Alimentation Couche-Tard: Cheap Quality Compounder or Gasoline Dinosaur ?

Disclaimer: This is not investment advice. PLEASE DO YOU OWN RESEARCH !!!

Management Summary:

![]()

Alimentation Couche-Tard (“CT”) is one of the historically best performing Canadian companies, operating gas stations and convenience stores around the world with a focus on North America.

The company currently looks like a very interesting GARP (growth at a reasonable price) stock. Over the last 10 years, the company showed exceptionally good numbers: 23% EPS CAGR and 10 year average returns on capital >20% (23% ROE, ~20% ROCE). The business model is very resilient, Covid-19 actually led to an increase in margins and profits, both on the convenience store segment as well as in fuel despite declining sales.

Clearly the company has some issues such as the impact of EV charging on the fuel business and some question marks on their M&A strategy. However if one assumes that these are manageable risks for this well run company, the current valuation at around 13-14x 2020/2021 earnings allows an attractive entry into a great company at a very reasonable price.

The business

CT operates gas stations and convenience stores around the world. The original Canadian Business these days accounts for only around 20% of top line. 2/3 of the revenues are from the US, the rest is Europe plus a kind of franchise business in some other countries globally. The company has been founded in 1980 with a single Canadian convenience store and has been growing over many years mainly through acquisitions but also due to some organical growth by opening stores. For 2019/2020, 60% of the profit come from convenience stores, 40% are profits from fuel distribution.

My first encounter with regard to Convenience stores in the blog was via FEMSA, where their OXO chain was supposed to be the “crown jewel” of the portfolio but where I could not persuade myself to buy.

According to CT’s annual report, the sector, both in North America and Europe is in a consolidation phase with oil majors selling of their networks which will offer opportunities. In the past, CT bought significant assets from oil companies such as Statoil and Valero.

In general the business is a relatively “low margin” business, however, as similar retailers, the company has a “negative” working capital position, i.e. retail customers pay cash whereas the suppliers are getting paid later which creates very decent returns on capital despite the low margins..

Convenience stores are also less impacted by E-Commerce. You go to a convenience store either if you need to fill your tank or if you want to have a coffee and a quick pack of cigarettes, along with some potato chips and a six pack of beer. Maybe in super Urban areas you have some kind of rapid delivery, but on the country side the convenience stores are the best place to get all this. In addition, I think convenience sores are als less effected by “hard discounters” like Aldi, Lidl etc.

The barriers to entry are pretty high in order to establish a new “brand” of convenience stores, especially in connection with filling stations. It is clearly an economics of scale business. However, the assortments of convenience stores need to be adapted to local requirements.

Overall I would rate the business as attractive and defensive, especially if done right.

Company culture

CT stresses that they retain their entrepreneurial spirit and manage businesses on a decentralized basis. They have close to 30 business units which seems to be able to act relatively independent which is important for adapting to local markets. They also stress a cost focused strategy. Compared to Applegreen for instance, it becomes pretty clear that they “walk the talk” with a significant lower cost ratio for a very comparable business. They have a very good track record in integrating acquisitions and demonstrated that they can operate successfully internationally. From the outside, it looks that the company culture is clearly a plus.

CEO/Founder/Ownership

Alain Bouchard founded the company in 1980 and grew it form one station into an empire. He is now 71 years old but has already passed the reigns to an outside manager in 2014 but remains Executive Chairman.

Together with 3 co-founders, he controls around 23% of the shares, due to a split into A/B shares, however he controls ~67% of the votes. As a Chairman, he still receives a pretty decent salary (~6 mn CAD in 2020) but I guess he is still heavily involved in the company. The CEO Brian Hannasch is the top earner, netting a cool 12 mn CAD in 2020 including various bonuses. However, Hannasch owns a significant amount of CT stock (close to 30 mn CAD) and the bonus is to a large extent paid in equity. Alignment of management and shareholders seem to be pretty Ok on that basis.

There has been a book written about the Couche-Tard story that I read 3 or 4 years ago. Unfortunately it doesn’t seem widely available right now:

It portraits Bouchard as a super hard working, non-nonsense entrepreneur who had to overcome many difficulties to get where he is now. The only slightly negative aspect is the fact that Bouchar now is already 72 years old. I think he is still calling the shots with regard to big decisions. There are many examples of founders being able to run businesses at a far higher age, however there are also negative examples where founders lost their way. The fact that the successor CEO is already in place since more than 6 years is a good sign.

All in all, I would rate management & alignment of interest with shareholders as very high.

Antifragile business model / Covid-19 Windfall profits

Filling stations and convenience stores are supposed to be stable businesses, often this is even considered some kind of infrastructure asset. However during the pandemic, it turned out that the business is rather “antifragil”:

One one hand, the convenience stores saw a lot more traffic and business. On the other hand especially during the hard lock down, road transportation went down significantly but gross profit went up. My guess is that falling oil prices could be passed on to customers with a delay which more than compensated for lower activity. overall, the pandemic was good for business.Interestingly, in contrast to let’s say online furniture companies or home improvement stores, investors seem to ignore these windfall profits completely as Couche-Tard trades below beginning of 2020 levels, despite profits being up around +30% yoy. Clearly not all of this windfall profits will be recurring but it clearly shows the defensive qualities of the business.

Capital allocation / Acquisition strategy:

As (smart) acquisitions were of cornerstone of CT’s growth in the past, it makes sense to look at the biggest deals in the last 10 years: SFR (Statoil) in 2012 for 2.8 bn USD and CST (Valero) in 2017 for 4.4 bn USD. Both were typical deals, buying gas station networks from integrated oil companies, integrating them and then quickly bringing them up to CT standards. They mostly finance them with debt, but pay down debt quickly after the acquisitions (more on that later).

The full acquisition story is to be found on the company web site.

However the latest 3 acquisition attempts were not successful. In 2019, CT approached listed Australian company Caltex for a USD 5,6 bn take over but dropped it in April 2020. In August 2020, they lost out against Japanese 7-Eleven in the bid for Marathon Petroleum’ss US network of gas stations which was sold for a whopping 21 bn USD or 15x EV/EBITDA in cash. And just a few days ago, CT announced that they were in negotiation with French Carrefour only to be stopped by the French Government which was fearing for “French food security”.

Interestingly, CT’s share price dropped after the initial announcement and didn’t recover much after the the French Government stopped it. Somehow investors seem to have been spooked by the size of the transaction (16 bn EUR). Personally I found the attempt very interesting. Carrefour has indeed some issues and big box super markets would be a new format for CT, however Carrefour is also strong in Convenience stores and I am pretty sure that CT would have split up Carrefour and sold the Supermarkets of to someone else. The valuation of Carrefour is pretty cheap. Let’s see how the situation develops, maybe they can do a different deal with Carrefour at some point in time.

Clearly, the easy “roll up days” are over, as competition in this area for deals hits up. PE giant Blackstone recently announced the take private of Ireland’s version of CT, Applegreen and there is now even a SPAC with a smaller US convenience operator called Arko.

Although the Carrefour deal had a negative impact on the share price I do think it shows that CT is a shrewd capital allocator and doesn’t overpay. With their international footprint they clearly see a lot of opportunities and wait patiently until they have the right deal or they buy back stock.

The biggest issue: Electrical cars / Charging:

One big question is clearly: When EVs will take over sooner or later, what will happen to gasoline filling stations ? The current bubble/boom in EV stocks seems to indicate that by next year we will all drive electric. If we all drive electric, the question is: Will consumers only charge at home ? So far no one knows the answer.

Interestingly, via their subsidiary Circle K, they are the leading operator of charging stations in Norway which ist also by coincidence the leading global market in EVs (measured by relative share). Here is an interesting interview from 2020 the the GM of Circle K Norway. It’s interesting to see how they test various strategies, from cooperation with Tesla to home charging solutions for residential buildings.

In 2020, in Norway for the first time more EVs have been sold than cars with combustion engines. However even at the pace of Norway, it takes time to replace the overall fleet of existing cars. The average age of the car fleet in Germany is 9,6 years and this is one of the lowest in the Western world. So even with a 50% share of EVs in new car sales, it would take 20 years to fully replace the old fleet. And not every country has the financial resources of Scandinavian countries to support this with significant subsidies.

However there are indications in Scandinavia that many EV owners prefer to charge at home or at work which clearly works best if you own a house. What I do like is that they see this challenge also as an opportunity, as it can be seen in this investor presentation from 2019.

Overall, EVs and charging are clearly the major threat for the traditional fuel business but also a significant opportunity if done right.

Other topics: Tobacco / Cannabis /ESG aspects

When looking at the convenience store side it is important to understand that tobacco distribution is clearly a big part of the business and CT itself wants to be also a leader in Cannabis based products where it is legal. However, Cannabis is still not legal at a federal level in the US and Tobacco is in a structural decline.

As CT sells Tobacco and fossil fuels, It clearly will have issues to be included in many ESG based mandates. However I was surprised that its ESG scores aren’t that bad when I for instance tried the Arabesque Sray score also at Systainalytics the company scores “average”. Not great but also not a disaster.

Why is it “cheap” ?

As partially discussed above, I have identified these main points that could be responsible for the current low valuation:

- Shareholders are irritated by the perceived M&A strategy change after Carrefour, potential concern about growth opportunities

- EV charging is perceived as existential threat mid- to long term

- “Non ESG” characteristics (tobacco, gasoline)

- low dividend yield makes it uninteresting for yield oriented investors

- Age of Alain Bouchard

Looking at the share price (in EUR) it becomes clear that over the past few years, the stock has been stagnating after an epic 10x run from 2008-2015:

Financials/Valuation:

During the 10 years of my blog I haven’t covered a company with such good and consistent historical numbers. Here is a small snapshot of Growth and Profitability over the past 10 years:

| 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | ||

| Gross margin | 14.80% | 12.91% | 13.00% | 13.15% | 15.26% | 17.81% | 17.10% | 15.78% | 15.55% | 17.98% | |

| EBIT Margin | 2.71% | 2.51% | 2.37% | 2.72% | 3.82% | 4.89% | 4.48% | 3.97% | 4.21% | 5.84% | |

| ROE | 20.54% | 22.06% | 21.26% | 22.62% | 23.69% | 26.74% | 21.86% | 24.65% | 22.25% | 24.79% | |

| ROCE | 23.37% | 24.56% | 19.29% | 16.92% | 21.21% | 24.41% | 21.08% | 16.59% | 16.15% | 21.66% | |

|

Gross Margin growth

|

7.52% | 8.12% | 55.24% | 8.29% | 5.55% | 15.43% | 6.59% | 25.15% | 13.35% | 5.86% | |

| NI Growth | 81.77% | 24.12% | 25.11% | 41.71% | 14.53% | 28.39% | 1.17% | 38.49% | 9.62% | 28.35% | |

| EPS Growth | 22.50% | 27.04% | 22.89% | 40.20% | 13.99% | 28.83% | 0.95% | 39.15% | 9.83% | 29.01% |

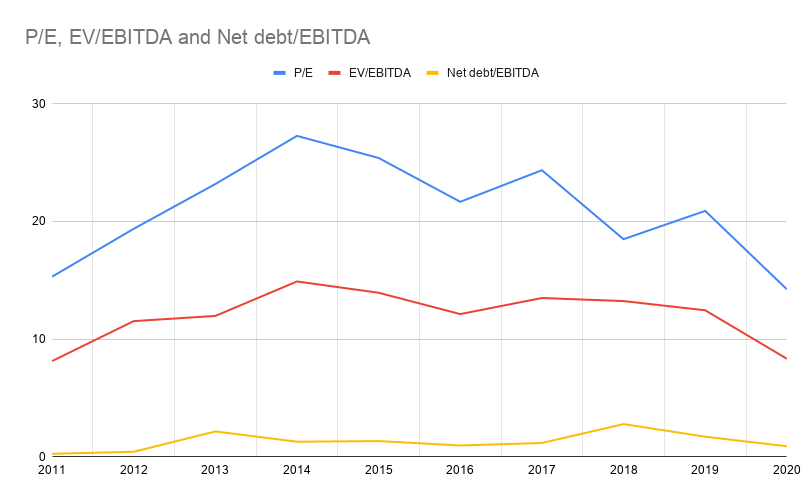

Here is another interesting chart:

This chart shows that since around 2015, valuation multiples have gone down significantly from a peak of ~28x P/E to the current level of around 13-14x P/E. And this despite a very conservative debt position with net debt to EBITDA significantly below 1 and increasing margins as shown above.

Of course, history might be not the best guide for the future, but to me it is pretty obvious that the current valuation does not include any growth expectations.

To be honest, I do think that the times of 20% p.a. earnings growth might be over despite their stated goal to “double the company in 5 years again”. But even if they manage only half of that, like 10% p.a. and I ignore the 2020/2021 positive outlier year, I would end up with ~3.4 USD earnings per share in 5 years. Assuming a “fair” P/E of 20 for a high quality company, this would lead to a target price of 68 USD or around ~86 CAD per share compared to the current 38 CAD.

Even if they don’t grow, they could buy back around 1/3 of all outstanding shares if they use their free cash flow for this purpose which would support EPS growth.

Game plan:

I do like the company a lot and have been watching them for 3-4 years now. I think the price is interesting but there are clearly some risks. therefore I’ll start with a 3% position which I was able to buy at around 37,5 CAD/share last week. Target holding period is 4-6 years with a target return of 100%. I’ll allocate this into my long term “bucket”.

As described above, a few things need to be watched. In the shorter term, one will need to see how they allocate all the free cash that is coming in. If they overpay for an acquisition or suddenly start to pay high dividends, then this would be a warning sign.

Over the next 2-3 years I will need to do some more research into the actual effect of EV charging on gas stations and related convenience store sales. My assumption is there won’t be much effect in the next 2-3 years, but I could be of course wrong. But clearly even the highest quality company is struggling if the wind blows hard in its face, as seen with Handelsbanken.

Disclaimer: This is not investment advice. PLEASE DO YOU OWN RESEARCH !!!

MMI! What a lovely lovely business! And it’s so good to have you back from start-up VC investing land! I was worried you were going to start doing crypto posts next, what a delight to see such a gorgeous value business. I also think this is the first time I’ve read something non-European here – definitely want to see more of that. Thanks!

Be careful, my non-European track record (Silver Chef, Cars.com) is not great….

The book is available as an ebook here: https://www.kobo.com/ebook/daring-to-succed

The book is available as a cheap ebook here: https://www.kobo.com/ch/en/ebook/daring-to-succed

I added a comment yesterday, but it appears not to have been posted. Apologies.

I would re-iterate what was always said:

(1) I too recently bought ATD shares,

(2) I was perhaps more “transparent” about their “drug biz” (tobacco, white nicotine, alcohol, lottery tix),

(3) Here in Texas it is common for people to start filling their cars (OK, trucks!) and go into the store. This behavior seems perfect for EVs with, say, at 20 minute charge cycle. If EVs are ubiquitous, distributed charging will be necessary.

(4) They seem to be disciplined buyers. I think the stock did not fully recover because they left the door open to a future deal for Carrefour.

Thanks…

Hi MMI,

did you bought class A or class B shares?

Class B.

I assume the profit comes less from selling gasoline than from selling all else, with the former being the reasons to stop (and shop for the latter).

From this perspective EV is certainly a threat.

But, could it be THE opportunity to sell more per client? w/o being anything close to an EV expert, what is charging your car takes a few minutes in x years and CT succeeds in making this ‘waiting time’ the perfect time for a coffee + snack, cigarettes and a good old newspaper, with higher high-margin sales per shopper?

Thanks for the write up… I also recently bot ATD for similar reasons. I would only emphasize that they do appear to be disciplined buyers… Part of the reason the stock didn’t fully recover might be that ATD left the door open to a future acquisition of Carrefour.

And I was maybe more explicit in my analysis of their “drug dealing” biz… White nicotine, alcohol, and lottery tix.

Not sure about EVs… Here in Texas, it is common for people to begin filling their gas tanks and go into the store for food, etc. Seems that behavior would be perfect for a 20 minute EV charge! Universal EVs is going to require charging stations, might as well shop, too…

Hong Kong stores are just quick pkg food and misc. Seems very durable…

For past acquisitions, each store spits off $200k and can be bot for $1m? Roughly correct?

Have you looked at Treasury Wine Estates?

Feel free to email me…

Very nice summary. Value seems to work in Canada. I just finished some interesting research that indicates Sweden of all places is a good hunting ground for value stocks (never would have thought that!) I’ve summarized it on my humble wordpress. Cheers