Northgate Plc (NTG): Just another vehicle rental/leasing company ?

![]()

Business / Background:

Northgate is a UK based company that specialises in what they call “flexible rental” of smaller delivery vans to small businesses. My main interest in Northgate is not that I am so bullish on the UK and this sector, but that this company is somehow similar at least to the GoGetta part of Silverchef and I was looking for a peer company in order to be able to compare some metrics.

On a stand-alone basis, Northgate looks cheap:

Market cap: 570 mn GBP

P/E: 9,3

P/B: 1,1

EV/EBITDA 3,7

Div. Yield 4,1%

Business model:

Similar to Silver Chef’s GoGetta, Northgate rents out Light commercial Vehicles (LCVs) to small business, although mostly on a shorter term basis and without a “purchase option”. According to Northgate’s presentation, the companies’ competitive advantages are the following:

Core Strategic Advantages» Significant OEM purchasing terms» Low cost of debt» In-house workshop networks» Van Monster disposal channel» Low cost entry to fixed term product adjacencies

So let’s look at them point by point:

Significant OEM purchasing terms

This is clearly one advantage touted by many leasing or rental companies: they can buy cheaper than the “average Joe”. When I looked at AerCap, this was basically the only justification. I think this advantage has some merit but Northgate with around 80k vehicles is not a huge player.

Low cost of debt

Well, these days I would say that this is a small advantage compared to the financing costs of the small business, but again, Northgate is a relatively small player. However it is conservatively financed.

In-house workshop networks

This is more interesting. Northgate manages a network of depots and 24/7 repair services which is an interesting aspect on top of the financing/rental business. I guess this might be cheaper for them then to use third-party or vendor services, as repair service (and spare parts) are the areas war automotive vendors these days earn the fattest margins

Van Monster disposal channel

For a rental/leasing business, being able to sell the vehicles at a good price is also important. Without having checked this in detail, it seems that Northgate has a relatively good own channel called “van Monster” to do so.

Low cost entry to fixed term product adjacencies

This seems to be their “new idea” to branch out from rental into longer term financing agreements. It will be interesting to see how they can convert and expand this going forward.

Main difference to Silver Chef /GoGetta

In my understanding, Northgate in its core business offers shorter term rentals than GoGetta plus more flexibility and Service. Gogetta “only” offers rental contracts for 12 months with a purchase option (or an extension) for a single asset. Northgate doesn’t offer the “Purchase option” which reimburses part of the rental fee paid in the previous 12 months. On the other hand, GoGetta offers a more diverse range of assets, Northgate specializes on LCVs.

KPI comparison with Silver Chef

Now comes the fun part. I tried to calculate and compare some KPIs from Nortgate with Silver Chef. Clearly one cannot compare the businesses 1:1 but let’s check if we can extract something useful:

From my point of view the following issues are especially striking:

- Whereas Northgates actually makes money selling vehicles (~16-24% of book value), Silver Chef shows losses (-12-16%) when they sell assets plus additional impairments which do not exist at Northgate

- Receivables from Silver Chef have increased. However the biggest difference is that overdue receivables at Northgate are more than fully covered with reserves whereas Silver Chef has reserved only ~20% of overdues.

- Silver Chef has leveraged their assets significantly more than Northgate. This is clearly a function of the strong growth whereas Northgate has been stagnating for some time now.

- Silver Chef has a lot higher gross margins, but that gets eaten up by “other costs” which are not really easy to understand for me.

So apart from growth rates , Northgate somehow looks much more solid than Silver Chef, at least based on these selected KPIs

Back to Northgate: Where is the problem ?

In Northgate’s case the problem is relatively easy to identify: The company is shrinking, especially in its core UK market. Interestingly, this seems to be a company specific problem so far. The 2017 annual report has a pretty decent “market & strategy” section which shows that in the UK, the rental market grew by +6% but Northgate lost around -5% of sales. The new CEO has identified and addressed the UK issues like this:

Some key weaknesses have persisted which have contributed to this performance, namely:

| Leadership: aligning business priorities to the changing dynamics of the market;

| Marketing: insufficient lead generation, digital innovation and customer data acquisition;

| Sales: insufficient time in front of customers, price inflexibility and conversion of opportunities;

| Talent: fragmented leadership and insufficient access to strong commercial talent; and

| IT: legacy systems are inflexible, not supporting required changes.

A number of self-help actions have already been taken to fix these weaknesses:

| New leadership appointments in the UK executive team to Managing Director, Sales Director and Marketing Director roles;

| Tactical changes in sales and marketing, introducing enhanced pricing flexibility and re-directing spend in lead generation through telesales and digital channels;

| Formation of a small commercial centre in Reading in order to access a wider talent pool and work collaboratively; and

| Replacement of core IT systems is underway

By browsing previous annual reports, the IT system issue seems to be an old one. Already in 2012 they talked about this issue.

On top of these company specific issues there is clearly the Brexit issue looming like in many other UK-based companies.

Where is the upside for Northgate Plc ?

Spain:

One obvious upside potential is the fact that almost 50% of the operating profit comes from the Spanish subsidiary. Although it shows less sales than the UK market, it is more profitable and seems to grow strongly. After a long period of struggle, Spain was the first “Club Med” country that seems to have (for now) left the crisis behind and things look a lot better than before. In its latest trading statement, it clearly looks like that Spain is doing well for Northgate these days.

“Fixed Rental” product

This is Northgate’s entry into what one would normally call “leasing”. This is what they say in their report:

2. Gain share in fixed term markets We see a significant opportunity to grow our

share of the contract hire market. At £2bn in market revenue, with volumes growing at 8% per annum and both EBIT margins and return on capital similar to that of flexible rental, we see an outstanding opportunity to grow from a position of low market share today. We see this as a natural adjacency requiring limited variations in our operating model to serve it and with substantial opportunities to cross sell within our existing customer base.

If that strategy works, this could be interesting. The market is twice as big as the rental market according to Northgate. Northgate claims to have on average ~30% market share in rentals (Ireland, Spain & UK) but close to nothing in fixed rental. So theoretically, if they could just get half of the market share they have in rental, they could still double their sales.

On the other hand, the fixed rental product might also be a bit riskier for them. But we will see, at least it looks like a potentially interesting growth opportunity.

Financial crisis 2008-2010 – lessons

Before getting too excited about the company, let’s look what happened back in 2009/2010 after the buig financial crisis. Back then, Northgate got into trouble and had to issue a distressed capital increase:

By the end of the 2008 financial year the Group had aggressively expanded its fleet to a level of 68,600 vehicles in the UK and 62,750 in Spain, but some of this growth had been at the expense of margins. When the recession hit, utilisation levels fell in 2009 to 88% in the UK and 83% in Spain, compared to historic rates

of over 90% and the problem was exacerbated by a dramatic fall in vehicle residual values in both the UK and Spain. This put inordinate strain on the balance sheet and, at the beginning of the financial year, the Group raised £108m (£77m net of equity and debt arrangement fees) from a rights issue, thus refinancing its debt and securing the capital structure up until September 2012

The big issue was of course too much leverage before the crisis. In 2008, the company had around ~1 bn GBP in rental assets, financed by around 900 mn GBP net debt. Only 400 mn equity secured this. However then in 2009, the company had to write down 200 mn (or around 20%) of its fleet which then lead to the capital increase as too little equity was supporting the huge debt load.

Looking at the KPIs above, we can clearly see that Northgate these days is managed much more prudently and seems to have learned its lesson.

No one knows how the Brexit issue will continue but I do think Northgate is less exposed to a downturn than in 2008/2009

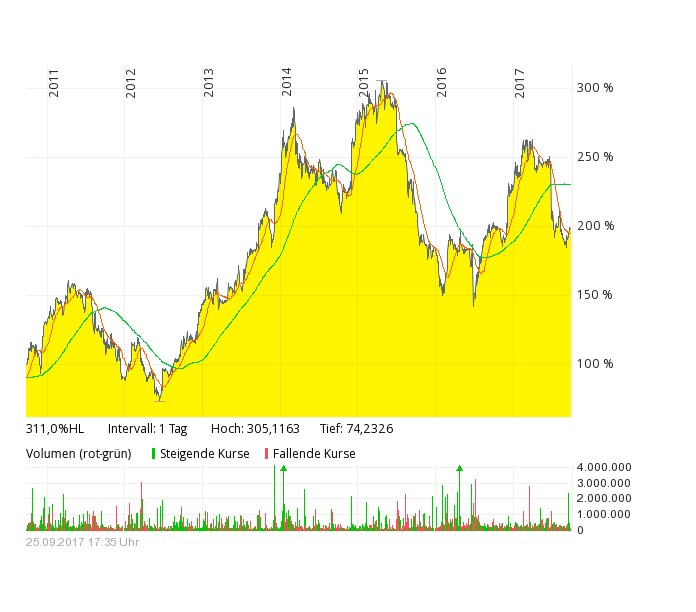

Stock price:

It is interesting to see that the stock has been suffering well before the Brexit:

I guess this is directly related to the fact that profits at Northgate topped in 2014/2015. Interestingly enough they had a strategy as well in 2014/2015 to improve business. Back then they wanted to open more depots and offer more different types of vehicles whoch obviously didn’t generate the desired results.

Quick Pro & Con summary for Northgate:

Pros

+ looks cheap

+ financially conservative (lessons learned from financial crisis)

+ underlying market seems to be still growing (before Brexit), so no structural issues

+ clear strategy under new management

+ interesting growth options

Cons

– cyclicality & issues in the core UK market

– Brexit

– new management /turnaround (liitel stock ownership)

– execution risk for new market segment

Summary:

My initial reason to look at Northgate was mainly to have a peer company to Silver Chef. Compared to Silver Chef, the company looks a lot more conservative, however the core UK business has been shrinking for some time now.

Nevertheless Northgate looks quite interesting on its own. It remains to bee seen how the new CEO implements the new strategy, but I will keep the stock on watch for early signs that they will manage a turn around in the UK. then the stock could be quite interesting.

For Silver Chef, I think I did too little research into the underlying business model when I bought the stock. So far I will still keep the position but I still need to learn more about this kind of business. So I might look at further rental/leasing companies.

Hi, it could be good time to review Northgate. They came out with a trading update this morning, which was taken negatively by the market, but includes several positive elements. The fleet is growing again after a long decline. Spain is on fire and the UK finally seems to be on track to stabilize the business. After a review, management has decided to let the fleet age a bit, which means that they are selling a lot less vehicles for a couple of months and profit from disposals will be a lot lower in the short term. This was given as an explanation for lower profits this year. The market seems to focus completely on the short term profit impact, but in future periods a slightly older fleet on average should lead to higher RoCE. The shares are now trading at ca 80% of TBV, which in my mind is not consistent with a growing business and attractive returns.

Thanks for the comment. the only thing I ask myself:. Maybe they are not able to sell the fleet at book value and need to postpone ? This would be a more negative interpretation of the strategy shift.

It seems obvious that mistakes were made in selling vehicles at a relatively low age, when they have not been depreciated enough to earn attractive PPU. As the fleet is also growing, they had to replace those disposals with new purchases, which drove up capital employed and debt. Letting the fleet age a bit takes away disposal profits temporarily, but should allow higher RoCE in the future. As far as I can tell, there is no indication that demand for second hand vans is lower in Spain or the UK. At the current mkt cap, one could argue that Spain alone justifies that value and rest is for free.

Not before a post-mortem analysis of silverchef I’d say….

Silver Chef is in the process of reducing its light commercial vehicle (“LCV”) exposure dramatically. This is owing to poor experience in the LCV market that has seen significantly lower credit quality than the more ideosyncratic equipment types that GoGetta set out to rent out in its beginnings. Hence, going forward the similarities with Northgate should reduce further.

Maybe Synchrony Financial A117UJ can be to large.

Are you familiar with Ixus, a large Japanese leasing company listed in Tokyo & NY via ADRs.

No never herd of them…do you have the ticker ?

Grenkeleasing

done that…

https://valueandopportunity.com/2016/04/04/free-cashflow-reporting-doing-it-grenke-style-grenke-silver-chef/

Thanks a lot for the interesting analysis, mmi. I have high esteem for how you consistently question investment cases after your investment.

No, I am actually not analyzing car rental companies. Northgate is a “business to business equipment” retal company. This is very different from a B2C car rental company.

Sixt is much more a “retail consumer” company. This is a different business model.

If you are analizing car rental companies: What about analyzing Sixt?

In the last tens of years the company has shown a simply amazing development. Actually they seem to experience a strong growth in the United States, what should be a kind of saturated market for car rentals.

What do they do different that they can profitably outgrow their rivals in such an amazingly way? (I have no clue at all!)

The stock is expensive. But if they can continue their strong and profitable growth, the share price may be attractive.

As a shareholder of Sixt Vz (with entry at 25€ where I considered it quite cheap) I can say that I do have a clue about their strengths: They are efficient and have the self-esteem to stay away from price wars and low-margin business, partly because they offer more premium brand rentals. At the same time they work very efficient and have really good marketing campaigns, and if you compare the margins with Avis/Budget and Hertz you see that they are bound to outgrow the market for years (they still can lower prices while the others already bleed). But they are quite expensive indeed, I guess the chances are good to pick them up at a better price in the next downturn.

MMI is right that this is another business, mainly due to different kind of marketing, service differentiation and (especially in the south european tourist hotspots) a very very high seasonality of the business. But still similar enough that I can imagine Sixt venturing into B2B leasing like Hertz for example also does.

@ MMI: As everyone makes suggestions for commercial leasing peers, did you look at eastern european companies like Herkules SA or AviaAm Leasing ? They have higher volatility but still might be interesting.