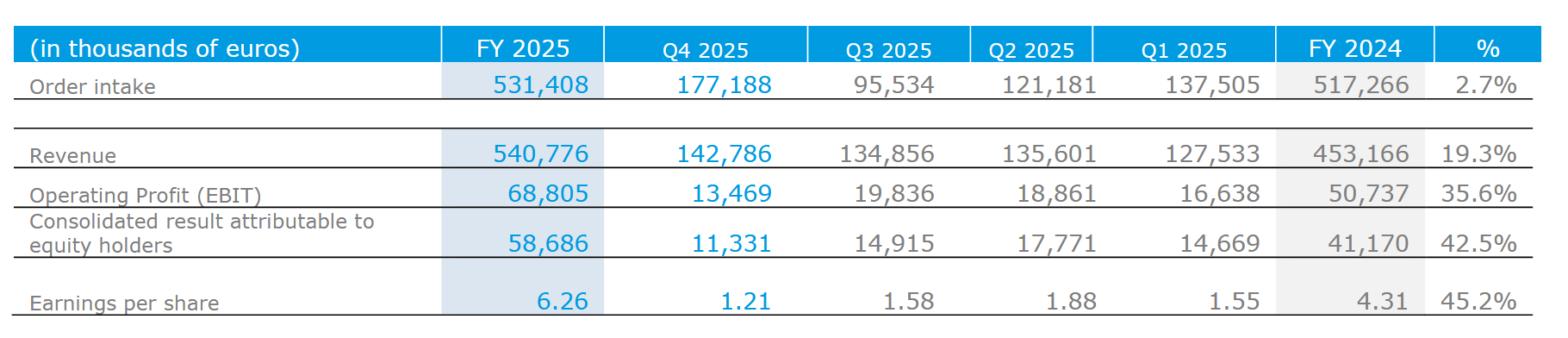

Sales up 19,3%, EPS up +45%. The Dividend will be 1,50 EUR, up 0,50 EUR from the year before. The only not extremely positive number was order intake which was only slightly up. I think it would be foolish to think that Jensen can grow 20% sales every year, but Management sounded quite confident for 2026 as well:

At a trailing PE of 11, the stock is now exactly as cheap (LTM) as when I published the initial analysis in January 2025, despite a 50% plus share price increase.

I have added a little (0,4% of portfolio) to my position at Friday’s price as I think the stock is still way too cheap given the quality. I should have waited until today, but such is life.

SFS

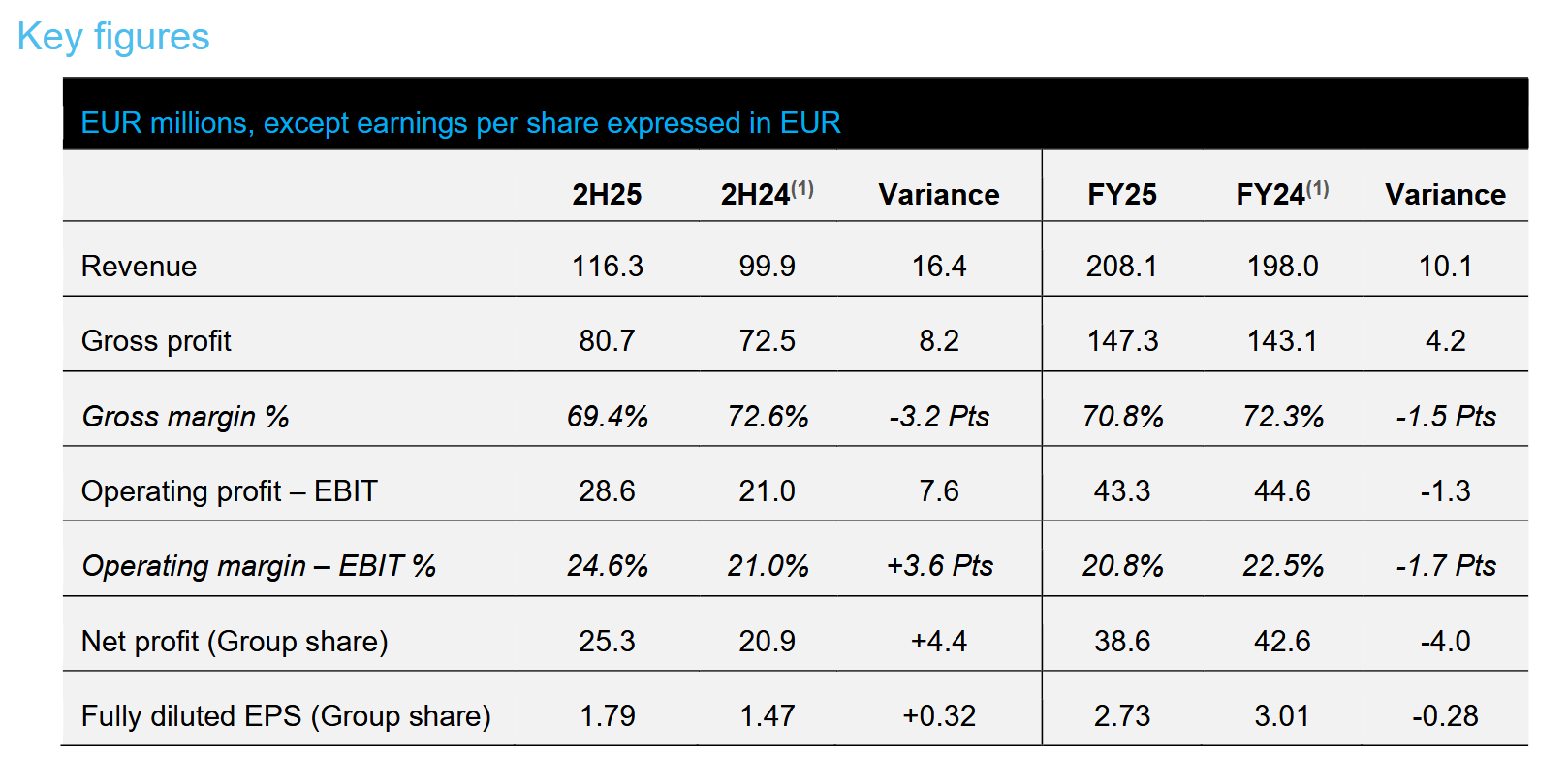

SFS, the Swiss parts and tools manufacturer/distributor also published preliminary results last week. Given the difficult state of many of its end markets, organic growth of ~3% before FX is quite impressive.

Unfortunately, profit suffered a little more as we can see in this table (before “normalisation”):

To be honest, SFS is quite behind against my expectations from 3 years ago, even factoring in CHF/EUR development.

I think back in 2023, I was too optimistic about manufacturing in Europe which really is struggling:

The stock is now much more expensive despite EPS being lower. So I really need to think about whether I should continue to hold the stock.

Italmobiliare

Italmobiliare’s preliminary 2025 numbers were a “mixed bag”. NAV increased (incl. dividends) by 6%, but for the two largest stakes, Borbone (Ebitda down because of high Coffee prices) and Santa Maria Novella (only single digit growth), the results were a little bit disappointing.

On the plus side, they managed to acquire an additional 5% stake in Bene and Casa de Salute grows nicely.

The stock reacted quite negatively which lead to an increase in discount to NAV.

At least for Borbone, things should look a lot better in 2026 as Coffee prices have come down again:

It will be interesting to see if SMN can grow double digit again.

On the plus side, the NAV increased by 10% in 2025, mainly driven by the Chocolate business:

Also positive is that they will acquire the remaining 34% of Jeff De Brugges, their second Chocolate Brand.

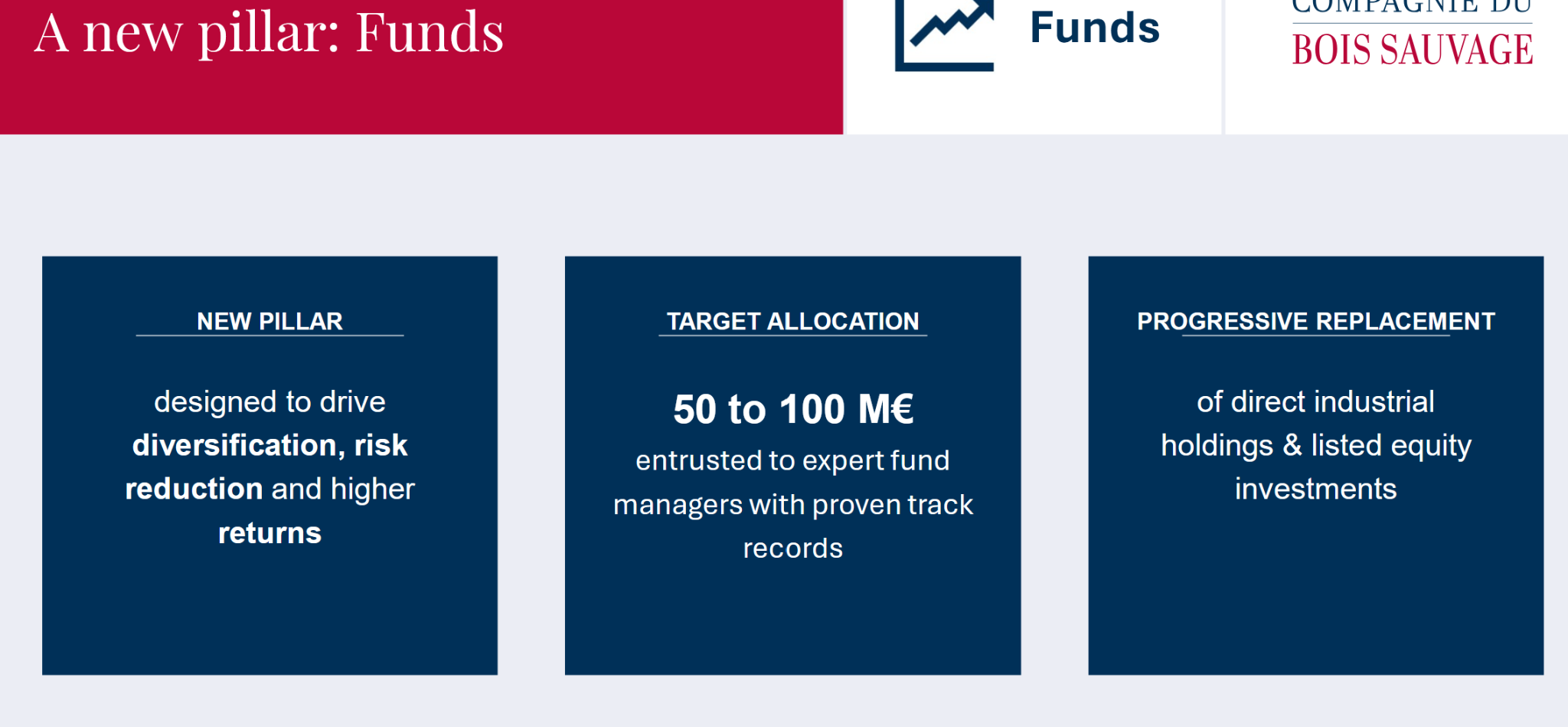

Less positive was the disappointing development of the Real estate pillar (NAV -10%) and the decision to discontinue industrial participations and invest into PE funds instead:

This is really a downer in my opinion. As much as I like the Chocolate business, I do not understand this “new pillar”. As I mentioned in the initial post, this was meant to be a short term special situation. Therefore I decided to exit the stock at current prices (318 EUR). This was a decent Short term special situation with a 20% plus return in 3 months.

The last few days are super busy with 8 (or more ?) of my companies reporting 2025 numbers. That’s why I do only the first 4 right now, the others (Jensen, SFS, Bois Sauvage and Italmobiliare) will follow soon.

EVS Broadcast 2025 preliminary results

EVS released preliminary numbers last Friday. At first sight, they were a little bit of a “mixed bag”. Revenue was up which is good for an “odd” year, EPS slightly down.

EVS explained that that they have invested into people to penetrate especially the US market. The second half of the year was really good, the first 6 months were weaker, mainly because of the “Tarif tantrum” from Uncle Donald.

The outlook for 2026 was quite good:

In the call, the CFO mentioned that for 2026 they don’t plan big additional investments into staff and that more M&A could be possible.

According to TIKR, analysts expect EPS of 3,36 for 2026. So far, the development is roughly within the initially expected case from 2024. Knowing EVS, there is also a good chance that they will revise 2026 numbers upwards during the year.

The 1,20 EUR dividend will compensate for waiting a little bit longer although Belgian withholding tax is not nice.

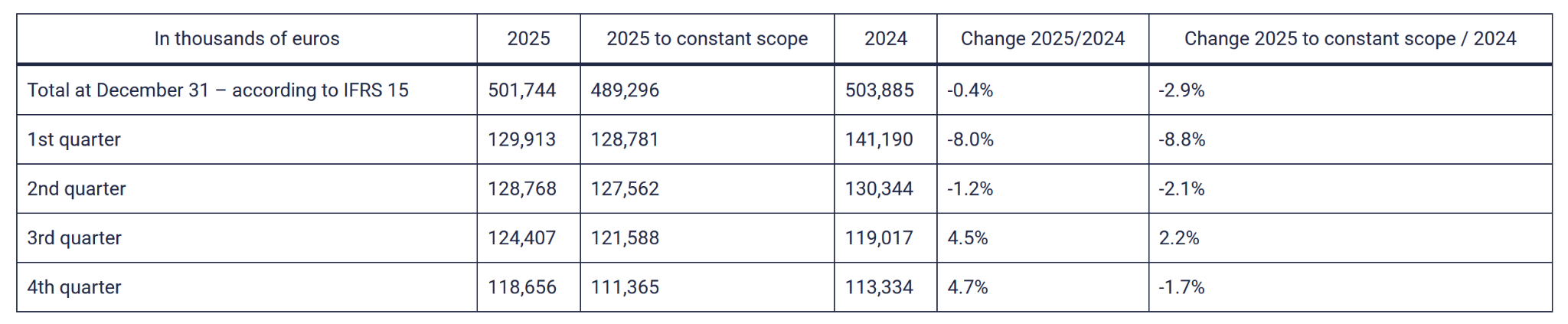

Thermador 2025 preliminary results

Thermador followed this week with 2025 results. As to be expected, sales were slightly negative y-oyy as construction and modernization is still weak in France:

What I find very surprising is how well the result kept up:

They managed to reduce working capital so they have a decent net cash position which should allow them again some M&A. And maybe, maybe the sector looks a little bit better in 2026. Analysts are quite positive. Thermador itself mentions a couple of Government programs which could be positive for them.

Thermador is a “hold” for me at the moment. Nothing to change here.

Eurokai preliminary results 20025

Eurokai also came out with an “Estimate” of the 2025 result. Typically for Eurokai, the result for 2025 will be significantly better than the revised estimates during the year.

They estimate now that 2025 Earnings will be above the 2024 earnings of 88 mn EUR (which included a 19 mn Non-cash positive one off).

Depending on what allocation the Golden share gets at Holdco level, this could result in an EPS of up to 6 EUR . Which means that despite the significant increase in the share price, Eurokai is still very cheap.

Investors should prepare once again for a very cautious outlook for 2026, although in my opinion, there are a lot of factors which indicate that 2026 could be once again better than 2025, even before any “juicy” one-off profits from partial sales to Container shippers.

The share price is now slowly approaching the historical ATHs from 2006/2007.

Eurokai is now by far my largest position but I leave that one untouched.

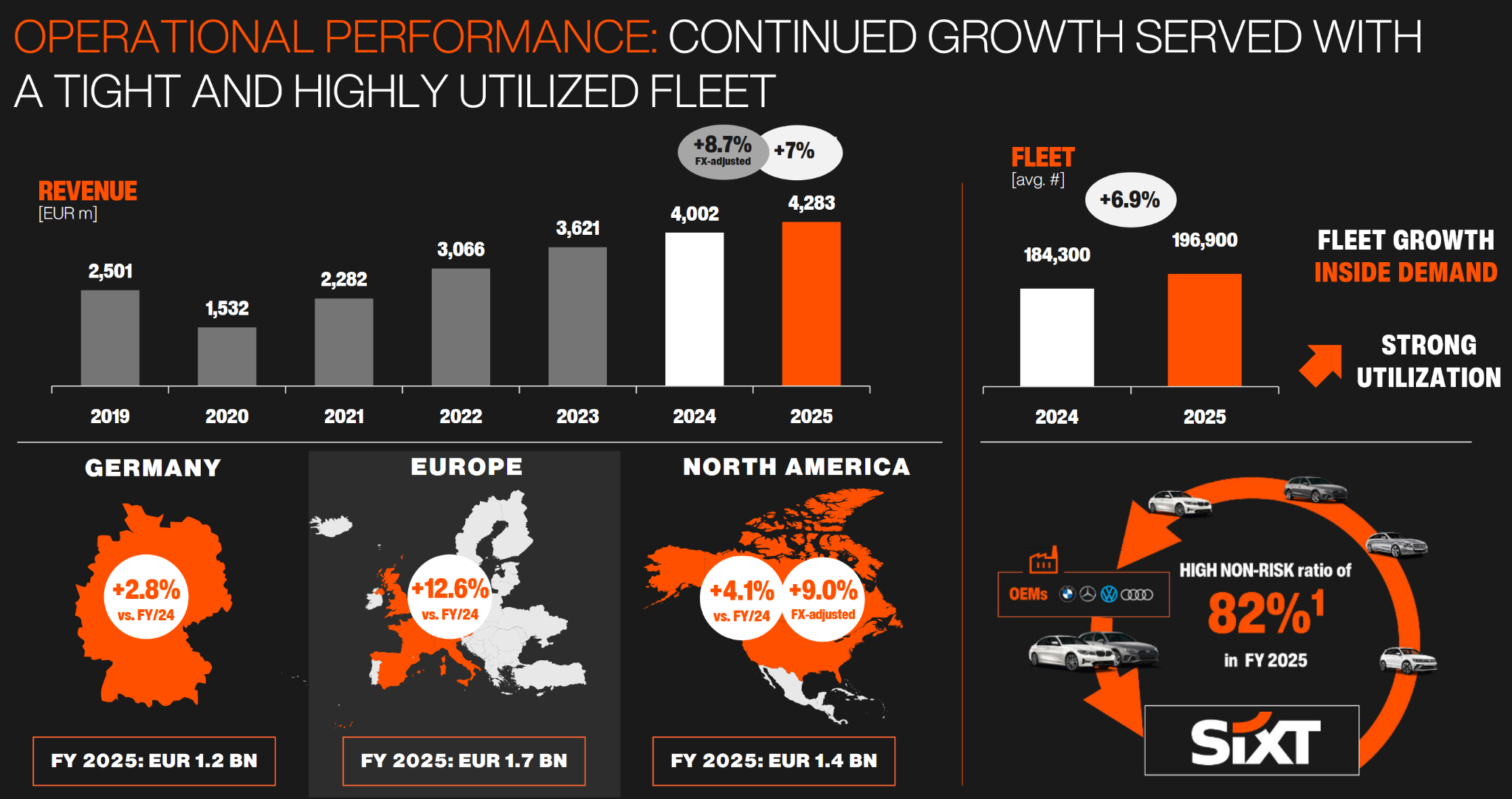

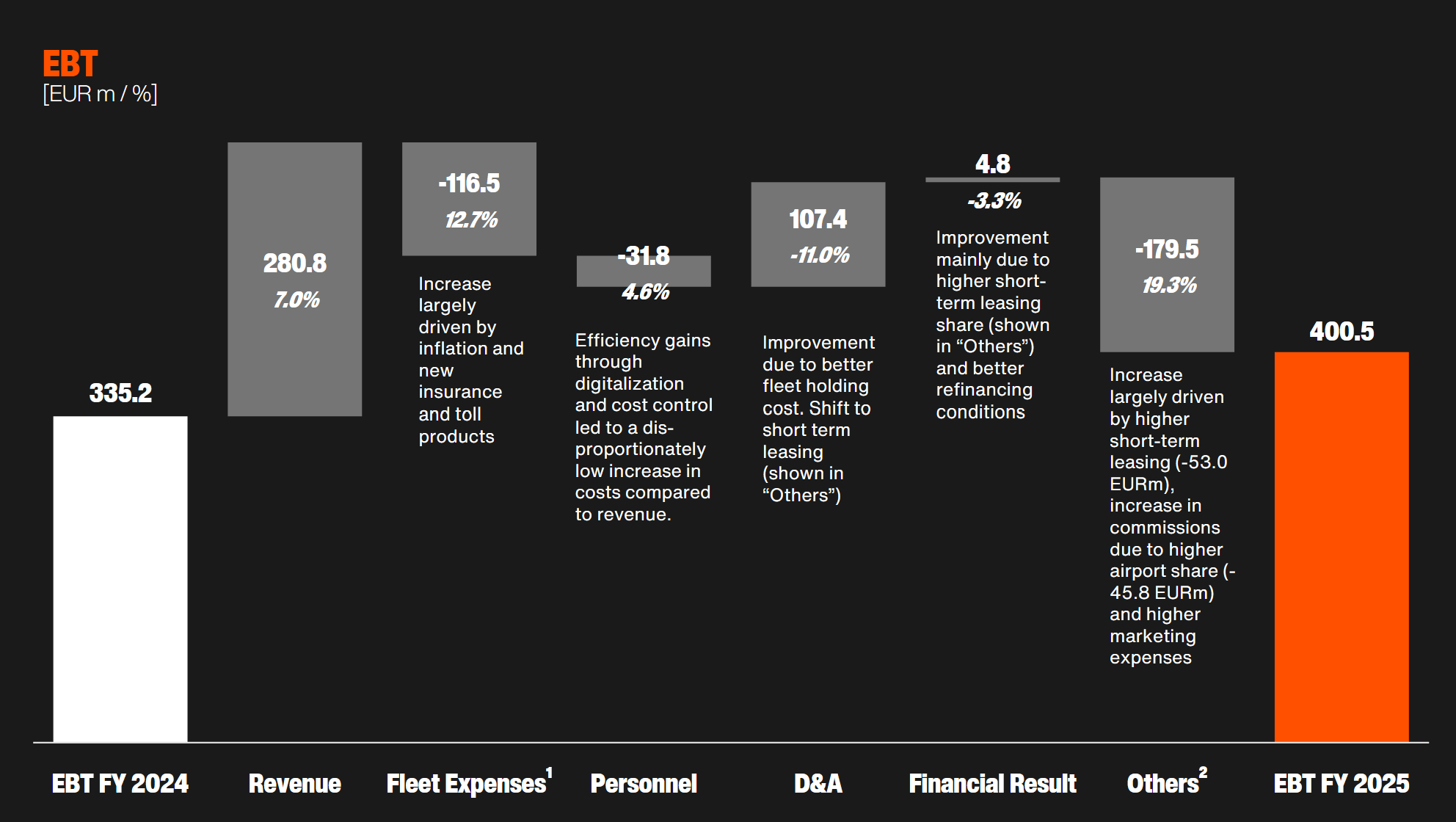

Sixt Preliminary results 2025

Sixt was the fourth company that week that released 2025 results. Although the results ended up to be a little bit below the forecast from Q3, it clearly seems that analysts have expected worse as Avis and Hertz both showed huge losses and declining revenues.

Sixt in contrast managed to grow also in the US:

And a significant increase in Profits:

What analysts seemed to have really liked was a quite optimistic outlook for 2026:

That seems to have surprised analysts and led to a “decoupling” of the share price from those of the weaker US competitors:

With a trailing P/E of 9 and a dividend yield of 5,8%, the pref shares are really “good value” in my opinion.

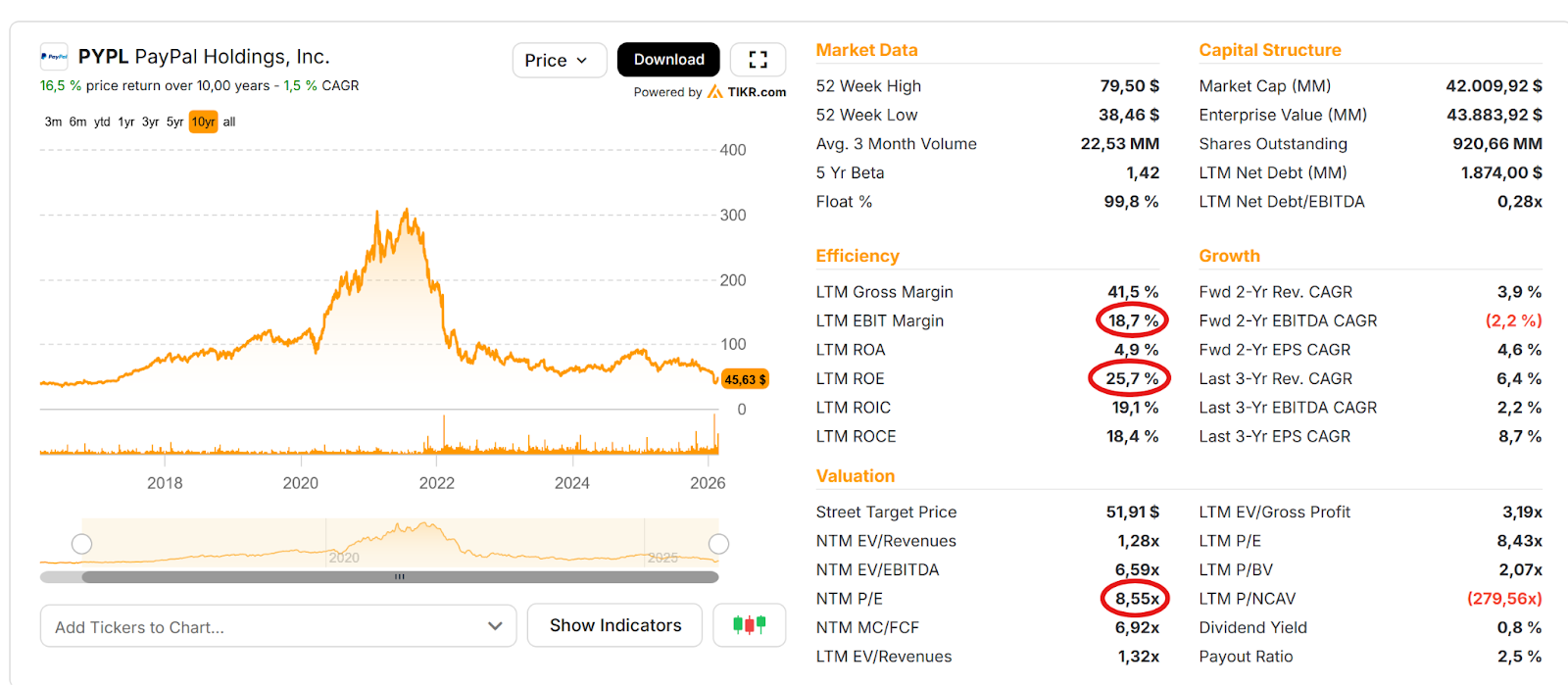

In this post I try to explore if Paypal is suffering only from temporary issues or if they have structural problems. My take away from a rather short analysis is that the problems are indeed structural and therefore the stock is not of interest to me for the time being.

Introduction

Paypal is one of those stocks that is both very present on my “”TwiX” timeline as well as has been mentioned in a couple of recent discussions with investors that I value highly.

At first sight it looks like a decent “Value” stock. Single digit P/E, large share buy backs, high free cash flow, good margins, decent ROE, hundreds of millions of clients etc. So what is not to like ? Here is the TIKR overview:

Paypal is also one of those stocks where everyone has an opinion as almost everyone has a Paypal account or is using other payment services frequently So at first sight, it looks like an easy to understand business which might lower their “barrier to entry” even for more inexperienced investors

Personally I have to admit that I find the payment space super complex and not easy to understand.

What problem does Paypal solve ?

Paypal’s main business is to allow retail customers to pay online for E-commerce activities and/or send money from one user to another within the Paypal network or via their additional P2P service Venmo.

Paypal has become successful because for consumers it used to provide a very convenient way without a lot of friction as compared to typing in your credit card details every time you use a new online merchant for instance. Paypal was also one of the first widely available services to send P2P money. You just need to know the Email address of the recipient.

Paypal describes itself as a “2-sided market place” connecting retail clients with E-commerce merchants.

For merchants, this was initially also very attractive as Paypal removed friction and increased the probability that a customer would actually finalize the purchase.

What Problems does Paypal have ?

When a widely known stock such as Paypal looks obviously cheap, my first thought is always the following:

What obvious problems does that company have and do I have a “variant perspective” ?

Especially for larger US stocks, assuming that everyone else is just stupid and you are the only one who can identify a single digit P/E ratio is naive to say it in a friendly way.

For me, temporary problems would be an invitation to dig deeper, whereas structural problems are much harder to handicap.

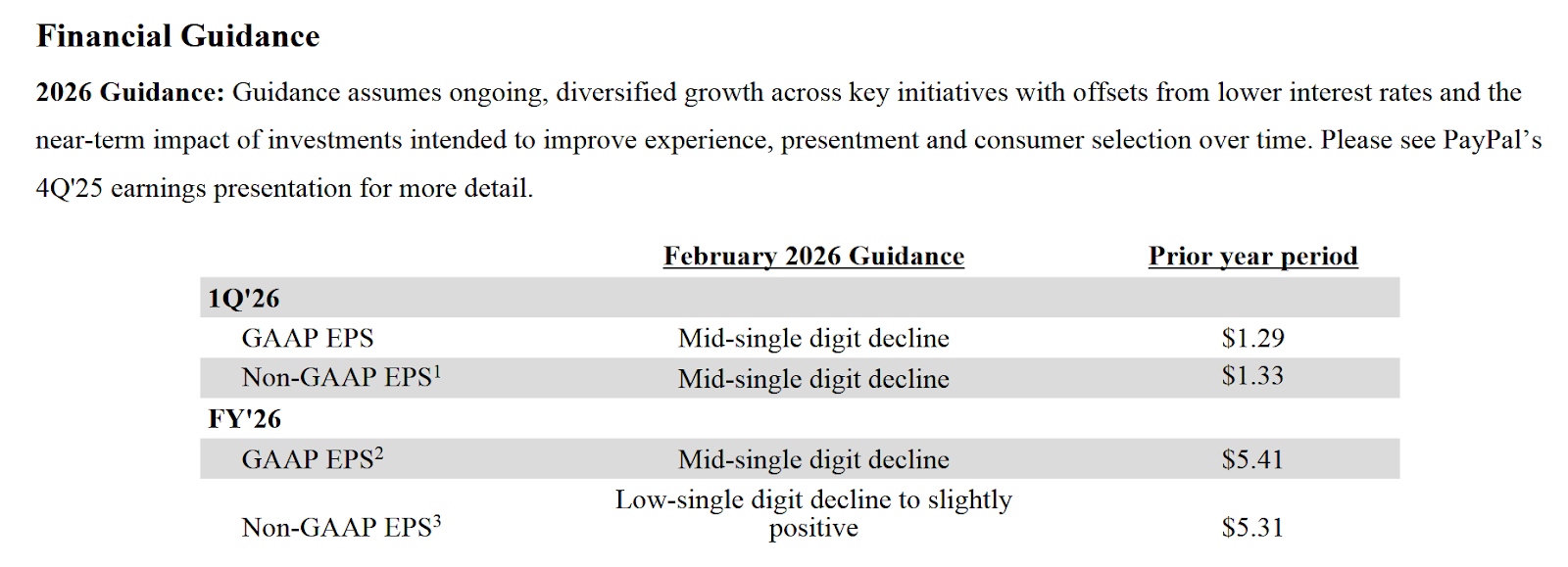

Paypal has some obvious issues, one of them being having a new CEO with little experience in the actual business and having guided to lower sales and profits in 2026

The new CEO since March 1st, Enrique Lores, is a long time HP Executive, who, according to Linkedin, has no direct payment or financial services experience.

Lores has some strong incentives directly linked to the share price. He will achieve the maximum amount if the share price hits 125 USD until 2029. His maximum compensation would be ~125 mn USD. This sounds like a large sum, but for Lorres, an long term HP executive, even that might not be life changing. He seemed to have earned around 19 mn USD and his net worth is estimated to be at least 50 mn USD. So he is rich already.

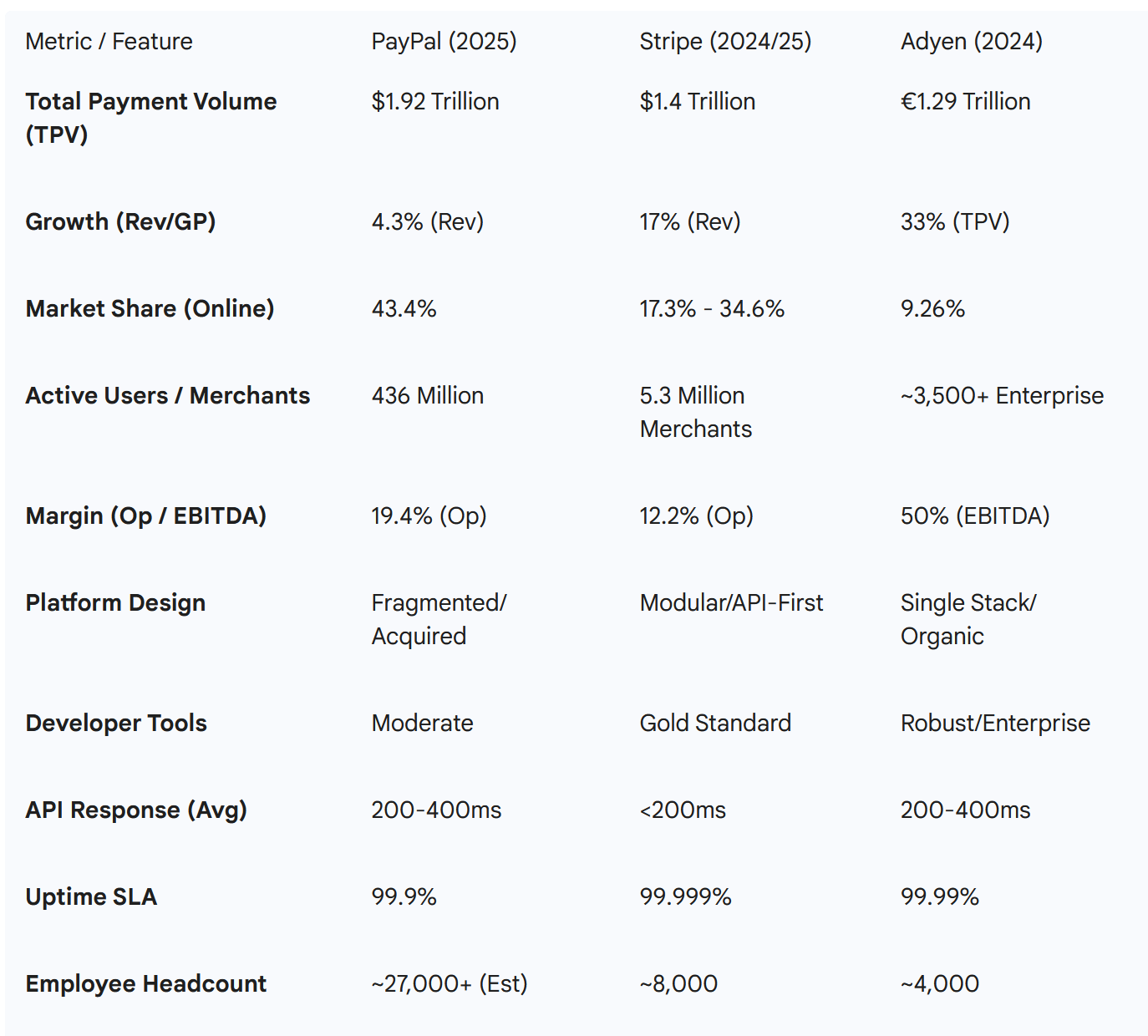

The bigger problem is clearly that the 2026 outlook looked very bleak. Especially compared to competitor Adyen which guided to 20% revenue growth in 2026 and beyond and not to speak of Stripe which has grown gross transaction volume by +34% in 2025.

It’s especially interesting to look at the 2025 investor day presentation. Back then, the former CEO Alex Chriss, who had at least some financial services background from Intuit actually made a pretty convincing pitch positioning Paypal as a “commerce platform”. This was their ambition back then:

After shrinking in 2023, Paypal delivered some growth in 2024 and also some growth in 2025 but as mentioned above, next year looks like shrinking again.

2025 results looke d“okayish” but on a quarterly basis, growth decelerated each quarter which most likely led to the dismissal of the old CEO-.

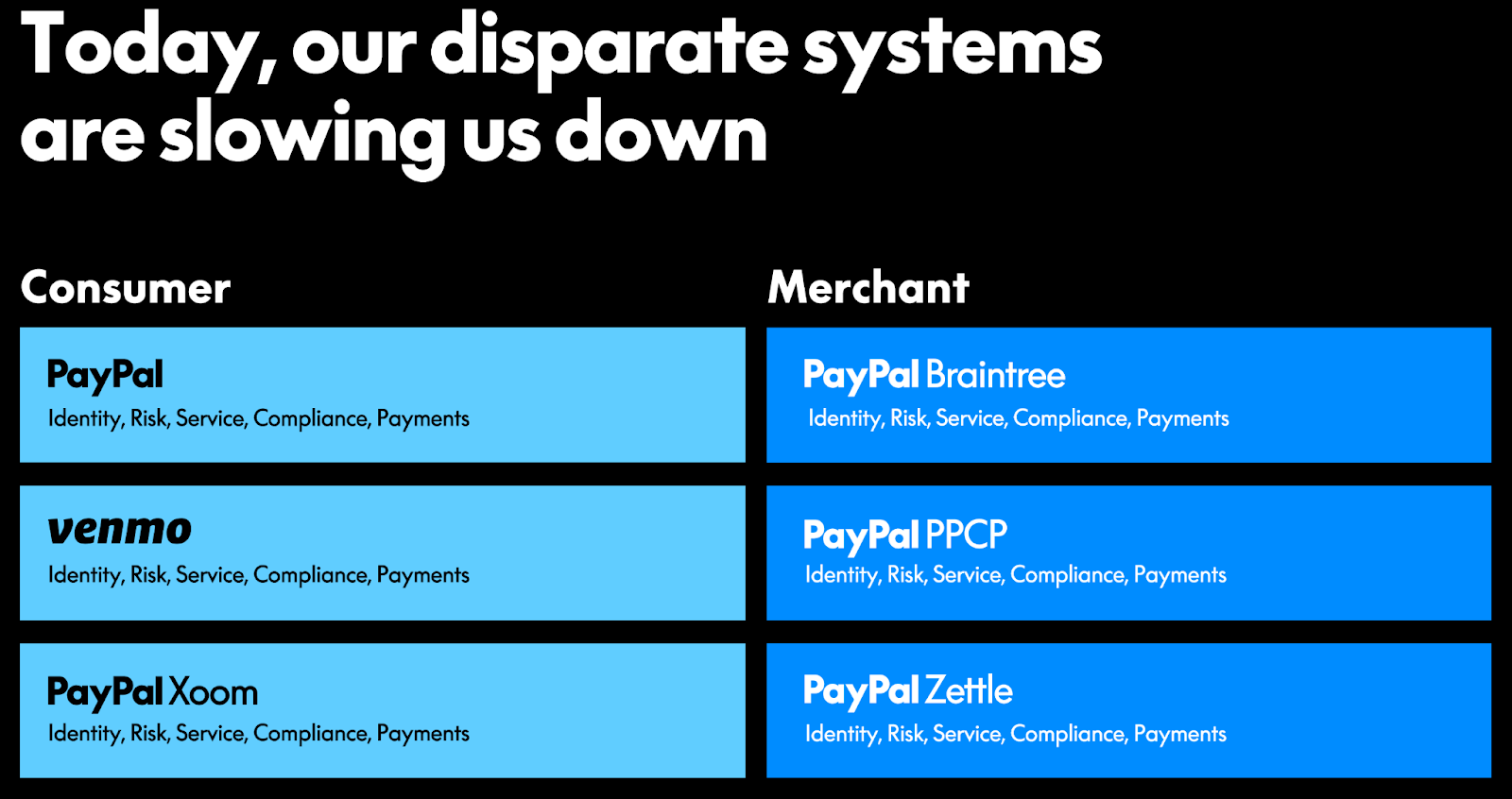

One of the major issues seems to be that Paypal runs at least 6 different platforms within Paypal according to this slide:

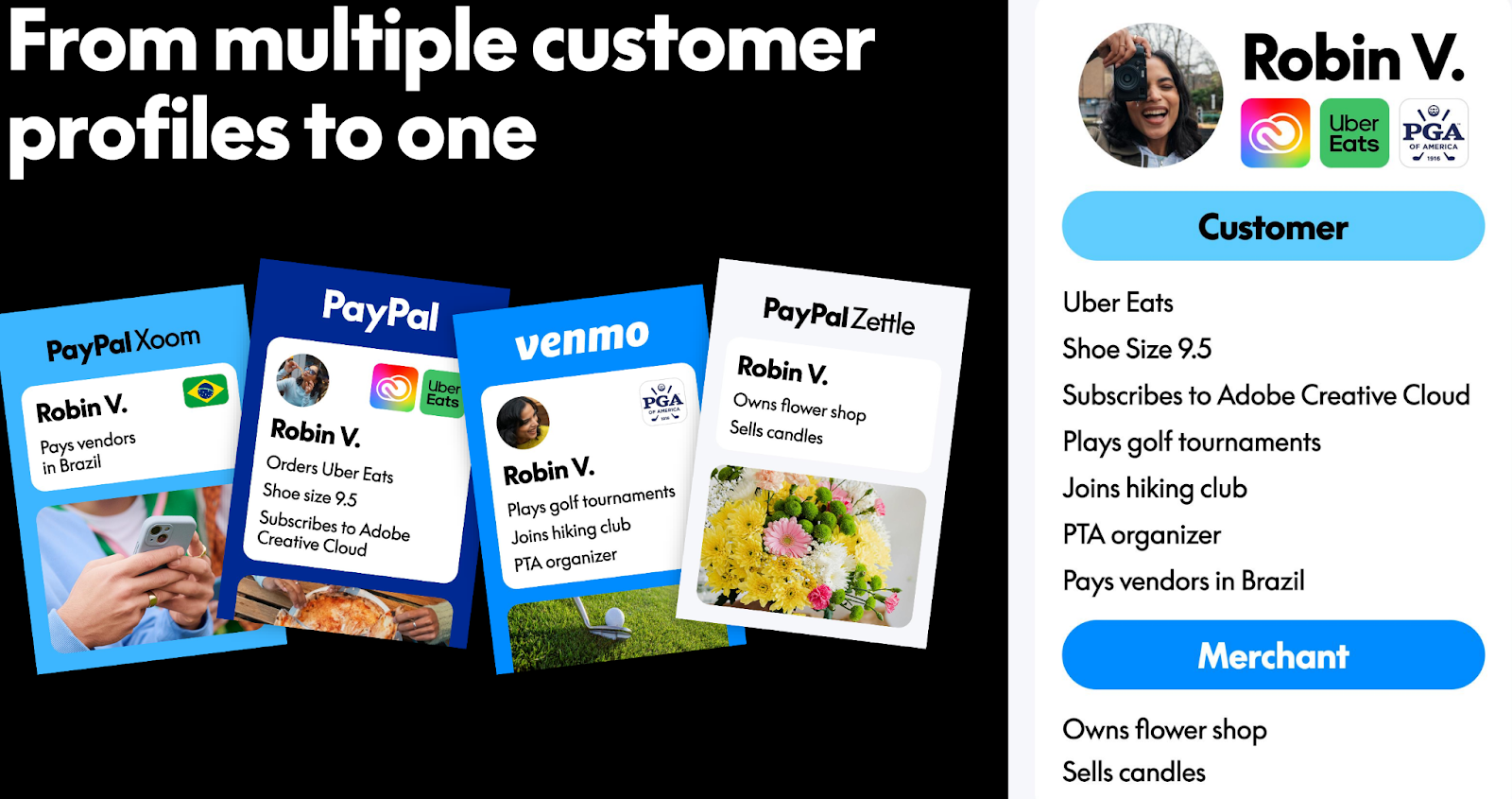

According to this slide, one user might have 4 different IDs across the Paypal services which are not connected so far:

Technical debt: Separate & outdated technical infrastructure vs, competitors on the merchant side

The chart points to one of the main weaknesses of Paypal: Paypal can be considered already a legacy player in the payments space. They have created separate platforms for separate use cases that are now just very difficult and expensive to handle.

The newer competitors from the merchant side like Stripe or Adyen all have one platform that runs all of their activities which makes it a lot easier to react and improve upon.

What is also interesting is that Paypal employs more than twice the employees of Stripe and Adyen combined. This is a table that Gemini compiled for me.

Additional attacks on the retail client side: Google Pay & Apple Pay, Revolout, Wise, Cash App etc.

As a “2 sided market palace”, Paypal unfortunately is also subject to massive disruption on the retail customer side.

If you are a mobile user, the probability is high that if you purchase something offline or online it is most likely down directly via your phone. You either hold your phone to a POS terminal in a physical shop or you confirm the purchase with a finger print or face scan of your phone which is even more convenient thant the Paypal Check-out.

At P2P level, both Paypal services are subject to a lot of competitors, such as Block’s Cash app, Revolut’s free transfers or Wise’s international transfers.

So simply said: there is no place to hide for Papyal.

Paypal is the most expensive option

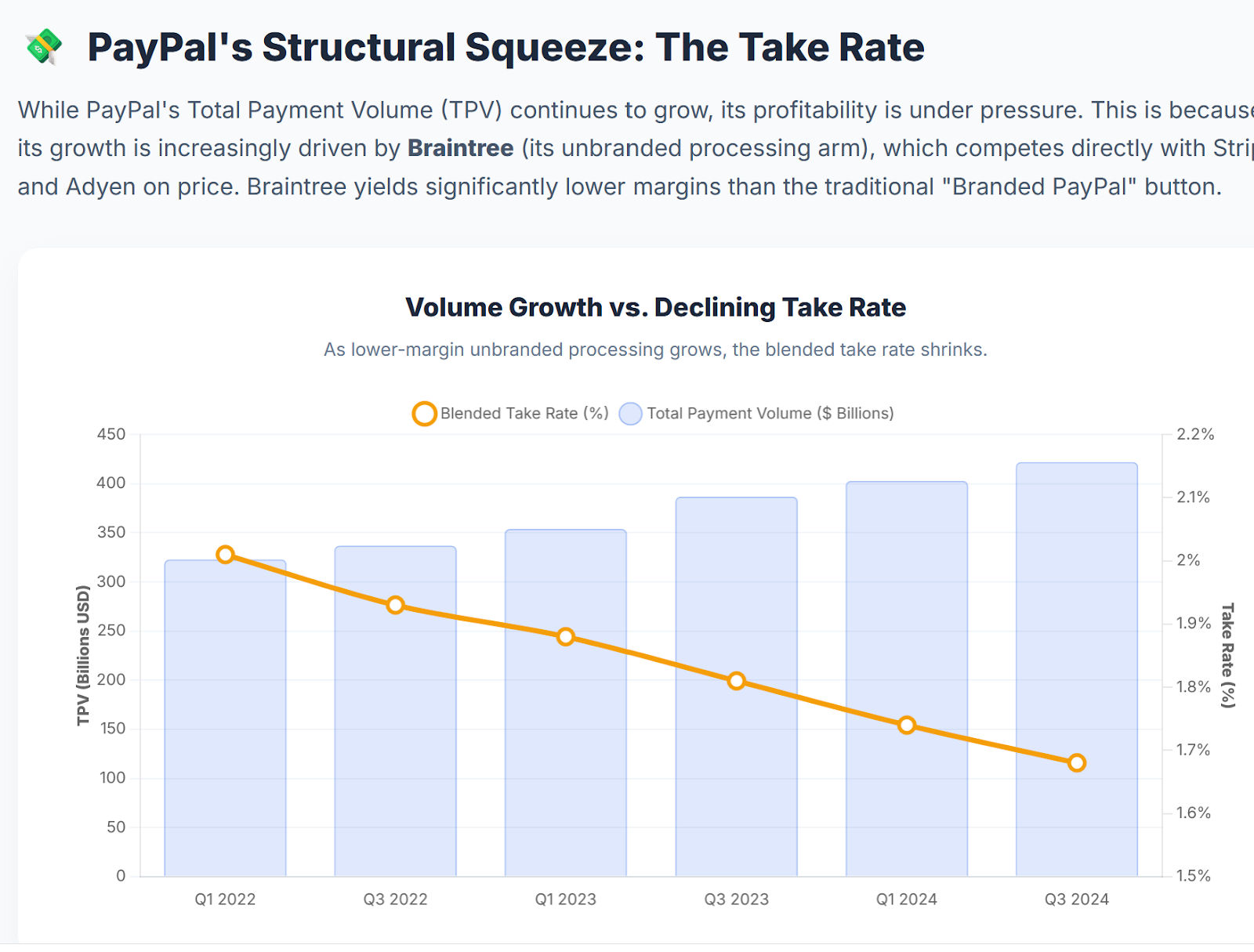

Some people will argue that Paypal is currently maybe the most profitable of the payments players. The main driver of this profitability is that Paypal charges significantly higher prices, both to merchants but also for instance for international transfers.

What looks now as a strength could turn out to be a weakness. “Your margin is my opportunity” was the famous motto of Jeff Bezos. The “take rate” of Paypal is heading down for quite some time (Chart from Gemini) as growth comes mainly from lower margin products:

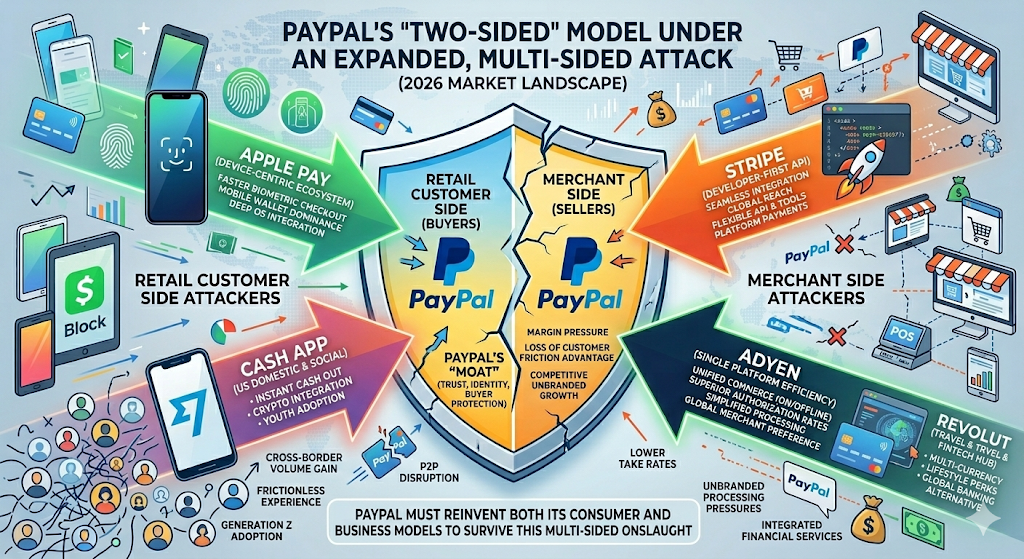

Paypal is under attack from all sides

Bringing it altogether is this graph that I asked Nano banana to create:

Paypal is the legacy player that gets attacked from all side from very agile and large competitors who have a much more modern infrastructure,

That’s the reason why Paypal is cheap. The last CEO tried to counter that but obviously was not very successful.

The Stripe take-over rumour

In the past few days, suddenly a rumour came up that Stripe might buy Paypal. To be honest, these kind of “someone told Bloomberg” rumours are often false.

As far as I understand Stripe’s business model, Stripe would have little to gain from a takeover. As a pure B2B company, I am not sure that the retail client base is of interest to them and if they could leverage that. And on the B2B side, Stripe can already do what Paypal is doing and I am not sure if they want to clean up the technical debt.

I guess Paypal would be a more interesting target for someone who might be able to leverage the retail customer base, but at 40 bn plus market cap plus premium it is maybe to big to be swallowed by most of the Fintech players.

“Too hard” for me

For me, the outcome of this quick exercise is that Paypal’s problem seems to be much more structural than temporary which for me makes it “too hard” to invest into.

Maybe the new CEO will pull all the levers and manage to turn around the business. But maybe he will not. It will be interesting to see if he will be able to implement a “kitchen sink” approach and maybe sacrifice a few quarters with really bad results or if the pressure is high to keep up share buy backs which will make it difficult to pay off the “technical debt”.

For the time being, Paypal looks similar to the hero of Jethro Tull’s song “Too old to Rock’n Roll”:

The old rocker wore his hair too long

Wore his trouser cuffs too tight

Unfashionable to the end

Drank his ale too light

Death’s head belt buckle, yesterday’s dreams

The transport caf’, prophet of doom

Ringing no change in his double-sewn seams

In his post-war-babe gloom

Now he’s too old to rock and roll

But he’s too young to die

Yes, he’s too old to rock and roll

But he’s too young to die

But anyway, this does not look like something that I would be comfortable to be invested in despite the superficially attractive “value KPIs”.

If someone has a very different view from the business perspective with regard to the competitive landscape, I am willing to listen 😉

Bonus Soundtrack:

Of course my choice is Jethro Tull – Too old to Rock n’Roll

Munich, 25. February 2026 – innoscripta SE (ISIN: DE000A40QVM8, the “Company”) expects an increase in revenue and earnings for the 2026 financial year based on current business development and continued high demand.

The Company’s Management Board currently expects the following for the 2026 financial year:

consolidated revenue of at least EUR 140 million and

EBIT of at least EUR 80 million

The guidance is based on the current order situation, the scalability of the business model, and stable regulatory conditions.

This guidance represents an expected +36% sales growth for 2026 (vs. + 60% in 2025) and +27% EBIT growth (vs. +70% in 2025). The implied 2026 EBIT margin is 57% against 61%.

Overall, despite the slow down in growth rates, these are still very impressive numbers. The stock trades currently at around 14x 2026 P/E. Still, investors don’t seem to be convinced that this is a good investment.

Maybe the “AI fear” is the driver here. To be honest, I find it very difficult for now, to get the conviction to invest into the currently very negative share price momentum, but I will keep watching and hopefully be able to attend the AGM in Munich in person.

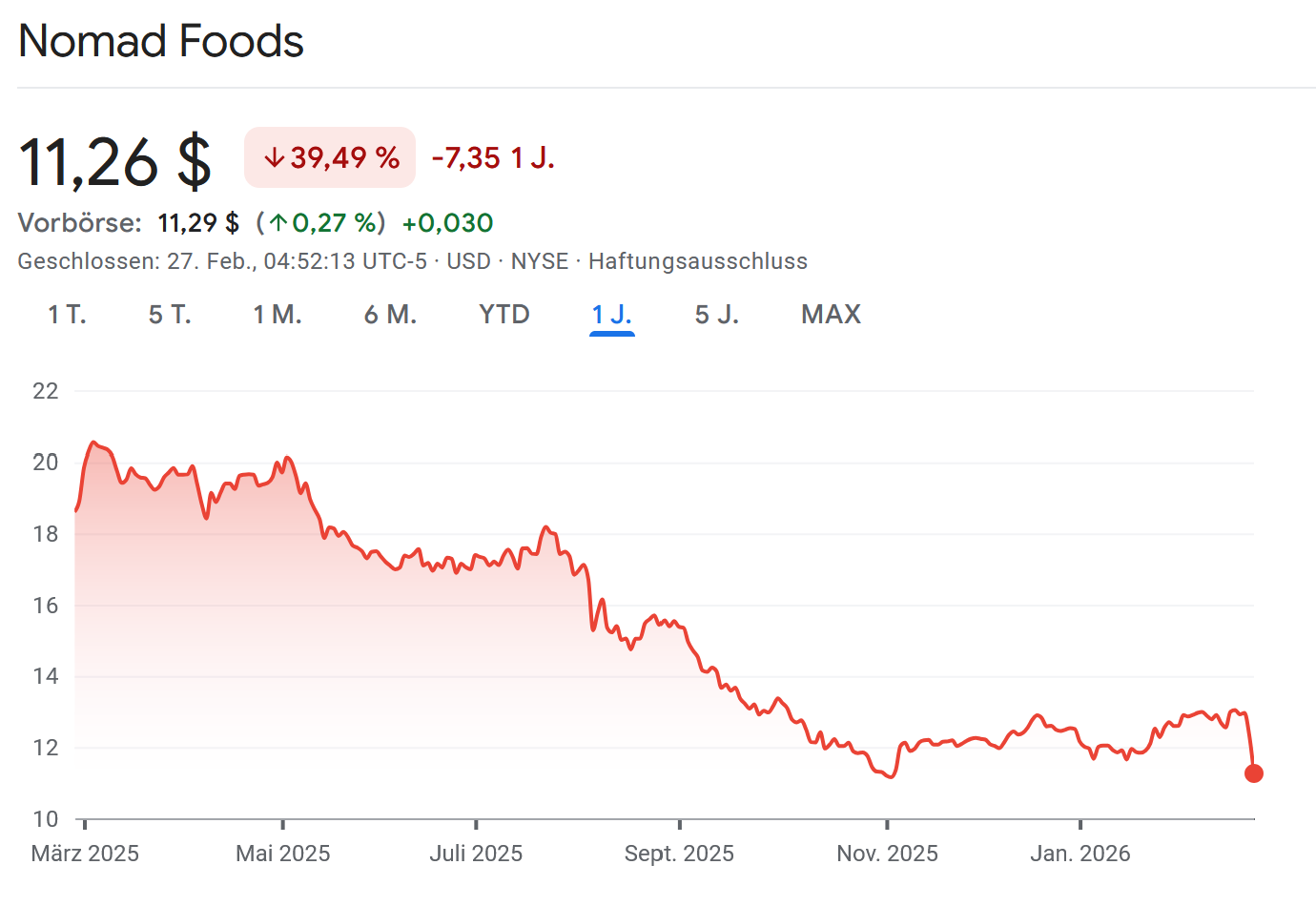

The picture was not pretty at all. Sales down, margins down, earnings down. Unadjusted they actually made a GAAP loss in Q4.

The guidance for 2026 doesn’t look much better either, but rather worse:

If we compare this to Frosta who have increased sales double digits, improved gross margins and only have shown lower net margins because of higher advertising spend, it is pretty clear that Nomad Food and especially the Iglo brand seems to be losing market share.

My gut feeling is that in Nomad’s case, the focus on Cash generation and share buy backs has maybe led to underinvestment into the brand which is not so easy and quick to reverse. Pretty much the same “playbook” and issues like Kraft-Heinz or Anheuser-Busch.

In the consumer space, the safer long term bets are those guys who invest long term into the brand and not the spreadsheet jockeys.

With a further EBITDA decline and current Debt/EBITDA of 3,8x, I am not sure for how long they can continue to pay dividends and buy back shares.

This one looks really vulnerable. For Frosta, there could be a msall risk that if Nomad gets really desperate and needs cash, that they start to dump their products into the market. So I think it makes sense to look at Nomad updates as a Frosta shareholder in any case.

This week was quite busy, with (at least) 5 of my companies releasing 2025 numbers, some more preliminary than others. Overall it was a “mixed bad”. Some good, some not so good. Let’s jump in:

“One important thing to understand with Frosta is that they don’t try to smooth earnings much, at least not to the upside. So you might always be in for some surprise either at the 6 month mark or annual report. Their guidance is usually very wide. Sometimes they decide to increase marketing expenses significantly which lowers profit in the current year but boosts revenues in the next year. In the long run, this has turned out very well for shareholders but for “weak hands” this can be a little bit unnerving.”

I guess this was once again such an event. Net income actually declined -12% in 2025. On the other side, growth of the Frosta Brand with ~16% and the ready made meals with almost 18% in 2026 is far above the market growth. So Frosta is taking significant market share. The dividend will remain at 2,40 EUR. They guide towards overall growth between 4-9% and a net margin of 4-8% in 2026 which is of course again very wide but implies that growth will continue for the Brand.

My timing of my Innoscripta write-up was a little bit unfortunate. Just a day later, Innoscripta held a conference call explaining the 2025 numbers. I think I need to better check the calenders of the companies I write about in the future….

I listened to the Call on Quartr. My main (and of course subjective) take-aways:

as a relatively new initiative, they develop a “safe storage” for R&D data

the arguments about LLMs and their limitations did not overly convince me. The arguments rely on today’s abilities of LLMs, but the question is how this will develop in 1,3 or 5 years. Especially I do not see that the LLM in the hand of a client itself is the competitor but competitors (especially other consultants) using AI to rapidly develop (cheaper) alternatives

Cash conversion (to EBIT) is currently around ~60% but they try to improve cash collection

They are bullish on the Government increasing the programs in general (regulatory tailwinds)

They claim that they see increasing revenue from the same clients which I find quite surprising. They didn’t however provide any concrete numbers

The clarified that the overall proces from application to cash collection is 9-12 months (3 months for innovation approval, 6-9 months for tax credits)

They claim that the “front loading” of 4 year applications seems not so significant

There is a clear seasonality that companies hand in filings mostly in Q4 in order not to lose credits for T-4 projects

Revenue in Q1 2026 should look good (whatever that means, not sure if they compare this to Q4 2025 or Q1 2025)

The currently do not consider M&A for international expansion but try to grow organically in 4 different countries (UK & US was mentioned)

The question if the 40% growth for 2026 is relevant was somehow confirmed but very indirectly. A “real” guidance should be expected for the AGM in April

Interestingly, the overall growth in the German Tax Credit market was +60% in 2025 which means Innoscripta’s growth is in line with the market and they want to grow with the market. More details again shall be provided at the AGM. The analyst mentioned that the market will grow less than 40% in 2026

The question how big the “4 year front loading effect” actually is, they were quite evasive. They mentioned that there will be growth internationally and through “Software” and Tax Credits is described as a “Milestone” or “trojan horse” to get other business.

Cash usage: No additional cash is needed for growth. Buy backs limited due to limited liquidity but rather distributions.

Overall my impression is that at least 2026 should look pretty Ok, but further out it gets a little bit vague. International expansion is clearly more risky than increasing market share in Germany.

But overall it remains a very interesting and dynmaic company and I am looking forward to the Annual Shareholder Meeting which I hopefully can attend.

Just a few days after my writeup, Wise published 6M numbers. On the positive side, with regard to Transfer volume, new customers and deposits, Wise grew strongly between 18-37% as we can see in this chart:

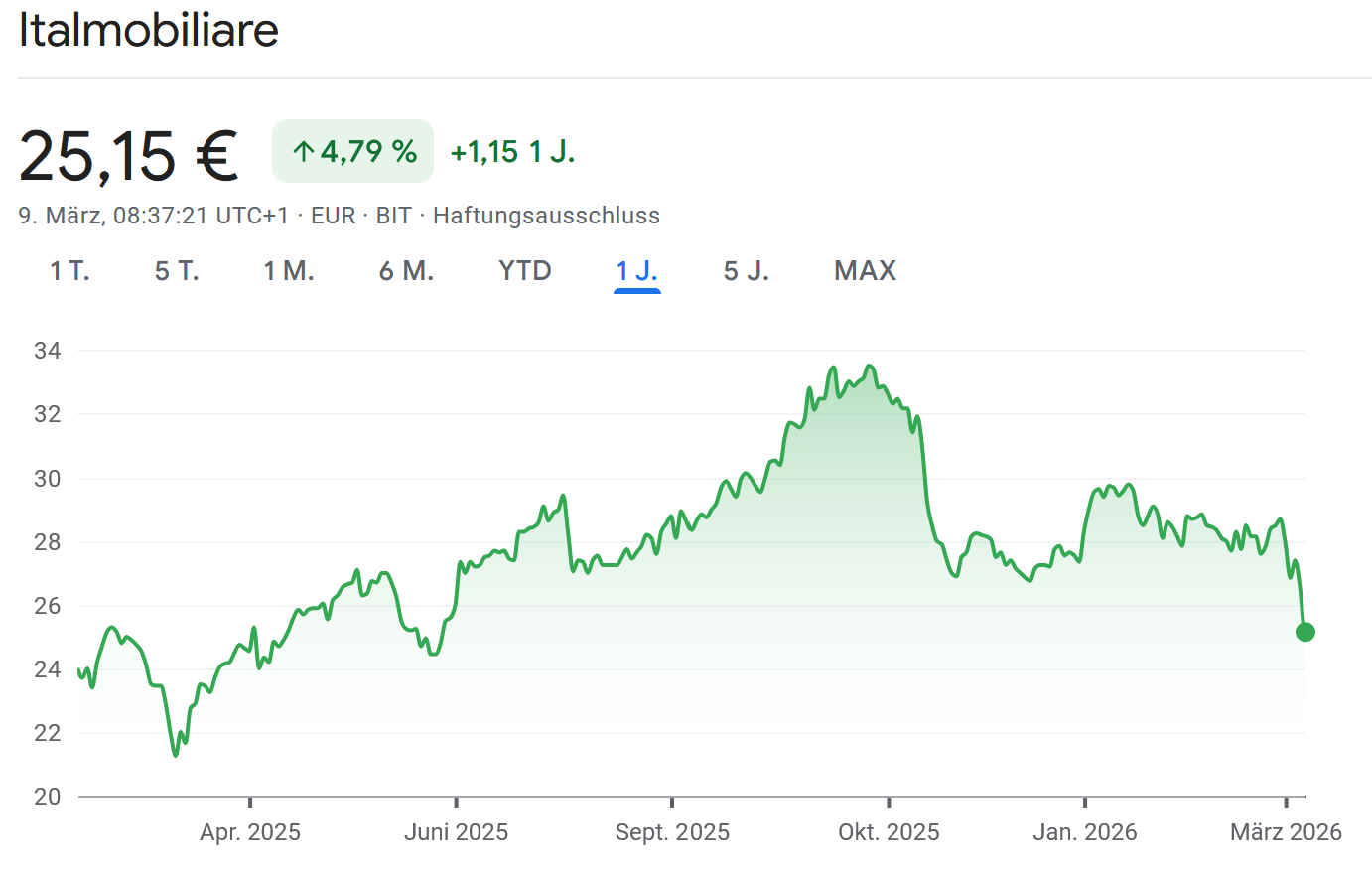

Italmobiliare published preliminary numbers already some days ago. The first reaction of the market was not so kind:

To be honest, I do not fully understand why the reaction was so negative. NAV development has been quite solid including the dividend as this chart shows:

Portfolio company SFS published 2024 numbers last week. Intitially, the stock reacted very negatively, dropping ~-9% only to recover fully by the time of writing:

The next 25 randomly selected company in my “Grand Tour Germany” project with 6 of them going onto my watch list. Enjoy !!

201. TTL Beteiligungs- und Grundbesitz AG

A 67 mn EUR market cap company that started as tech company in the dot.com boom, went bust and then reemerged as real estate company a few years ago. The company invests into real estate and real estate companies. As mentioned several times, not an area that I am much interested in. “Pass”.