All German Shares – Part 11 (Nr. 151-175)

And the next 25 stocks, this time with 5 candidates for the watch list. Enjoy !!!

151. Hesse Newmann AG

Troubled 4 mn EUR market cap asset manager fully depending on major share holder. “pass”.

152. Aareal Bank AG

1.8 bn market cap specialized Real estate lender. Significantly below book value of equity (2.8 bn) , however also after tax ROE is only around 5% and the core lending business is struggling, among others with exposure towards UK retail assets. The moste interesting part is subsidiary Aareon which is a consulting / software company offering real estate management solutions. Currently an activist hedge fund tries to push Aareal to sell/monetize this asset. Therefore a “watch” as special situation.

153. Easy Software AG

48 mn EUR market cap software/consulting company specializing in digital archiving and “content management”. Largest shareholder is Deutsche Balaton, a company that I generally try to stay away from when they are invested, The company had problems in the past and is among other things suing its former CEO. For me a “pass”.

154. Paragon GmbH & Co Kgaa

55 mn EUR market cap car supplier with an “Interesting” past. The company went bankrupt in 2009 but reemerged. The market cap is significantly below book value, but there are large intangibles on the balance sheet which might not be that valuable as the company is loss making. Additionally, there seem to have some significant accounting errors in the past. The stock used to be one of the top perfomers until end of 2017 but losz more than -90% since then. Paragon has a listed subsidiary called “Voltabox” which has a market cap of currently 115 mn EUR. The CEO and majority shareholder also seems to own other companies, among others an electric car manufacturer called Artega which is a client of Paragon/Voltabox. The CEO also seems to be a keen fan of driving car races. Although the stock might be worth a look from an educational point of view (long term performance of stocks run by a car racing CEO), for this purpose it is a strong “pass”.

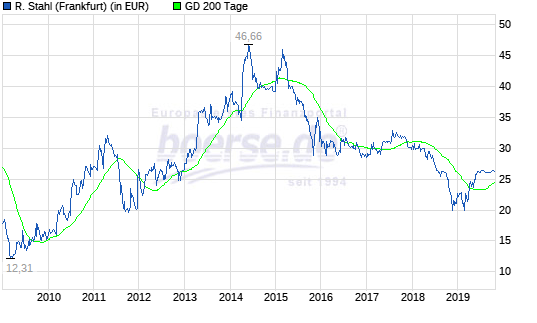

155. R. Stahl AG

R. Stahl AG is an “Old friend” of mine. I owned the stock in the past as a turn around speculation and even started a discussion threat in 2003 (!!!) on the stock in the German forum Wallstreet Online. These days, the 170 mn EUR market cap company is struggling. The company is manufacturing electrical equipment for “dangerous” environment such as the oil and gas industry. As the demand from this industry has weakened significantly over the years, the company has been struggling now for some time as the share price shows:

The spike in 2014 was driven by an (unfriendly) take over offer at EUR 50 that the CEO back then dismissed as “too low”. The CEO was subsequently removed but things went downhill from there.

R .Stahl has little direct debt and if they return to profitability at some time this could become interesting. A stock to “watch”.

156. WEBAC Holding

Tiny, 4 mn market cap company without real operating business. “pass”.

157. Westag & Getalit AG

140 mn market cap supplier to the construction sector. A stock that I actually owned but sold in 2012. Despite long running boom in German construction, stagnating top line and decreasing profits. The main shareholder sold out in 2018 at around 30 EUR/share. In theory there might be a squeeze out at some point in time but for me the stock is a “pass”.

158. Deutsche Forfait AG

19 mn EUR makret cap trade financing company Went insolvent but somehow reemerged with a strong stock price perfomance in 2019. Nevrtheless not interesting for me, “pass”

159. Primag AG

4.5 mn market cap residential real estate development company. Loss making for the last 2 years. “pass”.

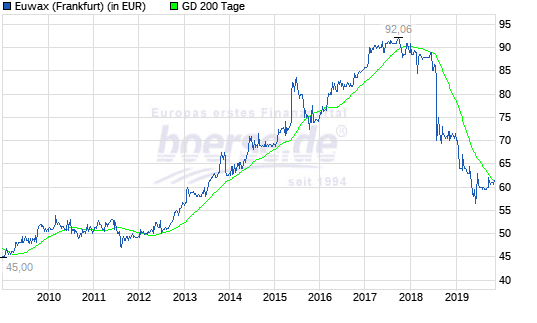

160. Euwax AG

Euwax is a 317 mn market cap trading/liquidity provider for The regional stock exchange in Stuttgart, I actually owned the stock a long time ago. The majority owner of Euwax is the regional stock exchange and in 2008, the Stuttgart stcok exchange implemented a “domination and profti transfer” agreement that allows the majority shareholder to claim all the profit in exchange for a guaranteed dividend. For a long time, the stock climbed steadily to a price of 90 EUR but then last year, for no obvious reason traded down to around 60 EUR per share.

With more than 3 EUR dividend per share, this looks like an interesting high yield bond, however the underlying business deteriorated and it is not guaranteed that the agreement will remain forever.

Nevertheless I will put the stock on “watch” as a special situation but with low priority.

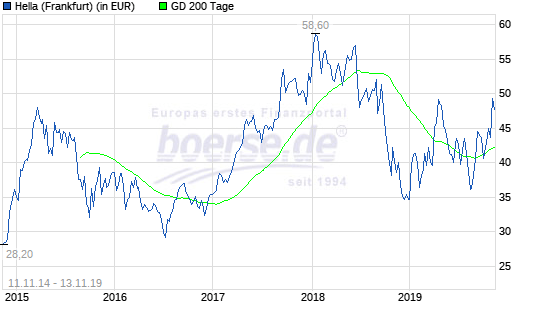

161. Hella Hueck KgaA

Hella Hueck Kgaa is a 5.4 bn market cap supplier to the automobile industry. The family controlled company went public in November 2014 but controls the company similar to Henkel wie a “KGaA” structur which is comparable to a GP/LP structure where public shareholders have only very limited governance rights.

As most of the other automobile sector companies, Hella shows currently declining revenues (-5% in the last quarter yoy) and even stronger declining profits (-20%).

What is interesting though are the still Ok margins (between 7-8% EBIT margin) and an ROE >20% despite limited net debt.

Hella seems to concentrate on technologically advanced components with the focus on lighting solutions but also offer systems for battery power mangament. So my first assessment would be that they are less impacted from a switch to electrical cars. The stock price reflects this to a certain extent as the stock performed better than many of its peers:

The Hella stock is not super cheap and the KgaA structure is not my first preference, however the company looks like a quality company and will go onto my “watch” list.

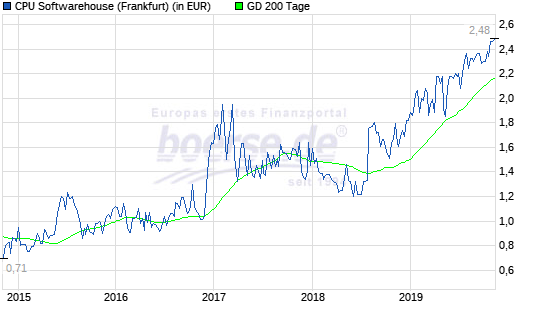

162. CPU Softwarehouse AG

10 mn EUR market cap Consulting / software company specializing in banking projects. One of the big stars of the “Neuer Markt” in the late 90ties / early 2000s, the comapny almost wnet under but somehow recovered over the past few years:

The company recnetly published a 4x increase in profits for the first 6 months, although oublishing 6 months result in November as such is not a sign of a good company. As the topline also has been shrinking in 2018 and I am in general not a fan of small IT consulting companies, I will “pass” on this one.

163. Vivanco AG

Vivanco is a 18.5 mn EUR market cap distributor of electronics supply. The bsuiness in 2019 seems to be in delcine and I see no points that make this one interesting. Plus it seems that the main shareholder is now a Chinese investor. “pass”

164. Shareholder Value Beteiligungs AG

Shareholder Value AG is a very unique stock. The compan is run by Frank Fischer, a well respected German Value investor who, among others is running the big Frankfurter Aktienfonds für Stiftungen and he is clearly one of the most known German “value investors”. Despite a week performance in 2019, his long term track record is really good. The listed company is a actually a kind of closed end fund mirroring the other portfolios.

Especially the presentations for the annual shareholder meeting gives a nice overview over the past track record and the current portfolio.

Currently, the stock seems to trade at a certain discount to NAV (105 EUR NAV vs. ~92 EUR for the share), but management fees and a “carry” structure justify this to a large extent.

For me a “pass” although I recommend to read the reports.

165. DIC Asset AG

945 mn EUR market cap commerical real estate company. Company reports an NAV of around 16,33 EUR/share compared to a share price of 13 EUR. However, as a non-expert in real estate and my dislike for non-REIT structures, DIC Asset is a “pass”.

166. StarDSL AG

0,23 mn EUR nanocap. “pass”.

167. SFC Energy AG

“Clean energy” company woth a 104 mn EUR market cap. The company manufacturs pertable fuel cells. In the first 6M 2019, business has stagnated and losses increased. In November, they cancelled their 2019 target. The business looks quite unpredictable and relying on large orders. “pass”.

168. Hamborner REIT AG

Hamborner is a 765 mn EUR market cap German Commercial real estate REIT. Other than the many non-REIT companies, Hamborner has limited possibilities to leverage up and therfore only grows slowly. The NAV is 10,8 at market values vs. ~9,60 for the shares. If I would need to construct a dividend portfolio, Hamborner would be a good choice. However, as I do not require dividend income, the stock is a “Pass”.

169. First Sensor AG

First Sensor AG is as the name says, a 359 mn EUR company specializing in sensors. The company is growing with single digit % and has Ok EBIT margins at currently 8%. SO why ist this company trading >40x Earnings ? The reason is most likely a take over of the majority by US based TE Communications this summer at a stock price of around 29 EUR. Investors seem to speculate on some sort of squeeze out. The company seems to be involved in the autonomous driving space, so there might be a bright future.

For the time being I put them on “watch” as a potential special situation.

170. Ecotel AG

23 mn market cap telecom company, IPOed in 2006 at 17 EUR per share, but never reached that value again. Shrinking top line, almost non-existent EBIT margin. Managment celebrates increasing gross results and EBITDA which are driven by IFRS changes. As a special effect. more than 100% of the result is attributed to minorities. “pass”.

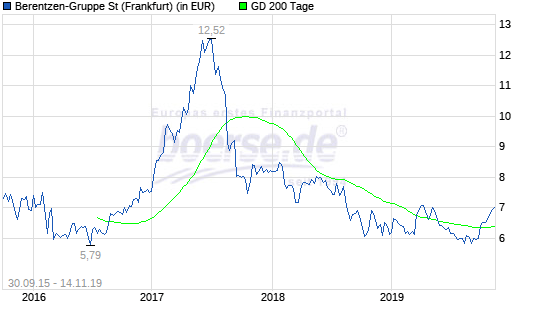

171. Berentzen Gruppe

Berentzen is a 67 mn EUR market cap beverage company, famous for its apple based “Schnaps”. For a couple of years, Berentzen was owned by infamous Aurelius and now seems to be without majority shareholder. According to their last report they seem to have diversified into non-alcoholic beverages which now account for 50% of their sales. The non-alcohol part is growing, alcohol is shrinking. The stock price is quite volatile:

A candidate for my “watch” list, although the balance sheet looks a little bit strange with a high liability for alcohol taxes.

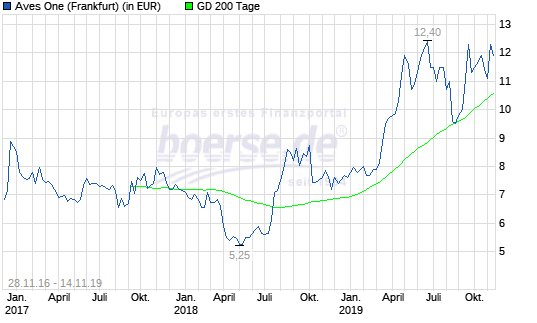

172. Aves One

Aves One is a 158 mn EUR market cap company that I have never heard of. It seems to be a commercial real estate company focusing on logistics assets, mostly rolling stock and container assets. The company has an “interesting” business model: 34 mn equity back 900 mn debt. With ultra low interest rates, this has worked so far quite well:

However such a leveraged business model is not something I want to own as a lot of things can suddenly go wrong (i.e. refinancing). So a clear “pass”.

173. Vapiano AG

Vapiona is a 110 mn EUR market cap restaurant chain. The company IPOed in June 2017 at 23 EUR/per stock but pretty soon ran into troubles. Managment changes and losses are piling up. In their 6m report, the loss increased to -35 mn and equity more or less disappeared. Debt incl. capitalised leases is >500 mn and >20 x EBITDA which is not sustainable. Personally, i never liked the concept anyway. “pass”

174. Deutsche Rohstoff AG

71 mn EUR market cap Oil & Gas company that runs some smaller explorations in Germany and has some producing assets in North America. Company has a lot of leverage. Not really my area of expertise and it looks like a “story stock”. “pass”.

175. Gateway Real Estate Ag

Another listed Real Estate company with a market cap of 721 mn EUR. Gateway seems to be a developer which has been growing quckly and has been raising capital recently. Not sure how a 220 mn equiyt “new” real estate company can be worth 720 mn. Clearly one sign of the current easy money policy. Fro me a clear “pass”.

Ok, thanks. I didn’t look so deep into the P&L during this exercise.

Hella’s margins and returns go down quite a bit if you adjust for their ample cost capitalizations. Then it looks more like an average automotive supplier (at least to me).