All Swiss Shares part 14 – Nr. 131-140

And on we go. Another 10 randomly selected Swiss shares. This time, three companies are going on to the extended watch list and one is actually a current holding of mine. As we are now already at around 2/3 of the Swiss Stock universe, I need to think about the next market to look at.

131. Perrot Duval AG

Perrot Duval is a 13 mn CHF micro cap. According to their latest annual report, the company is already 116 years old. The company seems to have sold its major operating business a year ago or so and now concentrates on the sector process automation, although I did not really understand what their remaining subsidiary called “Füll” really does.

What is kind of interesting is the fact that the company sits on 17 mn CHF of net cash and therefore the market seems to discount a lot. The CEO and Chairman owns 35% of the shares. In the mean time, the company seems to have made further acquisitions.

The stock could be interesting for some “deep value” investors who might also be able to talk with the CEO, however for me this is clearly “Too hard”, therfore I’ll pass.

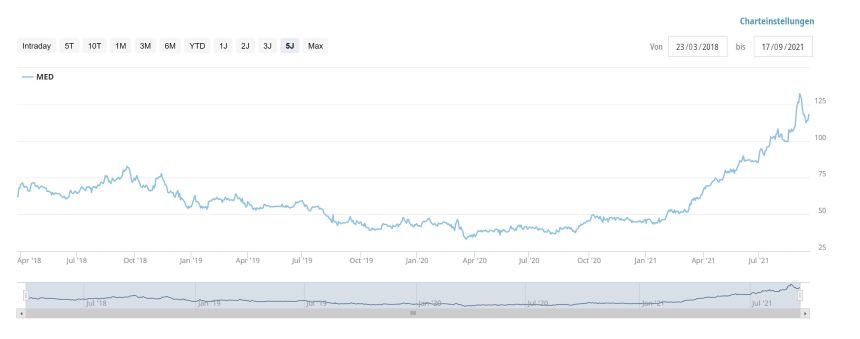

132. Medartis AG

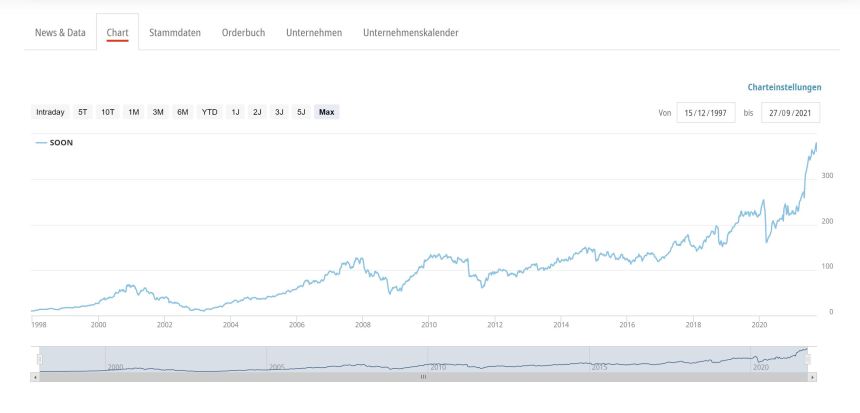

Medartis is a 1.4 bn CHF market cap “Medtech” company that specializes in implants and surgery technology, especially for foots, hand and face surgeries. The company was initially part of Straumann, but then separated. The company went public in March 2018 at 48 CHF per share.

Up until march this year, this looked like a typical “IPO dud” before the stock got a rocket boost and did around 3x in the last 6 Months:

According to their 6M report, the company is growing nicely at around 30% and margins are scaling up.

I found the company very interesting, but at 8-9 times 2021 revenue, the valuation looks quite rich after the run up in the share price. However I think 10xsales instead of 10x earnings is the new benchmark in this sector. I will definitely “watch” this one.

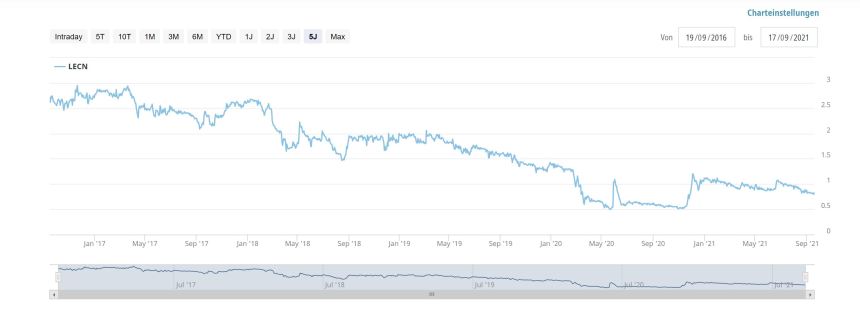

133. Leclanché SA

Leclanché is a 270 mn CHF market cap “penny stock”. The company tries to sell itself as a 111 year old startup and is active in “etransport” and energy storage, which i find very interesting at first glance. In essence they seem to be focusing on developing batteries for different use cases such as marine transport, trucks and sationary strorage.

However the startup reference means that the company is currently burning (2019/2020) around -50 mn CHF annually which is funded by loans.

The main shareholder with a 75% share is an entity called SEFAM which itself seems to be a family of funds managed by an asset manager called Crestbridge.,which however seems to be more of an administrator. Within my limited time >I did not find out who really owns this company.

Last year, Leclanché announced a far reaching cooperation with a Polish company. Looking at the stock price however it seems, that investors are not so excited about the company (yet):

As I am very interested in Battery technology, I will keep them on “watch”, however I will most liekly not consider investing int them as this looks very difficult to really understand.

134. Groupe Minoteries SA

GMSA is a 136 n CHF market cap flour mill group. They seem to concentrate mostly on Switzerland by sourcing local grain and selling locally. Not much to see here, “pass”.

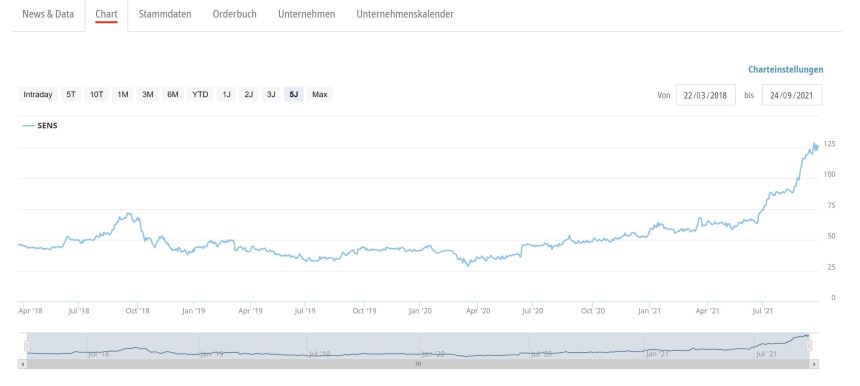

135. Sensirion AG

Sensirion is 1,95 bn CHF market cap that, like many other stocks I have covered in this series, did very well since the pandemic stroke:

The company IPOed in late 2018 at 36 CHF and IPO buyers who kept the shares are most likely very happy with >3x in less then 3 years. The company manufactures sensors for a wide variety of use cases.

Looking at the 6M 2021 report, the numbers are indeed impressive. 6M revenues are now as high as full year 2017 revenues and EBITDA margins have doubled since then. Net profit has increased 3x yoy. In 2020 they seem to have benefited mainly from sensors for respiratory machines, now it looks like that their industrial sensors, espicially for CO2 measurement are really taking off. So far I haven’t thaought baout the fact that maybe one needs a lot of CO2 sensors for the whole decarbonisation process.

Just doubling 6M numbers, Sensirion is trading at ~30xPE, which is not that expensive compared to other Swiss stocks. As I find the CO2 sensors really interesting, this is a stock to “watch”.

136. Zur Rose AG

Zur Rose is a 3,9 bn company that distributes pharmaceuticals in Europe, especially in Switzerland and Germany. I bought the stock in March 2019 which was lucky timing.

On top of the potential deregulation of prescription drugs in Germany which should greatly benefit their DoMorris subsidiary, Zur Rose managed to actually be part of the consortium that builds the technical infrastructure for the GErman E-Rezept. On the other hand, Zur Rose is one of the most shorted stocks in Switzerland with a very volatile share price.

I did sell 40% of my initial position at around 250 CHF/per share, recapturing my initial investment plus something. The remainder of the position (5% of the portfolio) will stay a a long term position. Therefore Zur Rose is a “Hold”.

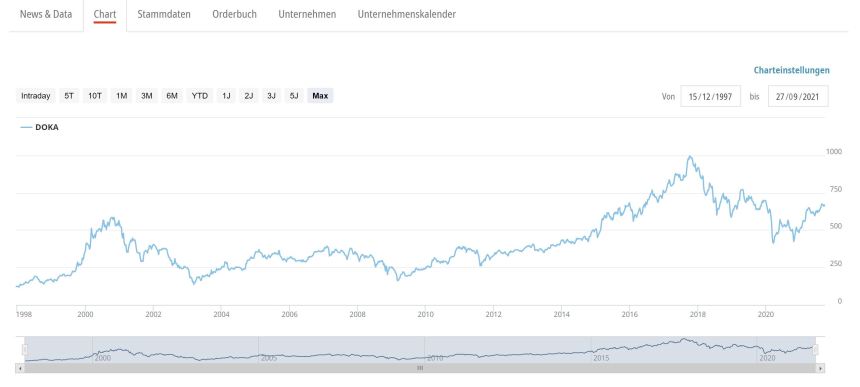

137. dormakaba AG

dormakaba is a 2,8 bn CHF market cap company that specializes in commercial lock systems and related physical security applications. I looked at the company back in 2018 when I was owning Dom Security, the smaller French competitor. Due to the significant minority interests, I found the stock too expensive at an EV/EBITDA of ~15 back then. At the time of writing, dormakabe is atrading at the same level as back then:

Covid had a certain impact on dormakaba,, both sales and EBITDA for the FY 2020/2021 (ending 30th june) are lower than 2017/18 when I looked at them, so the stock implicitly got more expensive. With a trailing PE after minorities of around 28x, I’ll “pass” again.

138. Warteck Invest AG

Warteck is a 600 mn CHF market cap real estate company that seems to have its roots in the brewing business. Despite a pretty decent long term track record, I do not want to use a lot of time on this, therefore I’ll “pass”.

139. Arundel AG

Arundel is a 36 mn CHF market cap company that seems to be a strange mixture of real estate and investment banking. On paper the company has a PE of only 3x, but profits mostly come from revaluing real estate. The company is highly levered. “Pass”.

140. Sonova AG

Sonova is a 23,3 bn CHF company that is one of the leading players in hearing aids. The company is one of the typical Swiss MedTech players with nice growth and nice margins. However, Covid set them back to levels from 2018. Looking at the chart, investors gave them the “Thumbs up” nevertheless and the stock price went up like hell in the last few months:

The company now trades at 9x sales and 40xEBIT. Yes, it is a decent business but I am really struggling to understand what kind of expectations investors have, who buy this stock at the current valuation, unless Covid vaccination significantly accelerates hearing loss (Joke !!). i haven’t checked in detail, but a company at thsi size will have much more difficulties to “grow into the valuation” than a smaller one.

Sonova is clearly a very good company but at these levels there is clearly very little room for mistakes, both, at a company level but also at investor level. “Pass”.

Have you looked at the online travel company lastminute.com? Trades on 6x EBIT and a 60% discount to Edreams. Management owns a large chunk.

Yes. You can search the blog for my opinion…

You could also go back through all the stocks that are on your watch list at some time.

Yes, i will slim down the watchlist of the end of the series.

Thank you for this brief but useful analysis. Next market to analyse could be the Austrian market therefore you will have covered the DACH region. And I am sure many readers do not know a lot about Austrian stocks (except the major names as Andritz).

Maybe I am prejudiced, but I don’t think that Austria is a ver yinteresting market, at least for me. Maybe at a later stage.

May you share your prejudice? 😉

As a former colleague (Austrian) told: wirh regard to financial markets, Austria is the most western country of the Balkans.

Sweden or Finland would be interesting. Former is wildly overpriced but some incredible companies. Latter has some quality hidden champions (Harvia, Musti, Valmet) that have done great.

The Nordics are interesting, indeed. However I would also think about Denmark (already 2 stocks in my portfolio) and Norway (3 stocks in my portfolio).