All Danish Shares part 9 – Nr. 81-90

And on we go, another 10 randomly selected Danish stocks. In the current batch, there are some very interesting and unique business models, however only one made it onto the “watch list”. We are now at ~50% coverage of the universe. Once again a quick reminder: Thank you for any requests to look at a specific company, but the random generator determines in what order I look at companies.

81. Scandinavian Medical Solution A/S

Scandinavian Medical is a 17 mn EUR market cap company that seems to be active in trading second-hand medical equipment that was IPOed in late 2021. Not my area of expertise. “pass”.

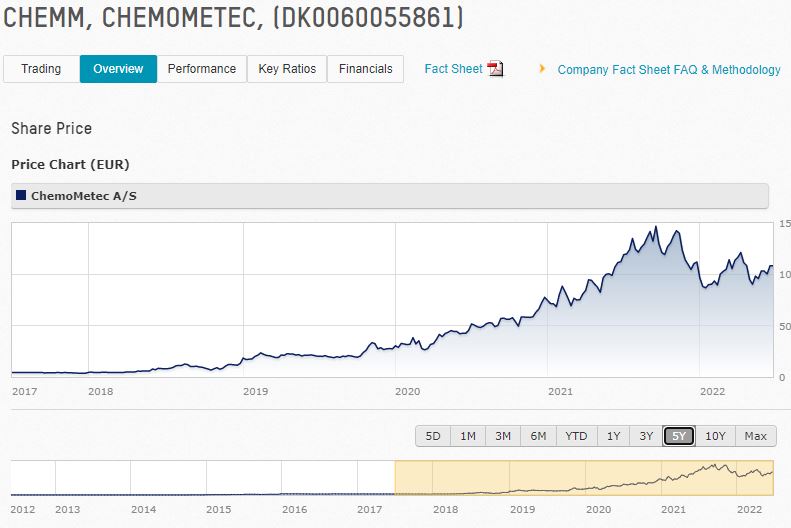

82. ChemoMetec A/S

ChemoMetec is a 1,9 bn EUR market cap MedTech company that offers Equipment to count cells which, among others is used for Advanced Cell Analysis, Counting of Mammalian Cells, Yeast Cells, and Sperm Cells.

The stock has performed very well over the last 5 years:

The company has been growing 20-50% p.a. over the past few years and is very profitable (Gross margins 90%, operating margins 45%). However at 40x sales and 85x EV/EBIT, there seems to be a lot of growth priced in. Much too expensive for me, although it looks like an interesting company. “Pass”.

83. SameSystem A/S

SameSystem is a 18 mn EUR market cap SaaS company offering some kind of HR solution. The company IPOed in 2021 and for some reasons, earnings turned highly negative after the IPO and the share price declined by more than -60% form the IPO. “Pass”.

84. EGNSInvest EJD., TYSKLAND

EGNSInvest is a 87 mn EUR market cap real estate company. As the name indicates, the company invests only in Germany, mostly in Berlin. The share performance is quite impressive, doing almost 4x over the last 10 years. Information however is only in Danish and I am not such a big real estate fan, therefore I’ll “pass”.

85. CEMAT A/S

CEMAT is a 29 mn EUR market cap real estate holding that seems to own only one Warsaw property. The share price jumped significantly last year and the company showed a very high profit in 2021 but it seems that this was due to a (non-cash) revaluation of the property. “Pass”.

86. Brdr. Hartmann A/S

Hartmann is a 231 mn EUR market cap company that has nothing to do with the German/Swiss Hartmann Group. The company has a very interesting business: It is specialized in producing egg packaging. On top of that, the company is also active in fruit packaging in South America and in manufacturing machinery for egg packaging.

The long term share price development is somehow mixed as one can see in the chart:

The company is majority owned (69%) by a bigger conglomerate named Thornico. In 2020/2021, the company enjoyed extra business and much higher margins due to Covid. However in 2022, Hartmann seems to have been hit hard by Ukraine and Russia, where they seem to have been quite active and acquired a company in 2020.

The company also seems to have been hit in Q1 by increasing energy costs and input costs (recycled paper) which they could not pass on to clients. Hartmann gave a very wide range for 2022 guidance, anywhere between 2-7% net margin on ~1,9-3,3 bn DKK sales. Taking the midpoint, Hartmann would earn (3,1 bn *4,5%)= 140 mn DKK which translates into a P/E of around 12,4x.

Historically, the company earned around 30% of Gross Margins ~10% EBIT margins and net margins between 4-7%, returns on capital also looked quite ok. So if they manage to go back to the historical range, the stock would even be cheaper.

On the negative side, organic growth might be limited and they do have exposure to more volatile markets (e.g. LatAm).

Overall, I think Hartmann could be an interesting company despite the current problems, therefore I’ll put them on “watch”.

87. Astralis A/S

Astralis is a 17 mn EUR market cap company that is active in Esports and owns three esports teams competing in Counter-Strike, League of Legends, and FIFA. The company was IPOed in 2019 and looking at the share price, doesn’t seem to do so well:

After losing money, both in 2020 and 2021, the company predicts at least EBITDA break even for 2022. My gut feeling says that just owning an E-sports team might not be the best business in the world,. Most likely game developers are those who make the most money. Therefore I’ll “pass”.

88. Re-Match Holding A/S

Re-Match, with a market cap of 27 mn EUR, is another young company with a quite interesting business model per the stock exchange summary: ” an international recycler of synthetic turf fields and is committed to environmental sustainability. It provides sports arenas and stadiums with the opportunity to dispose of worn-out synthetic turf in a safe and environmentally friendly way.” However, the stock price has halved since IPO. This might have to do with the fact that sales are not growing, but losses are increasing. “Pass”.

89. FastPass Corp A/S

FastPass is a 5 mn EUR market cap Software company that seems to be around for some time without much progress, they don’t seem to have any sales. “Pass”.

90. Glunz & Jensen Holding A/S

Glunz & Jensen is a supplier to the printing industry with a 19 mn EUR market cap. The company has been shrinking consistently over the past 10 years, nevertheless they managed some turnaround in 2021. As I do not like investing into strong headwinds, I’ll “pass” here as well.

Gibt es irgendwelche Probleme mit der dänischen Quellensteuer?

Hi MMI,

Do you mind if I ask what retail broker is good for trading Danish stocks? Greatly appreciate in advance. I was about to place an order on Brodrene A&O Johansen then I found out IBKR didn’t deal with Copenhagen. What a bummer.

I use regular German brokers ( Consors, Sbroker). Both offer Copenhagen.

I bought A&O via Comdirect

thanks fellas