How to invest into Venture Capital part 2: Augmentum, Vostok & others

This is the follow-up on part 1 some days ago.. These were the listed VC vehicles,I presented as the base in part 1 (in brackets my short vote for the first 4)

- Softbank (too crazy)

- Kinnevik (Yes)

- Rocket Internet (bad rep)

- German Startup Group (no thanks)

- Vostok New Ventures

- Vostok Emerging Finance

- Augmentum

I have added two US vehicles to this list:

- Firsthand Technology Value Fund (SVVC)

- GSV Capital (GSVC)

A few thoughts on Permanent Capital vs. “classical” fund structure vs. “SPACs”

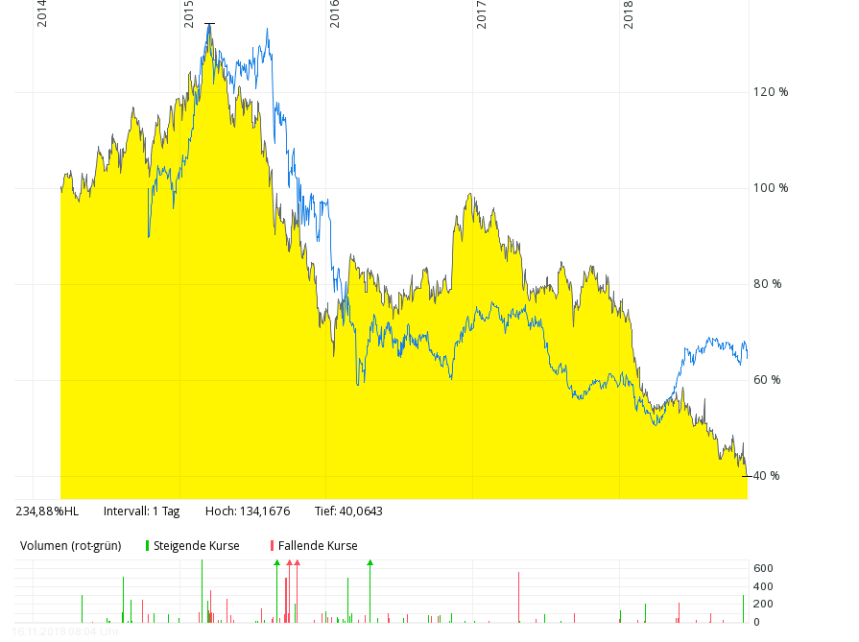

In the previous post, one commentator mentioned that he was “sceptical of permanent capital” vehicles. Personally I would not support this. Berkshire Hathaway for instance is a permanent investment vehicle with quite some success. However there are other vehicles like Greenlight Re or Bill Ackman’s Persing NV which clearly have done a lousy job for shareholders as we can see in this chart: (Greenlight in yellow, Pershing Square blue):

A “classical” VC or P/E structure is usually dissolved after 7-10 years and cash is send back to investors. This has a few advantages like avoiding for instance that asset managers charge performance fees on paper profits. However, the structure also has negatives, as towards the end of the fund life, managers often HAVE to sell and can therefore not maximise profits from successful positions. Another issue is that such funds only contain investments of a certain “vintage” as the investment period is usually only 1-3 years or so

In Einhorn’s and Ackman’s case I think one of the additional issues was that they all created their permanent vehicles after a long positive streak with most likely too much AuM which then created the problems we have seen in the past years.

In my opinion, a permanent capital structure is best for a really long-term investor, when incentives are properly aligned, i.e. no management fees are “sucked” out of the vehicle.

SPACs in contrast suffer a little bit the same issue than a normal fund: Money is collected at a certain point in time and then management has to invest which I think is not super optimal.

Kinnevik for instance is a permanent structure but what they often do is to distribute their holdings to shareholders if they think that they cannot add value any more, for instance they distributed their Modern Times Group shares fully to shareholders in 2018.

One of the major issues with permanent listed vehicles is the existence of carried interest. If managers are paid for carried interest in such a set-up, they always have an interest in keeping as much money as possible and they do not care about any discount to NAV of the listed securities. In my opinion for listed vehicles, share ownership and/or carefully structured option plans with the shares as underlying are the much better alternative.

Augmentum PLC

Augmentum is a specialised Fintech VC that IPOed in early 2018. The portfolio consists of mostly UK-based Fintech companies. Some of the investments were brought into the vehicle in the beginning from a previous fund, the rest is used to make new investments.

Overall, I would judge it as an interesting play on the UK Fintech scene. The management of Augmentum is experienced and they have access to good deals. The company is back by RIT Capital, an investment vehicle of the Rothschild family.

My only concern would be if now is the best time to invest into UK Fintechs with Brexit on the horizon..

Fee wise, the structure seems to be 1.5%/15% for the advisor (1.5% managment fee, 15% carried interest) with a hurdle rate of 10%. For VC terms this is Ok, but clearly not cheap.

Vostok New Ventures & Vostok Emerging Finance

Despite its name, the two Vostok vehicles are Swedish based companies. This is what they say about the history of the company on their website:

Vostok New Ventures was founded in 2007 in connection with the restructuring of “Old Vostok Nafta”. Even though Vostok New Ventures was formed as recently as 2007, we have a history dating back to 1996 when Adolf H. Lundin founded “Old Vostok Nafta” with the business idea of implementing portfolio investments and direct investments in the former Soviet Union. The investments were initially conducted in the oil, gas and mining industries, but is today focused on Internet and consumer focused sectors in Russia and other markets.

At some point in time, Vostok changed its focus on venture capital, but as a result of its (successful) Russian past both entities have their largest investment still in Russia.

The company initially called Vostok Nafta spun off Vostok Emerging Finance in 2015, consisting mostly out of their very succesful (and now listed) investment into Tinkoff Credit Systems (TCS). The remainder was then renamed Vostok New Ventures.

Vostok Emerging Finance

As Augmentum, Vostok Emerging Finance is a “Fintech” investor, however with a clear focus on Emerging Markets. The largest position is still Tinkoff Credit Systems, the Russian Credit Card / Online bank with ~24% of the portfolio as per Q3.

They are selling down TCS slowly in order to allocate money to other regions. The second largest position is Creditas, a Brazilian Fintech with 12% of the portfolio, followed by another brazilian Fintech (9%) and a Turkish Payment company.

So clearly, Vostok Emerging Finance is exposed to many regions where some stress is in the markets. On the other side, the stock has performed quite well since spin-off, despite the pullback this year:

With an NAV of SEK 2,79 per share, the discount at the current 1,75 SEK per share is a quite substantial 36%. I guess some kind of discount might be warranted but this looks a little bit overdone.

Vostok New Ventures

Vostok New Ventures specializes mostly in online classifieds / Marketplace venture investments, the portfolio can be seen here.

More recently they also did more investments in Healthcare and mobility, but often with an Emerging Market focus.

What I do like about Vostok New Ventures is the fact that they report quite transparent and explain their portfolio companies quite well in their official reports.

The biggest risk at Vostok New Venture is clearly the fact that 61% of their NAV consists of Russian Online Classified company Avito, so the portfolio is much more concentrated that at the sister company. However, similar as Kinnivik’s Zalando position, for a venture capital company it is pretty normal to have large single exposures if you hit a real home run. Interestingly, Avito is paying already substantial dividends to Vostok.

AVito itself could become “liquid” at some point in time, as majority owner Naspers seems to be keen on buying out minorities in Avito and other holdings.

Interestingly, Vostok New Ventures also trades at a significant discount to NAV. As of Q3, NAV has been ~912 mn USD or ~ 98 SEK per share compared to the actual traded price between 65-70 SEK since the end of Q3.

Clearly investors apply a kind of risk discount with regard to the concentration risk with Avito, but still this looks like a large discount for a company which in my opinion is very well-managed. I do think that some of the portfolio holdings might be worth a lot more than they are showing right now, for instance Babylon is rumored to do a round with a significantly higher valuation as well as VOI, the E-scooter start-up just did a huge capital raise (for their stage).

What I like about both Vostok vehicles is the fact that they have an extremely lean set-up. Both companies are managed by only a handful of employees, which keeps costs down (see below). It’s worth mentioning, that Ruane Cunnif Goldfarb (“Sequoia Value”) own ~20% of the shares of Vostok New Ventures.

Other vehicles: GSVC and SVVC

GSV Capital (GSVC) has been mentioned by someone in the comments. It is an US-based vehicle claiming to be “the first publicly traded security enabling any investor to own a piece of the world’s most dynamic, VC-backed private companies.”

At first sight, the company looks interesting. It’s top positions are very well-known VC backed companies (Spotify, Palantir, Dropbox) and according to its latest presentation, Q3 NAV was USD 10.58/per share compared to 6,70 USD/share right now.

However, looking at the longer term chart, it is easy to see that they haven’t done well over the last years:

They seem to have distributed money along the way, but still, the performance seems to look weak compared to just buying a Nasdaq tracker fund.

The bad performance is difficult to explain, as their portfolio seems to consist of “the great names”. However a quick glance into the latest quarterly report shows some pretty bad stuff:

- the company employs significant leverage

- an incredible amount of fees is “sucked” out of the Vehicle. For the first 9 months 2018, ~10 mn USD of fees have been charged to the vehicle, after a 5 mn “waiver”. In Q3 2017 this number has been 18 mn and for the full year 2017 around 22mn USD, which represents 10% (!!!!!) of the NAV. If we compare this for instance to Vostok Emerging Finance which has the same size in NAV: Total operating cost was only 4 mn USD in 2017, i.e. 2% of NAV. Vostok New Ventures had 6,5 mn USD of expenses in 2017 which translates in less than 1% of NAV

So without further research I would recommend to stay away as far as possible from that one as this clearly seems to be a “fee self-service” vehicle for management.

Firsthand Technology Value Fund (SVVC)

At first sight, SVVC looks equally unattractive than GSVC. Anemic performance over the last 7 years. However, they do not employ leverage and charge less fees (6 mn USD based on ~180 mn USD). However their main problem seems to be that over time, they didn’t manage to generate any significant gains in their portfolio.

They also seemed to have invested to a large extent in public companies in the past where in my opinion their fee structure (2/20) soesna#t make a lot of sense.

So again, despite a “discount to NAV” I would stay away from this one as they haven’t proven to be able to generate any value over time.

Summary:

Although the analysis hasn’t been very deep, I think especially the comparison with the American vehicles has shown some relevant aspects:

- Fees are an issue. Management fees, carried interest and other expenses can add up and eat up investment returns. In this regard the Vostok vehicles look a lot better than the other companies in this post, especially Vostok New Ventures. Kinnevik looks ok in this respect too. ~25 mn EUR of admin costs for a 9 bn EUR portfolio is around 0,3% p..a…..

- investment track record is important, especially over the past few years. Especially over the past few years, returns for the tech sector have been very good. A management team that doesn’t create performance in such an environment will have even more issues when the tide goes out. Without being able to prove it scientifically, I think that “alpha” in the VC area is more sustainable than in the equity

Besides Kinnevik, the only vehicles that look interesting are the Vostok companies. Personally I prefer Vostok New Ventures, despite the concentration on Avito. as the fee level is low and I like the broader philosophy very much.

I also had the chance to have some conversations with the management and I like their unpretentious style a lot

Therefore I will add a 1% position in Vostok New Ventures with the goal of adding to this over time, too.

In order to manage my risk, I will most likely reduce my direct “venture” investments to a certain extent, especially Cars.com but also possibly Fitbit.

{kind=link}

Thanks a lot for the article

There is one more VC fund that you have bot covered, Draper Esprit, they have some high profile European startups in the portfolio and share price have have recently dipped below NAV. Would love to get your take on them

Venture capital financing is the lifeblood of new business development. Very nice blog

I am surprised the share price is not moving much higher…now below 70 SEK…

VERY good news from Vostok;

https://www.finanzen.net/nachricht/aktien/vostok-new-ventures-sells-all-its-shares-in-avito-for-a-cash-consideration-of-usd-540-million-and-plans-to-distribute-approx-sek-25-per-sdr-to-its-shareholders-and-redeem-outstanding-bonds-7065767

Hm… I am also happy about that, because it shows the possibility to make money and the “real value” of Avito.

But I also would have liked to hold Avito for some time and let the company grow. I hope the discount to NAV will close now and I happy to see the new investment possibilities.

Is the share redemption program the most efficient way to distribute the cash (from a tax perspective)?

As mentioned in the FitBit comments, I “swapped” my Fitbit shares for Vostok at 66 SEK/share. Size now 2% of portfolio.

I don’t think that it is appropriate to compare Naspers and Vostok. The discount to NAV of Naspers is justified for two reasons. First, their Tencent stake is worth over $100 Bn. and Tencent is already a listed company. As a consequence, it’s extremely difficult to liquidate this position without influencing the price of Tencent. Contrary to that, the complete portfolio of Vostok is worth around $900 million and none of the companies IPOed so far. Second, if Naspers sells their Tencent stake, it’s unclear how big the tax burden will be (it won’t be zero). However, Vostok is exempt from capital gains tax.

I did not say that one can compare the two but that Naspers is worth a look too, belongs to the topic and that I would love to hear his views.

According to South African law Naspers can sell down to 10% of their foreign holdings without paying capital gain taxes. In Tecent’s case that would mean another 22,2% without paying capital gain taxes. In addition to that they have, similar to Vostok, tax effiecient structures in place for all of their investments. Look at their latest earnings, they did not pay any capital gain tax for their 2% Tencent sale. So maybe it is zero or in the low single digit percentage range.

BB Biotech is maybe another name to consider in part 3. This name funnily trades at a premium to NAV at present, I think.

Thanks for the interesting blogpost. Did you have a look at Naspers? They own a lot of interesting staff beside their Tencent investment (their IRR ex Tencent if I have it right in my mind is 23% and accelerating and they trade around 30% under NAV). They were really cheap a few weeks ago with the drop in Tencent. If you like Vostok and are comfortable with Nasper’s large stake in Tencent you will probably like them too and I would love to hear your views.

Thanks for the article and welcome on board at Vostok New Ventures. You might want to take a look at the report I have written on the Investors day in Berlin: https://www.valuedach.de/en/2018/07/24/vostok-new-ventures-investors-day-2018/

I think Naspers and Rakuten are also potential options.

Love the write up on Vostok. Will give it another look for my PA