Amsterdam Commodities (ISIN NL0000313286) – a 60-bagger over 20 years -but why ?

Amsterdam Commodities (Acomo) is a Dutch based company which “trades and distributes agricultural products”.

The company went on my “to-do list” some time ago because at first glance it looked like a company which managed to grow nicely over many years by maintaining very health returns on capital.

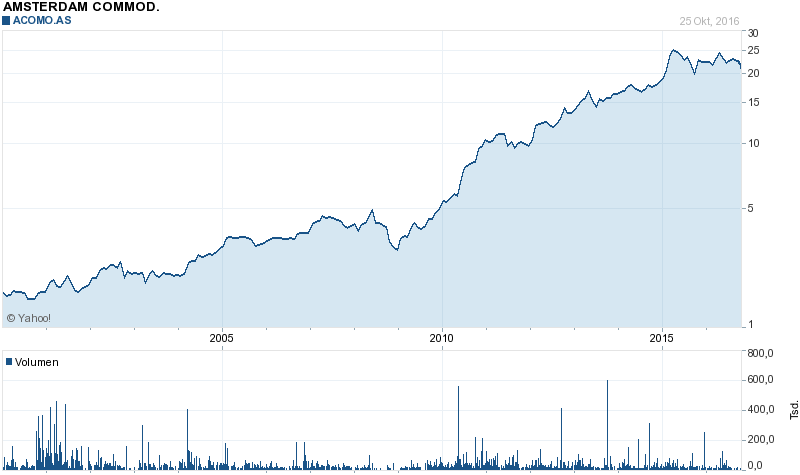

This resulted in very healthy shareholder returns over the last years as we can see in the chart:

Including dividends, ACOMO Shareholders made 27,2% p.a. over the last 10 years and (10-bagger), 25,2% p.a. over 15 years (29 bagger) and 22,5% p.a. (60-bagger) over 20 years. So a real success story. Interestingly, despite these mind-boggling returns, only 2 analysts cover the stock according to Bloomberg.

Looking at standard multiples, the company is not cheap but not expensive either:

Market Cap: 513 mn EUR

P/E 2015: 15,7

P/E 2016: 15,1

P/B: 3,0

EV/EBITDA 12,2

Div. Yield 4,7%

This is a snapshot of some standard ratios over the last 16 years:

| P/E ratio | EPS | Dvd | FCF | ROE | ROIC | Sales/share | Net margin | |

|---|---|---|---|---|---|---|---|---|

| 1999 | 9,1 | 0,20 | 0,05 | -0,47 | 20,9% | 13,6% | 4,1 | 1,5% |

| 2000 | 8,1 | 0,23 | 0,09 | -0,51 | 22,9% | 12,0% | 5,0 | 1,5% |

| 2001 | 5,5 | 0,40 | 0,15 | 0,91 | 35,5% | 19,7% | 5,8 | 2,4% |

| 2002 | 6,7 | 0,35 | 0,20 | -0,06 | 28,6% | 18,5% | 5,9 | 4,7% |

| 2003 | 5,5 | 0,41 | 0,20 | 0,34 | 30,5% | 18,9% | 5,7 | 5,9% |

| 2004 | 9,7 | 0,34 | 0,25 | 0,20 | 22,9% | n.a. | 6,0 | 4,7% |

| 2005 | 11,0 | 0,31 | 0,25 | 0,09 | 19,7% | n.a.! | 6,9 | 4,2% |

| 2006 | 8,1 | 0,48 | 0,25 | 0,13 | 28,0% | n.a. | 7,7 | 5,5% |

| 2007 | 7,9 | 0,54 | 0,30 | 0,40 | 28,8% | 18,2% | 8,5 | 5,5% |

| 2008 | 6,3 | 0,54 | 0,15 | 0,47 | 26,1% | 14,6% | 9,7 | 5,0% |

| 2009 | 8,5 | 0,64 | 0,35 | 0,67 | 28,4% | 18,9% | 9,0 | 6,4% |

| 2010 | 10,9 | 1,02 | 0,41 | 1,18 | 27,1% | 17,7% | 10,5 | 4,1% |

| 2011 | 8,9 | 1,16 | 0,52 | 0,58 | 28,0% | 14,6% | 12,0 | 4,6% |

| 2012 | 12,0 | 1,16 | 0,67 | 0,69 | 23,1% | 14,1% | 13,6 | 4,6% |

| 2013 | 14,1 | 1,17 | 0,72 | 0,82 | 21,7% | 14,3% | 14,1 | 4,7% |

| 2014 | 13,6 | 1,40 | 1,00 | 1,4595 | 23,4% | 15,2% | 14,7 | 5,3% |

| 2015 | 17,2 | 1,35 | 1,10 | 1,1427 | 20,1% | 13,2% | 17,4 | 4,7% |

What I found interesting is the following:

- Margins doubled in the crisis year 2002 and stayed there since then

- For a long time, the company traded at single digit earnings multiples despite good growth and high returns on capital

- Multiple expansion only happened in the last 4 years or so.

- Growth in EPS is not smooth but lumpy with significant “jumps”

- Economic crisis only had very limited impact on the results

- Return on capital went down from 2011

Strategy change in 2010

Looking at the available annual reports from 2008 on, the year 2010 seems to have been the pivotal year in the life of the company. Before 2010, the company was basically one trading company (Catz) and a minority stake in a natural rubber trading company.

I did not fully understand the business model of the “trading house” but it seemed to be a very capital light and surprisingly stable model. This is a comment form the 2011 annual report:

Catz International (spices, dessicated coconut, nuts, dried fruits) once again confirmed its reputation of star performer of the Acomo Group. Sales increased by more than 30% to € 237 million (2010: € 181 million), reflecting substantially higher prices of many products throughout the year, especially for spices, coconut and nuts. Net profit amounted to € 13.7 million, 16% higher than in 2010 (€ 11.8 million). Testimony to the trading talents of Henk Moerman and his teams is the fact that Catz’ results have increased threefold since 2005. They deserve full credit for their ability to secure the sourcing of the products from critical locations to meet the industry’s demand at all times and to achieve continued growth in doing so. Catz’ representative office in Vietnam proved to be a highly valuable resource for market information and proximity to the growers of important items like pepper, coconut and cashews. All activities

So it seems that securing the product itself is also part of the business, they are not a simple trader on commodity exchanges.

In 2010 then, they sold the minority natural rubber stake (at a loss), increased their capital, took out a significant loan and acquired 3 companies which resulted in more than a doubling of sales. The purchased companies were expanding the range both horizontally (tea), geographically (US), but also vertically as the acquired sunflower seeds business also has storage and processing facilities.

Interestingly, after full consideration of those acquired companies took place in 2011, growth stalled to a larg extent until today. 2011 EPS was 1,16 against 2015 EPS of 1,35. First 6M 2016 was flat or slightly negative compared to 2015.

So why was the company so succesful ?

What I found interesting is that the company was so succesful despite

- they don’t seem to have any observable “Moat” in the classic sense

- there was nothing special with regard to management

- CEO had no ownership in the company

- Capital allocation was OK but not great

- the business as such seems to be a “good” one but not “great”

From the outside it looks like that the company was at the right place at the right time. The timing of the M&A transactions in hindsight was also very good. 2010 was a year where still most people were scared. So raising significant capital and acquiring big time needed courage.

But even before, this unspectacular business produced outstanding results. Combined with a low starting valuation and a multiple expansion, this can create fantastic returns for shareholders.

What to learn from this ?

As an investor, I think it is really hard to forecast such developments. On the other hand, I do think that Acomo is a good example that investing into cheap but solid companies even (or especially) when they do not have any observable moats, can be very interesting. As the other example AQ Group showed, very good operative execution even in very tough industries can produce fantastic results over long period of time when the starting point is attractive enough.

A portfolio of 20-30 such “Boring” stocks will produce interesting results with relatively low downside but maybe every now and then some spectacular long-term upside.

In my own portfolio, I do think that companies like Miko, G. Perrier or DOM Security have the same kind of potential, although as I described above it is difficult to forecast this at individual levels.

Edit: However I do think the most difficult part is to hold these kind of stocks over a real long time horizon. This is something very few investors manage (including myself).

Is the stock still attractive ?

For me ACOMO would be interesting if they would trade cheaper. At the current 15x P/E or 12x EV/EBIT, the upside is relatively limited as organic growth seems limited. I would be interested at a valuation below 10x EV/EBIT (all other things constant) or if they manage to buy (cheaply) other companies.

“Capital allocation was OK but not great”

With ROE and ROIC in the 20s I don’t think so…

ROE or ROIC itself are not a proof for good capital allocation.

“There was nothing special with regard to management” . Yeah, right. The risk management skills of former CEO Stephane Holvoet are simply unparallelled. As a CEO of a fysical commodity trading house, he was second to none. 26years of running a commodity trading house, without a single blow-up, nothing special…?

Think you don’t understand the complexity of this business at all.

Maybe he doesn’t. How is your comment constructive in a way for all of us to understand the business better?

I guess it is down to collective wisdom: either you value it, or you should look elsewhere.

#panly, obviously I don’t understand the business. Maybe you can enlighten me ?

mmi

I stumbled across Acomo a while ago, but never invested. But one thing I do know is that in wholesale/distribution businesses management can make an extreme difference. So I would be very interested in these risk management skills of Stephane Holvoet, too, Panly.

What’s the secret sauce? I don’t understand a “fysical commodity trading house” either, but would be interested in learning about it.

Tom

” The risk management skills of former CEO Stephane Holvoet are simply unparallelled.”

Thank you for that insight!

The word “former” in your praise sonds like a red flag for me: They had a genius in the past who may have been responsible for the growth, but they dont have it anymore. So their main advantage about competitors may be lost?

mmi,

Thank you for this interesting article.

For my temper a portfolio of 30 such companies bought at the right price would be ideal. Probably Ben Graham would approve such a portfolio.

About the manager and the business of a company like Majestic Wine I do not know enough to evaluate it’s future. Retail is a difficult industry where even an outsider manager may not succeed.

Regards

malt

Thanks MMI.

I wonder where you sourced the data from to compile the 16-yr standard ratios table?

T

Was it the Bloomberg Terminal?

Thanks for the article. Interesting company which I would otherwise have stumbled across. I wonder whether a company like McCormack would buy them out ?

Ooops, meant to say “would otherwise have NOT stumbled across…”