Metro Bank Plc – Terminal decline or Deep Value opportunity ?

Warning: This is not investment advice. The author recently had a very disappointing track record so you might want to stay away as far as possible from this stock. DO YOUR OWN research.

Some three and a half year ago I briefly looked at Metro Bank, then the much hyped “Apple of Banking” and I didn’t like it that much. My summary back then was as follows:

Fundamentally, I do think that at the current share prIce the stock is already very “richly” valued as I don’t see a sustainable business model to earn the required returns on equity in the long run.I see a large risk that Metro Bank is rather a “one-trick pony” which worked well once but most likely not a second time.

At some point in time in the future this could even turn out to be an interesting short opportunity when growth is slowing and defaults start catching up.

In the meantime a couple of things happened:

- the bank got into issues with the regulator because of miss clasifying risk assets (to their advantage of course)

- they were forced to raise capital in 2018 and 2019

- Founder / Chairman Vernon Hill (plus spouse and dog) left as well as the CEO Craig Donaldson

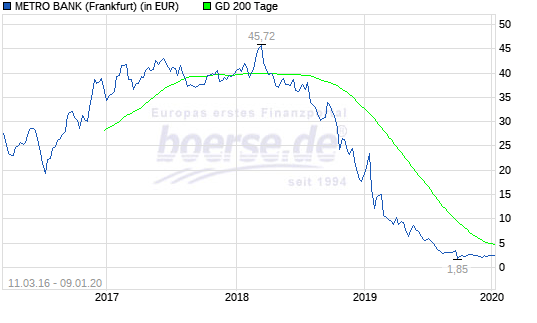

- The stock price dropped more than -90% since then (and I missed the short opportunity….)

- some bond issues flopped, they had to pay 9,5% coupon on a subordinated bond issue

- A new CEO has been appointed who has significant banking restructuring expertise

- Surprisingly they are still able to add a sizable amount of new customers every quarter

A few days ago, I was quite surprised that Ennismore disclosed that they have added a small (1%) position in their December monthly report (it is worth mentioning that Ennismore’s Net long position is very small these days…)

Their case is quite simple: At the current valuation of ~360 mn GBP and shareholder equity of around 1,7 bn, they assume that even a direct run-off of the business would lead to a 100% gain return on investment which I find is entirely plausible.

Of course there are a lot of risks/negatives regarding Metro Bank, among others:

- maybe the miss-classifcation is not the only “corpse in the basement” of the old management

- Brexit exposure (small business loans)

- their leases could be under water which would lead to losses in a run-off

- Reputational damage might not be easy to repair (not relevant in run off)

- Commercial deposits have been shrinking quickly over the last few months

- increased financing costs which led to a loss in Q3

- increasing competition from Fintechs on the SEM lending space

- potentially further decrease in interest rates

- “kitchen sink” approach of the new CEO

- etc etc

On the other hand, I do think there are less “unknown unknowns” than for instance with the likes of RBS or Deutsche Bank because Metro ran a pretty simple business model and the bank should actually be not that difficult to run off compared to banks with toxic long term derivatives books etc.

I assume that specialist players like Apollo or Cerberus might be already circling, theoretically this could also be an interesting target for Fintechs like Monzo or Revolut. On a side note: The business models of the UK challenger banks are quite shaky, nevertheless they are “priced” at insane valuations which makes their stock to an interesting acquisition currency.

Amazon for instance is a good example that successful online businesses at some point in time add retail locations and Metro Bank would fit to any of the new online challengers in my opinion. Most recently, a Colombian billionaire has been building up a stakein Metro Bank.

Summary/Risk management:

There is clearly a risk that Metro Bank never recovers and is on the way to terminal decline. On the other hand, I do think that there is a decent chance of either a take over or an attempt to actively run off the bank with a result that is significantly higher than the current valuation.

Like my Uber position, I am aware that this is a very risky bet, but I still think that the risk/return doesn’t look too bad. I’ll therefore allocate 2,0% position of the portfolio into Metro Bank at ~2,01 GBP/share. Similar to the Ennismore guys, I would hope for a 50% upside with a time horizon of max 12 months. If the stock drops below 1,50 GBP, I will be selling.

Somehow I forgot about my stop-loss. Grrrrr

Via Ennismore: „2020 could have a deteriorating profit situation due to the impact of debt issuance this year“ => But isn’t this is a long term issue with a 9.5% coupon on a 350MM relative to the income generation? The bond only get callable in 2024 so would need to LME if they want to get rid of it. By the way, these are senior not subs.

Omnicon, technically the 9.5% is an MREL bond which is loss absorbing and economically subordinated to “true” seniors. And remember: this is Not a long term bet for me.

https://www.metrobankonline.co.uk/investor-relations/shareholder-information/shareholder-information/share-price-chart/

value and opportunity ezt írta (időpont: 2020. jan. 15., Sze, 7:32):

> memyselfandi007 posted: „Warning: This is not investment advice. The > author recently had a very disappointing track record so you might want to > stay away as far as possible from this stock. DO YOUR OWN research. Some > three and a half year ago I briefly looked at Metro Bank, then “ >

Well, not sure if that disclaimer is cynisism or frustration, but I personally am grateful for your blog (Uber !) and the ideas that come up. Took a small position in Metrobank right after this post: experience tells me that for a frustrated or angry investor to take up a new position, he usually is extra careful (or mad…). I haven’t done any homework, but I trust you have. Some aggressive buying in the Draegerwerk genuessschein today btw, announcement coming up ? Keep it up !

Eddie, i am neither angry nor frustrated. So no reason to buy this stock….

Haha, great disclaimer

Omg ! Unprecedented !!! German sense of humor !!! Like it !! ❤ 🙂

Loved the disclaimer as well 😀

(at least my disclaimer has the same colour 😉 )