Update Handelsbanken – HOLD

Handelsbanken Update:

2018 was on the surface a solid year for Handelsbanken. According to the 2018 annual report, operating profit increased by +5% and net income by +8%, top line by +5%. ROE was 12,8% which is below my assumed 15% but still a remarkably good number for a large bank.

Just looking at the bottom line, the first quarter of Handelsbanken looks great: Net income up +19%, operating profit up +18%. However top line only grew at +4% (vs. Q1 2018).

However this is solely a function of the fact that the bank reversed their provision into the Oktogonen pension fund for employees which they clearly state in the quarterly report:

The Group’s operating profit increased by 18% to SEK 6,110m (5,161). The Board has assessed the financial performance of the Bank in 2018 and has decided that

there will be no provision to the Oktogonen profitsharing scheme for 2018. The previously recorded provision to the Oktogonen for 2018, SEK -827m, has

been reversed. Adjusted for this reversal, one-off effects and exchange rate effects, operating profit was more or less unchanged.

I found this an interesting move. Just as a reminder: The Oktogonen fund is basically the long term bonus pool for all employees which they can access once they retire. What this move means is that no employee from Handelsabnken got ANY bonus for 2018. This is a huge contrast compared for instance to Deutsche Bank which still lists 639 (!!!!) employees earning more than 1 mn EUR.

According to this Swedish article, employees were not happy. According to another article, cost increases seem to have been the main reason for this decision and in the first quarter no additional reserves have been made.

On the one hand this is really a tough decision as employees will obviously be pissed of, on the other hand, for me it shows the “outsider” character of the company which doesn’t seem to mind making hard decisions even before a really bad situation occurs

Performance:

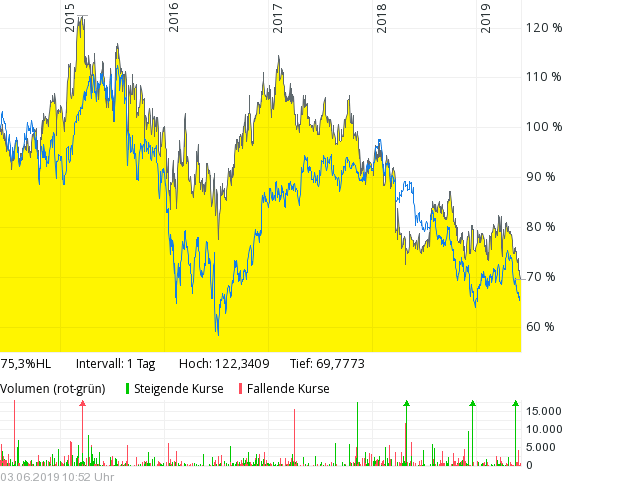

Performance so far: Since I bought Handelsbanken in January 2016, the performance was clearly underwhelming. Including dividends, the stock is more or less flat -0.75%) vs. +38% performance for the whole V&O portfolio. Part of that is a weaker Swedish Krona, which lost ~15% since I invested. Another issue is that profits didn’t develop as I expected. Net profit increased by 14% from 2015 to 2018, however not per annum as I assumed but in total. This resulted in a significant multiple reduction. When I bought Handelsbanken, P/B was around 2,1, in the meantime it is around 1.3. Trailing P/E is now ~10,5 compared to around 14 at the time of purchase.

In the underlying countries, UK, despite the issues is doing well as do the Netherlands and Denmark. Sweden is doing OK but especially Norway and Finland are struggling.

Interestinlgy, the stock did only a little better (in EUR) as the Stoxx banks over the last 5 years:

Digital disruption: Could Handelsbanke be the Costco of banking ?

Handelsbanken is clearly aware of the digital disruption happening but sticks to their now 50 year old business model of having independent branches but with digital access for clients. I have written on the blog a lot about the threats of new entrants in the banking market. Direct lending, mobile only, FX transfers, internet payment are only a fraction of areas where the “disruptors” already seem to have gained th upper hand.

Will this mean that all traditional banks will disappear ? This could be possible but for instance looking at the retail world, disruption clearls has it limits. Costco for instance is still going strong because they have a very differentiated business model.

Costco’s usccess would merit a whole blog post, but they are doing so many things differently which both, makes them hard to copy and allows them to be competitive despite the attack from Amazon. For instance, Costco only invests a relatively small amount into online and nevertheless sells more online than for instance Walmart. The “treasury hunt” business model really seems to work well even in the interent age.

So the question is: Could Handelbanken be the “Costco for Banking” ? I think there are certain similarities like the really distinct culture and business model. On the other hand, banking is a much more digital product than actual retail.

The short answer is: I don’t know, but I think there is a good probability that Handelsbanken can not only survive but at some point in time really gain market share again especially from other traditional banks that execute poorly.

The traditional players seem to hurt themselves wherever they can. For instance the recent huge money laundering scandal centered around Danse also involved Svedbank and Nordea, two big competitors of Handelsbanken. Clealry also Handelsbanken is not immune against these kind of issues but I think with a clearly lower probability due to its distinct culture and long term focus

Summary & what to do now ?

In summary, despite the disappointing stock price performance I will keep the Handelsbanken shares and if there is further weakness, I will increase the position from its currently low 2,2% weight to a “half position”.

As outlined above, I do think that its distinctive long term culture will make Handelsbanken a “survivor”. At the current valuation (P/B 1,3, P/E ~10) I think the stock is good value. In my opinion Handelsbanken is the best player in a troubled industry but with relatuvley good chances of a satisfying investment return over the next 3-5 years. At a current dividen yield of +6% and 4-5% growth p.a., my implied estimate

P,.S.: Please spare me comments with” but what about bank xyz which trades at 0.x of book value. In banking, in my opinion “quality” is even more relevant for the long term than elsewhere and Handelbanken is clearly the best quality bank in Europe.

Sold my Handelsbanken shares yesterday. More in a post soon.

Agree on the analysis/update. Also a shareholder since 2016. Q2 come flattish but mgt keep right course imho: „No provision was made to the Oktogonen profit-sharing scheme during the quarter (0)“

Take care

Any views on KBC as a high quality European bank?

What is your view on Credit loss levels in the UK? I think that is one of the largest worries for me. How to export a Swedish Credit culture to the bank branch managers that used to work at HSBC, Stan Chart etc. The amazing Credit loss track record in Sweden is kind of assumed will continue in UK, but the early signs we have so far, seems to speak differently. But I guess we will not know for sure before we went through a crisis..