Novo Nordisk (DK0060534915)- What now ?

When I looked at Novo Nordisk 3 months ago, I found the stock too expensive at 315 DKK/share. That was my summary back then:

What could make the stock interesting again ?

Well, that’s simple: Either a lower stock price or higher growth. Maybe management has low-balled growth ? Who knows. Maybe the market over reacts if the next quarters don’t look that good ? According to Bloomberg, analysts officially still expect double-digit earnings per share growth well into 2019. Even adjusting for share buy backs, this will be difficult to achieve based on the growth rates communicated by management.

For me, the stock would become more interesting at around 250 DKK under the current growth assumptions. I think I would also like to see more negative comments from analysts.

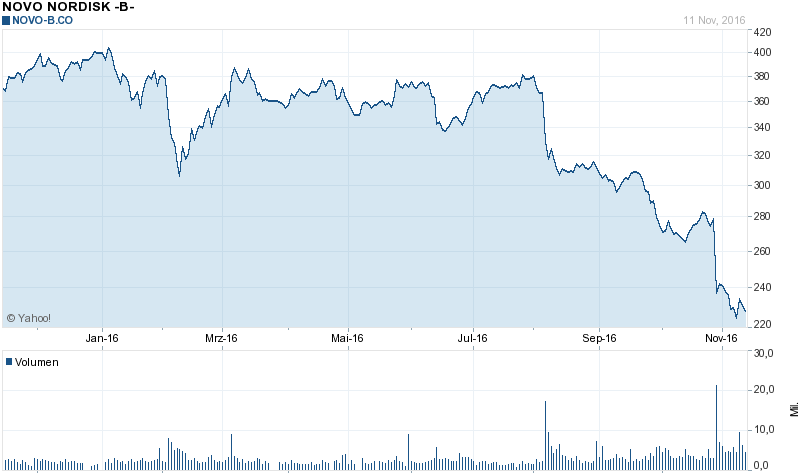

With the stock now trading at ~229 DKK, it is clearly necessary to revisit the stock again.

So let’s look what happened when they released Q3 numbers. The news which seemed to have spooked investors seems to have been this passage:

During 2016, the market environment in the USA has become significantly more challenging,negatively impacting future pricing for Novo Nordisk’s products.

Consequently, the preliminary outlook for 2017 indicates low single-digit growth in sales and flat to low single-digit growth in operating profit, both measured in local currencies. In terms of long-term financial targets, Novo Nordisk no longer deems itachievable to reach the operating profit growth target of 10% set in February 2016. As a result, the target has been revised and Novo Nordisk is now aiming for anaverage operating profit growth of 5%. The two other financial targets remain unchanged.

This is now down from the 15% Operating profit growth target 2,5 years ago when Rob Vinall wrote about the company and slightly down from “5-8% operating profit growth” in the last quarter.

The first reaction would look like this: Wow, only a small reduction in growth leads to -30% in the stock price, now the stock must be a bargain.

In my old post, I calculated the expected yield based on this simple formula (“stolen” from Rob Vinall):

4,5% “Current” yield + 6,5% (mid-point) growth = 11% “expected yield”.

So let’s update this calculation at a current Price of 230 DKK and a P/E of 15:

6,7% “Current” yield + 5% (estimated) growth = 11,7% “expected yield”.

So we can clearly see that if one uses this kind of measurement, Novo Nordisk hasn’t become a lot cheaper as the drop in price more or less reflects the reduction in expected growth.

Personally, I think this is also one of the weaknesses of this approach where the “expected yield” for a stock is calculated as the inverse P/E (“earnings yield”) plus the assumed rate of growth. The sensitivity of the valuation to growth assumptions is enourmous.

In Novo’s example, the stock price would have needed to drop by ~25% to compensate for the 1,5% drop in growth in order to maintain the required yield. So the -30% drop is more or less 1:1. a decrease in value, assuming everything else stays the same.

Analyst ratings still quite positive

With a “stock market darling” like Novo Nordisk, it usually takes time until the overwhelmingly positive analysts change their opinion. Although the analysts have reduced their price targets from 400 DKK in summer, the current target with around 280 DKK is still significantly above the current market price.

Very few analysts have changed their conviction completely like the guy from Oddo who went from “neutral, 335 DKK price target” to “sell, 206 DKK price target”. The same guy had the stock as a buy and 450 DKK target by the end of 2015…..

So from a purely sentiment point of view, It doesn’t look like that analysts have given up on the stock.

Other considerations

Compared to other pharma stocks (P/E and EV/EBITDA), Novo trades now pretty “in line” with the other big players, but not at a discount.

When I looked at their presentation for Q3 I have to admit that I understand next to nothing about their business. What I found interesting was on page 27 that Eli Lilly seems to be gaining global market share at a very fast pace, whereas all the other players (including Novo) are stagnating.

Another aspect is the upcoming CEO change. I am not sure if the current reduction of the growth forecast is actually a kind of “kitchen sinking” for the new guy or if the new CEO will try to lower the threshold again.

Summary

Despite the signficant stock price drop, Novo Nordisk is not looking that much cheaper than 3 months ago because of the reduced growth outlook.

For me to invest, I think I would need to see much worse sentiment from analysts and significant position reductions of large shareholders which I haven’t seen yet. As I have next to no knowledge about the business, I would need a higher margin of safety than the current valuation. So no action.

I saw a news that Eli Lilly ended licesing agreement with a French biotech Adocia with several insulin products in late stage trails. Some say its product (BC Lispro) are better than existing ones. The shares were down 30% percents today.

If I understand well Lilly has its own similar product Humalog (fast acting insulin) but Adocia product BC Lispro performed better than Humalog in clinical trials.

Well, I have been studying this specific pharma industry in the last few months, but It certainly isn’t within my circle of competence (yet) .. The reason for my interest was the correction we have seen in the stockprice of Novo Nordisk and the fact that it should be doable to understand this tiny part of the BIG pharma industry. For me Sanofi & Lilly do way to many things to understand the overall picture. I will take a shot at the diabetes market… and hopefully build a new circle of competence.

Most people are confronted with diabetes because of their lifestyle. They have developed a sort of resistance against insulin. That is Type 2 Diabetes. A smaller group of people are born with a autoimmune disease that attack the cells in the pancreas responsible for producing insulin. These people have Type 1 Diabetes and need to start injecting insulin almost immediately.

Type 2 diabetes is in most cases an evolving disease. That means that some patients excercise can be a temporary solution, other patients need to start with oral medication/injectables right away and in most patients will end up injecting insulin.

When you look at the pharmacompanies involved in this industry, you have 3 big players, Eli Lilly, Sanofi & Novo Nordisk. It’s basically an oligopoly. Eli Lilly seems to have the best oral product called Jardiance and is a SGLT2 class product. It is the newest product on the market so longterm side effects are not yet visible. It is selling well because of it’s efficiency but also because of it’s major CV health benefits. Those CV benefits have become a major point for FDA approval over the last few years. A competitor in this type of class is J&J but they still have to finish their CV analysis next year. A major point that still needs to be addressed is potential kidney damage. But right now there is no significant proof for that according to the FDA…

SGLT2 still has a lot of growth potential. The ‘old’ drug DPP-IV is in decline because of SGLT2: DPP-IV’s are the largest oral class, with 9% share of prescriptions and they comprise 21% of global diabetes sales. The first was approved in 2006. However, safety concerns (for some) and the emergence of SGLT-2 inhibitors that show both weight loss and cardiovascular health benefits in 2013 has slowed the overall class growth. Over time It is expected SGLT-2 inhibitors to be used instead of DPP-IV inhibitors. Novo Nordisk didn’t have any programs to develop DPP-IV inhibitors nor do they have SGLT2 programs.

Novo Nordisk does have/had one of the best in class injectables Victoza with the same effects (weight loss, CV benefits) as SGLT2. This class is called GLP1. Victoza is a once daily injectable. Normally next year Semaglutide will be released on the market and that is a once weekly injectable. Semaglutide will have to compete with Lilly’s Trulicity (also a once weekly injectable) that is already available on the market. GLP-1s represent 3% of prescriptions as a first line injectable: However, at a global level they comprise 11% of global diabetes sales, given their high price. These high prices should go down because of the PMB price pressures in the US but it will still be a very delicate balancing act for these PMB’s. The first GLP-1 was approved in 2005 but it was not until Novo launched Victoza in 2009 (EU) & 2010 (US) that usage accelerated.

Insulins are reserved until the end, the most popular of which is the basal or long-acting insulin. Overall, insulin represents 25% of prescriptions but 57% of sales. By product, Lantus (Sanofi) is by far the largest insulin with 7,1$ billion annual sales and 19% share. Lantus is losing ground because of Novo’s Tresiba and PMB price pressures. In 2017 Lilly’s Basaglar will be commercialised.

According to Rob Vinall the actual competitive advantage of Novo is that they supply 50% of the world demand + insulin is a low value product that is complex to produce (it’s actually rocket science ;-)) and it needs tons of money (capex). So this is a huge hurdle for new competitors to try and enter the market… According to me there will be fierce competition between the large players. In my view the competition will be the fiercest between Lilly and Novo.

I do not think that a lot will change with the new CEO.I hope they keep on buying shares and paying their dividends. The actual powerhouse is the Novo Nordisk Foundation which holds 75% of the voting rights. This Foundation gets dividends from several companies and uses these funds to pave the way for Novo Nordisk in frontier markets. This Foundation is building the network that Novo Nordisk will use for free in the future when these countries are confronted with a rising diabetes population. This powerhouse is supplying Novo’s products at reduced prices to those countries but in the meantime they are building infrastructure for Novo Nordisk… Crazy, right? I think no other company has a helicopter parent like that ;-).

BR,

Pieter

I don’t know the industry much but some articles are showing that prices when through the roof over the last years and without any regards for the general inflation level of the economy. It may be a case where a great business (high customer stickiness) goes above its pricing power and prices its products way above their fair prices. Because the product is critical for people health it will get either regulated or a cartel enquiry could be initiated … It is just fun to see how Novo is now guiding for much lower growth, shortly after the publication of some articles on the absurde pricing of the industry ….

http://uk.businessinsider.com/insulin-prices-increase-2016-9?r=US&IR=T

https://www.washingtonpost.com/news/wonk/wp/2016/10/31/why-insulin-prices-have-kept-rising-for-95-years/

I believe the stock currently does not price the probability/risk of a longer-term impariment of pricing-power. Moreover the company is probably not used to doing business with stable prices and has probably no experience in cost control…so longer-term margin could even be way below than currently…

The reason why GSK and Takeda dropped essentially out of the diabetes market is because they had two drugs in the same class (GSK: rosiglitazone; Takeda: pioglitazone) which became very unpopular. Rosiglitazone was associated with an increased risk for heart attacks, pioglitazone was associated with an increased risk for bladder cancer.

The reason why Eli Lilly is gaining market share is less clear for me. They have several drugs in the market: (1) a recently developed analogue of the best-selling long-acting insulin by Sanofi (Basaglar) (2) a number of other insulin products which have been around for some time (3) a member of a new class of drugs, the SGLT2 inhibitors (empagliflozine), which has recently been shown to reduce the risk of cardiovascular death and does not have to be injected, (4) a substance from the class of DPP4 inhibitors (linagliptine) which can also be taken orally but does not seem to be beneficial to Diabetes patients, and (5) a GLP1 analogue (dulaglutide). I suspect that the recent growth in market share is primarily the result of aggressive marketing of linagliptine and empagliflozine, the two drugs for which Novo Nordisk does not have a competing product. Dulaglutide competes with Novo Nordisk’s liraglutide (Victoza(R)), and basaglar competes with Novo Nordisk’s long-acting insulins, especially insulin degludec (Tresiba(R)).

cktest, thanks for the comment. I always had the opinion that insulin is very specific, so patients will always stick to the type (or brand) of insulin they have adjusted to. SO if Eli Lilly can get new patients with aggressive marketing, could it be that patients can change mre easily, especially if it is a new form of insulin ?

As Pieter wrote above, diabetes comes in several flavours. Most patients have type 2 diabetes which is believed to be the result of too little exercise and too much caloric uptake. Type 2 diabetes is often initially treated with drugs that you can take by mouth (i.e. tablets). Novo Nordisk has currently no such drugs in the market but is working on a tablet formulation of semaglutide.

The most important drug that can be taken orally (i.e. by mouth) is metformine. This drug protects from cardiovascular death. However, it is an old drug and therefore you cannot earn a lot of money with it. The second most important class of drugs that can be taken orally is the sulfonyl ureas, also an old drug family. The sulfonyl ureas are quite good in lowering blood glucose but in the long term the patient is off worse than with metformin. The only other orally available drug that has been shown to protect the patient from cardiovascular death is empagliflozine by Eli Lilly. There are other drugs of this class on the market but so far there are no data to show that these drugs are protective (even though they can lower the blood sugar level).

In most type 2 diabetic patients, diabetes becomes worse over time. These patients can then start to inject what is called a GLP1 agonist. Liraglutide (Victoza(R)) by Novo Nordisk is the drug with the largest market share; it has to be injected once daily. Several companies have developed GLP1 agonists that need to be injected less frequently. However, currently Liraglutide is the only GLP1 agonist that has been shown to protect from cardiovascular death. Novo Nordisk is also working on a long-acting GLP1 agonist, semaglutide.

All the drugs mentioned above work either by reducing the requirement for insulin in the body or by squeezing more insulin from the pancreas. Eventually, the pancreas will not be able to supply enough insulin to achieve good blood sugar levels, therefore these patients will have to take insulin. Most of these patients (including type 1 diabetic patients) use two kinds of insulin: a long-acting basal insulin that has to be injected once a day, and a short-acting insulin that is injected directly before taking a meal. There are several long-acting basal insulins on the market, the most important (at least in Germany) being insulin glargine (sold under the tradenames Lantus(R) and Toujeo(R) by Sanofi and Basaglar(R) by Eli Lilly). Novo Nordisk has two long-acting insulins on the market, insulin detemir (Levemir(R)) and insulin degludec (Tresiba(R)). Tresiba(R) is the longest-acting insulin on the market. If a patient starts insulin therapy anew, a doctor will try various insulins until good blood sugar control is achieved. This is not trivial, therefore it is very unlikely that a patient will switch his/her long-acting insulin once good blood sugar control has been achieved. Thus, a change in market share can mostly be achieved by convincing new patients (and convincing those old patients for whom good blood sugar control was not available). It is rumoured that Tresiba(R) offers better blood sugar control than glargine, but for example in Germany this improvement was considered so minor that the authorities (the Gemeinsame Bundesausschuss) decided that it didn’t justify the hefty price tag that Novo Nordisk put on Tresiba(R). Consequently, you cannot get Tresiba(R) if you have a standard health insurance.

“When I looked at their presentation for Q3 I have to admit that I understand next to nothing about their business. What I found interesting was on page 27 that Eli Lilly seems to be gaining global market share at a very fast pace, whereas all the other players (including Novo) are stagnating.”

Thanks for writing this. I have to admit that I don’t understand pharma either. Not a bit. I just flew over the presentation and… nothing. I guess it needs a lot of upfront “deep work” and learning to understand this business. I’m not sure if it’s worth the time…

The market share slide is really interesting. Apart from Eli Lilly gaining share: do you know if there there is a special reason for GSK and Takeda losing share so rapidly in the past years? Did they lose a patent or something, or did they simply decide to leave the market?

Tom

No, I have absolutely no idea how market shares are gained or lost in this business.