Travel Series 8: GDS (Sabre, Amadeus, Travelport) – Ultimate travel platforms or Dinosaurs waiting for extinction ?

Time to do another “travel series” post after the last Tripadvisor post a few months ago.

GDS – The business

The so-called “GDS” (short form of Global Distribution System) is one of the oldest “platform business” I know about.

Basically (and as far as I understand it), it is a real-time repository of available airplane seats, hotel rooms and rental cars from different suppliers (airlines, Hotels etc.). This repository can then be accessed by travel agents, OTAs etc. in order to book these offers for their ultimate clients. The GDS charge money both for access to the system and transactions. The added value comes clearly from the fact that they act as a single interface to many different back-end systems on the supplier side.

The bulk of the business is still airplane tickets, although they try to expand more and more into hotels and rental cars as well. There are several GDSs serving the market, The biggest stock listed players are Sabre (focus North America, Asia), Amadeus (mostly Europe) and Travelport (US).

Originally, the GDSs were owned by the airlines but in the 90ies, the airlines sold their stakes and the GDSs became independent companies

Is the business still relevant ? (Metasearch…)

There is a clear tendency that travel suppliers and especially airlines try to cut out as many middlemen as possible. Not long ago for instance Lufthansa started to charge extra when a client wants to buy a ticket via a GDS, so from the Airlines point of view it is clear that they want to cut out the middle man. Lufthansa claims that the surcharge is a “great success”, although I couldn’t find any hard numbers for this.

However from a customer point of view it is not so clear if you should always book directly. For instance even for relatively simple direct flights, often a “mixed” flight with different airlines is cheaper than a return flight with the same airline etc.

So far, most Metasearches (Kayak etc.) still use GDS systems as major data sources for their searches and just enrich them with extra deals.

However things are seeming to change as this article shows. In short, the airlines industry (IATA) has developed a new standard/protocol which allows in principle meta searchers like Skyscanner (or Facebook….) to connect directly to airlines and cut out the GDS systems.

Although it doesn’t seem to be 100% clear that GDS will completely lose out, the Skyscanner whitepaper is definitely worth reading. But clearly, growth for the time being is slowing for GDSs in airline bookings.

GDSs have also been pushing into hotel reservation and rental cars, but in principle those areas face similar issues with regard to “disruption” and online competition. However, most GDS players show good growth in those categories which overall still leads to single digit sales growth for all of them.

What do the numbers say ?

Here is a table with selected comps from the 3 main listed GDS players:

| M. Cap | EV/EBITDA | EV/EBIT | P/E | P/B | P/S | Op. Margin | Net Margin | ROIC | Debt/EBITDA | |

|---|---|---|---|---|---|---|---|---|---|---|

| Sabre | 5,1 | 8,9 | 10,9 | 20,3 | 7,9 | 1,46 | 2,1% | -0,7% | 6,6% | 4,3 |

| Amadeus | 26,4 | 13,5 | 17,7 | 24,8 | 7,7 | 4,8 | 29,7% | 20,9% | 15,7% | 1,1 |

| Travelport | 1,8 | 6,8 | 11,4 | 16,0 | neg. | 0,73 | 12,1% | 5,7% | 8,4% | 3,9 |

The table shows clearly that Amadeus is not only the biggest player, but also the most profitable one.

Interestingly, Travelport, the smallest of the 3 looks better than Sabre. Sabre is highly indebted, a heritage of its Private Equity past.

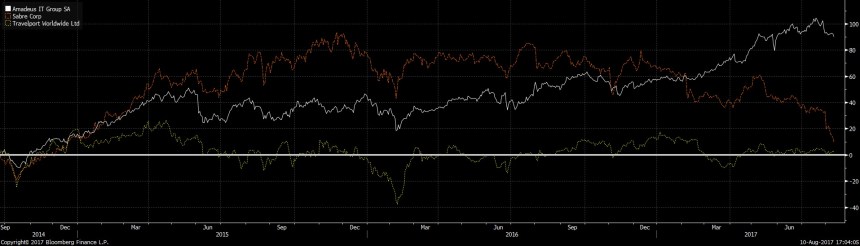

Stock price development:

Over the last 3 years (both, Sabre and Travelport went public in 2014), only Amadeus managed to show good returns. Sabre did well after the IPO but then got hammered especially in the last 12 months. Travelport somehow never moved much above its IPO price.

Quick check Sabre

Sabre in fact looks like the most vulnerable of the three. Being in an industry with signficant change ahead, having a big debt load could be a problem. Not surprisingly, short interest in Sabre is almost 17% of free float, a pretty large amount. Personally, even if Sabre would be cheaper, I would not invest in them as there is clearly a lot of risk due to the high debt load. 6M numbers didn’t look very nice if you ignore the many adjustments. Cash is down, debt is up so things don’t look that good.

Quick check Amadeus

Amadeus seems to be a class of its own in the GDS space, nevertheless, paying 25 times earnings or 18 times EBIT for a company that faces potentially disrupting changes is too steep for me in order to justify a deeper analysis at the current stage. I guess they will survive one way or the other but what that means for future profits seems to be quite difficult to forecast.

One needs to mention however that H1 2017 numbers were extremely strong, with profits increasing double-digit percentage points. As in many cases, quality seems to come at a price.

One part of their success seems that they integrate themselves deeper into the Airlines back office systems (for instance ticketing) so that they become more an IT service provider than a ticket distributor.

However I would be only interested if the price tag would be lower, below 20x earnings in order to invest more time into them. The Euro crisis would have been a good time to buy the shares…..

Quick check Travelport

Travelport finally looks in relative terms as the most interesting candidate for a potential investment. 6M numbers were strong and the company has earned already 0,73 USD/share in the first 6 months.

Travelport also has an interesting division callet eNett which offers integrated payment solution to their clients based on “Virtual Credit Card Numbers”. This business is growing very quickly. Based on their projection (500 mn sales in 2021) and current multiples for similar firms, this division could create a lot of value for Travelport.

However, their earnings record in the past was somehow not spectacular and usually they made a loss in Q4. Similar to Sabre, their financials show their private equity past. A relative large debt burden and negative GAAP equity do not fit very well with my personal investment style. For Travelport to be more interesting, I would need to see a couple of good quarters in order to gain more confidence in their overall business.

Summary:

The GDS players were the dominant force in international airline bookings for a long time. These days however, the really good times seem to be over, at least in airline bookings. Nevertheless they still hang around and try other things like payment systems (Travelport) or IT services (Amadeus).

Amadeus seems clearly to stand out but also looks very expensive. Sabre and Travelport unfortunately show their Private Equity past in highly leveraged balance sheets. Without digging too deep, Travelport looks more interesting, especially with regard to its eNett subsidiary.

However at the time being I might not dig deeper into them, as they are either too expensive or financially too weak.

Correct. My post is an “outsiders” view and might be totally wrong. As an investor however the question is: Will this stay forever or will others “disrupt” this business model. Plus will the pressure on fees continue ?

I am not sure. But maybe I know too little.

It seems that you don’t work in the industry, as you can’t see the real value added. For instance, how do you manage groups, events, checking at the airport, how do you define the prices of the tickets. How do you keep track of the services (meals, pets), customer experience management (people flying, their value and what you can offer them). What happens if a flight gets cancelled, how do you rebook people on alternate flights? How do you detect fraud? And this must work the whole day the whole year, getting billions of transactions per day (just imagine what happens if the system goes out an hour in the airports). So it’s not just a repository.

And concerning your analysis, Amadeus is way bigger than the others in Asia, and is increasing it’s market in America (southwest,air Canada, navitaire acquisition), that can explain why it’s still growing.

Good post. I was awaiting it for weeks. My two cents follow.

I have been tracking Amadeus since I saw it was a FUNDSMITH investment (hence there is probably some quality!). Return On Capital Employed (ROCE) is high, and growth comes both from:

1. the growing number of passangers and the cost advantage of scalability of their systems (negligible productions costs for each additive passenger, but mostly profits), and

2. their ticketing infrastructure & operation business which otherwise would be very expensive for airlines if they have to develop their (99.999% reliable) systems at competitive costs. Developing such systems on your own is economically unrealistic versus the use of an existing solution that only needs adjustments (despite the latter will come at a high price with high margins).

Because of all competitive barriers, disrupting the GDS business (ie. Amadeus) may be as ‘easy’ as disrupting coca-cola with a new product….

That said the volatility of Amadeus has been quite high and its financial performance will be highly correlated with the economic cycles (more business & more disposable income translate in more travelling).

Not long in the company, but in the radar just in case it falls to an attractive PE ratio.