly hurt by all this. The stock lost -50% in hard currency since the beginning of 2018:

The learning for me in this case is that in Emerging Markets politics do matter and that one should really take early warnings very serious and “panik first”.

well, I was avoiding Tesla but by the end of this year they may start making serious money…and then there is this:

https://ark-invest.com/research/tesla-private

Sorry for the stupd question but what tool/site are you using to check price developments over time and e.g. the charts you show in your posts? I would be interested to know as it looks good.

Rergarding Tesla I am not yet sure whether the move is smart or not but I think doable, if the Saudi arabean investors are really in (not clear at this stage). I started a a speculative long position at around 340 USD per share and will see how this plays out.

I have to disagree on your first point. Many Tesla longs would actually prefer him to raise more capital. I think he has made this promise to be cash flow and earnings positive and now is a “prisoner” of his own statements.

He should actually build factories like crazy considering the vast opportunity with the Tesla Semi and so on.

I agree. Tesla is way ahead of the competition. Tesla will have much better margins then traditional car companies.

I am not so sure on this. The smart Tesla longs maybe, but for instance not the momentum guys…