Softbank Part 2: Sum-of-parts Valuation and don’t forget the Taxman

A couple of days ago, I looked at Softbank more from a strategic point of view. This time I want to focus more on the actual assets and a sum-of-parts valuation

What is Softbank ?

Essentially the company at its core is a Telco company in Japan and US plus a lot of “extra assets” like the Alibaba stake, Yahoo Japan and then all the other stuff including the vision fund. The initial Software distribution business (this is where the name Softbank comes from) doesn’t play a big role anymore.

I will now try to walk through the major Softbank Assets in more detail:

- The Alibaba stake

Let’s start with the largest position first, the now so famous Alibaba stake. From a technical perspective, Softbank doesn’t own the listed shares but this:

Similar to the Yahoo Holdings Inc. spinoff Altaba Inc., what SoftBank owns in Alibaba isn’t the liquid American depository shares listed in New York, but “registrable securities” that lay claim to Alibaba’s Cayman Islands-based holding company.

The article goes on to explain that registration and trading are possible but that this process is not entirely straight forward.

Softbank’s 29% stake is worth around 136.6 bn USD on paper. The big question is however: If and how large are the adjustments one should make with regard to illiquitiy etc. ? Average trading volume for the listed Alibaba shares is between 3-4 bn USD per day, so the position is around 40 full trading days volume which is not that much (in theory).

Interestingly enough we can look at another listed company to get a better feeling about this: Altaba, the remainder of Yahoo. Yahoo sold its operating business to Verizon and what remains is a large Alibaba position and one in Yahoo Japan (plus some change).

Based on the information of that latest SEC reporting, this would be my attempt of an Altaba sum-of-part valuation:

| Altaba SOP | No shares | Price | Value |

|---|---|---|---|

| Alibaba | 383.6 | 184 | 70,582.4 |

| Yahoo Japan | 2025.9 | 4.78 | 9,683.8 |

| Bonds etc. | 5,000.0 | ||

| Total Assets | 85,266.2 | ||

| Market cap | 64,940.0 | ||

| Discount | 20,326.2 | ||

| in % of value | 23.84% |

The result is a ~23,8% discount. So should we use this as a proxy for Softbank’s Alibaba and Yahoo Japan stake ?

Not so fast. One issue with the Alibaba Shares in Altaba is taxes. The Alibaba shares (and also the Yahoo Japan shares) are subject to capital gains tax which in the US is taxable at the full corporate rate. Assuming that the unrealized gains are more or less equal to the actual value, the discount actually reflects the taxes to be paid (at the new Corporate Tax rate), so there is little or no structural discount observable for the fact that the Alibaba shares are unlisted.

There was always a discussion if and how “old” Yahoo could avoid taxes on the stake but in the end, no solution has been found (yet).

However, the same issue applies for Softbank. Under Japanese law, capital gains are normal corporate income and subject to the Corporate Tax rate. I have no idea if there are ways in Japan to get around those restrictions but to be on the safe side I will deduct ~31% both, from the value of the Alibaba stake and the Softbank Japan stake plus another 10% for the fact that the shares are not listed.

On the positive side, I do think that Son’s relationship to Jack Ma opens him a lot of doors in China. However this is something I do not include in a “sum-of-.part” valuation-

2. Softbank Telco Business Japan

This is clearly the “crown Jewel” and cash cow of Son’s empire. The core of the business is Vodafone Japan which he acquired in 2006. Based on 6M number I would assume that The Telco Business will generate around 1.100 bn YEN or 10 bn USD in EBITDA in the current financial year. Assuming a 6xEV/EBITDA multiple (competitors Docomo trade at 6,9x, KDDI at 5,4x), this company should be worth around 60 bn USD.

Just recently, there was talk of Softbank IPOing this business with an estimated valuation of around 70 bn:

The mobile business has an enterprise value of about $71 billion, according to Chris Lane, an analyst at Sanford Bernstein. Smithers has a similar valuation. The final amount will depend on how many liabilities are attached to it before the listing, Lane said. The SoftBank group had 12.1 trillion yen of net debt as of September.

However there seem to be some technical issues: According to a Bloomberg article, the Mobile unit has guaranteed most of Softbank’s corporate debt. Plus, Rakuten, a Japanese Online retailer seems to try to set up a 4th mobile network.

Without knowing too much about mobile networks, my rule of thumb was always that 3 networks is Ok but 4 could be a problem. In the article I linked to there is also talk of the Japanese Government actively pushing for lower prices. So I think using a more conservative valuation is appropriate.

3. The ARM stake

In a pretty surprising move in July 2016, Softbank bought UK chip maker / designer ARM for around 31 bn USD. This looked like a very steep price at that time.

However looking at other chip companies like Intel, AMD, Texas Instruments or Qualcomm we can see that chip companies are on a run since then and have gained between +14% (Qualcomm) and +110% (AMD). So maybe Son overpaid back then but by now I think one could use the purchase price as approximation for the fair value.

Son has contributed 25% of ARM “in kind” into the Vision fund (at cost) in order to fund part of his commitment which in my opinion is a smart move and saves him some cash.

4. The Sprint stake

Softbank initially bought around 70% of Sprint in 2012. Last year there was a lot of talk about a merger of Sprint and T-Mobile but in the end Son called off the merger. Sprint is in a difficult situation and carries significant debt, on the other hand at current prices the company looks cheap. Maybe one reason why Softbank is adding to its stake.

For the sum-of-parts, I just use the market value although one could argue that there could be some kind of control premium.

5. The Yahoo Japan stake

Yahoo Japan is a JV between Softbank and Yahoo established in 1996. Yahoo successor Altaba holds around 35%, Softbank 43%. Although the company quadruped sales since 2007, the stock price is well below its peak in 2006. This might be caused by a decrease in EBITDA margins which went down from 50% a few years ago to around 25% right now.

At some point in time Altaba might want to sell its stake and Son would be the natural buyer. If he has enough money at that point in time. As mentioned above: The Yahoo Japan stake was acquired very cheap, so capital gains tax will apply here as well and has to be adjusted in a sum-of-parts valuation.

6. Anything else

Among the other assets, I just want to point out one: The Vision fund. In my opinion this construct both, has intrinsic and strategic value. However I would just look at the intrinsic value.

What Son did was to create an alternative asset management company with around 65 bn of external funds from scratch. Usually, alternative equity managers are valued at around 5-10% of AUM. For the Vision Fund I would use the lower bound as it is not fully transparent how the arrangement actually works.

7. Debt /Cash

I assumed that the Sprint debt is “Non recourse” to Softbank and therefore excluded it for the NAV calculation. All other debt has to be deducted from Softbank’s sum-of parts calculation

Bringing it together: Sum of parts valuation:

This is a summary valuation based on the assumptions outlined above:

| “NAV” bn USD | Pre Tax | After Capital gains tax |

|---|---|---|

| Listed stocks | 167.39 | 113.3 |

| Unlisted stock | 99.34 | 99.34 |

| minus net debt | -67.3 | -67.3 |

| Total Sum-of parts | 199.4 | 145.4 |

| Market Cap | 91.2 | 91.2 |

| in % of NAV | 45.73% | 62.73% |

| Discount | 54.27% | 37.27% |

| Theoretical Upside | 118.66% | 59.40% |

We can see that the capital gains tax on Alibaba and Yahoo Japan significantly reduces the discount as those positions are basically 100% unrealized gains. Interestingly, I have never read about this in any Softbank analysis so far where analysts only compare the market values with Softbank’s market cap. I would be highly interested if a reader has experience with this issue as this clearly reduces the unadjusted discount significantly.

What discount is appropriate ?

Surprisingly already 5 years ago I had written a post on this topic. This is what I said back then:

For myself, I distinguish between 3 forms of holding companies:

A) Value adding HoldCos

B) Value neutral HoldCos

C) Value destroying HoldCos

What kind of HoldCo Softbank ? In the past, Son clearly added value by doing great deals. He also can travel to the Sheiks and come back with a 60 bn USD commitment. On the other hand, Softbank is not nearly as transparent as for instance Kinnevik and the significant leverage creates significant risks for the shareholders. That nearly wiped out the company after the Dotcom crisis.

So if I get Kinnevik for a 20% discount with very transparent reporting, no debt and a 80 year track record, I would say that Softbank should at least trade at a similar or even higher discount. So assuming a 30% holding discount, Softbank would be slightly undervalued but not by much.

ANother aspect for Holdcos is the following: It is preferable to invest in HoldCo’s where capital gains are not taxed at the full Corporate tax rate,.

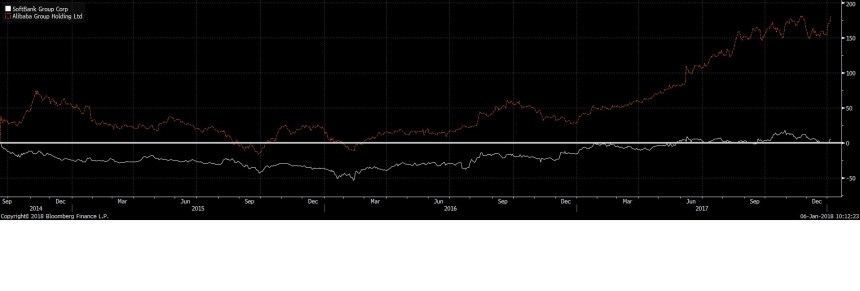

Stock price

When we look at the stock price of Softbank over the last 10 years we can see 2 things:

- the stock has almost quadrupled over the last 10 years

- but almost all the performance was achieved in 2013

My guess is that this is related with the excitement of the Alibaba IPO in September 2014 which at that time was the biggest IPO ever.

One thing I found remarkable however is if we compare Softbanks stock performance after the IPO with Alibaba:

Alibaba almost tripled since their IPO in 9/2014 whereas Softbank hardly gained in value at all over the last 3 years and 3 months. That’s kind of strange considering that the tripling of the Alibaba stake increased Softbank’s stake by more than 100 bn USD. Some of this might be explained with issues both, at Sprint and in the Japanese Telco business but not everything.

Other issues

.Succession is clearly an issue. Although Son claims that he will only need to find a successor in 10 years, the issue is that he had chosen a successor earlier with Google’s previous “number 4” employee Nikesh Arora. However in 2016, Arora suddenly quit and it is not really clear why.

There is also a small series of critical posts from the “Deep throat IPO blog” about Softbank and Alibaba. For instance:

“The Art of self dealing” (Softbank)

“Anatomy of financial Contagion” (Softbank)

I think it is clear that Softbank uses significant financial engineering. However one should also be clear that even the “Master” Warren Buffett does do similar things in order to leverage his success. “Deep Throats” major concern seems to be that Softbank on a consolidated level shows a lot of Goodwill a little “tangible net equity” but this is normal for digital investments. And to be honest: I find the balance sheet of Softbank much easier to understand than that of Berkshire Hathaway where I am not able to do a sum-of-parts analysis.

There are clearly question about what kind of numbers Alibaba produces, but in theory any Softbank buyer could hedge out this risks with an Alibaba short position.

In total I think all those issues clearly support the previous point, that some sort of discount to NAV is clearly justified compared to transparent companies like Kinnevik.

Summary: Not cheap enough (after tax)

Masa Son’s Softbank is really a unique company with a unique leader. He clearly has shown that he can allocate capital and do good deals (Alibaba, Yahoo Japan, Vodafone, Supercell), but for some reasons he prefers to leverage himself up as much as possible. He is an “outsider” in many aspects which is something I usually appreciate very much, but the combination of volatile high-tech assets and “full recourse” leverage makes Softbank quite risky.

He has also “disrupted” the market for financing tech companies in the last 2 years and his Vision Fund is something that few others (or actually no one) could achieve so far.

At first glance, Softbank seems to trade at a massive discount, but taking into account potential taxes on capital gains, this discount shrinks significantly.

At the end of the day, I think there might be some upside at the current level of the share price but not enough to fully compensate for the risk. So no investment unless it would turn out that the tax issue isn’t an issue at all.

P.S.: I think it is still worthwhile to follow what Softbank is doing. I am pretty sure that we could see more “Mega Tech funds” in the future. And maybe less IPOs….

P.S.2: Just after writing this, I saw this article in the WSJ about Seth Klarmann and Baupost:

Mr. Klarman also sees potential value in so-called unicorns, private companies with billion-dollar-plus valuations, that collapse on disappointment. In the thin markets for such private companies, it may be possible for Baupost to step in on preferential terms when promising companies stumble, says the letter.

So it looks like that Masa Son will soon get competition for his next “Uber like” deal. It will be interesting who else will try to mimic this. Maybe even Berkshire ? Who knows…..

Thank you but I have to say there is one mistake with regards to taxes. When a company uses the equity method it recognizes income each year which is taxed. So Alibaba’s book value is actually around $18 B now… hence taxes are already set aside for that amount. So the capital gain would be Alibaba’s current market value minus its book value * the rate. So taxes would be lower by 31% by $18 B on just that one position

Although I am not particularily interested in Softbank anymore, I think you have made a mistake unless you are a super expert on Japanese taxation.

In almost any jurisdiction, taxes apply for stock holdings on dividends paid and gains realized. An “at equity” accounting normally doesn’t trigger a tax liability (the income has been already taxed at the level of that company). My best guess is that Softbank has not accrued tax liabilities on the at equity earnings unless you can show me in detaul where this can be found in the Japanese Tax accounting rules.

IF sb is interested: I (also) tried to value Softbank Group and concluded it is worth buying…

https://searching4value.wordpress.com/2019/10/16/sftb/

How did you calculate the debt?

If you actually read the post, you’ll find ihr. 😎

still didnt answer how you came to the exact number of 67.3

well, you will have to do exactly one simple calculation and this is described in the post.

Maybe one hint: Friendly question, friendly answer. Unfriendly question…….

well i still find it a bit unclear upon reading the article again. would you be able to mathematically explain to me the 67,3 in the comments section? would be much appreciated

Weil, just read the post and look dir the wirds gaap and Sprint.

Hi, I did a quick debt calculation and got ~142bn usd. Can you please explain how you got your number?

Hey don’t you read the post ? It’s not that difficult.

I bought SoftBank at around 55 $ per share two years ago. Fair Value was for me around 105$ per share. I saw, for an european, SoftBank like an Option on the Asia/India tech market in future.

Sure its not necessary to be in the Asia/India tech market.

We will see.

Good analysis, I agree with most points of your points, but I have a different view on the following:

1) Value of the Telco business

In the last financial year, the FCF was 5 billion USD. Based on your valuation of 60 billion, that would be a FCF-multiple of only 12. That appears very low in today`s markets. We`ll see soon, but for me the 68 billion valuation that would be implied IPO target appears more realistic.

2) Other assets

What about Softbank`s other assets such as SoFi, Didi, and so on that were bought before the vision fund was installled? According to the FY2017 presentation these stakes have a value of 8.8 billion USD. They may be included in your “unlisted stock” component, but since you do not excplicitly mention them, I am not sure they are included. As other assets, which are in total 99.34 billion USD in your SOP calculation, you explicitly mention the telco business (60 billion USD) and Arm (23,75 billion USD). Where is the remaining 15.6 billion USD coming from? Softbanks contribution to the vision fund is 25 million, though it is not clear to me how much they have contributed by now…

3) Taxes

Your treatment of capital gains taxes assumes that Softbank would sell all these assets today and therefore have the respective tax bill by now. Son is a very long term holder and typically intends to never sell. What if Softbank never sells these assets or lets say in 30 years? In my opinion the tax bill would have to be discounted and the effect would be large.

Alibaba and Supercell were the exception from the general rule, as Son for years wanted to buy Arm and finally saw the opportunity. I can imagine that Son would sell some assets in the near future to contribute equity to vision fund II and III. Then however, there would be also a lot of value creation due to the external funds raised and the respective fees earned on that (See your value for the vision fund). So I would not assume a respective tax discount for partial sales to enable further vision funds if there is at least equivalent value creation on the other side of the coin.

4)

It would be great to read a bit more about your rationale for the 30% discount. Is that the long run historical average for conglomerates? In my opinion, based on Son`s track record, if at all, there should be a premium. You pay 2% fees for on average crappy active mutual fund managers, you pay 2/20 for on average crappy hedge fund managers. Private equity funds have a solid track record on average, but they also charge 2/20. And then you have this wonderful perpetual investment vehicle that Son has created with a visionary CEO that has a hell of a track record and that suddenly qualifies for a 30% discount?

PS: My take on Nikesh Arora`s leave is that he was disappointed that Masa suddenly wanted to stay for 10 more years. Son announced Arora effectively has his crown prince and said he wanted to retire by the age of 60. Then he changed his mind because he saw so many opportunities (too energized). Arora brought a lot of qualified people to Softbank that now have major roles in the vision fund, also Arora opened the door for Son for Indian PE investments.

An alternative story is that Arora made mistakes (self-dealing or overpaying for stakes in India) and was fired.

Anyway, I cannot see how Aroras departure is a negative for Softbank. 10 more years of Son at the helm was great news for me. And who knows if Son can really stop by the age of 70. I find that hard to imagine and would not rule out that he stays as long as he feels he is doing a good job and is excited (like Munger and Buffett). Remember, this is not some CEO that is hired for 5 years and then moves on or retires. It is his company.

Thanks for the comments. Indeed I tried to include the other assets in the unlisted buckets but in my opinion the disclosure here is not optimal.

Value Telco: Clearly you can use any multiple you like but I’d like to stay on the conservative side

Taxes: I disagree. These taxes are a liability which you have to deduct from the NAV. You could think of discounting them but leaving them out would be a mistake

30% Holdco discount: I think I made that clear. If a transparent Holdco like Kinnevik trades at a 20% discount, then a highly leveraged and somewhat intransparent company like Softbank requires an ever higher discount. Of course you can have a very different opinion on this but this is mine 😉

Everything stated in my posts is just an opinion, it clearly doesn’t need to be the ultimate truth.

mmi