Aggreko Plc (ISIN GB00BK1PTB77) – A great company with only temporary problems ?

Aggreko is a UK based company with a pretty simple business model:

They buy diesel engines, put them into big metal containers, add some basic electricity generating gear and rent them out globally to whoever needs them.

Aggreko’s generators are often used for big events, but also after natural catastrophes (Tsunami, hurricane), military campaigns (Afghanistan) or for mining projects in remote areas. I have been following Aggreko for some time, especially the annual reports are a pleasure to read through.

It’s clearly a niche business but quite simple. The main reason why they are able to earn 20%+ margins and 20%+ ROCE’s seems to be the fact that they are by far the biggest provider with an excellent reputation. So if you need let’s say 50 generators quickly, you can either call 4-5 local competitors to get this amount or you place one call to Aggreko. Via their global distribution net, they can als0 make sure that their generators are not idle for long. This is a very important factor for any company which is renting out equipment as it leads to lower costs. I am not sure if this is a “moat” but certainly a competitive advantage.

Multiple fundamental headwinds

Aggreko is currently hit by an almost “Perfect storm” with regard to their business model:

– there are no large natural disasters (good for the world, not so good for Aggreko)

– the number of large military campaigns has declined

– mining / oil projects get delayed and /or cancelled

– Emerging markets are struggling in general (weak currencies, weak economies)

– no big events in 2015 (Olympics, Football World cup etc)

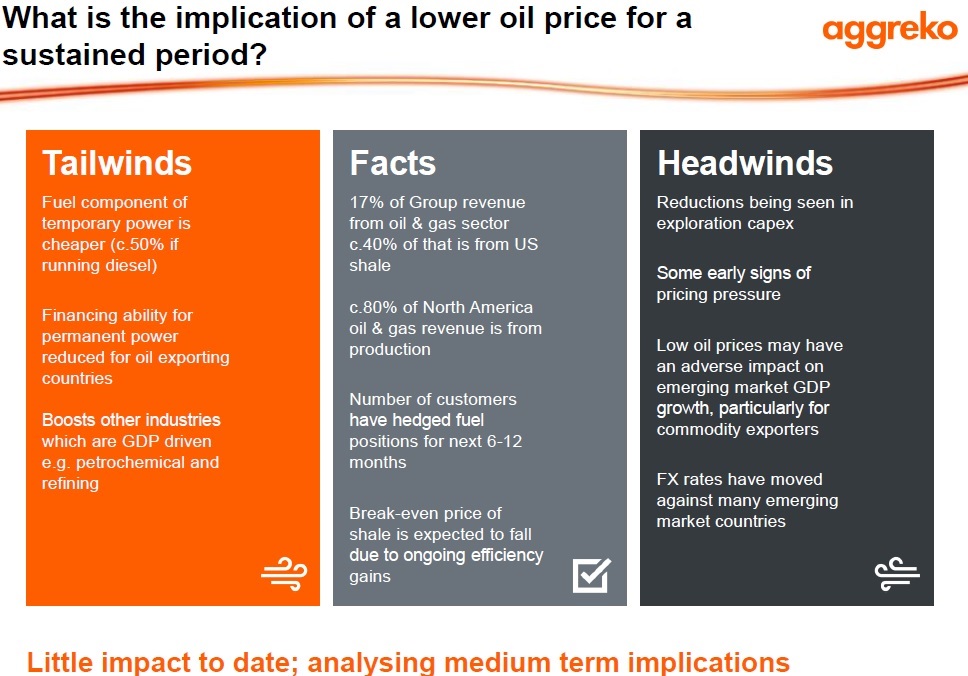

Looking at this it is almost surprising that Aggreko was able to manage to grow sales at least a little bit but margins have been clearly reduced compared to the boom years 2010-2012. So when we look at historical numbers one has to be aware that especially 2010-2012 were not representative years. With regard to oil prices, Aggreko showed an interesting chart how this affects their business:

On the other hand, this could make investing in Aggreko interesting. A great company with temporary problems due to external factors is basically the definition of a “value investment”. The question is clearly if the problems are indeed temporary.

The big issue: Management change

Aggreko used to have an outstanding management team and culture but CEO & CFO Rupert Soames and Angus Cockburn went to Serco, the new CEO has been hired from British Gas:

One of his first actions was to restructure the company’s division from regional to business line, as a result only 1 person of the old leadership team remains. I am usually sceptical about those restructurings but the new management team is a big unknown. Also changing the reporting segments is often an indicator for worse things to come. On the other hand I would say in Buffett’s words that Aggreko’s business model would almost allow an idiot to run the company, but let’s hope the new guy is not an idiot.

Another aspect with management change is the fact that the new management obviously in the beginning has very little equity interest in the company. We will come to that later, but clearly the link between management and owner is weaker when the management owns very little stock.

The strategic review:

A few days ago, the new CEO presented a strategic review. Investors seemed to have been disappointed by this outlook as it looks pretty sure that 2016 will be a transition year with even lower profit than 2015. I guess many had hoped for a quicker turn around.

I personally found it a quite solid review, nothing fantastic but also nothing stupid, just very realistic. I think one has also to keep in mind that the new CEO doesn’t have a big equity position yet. For him to aggresively promote a quick turn around would be quite counter productive. For him it’s better that he can accumulate equity via share bonuses at lower prices for some time and then deliver great numbers at a later stage.

If you look for instance on page 4 of the 6m presentation, it is quite uncommon to stress that underlying sales our down as actual sales are up. Any other CEO would have disclosed this maybe in the footnote and told a story how sales have increased. I do think that the new management is “low balling” a little bit.

Transition from Growth to Value Stock

Aggreko used to be one of the “hottest growth stocks” over many years. As we can see in the table below, despite a small set back in 2005/2005, Aggreko was able to increase earnings by an astonishing 17,9% p.a. with nice margins and good ROICs. That also explained why Aggreko was granted mostly a P/E above 20, on average 21,8 x earnings over this period:

| P/E | EPS | yoy Growth | Net margin | ROIC | |

|---|---|---|---|---|---|

| 30.12.1999 | 30,03 | 0,12 | 14,5% | 16,3% | |

| 29.12.2000 | 28,68 | 0,15 | 17,9% | 13,8% | 16,5% |

| 31.12.2001 | 23,32 | 0,16 | 9,0% | 13,0% | 15,1% |

| 31.12.2002 | 11,45 | 0,13 | -17,7% | 10,3% | 11,7% |

| 31.12.2003 | 15,29 | 0,10 | -21,5% | 8,2% | 9,6% |

| 31.12.2004 | 24,19 | 0,07 | -31,3% | 5,8% | 10,9% |

| 30.12.2005 | 19,58 | 0,14 | 99,4% | 8,8% | 13,0% |

| 29.12.2006 | 25,25 | 0,17 | 24,5% | 8,5% | 14,3% |

| 31.12.2007 | 17,75 | 0,30 | 74,2% | 11,6% | 18,4% |

| 31.12.2008 | 9,83 | 0,46 | 50,9% | 13,0% | 19,0% |

| 31.12.2009 | 14,98 | 0,63 | 37,0% | 16,4% | 21,3% |

| 31.12.2010 | 18,85 | 0,79 | 26,6% | 17,3% | 24,0% |

| 30.12.2011 | 20,71 | 0,98 | 23,4% | 18,6% | 23,9% |

| 31.12.2012 | 16,80 | 1,04 | 6,4% | 17,4% | 19,7% |

| Avg. P.a | 17,9% | 13,6% | 18,0% |

However those times are gone. From the 2012 peak of 1,04 EPS, Aggreko dropped to 0,92 in 2013 and 0,84 in 2014. The current consensus is 0,79 for 2015, the third consecutive decline, and this was not due to overall crisis but to the quite specific head winds mentioned above. This is one of the interesting things one can see in the stock market: If a former growth stocks stops to grow, it takes some time and pain until the last “Growth investor” has sold the stock and value investors move in.

Falling knife stock chart:

This transition to value can be seen nicely in the stock price which has been hammered down and lost almost -50% since the peak almost exactly 3 year ago in August 2012 when the going was still great.

This is a chart from a typical “momentum” investor, in this case Capital Group:

Buying into momentum, they almost owned 3% of the company in 2012 and then redeuced the position to close to zero. Looking at the shareholder base, one can see some value investors already, like FPA or Woodford, but most of them bought into Aggreko already in 2014 and are sitting on painful losses. Buying into this “falling knife” stock charts is usually a very bad idea, unless you have a very good view on the underlying value of the business.

Not surprisingly, Aggreko went from “Analyst’s darling” to being hated. Wenn you sort the Stoxx 600 by analyst rating consensus from highest to lowest, Aggreko is at number 580. Still slightly better than Admiral and TGS Nopec but pretty bad nevertheless.

Valuation

As I have mentioned often, I do like very simple valuation models with simple assumptions. For Aggreko I make 3 very simple assumptions as my “base case”:

– a P/E of 15 should be a fair P/E for Aggreko, so in 5 years time (2020) I can sell the stock at 15 times earnings (current trailing P/E is 14)

– Aggreko will reach 2012 earnings again in 2020 (2016 flat, 7% EPS growth thereafter)

– I need to earn 15% p.a. to reflect the uncertainties with regard to EM and new management

Together with assumed dividends I can then calculate what I am prepared to pay now in order to achieve a 15% IRR over the next 5 years:

| 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | |

|---|---|---|---|---|---|---|

| EPS | 0,79 | 0,79 | 0,85 | 0,90 | 0,97 | 1,04 |

| Target Price | 15,53 | |||||

| Dividend | 0,30 | 0,30 | 0,32 | 0,34 | 0,37 | |

| CF | -8,663 | 0,30 | 0,32 | 0,34 | 0,37 | 15,53 |

| IRR | 15,00% |

Now I could make this much more complicated with more cases etc. but overall it clearly shows that for my simple “base case” assumption, Aggreko still looks expensive compared to my return requirements. At the time of writing, at around 10,60 GBP the price would need to drop a further 2 GPB or -19% to make the investment interesting for me. At 10,60 GBP, my assumptions would only generate ~10% IRR which for me would not be enough.

I made the experience that my first valuation attempt was more often than not the best one, so for the time being I would stick with this and wait if Aggreko becomes cheaper. I think I would be tempted to buy below 0 GBP per share.

In an absolute bear case, the lower bound for Aggreko should be the replacemtn value, both of the genrators and the distribution network. I do think that a lot of this cost has been expensed, so I think replacemtn value should be significantly higher than book value, but I can’t value it. An upside case would take into account that Aggreko writes down generators aggresively, so free cash flow and owners eanrings should be higher than stated EPS.

Summary:

I do think that Aggreko has a good business model. The new management is clearly a question mark, as well as if and when EM turn around. Overall I do like the company a lot but buying atthe current price would not cover all the risks I see at the moment.

I would become highly interested if the price falls below 9 GBP and the new management doesn’t do anything very stupid. So this is my second “watch list” stock after Svenska Handelsbanken which I would buy more or less automatically if my limit would be hit.

.

P.S.:

My initial Pro/Con list

Pros:

+ Relatively simple business model

+ size –> moat (fleet size, distribution system). Not so easy to copy

+ no pension deficit, small DBO, reasonable debt levels

+ past growth was organic, much more robust than M&A driven grwoth

+ Transparent reporting, few adjustments

+ management salaries/bonuses based on ROCE & EPS growth

+ flexible Capex

+ “copycat” competitor APR went more or less belly up recently (Praktiker/Hornbach ?)

+ very bad analyst sentiment (bottom 20 of the Stoxx 600, next to TGS Nopec and Admiral)

+ even at a subdued business level still very profitable

+ potential long-term structural growth

Issues

– management change (CEO left early 2014)

– business in dangerous parts of the world

– receivables against weak counterparts

– increased debt to return money to shareholders

– stagnation in sales, profit warning

– co-investment plan dropped in 2015

– “lowering the bar” for EPS growth

– not “really” cheap (P/E 14)

Just saw that Aggreko was “taken under” at around 6 GBP /share. Lucky me.

https://www.insider.co.uk/news/aggreko-delists-stock-exchange-following-24751173

Aggreko issued some surprisingly bad numbers today. Luckily I sold out already.

Another plunge today below your 9 GBP level…

Plunge unjustified in my opinion (Argentina has been already written off).

Small volumes really.

I see the shares rallying in the coming months….

I don’t have an active opinion on AGK. Returns on capital now haven been deteriorating for the last 7 years or so and FCF generation is not as good as I would have expected. Maybe things turn around but who knows ?

It’s interesting to see that the fall in GBP didn’t have to seem an impact on their share price given that AGK makes almost all of their money outside the UK, with almost 60% in USD. Debt is mostly currency matched, so shouldn’t have an effect. Any thoughts on this?

On a sidenote: I’ve been following your blog for a long time and very much respect your thought process. Thanks for sharing.

Looking at the RNS – Deutsche Bank’s prop desk has been a significant seller over the last couple of weeks (c.5-6% of market cap). Some of that surely went through dark pools, but they probably constrained the market as well…

Price could bounce back slightly now that DB is out assuming nothing else comes in….

Thank you for the nice words …

AGK: It is always difficult to tell why exactly a stock goes up or down. One factor could be that AGK trades as a Emerging Markets proxy and Emerging markets were quite week after Trump.

Results better than expected yet the stock has not moved!

Good opportunity to add for people convinced by the trade I guess…

looks like that some investors are actually quite disappointed….

Not sure why really!

Good be the Argentine side of the business…

They said today: “We expect the 2016 full year results to be broadly in-line with current market expectations, with pre-exceptional profit before tax of around £225 million”

On the occasion of 1H update (post Brexit) they said they did expect to reach slightly lower PBT vs FY2015 (252 m).

Sell side consensus was 230 m PBT as of today.

So, everything seems to be pretty much known/discounted concerning the numbers.

The North America oil&gas pressure was also known in June.

I will wait for the transcript but nothing remarkable from the press release so far in my opinion.

My feeling as well! That’s why I am hinting to the delays in Argentina as a possible explanation.

On the other hand, distressed credit dealers in London are pricing the Maxpower Group senior loans at 20cts on the dollar today!

Same sector – different markets. It makes you look at the business model from a different optic.

Any thoughts as to why this is dropping like a stone?

nope. No idea.

I have purchased some shares. Mgt was relatively bullish on 2H (on the occasion of 1H results). Credit Suisse lowering T.P. 25% based on competition concerns for a business that has 25% global market share doesn’t seem a robust thinking to me (for the long term). As usual sell side measuring in quarter terms.

I think I will wait for more numbers before doing anything. In theory, the bounce back of the oil price should be positive for Aggreko.

Curious if you have anymore thoughts on Karpowership? Already at 1000MW and going to 2000MW this year w/ 6000MW in total being built. They are winning some big contracts (“5% of Southern Iraq, 27% of Lebanon, 22% of Ghana, 32% of Zambia and 31% of North Sulawesi Indonesia’s total electricity generation”), and it seems many countries are moving towards larger, longer-term deals. They also benefit from a working HFO solution and more fuel efficient engines, so total costs are lower albeit higher upfront capital costs to build the ships.

Thoughts on whether this compresses pricing and future returns for AGK?

hmm, I am not sure if the compete for the same kind of project with Aggreko. But honestly, I don’t know.

aggreko makes around 30 per cent of their revenues through their utilities division. Project sizes are big and aggreko and the the powership operators bid for the same contracts. Currently there appear to be quite a number of new ships being built. As this is a high margin part of the business this is a serious headwind for the company with margins decreasing. I doubt there will be much growth in the utilities segment in coming years. Not really new but could be part of the explanation for the recent drop.

I would add this with regard to powerships:

– the ships obviously are only a competitor if the project is near a sea shore

– and the size of the project has to be really big because you cannot divded up the ship

The Powership competition is nothing new and if this would be the “true reason” I would actually be a buyer. Clearly, Returns on capital have been sinking since 2010 as there seems to be too much capacity on the market.

good points.

-I believe, more people in developing countries live historically closer to shores than not. So ships could be an option more often than you may think.

-Aggreko reports that countries such as Mozambique, Argentina, Yemen etc. are clients of their Power Solutions Utility division. Therefore I gather that the utilities’ share of the revenue comprises to a large part of such big projects. And if you look at the size of some of the those, they are well in the range of 1 or even several ships’ capacity. There could be quite an impact on revenue if a contract is lost – i.e. a third of Aggreko’s revenue are dependent on a relatively low number of contracts. With the corresponding risk associated.

well, let’s simply look for instance at the project in Mozambique:

http://www.aggreko.com/media-centre/press-releases/power-plant-mozambique-namibia-expanded/

This Aggreko Powerplant is in Ressano (Google Maps): https://www.google.de/maps/search/ressano/@-25.884311,32.030466,9.5z

That’s around a 100 km from the seashore. So it would be interesting, how one of this powerships delivers the electricity to a place 100 km inland in a country where there most likely are no high voltage pwoer lines.

Karpowership has one Mazambique project as well, but obviously this is relying on existing infrastrcuture:

http://www.karpowership.com/en/projects/mozambique-zambia

If you read through the Aggreko material, many PPP projects are not providing power to people living near the seashore, but rather to mining or oil projects in the middle of nowhere. Again, there might be overlaps, but I am not convinced that those poerships are a game changer.

When you look at the Aggreko’s African projects, many of them are of relatively small size:

Related Pages

Power Plant for South Africa and Mozambique (107.5 MW)

Power Plant in Tanzania (100 MW)

Power Plant in Kenya (140 MW)

Power Plant in Gabon (30 MW)

Power Plant in Ethiopia (30 MW)

Gas Power Plant in Ivory Coast (70 MW)

Power Plant in Angola (90 MW)

In my (limited) understanding, there might be some overlaps but Karpowership is much more a competitor to people to guys like Siemens or GE who build entire power stations than for Aggreko which in my understanding does smaller and more flexible projects where there is no infrastructure.

just wondering what the cheaper power provider is, a ship or aggreko’s smaller units which can be used more flexible and decentralized.

Well, it depends on the situation. I guess if you need 350 MW and the infrustructure is there, then the new “Khan” class is maybe cheaper. If a ship has to run at 50% capacity (but still has to earn money on the unsused capacity) than I am pretty sure that Aggreko will be cheaper in the long run.

I am trying to understand why they kept employing more and more people despite the lack of growth in revenues since 2012. I coulnd’t find any straightforward comments in their annual reports. Any ideas anyone?

I guess they were somehow surprised by the slow down in business….

Increased position by 0,5% at ~8,45 GBP

For me the most probable short term impact is the shale oil decline due to the low oil price environment. As a lot of the growth was connected to drilling activity in North America we may see some more of this reversed in the short term as rig counts appear to drop further. Less rigs and compounds to be powered = less demand for Aggrekos products. It will be interesting how the competition game in current times of overcapacity will play out.

Did you ever look at Karpowership?

Yes, I have seen this. Seems to work for coastal projects only.

Hm I don’t know, if the substation (which is connected to the main grid) is near the shore it looks like it can work over a considerable amount of distance.. They’re already at +/- 2000 MW of capacity… Not so much a threat for the smaller projects (Local Power) as these ships are made for serious amounts of energy…

BTW: The powerships division has 2 ex-Aggreko key personnel among the employees…

Well it looks that they are really for very specific purposes.

Bought a “half” position of Aggreko today. Didn’t get them below 900 but at around 910. HSBC downgarde in my opinion bullxxxx

I am also looking at Aggreko but I think the competitive advantage isn’t as strong as you anticipate – the fact that the Bangladesh contract came in at much lower Marin suggests other parties bid – besides why would you really have a moat – they have a fleet of generators which means anyone with capital can match it. If you are a domestic you don’t care about an international fleet

I actually think there is a little bit more to the business than just buying generators and renting them to customers. I mean, when clients need power solutions it’s often for mission critical purposes so renting from John Doe who just spent 500 on a generator seems a little bit out of whack. The quality of service looks to be an important selling point.. In addition, after quality the next thing people value is ‘cost per MW’, and if you take into account that Agk designs and fabricates its own fleet of generators, the cost is significantly lower than competitors (estimates are around 40% cheaper).

JM, thanks for the comment. Agree with most points but one: I think the cost advantage comes much more from their network than from their design and fabrication. Thorugh the network, they can ensure higher usage of their generator compared to a local competitor. Nevertheless, in an oversupplied market this could still mean continuing pressure on margins.

Thanks for the comment. I agree the network allows for higher utilization, and thus higher ROIC. Thanks to their own design the fleet is optimized for moving & reliability in extreme conditions.

However, I also believe that their own design and fabrication allows for lower manufacturing costs (in addition the volume they take off definitely will give economies of scale in purchasing). This lower cost has the obvious beneficial impact on ROIC.

The reason why we still didn’t pull the trigger is that the company seems to have become rather bloated, if you look at efficiency measures such as revenue/Oper Inc per employee or others, margin evolution and others, they do not bode well… I think there is a lot of low hanging fruit here.. Also, I like the new CEO he reads experienced and motivated.

Thanks for the analysis!

I looked at this company about a year ago. Main issue in my analysis was that the power systems growth mainly driven by a shortage of utilities in emerging economies — a trend that will reverse over time. That was a big factor driving Aggreko’s growth to such a high percentage in the past. The analysis became complicated in trying to predict macro events over the next several decades over several countries. New management complicates this even more… trying to rework a business model that was clearly effective seems like a ridiculous move.

Kinda where I was going for with the revision of expected MW shortfall in my comment below.. It’s clear that current infrastructure is lacking in the EMs, but how many of these utility like projects will AGK and APR operate in 2020 and onwards?

Pierre, I think it becomes interesting when there is no growth priced in anymore. Then the stock coul dbe a real “bargain”.

Hi mmi,

just wondering which database you use to sort the Stoxx 600 according to analyst ratings. As I am not a professional investor I am usually relying on free web based offers for screening purposes. Your advise would be much appreciated.

I have access to a professional tool (Bloomberg).

What are your thoughts on management’s overestimation of global power shortage by 2020 by almost 50%? They thought it would be 195 GW and have currently revised that estimate to 105 GW.

Well, that is always the problem with long term projections. In Aggreko’s case I am not that concerned as they are quite flexible with regard to capex but you clearly have to adjust growth expectations. Which seems to take place right now ….

You might be interested in this article on APR with quite a bit of analysis of Aggreko:

http://seekingalpha.com/article/2153963-is-apr-energy-a-better-investment-than-aggreko

thanks for the link. very interesting indeed !!!

Lovely analysis. Thanks for sharing.

I like your straightforward analysis