Summertime is always a good time to look at stocks which are to a certain amount “strange”. I started this mini series last year with the two listed National banks of Switzerland and Belgium.

In this second part, I want to look at the Company called “East Asiatic Co Ltd.”, incorporated and listed in Denmark.

Why is this stock strange ? Well, first, for a company called “East Asiatic”, Denmark is not the most natural site to be located. Secondly, the description in Bloomberg is the following:

East Asiatic Company Ltd. A/S processes food and offers moving services. The Company raises and slaughters animals and processes meat in Venezuela; and provides relocation and records management services to corporate and individual clients in Asia.

So Venezuela is not directly in East Asia. According to this website, the name is only related to the historic business of the company:

East Asiatic Company (Ostasiatiske Kompagni, Aktieselskabet Det.), Copenhagen, Denmark. Formed 1897 by Capt. H. N. Andersen and associates. Operated between Denmark and the Far East, trading in rice, oilseed, timber and spices. Operated first commercial ocean-going diesel ship (Selandia (1912)) after which routes expanded to include South Africa, the West Indies, North America and Australia. Survived WWII with a depleted fleet but retained their rank amongst the worlds leading ship operators. Largely divested itself of shipping interests between 1994 and 1997 and diversified into other areas.

So let’s directly look on EACs website to find out what exactly they are doing today.

Subsidiary Santa Fa

If one looks up Santa Fe’s website, this looks like a potentially interesting global business services company. They seem to offer everything, from Visa, moving furniture and finding real estate.

According to EAC’s 2012 annual report, two subsidiaries of Santa Fe (Wridgways, Interdean) were bought in 2010/2011. Overall, Santa Fe made up 31% of EAC’s total sales.

EAC’s annual report by the way is very good. On page 19, they explain Santa Fe’s business model clearly, which looks attractive in a globalized world.

Business is growing strongly, but margins have been reduced, specifically as they feel already the slump in Australian mining activity.

Simple valuation of Santa Fe:

Plan: 5% CAGR until 2016, 300 mn EBITDA. EV/EBITDA of 6-8x realistic ?

Current borrowings 500 mn, growth by 5% in line with sales –> 600 mn debt in 2016

EV of 1.800 -2.400 –> equity value of 1.200 -1.800 in 2016. Discount by 15% for 3 years: NPV of Santa Fee according to this: 790 – 1.180 mn DKK

just for comparison reasons: Current market Cap EAC in total: 1.120 mn DKK

Plumrose:

No comes the fun part. Subsidiary Plumrose ist he leading pork producer in Venezuela, Cranswick of Venezuela so to say. However, other than Cranswick, Plumrose owns the complete vertical value chain. They are growing their animal feed, raising pigs, slaughtering, processing and distribution incl. branded food items.

As we all know, Venezuela has problems and doing business there is at least “challenging”. Among the problems specifically concerning Plumrose are restrictions of money transfers outside Venezuela and Hyperinflation.

Restriction on money transfers

According to the annual report, Venezuelan authorities did not allow to transfer dividends to EAc since 2007. Only one special dividend of 68 mn DNK was allowed in 2012. In parallel, EAC seems also to charge royalties to Plumrose, but again those royalties cannot be paid out.

The theoretical amount of those outstanding amount would be around 60 mn USD at current Bolivar exchange rates.

Inflation /Hyperinflation

Reading the annual report is also an interesting lesson in inflation and IFRS Inflation Accounting I didn’t know for instance that there is a separate IFRS article (IFRS 29) dealing with hyperinflation.

The big issue here in my opinion is the following: In a Hyperinflationary context, one usually is confronted with “official” fixed exchange rate which are subject to transfer restrictions and a black market rate which is usually a lot lower.

In Venezuela, the government devalued th Bolivar in February this year significantly by almost 50% from 4.3 USD/Bolivar to 6.3. Nevertheless, this is far away from the “black market” rate. currently, according to some sources, the “black” rate is around 32 Bolivar per USD, only a fraction of the official price.

Often, the black market rates are maybe too cheap because of the risk involved with “semi legal” transactions, but clearly, the official rate is far off the mark.

So if we look into the 2012 annual report of EAC, we can see that Plumrose is responsible for almost 80% of EAC’s profit as reported with an exchange rate of 4.3. If we look into Q3, we can see that Plumrose at 6.3 Bolivars er USD is responsible for almost all of EACs profits.

No, using the black market exchange rate, one should actually divided those numbers by 4 or 5 to come to a realistic representation. If one does so, then the currently cheap valuation of EAc (P/B 0.46, P/E 7 for 2012) suddenly look at lot different. Calculation with 30 Bolivar per USD, EAc would not have made a profit in 2012 and P/B would be around 1.

So this is an important lesson here: For any company having significant exposures in a hyperinflationary environment, one should not look at the “officially translated” earnings but recalculate at more realistic black market rates.

Other observations:

The company itself seems to be very shareholder friendly. Clearly, many investors would like the Santa Fe business but less the Venezuelan operations. On their website they state the following:

EAC strategy towards 2016

The overriding aim of the EAC Group is in the course of the coming years to develop its two businesses, Santa Fe Group and Plumrose in Venezuela, into strong and independent businesses; each with a size and scale sufficient to attract international investors and to become independent, listed companies.

So this is quite unusual. Many companies just want to become as big as possible. Here, it looks like that they really want to maximise value. This could also be a spin off opportunity at some point in time

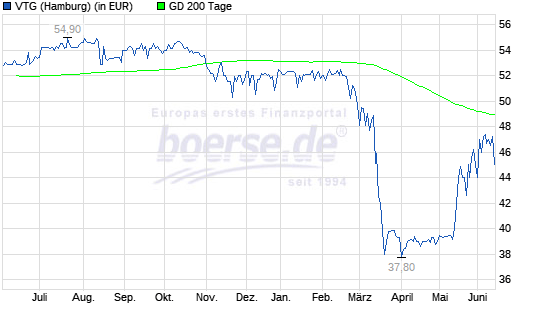

Stock price:

The stock price has seen better days:

So it looks like that there is not too much optimism priced in at the moment (or too much optimism in the past). The stock price most likely also reflects that Santa Fe is currently struggling due to the BRIC slow down.

Summary:

All in all, EAC is not only a “strange” stock but also an interesting stock. Although both subsidiaries are struggling, I see some “real option” value here. The Santa Fe business, if the execute as planned, is worth more or less the whole market cap at the moment. Therefore, Plumrose, the Venezuelan pork producer is like a “free” option betting on a better future for Venezuela. This future is highly uncertain, but some positive signs are also visible.

I do not know any other way to invest in Venezuela apart from Government bonds which have their own issues if one wants to bet on some kind of recovery like we have seen in neighbouring Colombia.

On the other hand, Santa Fe is definitely negatively impacted by the slow down in the BRIC and commodities world. So it will need sometime until this potential value could be unlocked.

For the time being, I will however NOT buy the stock but watch developments closely.If Santa Fe really recovers I will establish a position.

Nevertheles, keep in mind that this is not a typical “margin of safety” kind of stock. This is more like “ray Delio style risky but cheap “real option” investment with relatively uncorelated specific risks.