All German Shares Part 25 (Nr. 526-550)

Another batch of 25 randomly selected German stocks. This time with some quite interesting or even strange underlying businesses. Five candidates are worth “watching”.

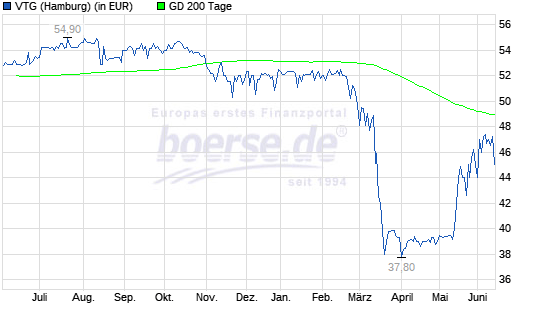

526. VTG AG

VTG is a 1.1 bn market cap company that is renting out/ leasing railway cars and was taken over by a Morgan Stanley infrastructure fund in 2018 at 53 EUR/share. The company has been de-listed and is trading only on the “Pink sheets”. Interestingly the stock price suffered after the crisis but has recovered in the past weeks as well:

2019 seems to have been a real great year for VTG. Despite their “Pink sheets” status, I’ll put them on “Watch”.

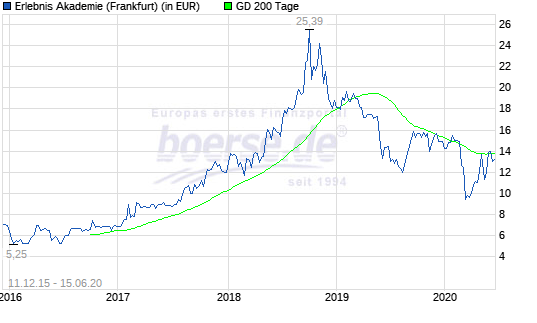

527. Erlebnis Akademie AG

Erlebnis Akademie is a 29 mn EUR company that I have never heard of. The company IPO ed in 2015 and runs recreational facilities that allow walking through and in tree tops (!!!). The company is expanding internationally.

The company is a growth company. They doubled sales from 2015 to 2018, 2019 only saw a small increase, however they planned to create new parks globally. The stock was hit hard by Corona but had declined already before after a big hype:

Covid-19 will of course hit them, but I think they could recover much faster than other tourist destinations as their concept doesn’t rely on packing tourists into one spot and the German locations for instance could benefit from ravel restrictions to foreign countries. In the recent weeks, the share price almost recovered to pre-crisis levels, maybe on expectations that “Local” attractions will recover better and faster,

A stock I will “watch” and revisit hopefully soon.

528. Coreo AG

Coreo AG is a 19.7 mn EUR market cap company that is active in ….Real Estate and used to be called “Nanostart AG” before the current change in business. The stock price indicates that they might not be so successful. “Pass”.

529. BHB Brauholding Bayern-Mitte AG

BHB is a 10 mn regional brewery in Bavaria specializing in the popular “Weizenbier” with the local brand Herrnbräu. The company looks very solid with little debt, but as many breweries, the business is capital intensiv and ROE/ROCEs are tiny.

If I would have more time, it would be a nice “hobby” stock, but I’ll “pass”.

530. GBS Software AG

GBS Software is a 4 mn EUR market cap company where I couldn’t actually find the home page or any financial reports. “Pass”.

531. Noratis AG

Noratis is a 69 mn residential real estate company. At first sight it looks as uninteresting as all the other “Newish” real estate companies. “Pass”.

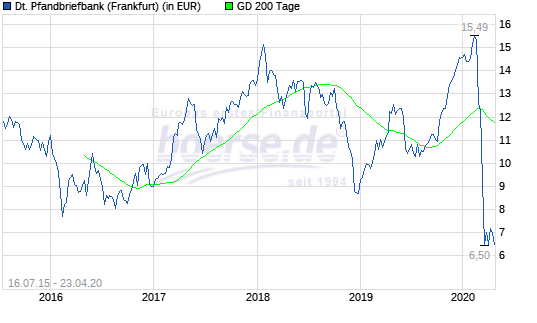

532. Deutsche Pfandbriefbank AG

A looong time ago (2015-2017) I owned this Real Estate financing specialist bank as a “forced IPO” situation. DPB got hit hard by the Corona crisis as the chart shows and now is valued at 930 mn EUR:

The company trades at 7x PE and and at around 1/3 of tangible equity. However 2019 profit is lower than 2016 where I was a shareholder despite the German real estate boom,. The Corona crisis will make things tough, especially with interest rates being lower than ever and crowding out by Government backed loans. It could be interesting for a deep value play but nothing that I would want to do at the moment. “pass”.

533. Mühl Product and Service

Once a “Neue Markt” high flyer, now a 2 mn market cap insolvent Zombie. “pass”.

534. Tiscon AG

0.2 mn market cap Zombie. “Pass”.

535. Sunline AG

0.1 mn market cap Zombie. “Pass”.

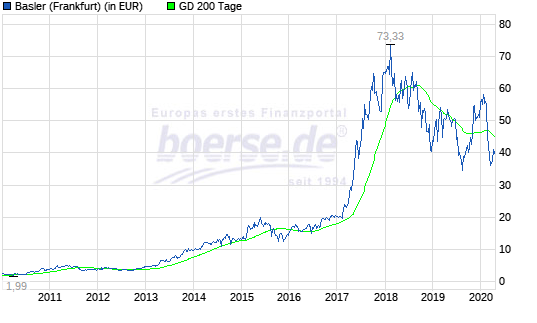

536. Basler AG

Basler is a 441 mn ER market cap company that specializes in optical inspection/digital camera systems, somehow similar as Isar Vision. As the company has mostly the automobile sector as its clients, organic sales have stagnated and operating profits are shrinking. Basler is still relatively profitabel compared to other automobile suppliers with 10% EBIT margins and 14% ROCE in 2019. The stock price has dropped ~-40% from its peak in 2018:

The company is majority owned by the founding Basler family and has net cash, however they sold a significant portion of treasury shares recently to bolster their cash reserves. However a P/E of 34 looks quite expensive for a stagnating business but maybe the underlying technology is worth it ? As I cannot judge this, it is a “pass” for me.

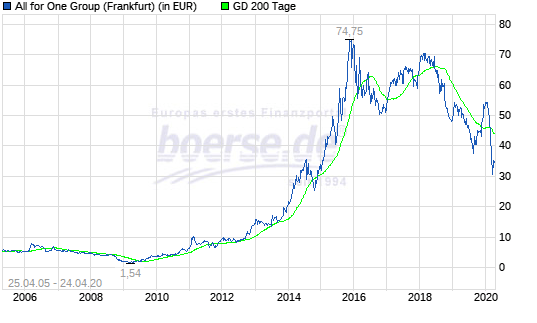

537. All for one Steeb

Despite having a curious name “All for one Steeb” is a 174 mn EUR market cap IT consulting company. The stock chart is quite interesting:

After achieving a 50-bagger from 2009 to End of 2015, the stock retreated since then before getting hit hard by the crisis. The company used to be a SAP-centric consultant but seems to have expanded into Microsoft and IBM products as well. Top line is still increasing nicely, but profits are stagnating since 2015 which explains the share price. The company is conservatively financed. 50% of the shares are held by a listed Austrian company called Unternehmens Invest AG, only 4% seems to be owned by management.

Anyway, I think this is one of the more interesting IT service / consulting companies. “Watch”.

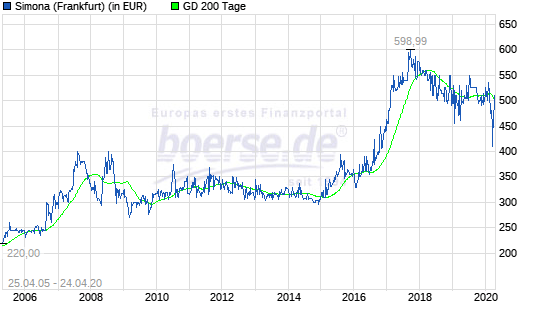

538. Simona AG

Simona AG is a 276 mn EUR market cap company that is very boring and under the radar, but also very steady. The stock price looks rather like a bond price:

The company produces all kind of plastics products (pipes etc.). The company seems to have grown in 2019 so far but profitability is not following. The company has net cash but a significant pension deficit. However a low oil price might be beneficial. Overall a candidate to “watch”.

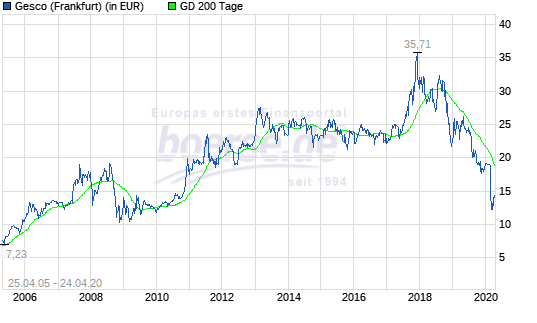

539. GESCO AG

GESCO is one of the older and more established “Mittelstandsholdings” in Germany. They try to position themselves as a long term investor compared to more “buy and sell” PE companies. The company has a 159 mn EUR market cap but clearly has seen better days and trades now near the level during the GFC:

Gesco has new management since 2018. The portfolio consist to a large extent of traditional metal working businesses which clearly are in a challenging situation, but personally I like the way GESCO thinks and presents itself. The company doesn’t have a dominating shareholder and looks quite cheap. Therefore I put them on “watch”.

540. NeXR Technologies AG

NeXR is the old “Staramba AG” which created a quite entertaining scandal with regard to faked sales etc. As mentioned already a fe times, the involvement of Mr. Elgeti as majority shareholder doesn’t really help either. Not clear why this pile of crap is valued at 12 mn EUR. “Pass”.

541. m+s Electronic

Insolvent zombie. “pass”.

542. Philion AG

A reverse IPO with 5 mn EUR market cap. I do not fully understand what they do, it has something to do with Telecommunication. “pass”.

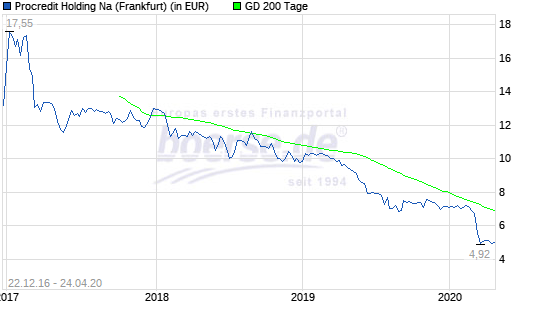

543. Pro-Credit Holding AG

ProCredit is a 300 mn EUR market cap bank holding company that I have never heard of before. The company seems to have been gone public in 2016 but did not place any shares. The did a capital increase in 2018. They seem to be active mostly in the Balkans and Eastern Europe, but strangely also in Ecuador. Looking at the stock price, they don’t seem to be too successful, the stock only went down after the first listing:

This is an odd bank. The do have a large deposit overhang in Germany and are active in super high risk countries like Albania, Kosovo and Ecuador. ROE is only at around 7% which for such a risky set up is not enough. With such a setup, it will be also super difficult for any auditor to find out how the quality of the loan book looks like. Not sure who wants to be invested in something like this. “Pass”.

544. Consus Real Estate AG

Consus is a 680 mn EUR property development company that seems to consider a merger with ADO, another listed RE company. Not my area of interest, “pass”.

545. Berchtesgadener Bergbahn Aktiengesellschaft

Berchtesgadener is a 12 mn EUR market cap company that operates mountain cable cars in the beautiful Berchtesgaden area. The stock is rarely traded and infomration is hard to get. Interesting for hobbyists but nor for me. “pass”.

546. Bitcoin Group SE

As the name says, the company operates in the crypto currency space. The company operates a market place that generated around 2 mn in sales in the first 6M 2019. They also hold themselves some crypto currency. Nevertheless, the company is valued at an astonishing 118 mn EUR. “Pass”.

547. Kremlin AG

Zombie stock, victmit of the “Reich Familie”, “pass”.

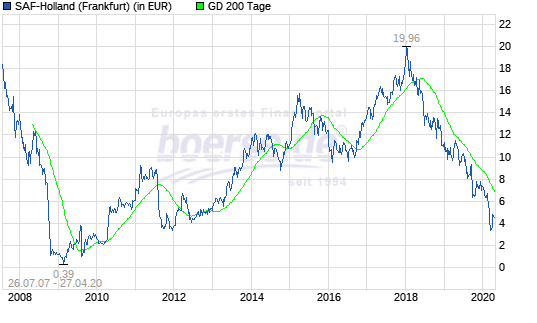

548. SAF Holland AG

SAF Holland is a 208 mn EUR market cap supplier to the truck industry. The company has an interesting past. They went public in July 2007, were almost bankrupt in 2009 but then took of like a rocket, before coming down from space since end of 2018:

Business at SAF has been in decline already in 2019 and margins have become thin but they were still profitable. The company does have debt and I am not sure if they are a company that will survive. Therefore “pass“.

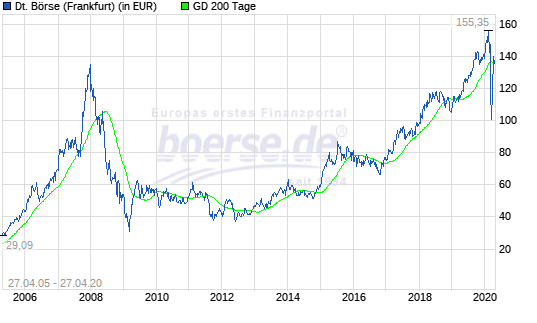

549. Deutsche Börse AG

Deutsche Börse is the operator of the German Stock exchanges valued at 26.6 bn EUR. That running a stock exchange is good business is not a secret, that’s why Dt. Börse is valued at around 26x trailing earnings and ~8x sales.

The big profit centers however is the Derivative Exchange Eurex and the deposit business Clearstream who account for 2/3 of the operating profit. They managed managed to increase top line by ~7% and bottom line by +20%.

The company made some headlines in the past about the failed merger attempt with LSE and insider issues with the former CEO.

The stock price has dropped a lot less in this crisis than in the GFC:

The stock price is pretty much there where it was in the beginning of 2020. Dt. Boerse is clearly a very good business but clearly there is no bargain to be found her. “pass”.

550. Decheng Technology AG

A late comer to the Chines-German fraud wave that IPOed in late 2016 but went pretty straight to zero afterwards. Pass.

Hi, very interesting summary.

On ProCredit, I came across them in Georgia, because I IPO’ed Bank of Georgia on the London Stock Exchange 10 years ago. ProCredit with a social mission, I got the impression that their RoE was so low, because they are often lending money to people who are not going to be profitable enough for the banks. An interesting comparison might be with International Personal Finance (IPF) which is listed in London. These shares haven’t done well, because they get into regulatory problems lending at high interest rates to people the banks prefer to avoid.

Whereabouts do you live in Germany? If you’re in Berlin and would like to meet up let me know.

Great site/write-up.

What do you as a data source for German share prices?

Thanks

Hi, thanks for sharing this work!

Re. Erlebnis Akademie:

Interesting article 2 months ago in the magazine Brand Eins:

https://www.brandeins.de/magazine/brand-eins-wirtschaftsmagazin/2020/investieren/wipfelstuermer

#543 Pro Credit: war bei denen mal zum Vorstellungsgespräch. Kleines setup. Vermeiden (angeblich) jeglichen Kontakt zu Politisch exponierten Personen.

Great run-through, will you do an Austrian and Swiss series as well? Thank you

Not Sure about that. Most likely not…