2021 Performance review – 2022 Outlook

2021 overview

2021 was a (for me) surprisingly strong year for equity markets with double digit growth across many equity markets.

In 2021, the Value & Opportunity portfolio gained +22,5% (including dividends, no taxes) against +18,5% for the Benchmark (Eurostoxx50(25%), Eurostoxx small 200 (25%), DAX (30%), MDAX (20%), all performance indices including Dividends).

Links to previous Performance reviews can be found on the Performance Page of the blog. Some other funds that I follow have performed as follows in 2020:

Partners Fund TGV: +38,2% (30.12.)

Profitlich/Schmidlin: +20,0% (30.12.)

Squad European Convictions (30.12.) +25,0%

Ennismore European Smaller Cos (30.12.) +23,1% (in EUR)

Frankfurter Aktienfonds für Stiftungen (30.12.) +17,3%

Greiff Special Situation (30.12.) +5,5,%

Squad Aguja Special Situation (30.12.) +5,4%

Paladin One (30.12.) +14,6%

It should be mentioned that this year, the performance of most funds clusters much closer together than in the “Corona lottery year”, where returns were spread between +35% and -10%. Lucky me that I am invested into the best performing fund in my peer group ;-). Interestingly, the best performing fund in 2020, Aguja, was the weakest performer in 2021.

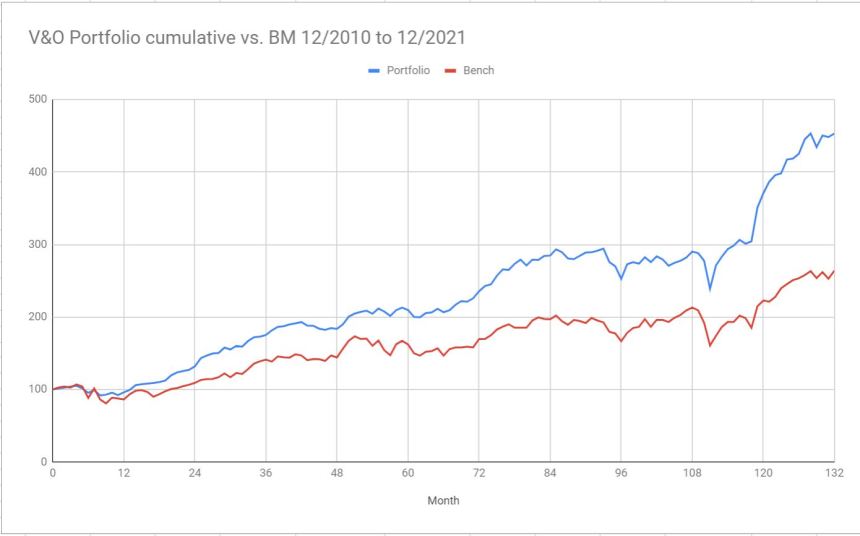

Over the 11 years from 12/31/2010 to 12/31/2021, the portfolio gained +354% against +169% against the Benchmark (Eurostoxx50(25%), Eurostoxx small 200 (25%), DAX (30%), MDAX (20%), all performance indices including Dividends).. In CAGR numbers this translates into 14,7% p.a. for the portfolio vs. 9,2% p.a. for the Benchmark. As a graph this looks as follows:

Current portfolio / Portfolio transactions

New positions:

In January, I added JustEat Takeaway.com and Alimentation Couche-Tard. I actually added to JET in April but then sold in June completely (with a loss of around 17% at 75,5 EUR).

In February, I bought a 2% position in BioNTech. I have to confess that despite the small position size, the volatility is not easy for me to stomach. I sold around 1/3 of the position with a profit of around 200% relatively early so that the remaining position is “profit only” which makes it easier for me to hold for a longer term. The last new position in Q1 was Euronext as a “opportunistic” investment.

In May I started the “Energy Transition Basket” with 2 new small stakes in Orsted and Aker Horizon. A month later, I added NKT and Nexans to the basket.

In July, Meier & Tobler joined the portfolio as the first “harvest” from my All Swiss Shares series. Other new Swissis were ABB and Schaffner. Both have an interesting Energy Transition/Electrification aspect. ABB is a little bit more opportunistic due to the expected EV spin-off in 2022.

Sold positions

I sold Installux, as well as my complete Travel Basket (Hostelworld, ENAV, JD Wetherspoon, Southwest and Dufry) as I got cold feet early on the 2021 travel season. I also sold SFPI (much too early) and Agfa.

The current portfolio per 31.12.2021 can be seen as always on the portfolio page.

Some Portfolio statistics

The weighted holding period as of 31.12.2021 has been 3,8 years and is within my target of 3-5 years. The 10 largest positions account for around 53% of the portfolio, the largest 20 for around 82%.

Allocation by country (ex Funds):

| Country |

In % of Portfolio

|

| FR | 19.4% |

| CH | 16.2% |

| DE | 13.5% |

| UK | 13.1% |

| NO | 7.3% |

| CA | 3.8% |

| SE | 3.2% |

| IE | 2.9% |

| DK | 2.8% |

Allocation by currency:

| Currency |

In % of Portfolio

|

| EUR | 39.7% |

| CHF | 16.2% |

| GBP | 13.1% |

| other | 10.2% |

| NOK | 7.3% |

| CAD | 3.8% |

| SEK | 3.2% |

| DKK | 2.8% |

From a country / currency perspective, this is clearly a European portfolio, within Europe it looks quite diversified. A surprise to myself was the relatively low weight of EUR based companies. This helped the portfolio a little bit in 2021, as many European non-EUR currencies appreciated against the EUR including the GBP.

Allocation by market cap (ex funds, cash):

| Market cap mn EUR | Percentage |

| 0-500 | 19.8% |

| 500-1000 | 26.7% |

| 1000-10000 | 14.2% |

| >10000 | 21.6% |

The range in market cap is quite high, from 98 mn EUR at the low end (Netfonds) to around 76 bn EUR (Richemont). From the perspective of US Mega caps, all these stocks look like small caps. Overall more than half of the direct held stocks are below 1 bn EUR market cap which I consider small caps.

Performance analysis:

“Active share” vs “do nothing”

The “Do nothing” approach, i.e. just letting the Portfolio run from 31.12.2020 and collect dividends would have only resulted in a performance of 16,75%, so my “active contribution” in 2021 was quite good (or the 2020 portfolio was not so good…). The main reason for this were to a large extent Biontech and Alimentation Couche Tard and the Electrification basket vs. the Tourism basket who together added something like 500 bps to performance. Also the partial cash outs for Play Magnus and Siemens Energy helped. SFPI on the other hand cost me a relative 100 bps from where I sold them.

So at least for me, being active in my portfolio seems to add value that offsets the tax impact I have at a personal level compared to “do nothing”.

Performance drivers

The top 10 performance contributors to 2021 were as follows (absolute contribution):

| Stock |

Contribution 2021

|

| Biontech | 2.8% |

| Thermador | 2.3% |

| Richemont | 2.2% |

| Partners fund | 2.1% |

| Perrier | 2.0% |

| Admiral | 1.7% |

| Sixt vz | 1.7% |

| Alimentation couche-tard | 1.5% |

| VEF | 1.2% |

| Netfonds | 0.9% |

| Top 10 total | 18.2% |

What is noteworthy is that many of the main performance drivers were well performing “mid size” positions (2-4%) and the largest positions from 2020 (Naked, Admiral, TFF) did not do that well. However this is normal for a longer term portfolio as not every stock can do well every year.

The main negative contributor was Zur Rose which was the main positive performance driver in 2020.

Monthly returns and outperformance:

| Perf BM | Perf Portf. | Delta | |

| Jan-21 | -0.7% | 4.3% | 5.0% |

| Feb-21 | 2.9% | 2.3% | -0.6% |

| Mar-21 | 5.3% | 0.6% | -4.7% |

| Apr-21 | 2.4% | 4.8% | 2.4% |

| May-21 | 2.2% | 0.3% | -1.9% |

| Jun-21 | 1.0% | 1.6% | 0.6% |

| Jul-21 | 1.7% | 4.7% | 3.0% |

| Aug-21 | 2.2% | 1.8% | -0.4% |

| Sep-21 | -3.7% | -4.2% | -0.5% |

| Oct-21 | 3.2% | 3.7% | 0.4% |

| Nov-21 | -3.4% | -0.5% | 3.0% |

| Dec-21 | 4.4% | 1.3% | -3.1% |

What is worth mentioning here is that outperformance is always “lumpy”, i.e. can change significantly from month to month. The monthly returns also show that my portfolio is not a “high beta” play.

Annual returns and outperformance:

| Perf BM | Perf. Portf. | Portf-BM | |

| 2011 | -13.8% | -4.1% | 9.8% |

| 2012 | 26.6% | 37.4% | 10.8% |

| 2013 | 29.3% | 32.8% | 3.5% |

| 2014 | 2.2% | 4.9% | 2.7% |

| 2015 | 12.5% | 14.1% | 1.7% |

| 2016 | 4.6% | 12.4% | 7.9% |

| 2017 | 16.1% | 20.9% | 4.7% |

| 2018 | -15.3% | -11.3% | 4.1% |

| 2019 | 27.9% | 15.0% | -12.9% |

| 2020 | 4.5% | 27.7% | 23.1% |

| 2021 | 18.5% | 22.5% | 3.9% |

What I mentioned above also applies for annual returns: Outperformance is lumpy. My target is 3-5% outperformance per year (currently 5,5% since inception), but in any year this can diverge a lot. As 2019 showed, there can be years that even show a significant underperformance as my portfolio is as far “off benchmark” as it can be.

Mistakes made in 2021

The biggest mistake in 2021 was clearly to sell SFPI too early. This was a behavioural mistake (selling when I was back in positive territory) as well as a principal mistake, as I never dug deep enough into the company, after I exchanged my DOM security shares into SFPI some years ago.

Other minor mistakes were not to add to positions where I originally intended to do so (VEF, Sixt Vz, Mediqon).

What went well in 2021

Overall, I was able to add some new “quality positions” at reasonable prices in 2021, especially Alimentation Couche-Tard, Schaffner and Meier could be long term holdings if things turn out as I expect. Also buying some BioNTech despite being outside my circle of competence turned out to be a good idea.

On the other hand, selling shares partially if the price appreciates very quickly, turned out to be a good strategy in 2021. Play Magnus, Siemens Energy and BioNTech were cases where it made sense to take some money off the table.

However one needs to be realistic: This could also been only pure luck, only time will tell.

What I have learned in 2021

I have (again) found out that I am not an investor who likes to have very volatile shares in my portfolio. With Play Magnus, Zur Rose, BioNTech and Naked Wine at times I had at least 4 very volatile stocks in 2021 and I have to say that this is the maximum that I can stomach. I have also learned that an initially relatively “normal” stock can become a hot stock within a relatively short period of time.

Another lesson was the confirmation that I am not able to predict the relative development of my portfolio stocks in any given year. Over the years, I participated in some “give me your 3 favourite stocks” contests and I always perform poorly. The best performers are usually stocks where i wouldn’t have expected it. Therefore, at least for me, more concentration doesn’t make sense.

Outlook & Strategy 2022

If I look through my annual performance reviews, the outlook and strategy is almost always the same: Stay Cautiously optimistic and continue to do what I have been doing and try to improve gradually.

My gut feeling tells me that I should be extra cautious, as 2021 has shown even crazier mini bubbles than in the already crazy years before (EV stocks, Crypto, SaaS, Frank Thelen etc.). However this “market timing gut feeling” has been wrong more often than it was right so I try to ignore it as good as I can.

One trend that I described in the Q3 comment seems to be playing out rather rapidly: The “Easy Tech” money really seems to be over. The momentum darlings are falling harder than ever. I would be extremely cautious to assume a “V-Shaped” recovery for many of these stocks. Some of those that I have covered in the blog (Auto1) are still significantly overvalued.

I think we will see a few interesting effects: First of all, there will be a couple of new “Theranos and Enrons” revealed, both in the public and private space. Once the money flow is stopping, these “businesses” might unravel quickly. I might be wrong but the fact that no one is doing real DD any more (Tiger Global, Softbank, SPACs) makes it very easy for fraudsters. Nikola, one of these frauds that I had covered, might only be the tip of the Iceberg.

A second effect will be that a lot of high growth / high loss companies will need to cut advertising budgets and suddenly they will become low growth / high loss companies.

Of course there will be some companies that are really the next Google or Amazon or Salesforce, but hose are very few in my opinion.

However, as anyone who remembers the Dot.com area, there is always the chance for one crazy final “melt-up” like it has happened in early 2000 after the initial Y2K panic. So for me this means that despite the attraction, I will stay away from shorting.

The only idea that I am contemplating is to buy “very far out of the money puts” on the “nothing will ever go wrong” stocks like Google, Microsoft or Apple. Because something might go wrong at some point in time.

2021 was a tough year in terms of keeping up with long only benchmarks, so nice work!

The Agfa position

Interesting as always. The portfolio has a 1.9% exposure to Belgium?

Good observation. I have mislabeled Euronext which is French/Dutch and not from belgium. Agfa I sold already in 2021.