AFter the introduction and some technical aspects in the first part, let’s look at how inflation is impacting pension liabilities. Inflation in my experience is something which is widely misunderstood when it comes to pension plans.

In many countries, especially Germany and UK, defined benefit pension plans work in general the following way:

Accumulation/active phase:

For active employees, each year the work for the company, they get promised a pension in relation to their current salary. So the longer they work and the more they earn, the higher the future pension promise. Companies have to disclose the assumption for the increase in salaries. Salary increases are a function of inflation and promotion. People who work a long time in companies and get promoted, usually increase their salary much more than inflation. Nevertheless it is fair to assume that in many cases, inflation will be reflected in salary increases.

Payout phase

Once an employee has retired, his pension payments are often linked to an inflation rate. In Germany for instance, those payments are linked to the German CPI (consumer price inflation) but with a minimum increase of 1% in any case.

Inflation Compounding

What many people don’t realize is that a permanent increase in the inflation level has a compounding effect, the adverse effect of course with decreasing inflation level. Roughly, an increase in inflation by a certain percentage has the same “sensitivity” as the discount rate.

Example Thyssen:

Thyssen Krupp for instance uses in their annual report 2012/2013 the following assumptions (Germany):

– Inflation rate for pension payments 1.5%

– Wage increases 2.5%

They show that a 1% change in the discount rate will change the pension liability by around 920 mn EUR. With a current net pension liability of 6.2 bn we can “reverse engineer” the duration of the liability simply by dividing 20/6.2 bn ~ 15 years.

This duration can be used both, as a simplified multiplier for changes tinterest rates and changes in assumed inflation rates. For instance if one assumes 2% instead of 1.5% as future inflation, the pension liability would be 15×0.5%=7.5% higher than it is shown on the balance sheet.

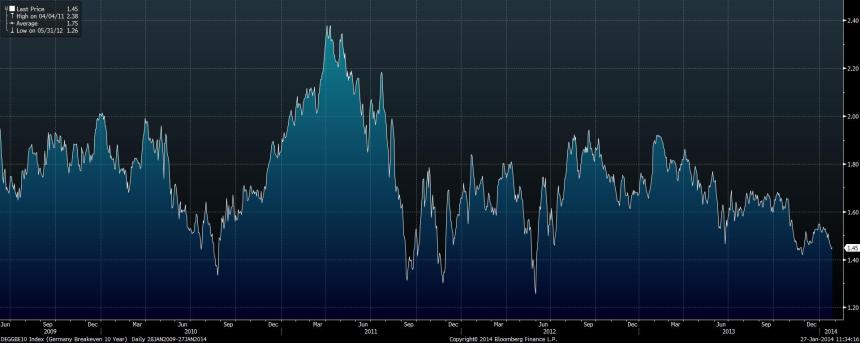

Inflation expectation vs. break even inflation rates

Many people especially here in Germany do think that we will see higher inflation going forward. I would not base my inflation expectations on subjective opinions but on observable market prices. Luckily we do have observable market prices for inflation: So called “inflation break even rates“, i.e the yield differences between nominal bonds and inflation linked bonds of the same issuer with the same maturity.

In order to adjust for inflation, one should always use those break even rates, as they are the best (and actually traded) proxies for inflation. Let’s look quickly at German Break even rates:

So we can see that currently, the break even rate is very close to the actual assumed inflation rates for Thyssenkrupp and we do not need to adjust for this. However, when inflation rates would go up, we would need to adjust and the impact can be huge. For further information about inflation linked bonds, there is a lot of stuff available, for instance here.

Deflation put

There is however one “small” problem with the approach above: The price difference between inflation linked bonds and nominal bonds includes the scenario of deflation. Normal, EUR based inflation linked bonds will have a floor at 0% inflation, i.e. they don’t loose nominal value in a deflation scenario. German pension plans however have a floor at +1% inflation. If I would compare a German Inflation linked bond with a floor at 0% and one with a floor at 1%, the one with the 1% floor is clearly more valuable, which means that this put granted to the retirees is definitely worth something. Modelling inflation linked options is quite complex, so as a proxy I would use maybe a 2-3% top up for German pension plans in order to reflect this 1% “floor” granted to the retirees.

Common myth: Inflation component is not important as profits of the company and or nominal interest rates will increase with inflation

This is an argument I often hear: You don’t need to care about the inflation in pension liabilities, as the profit of the company will increase with inflation. A second argument is that if inlfation increases, interest rates will automatically go up and thus, offsetting the increase. Let’s tackle the issues one after another:

Company profits and inflation

Honestly, I think not many of us do really know how a period of increasing inflation looks like. In Germany for instance, the inflation rate was between 0-2% p.a. for the last 20 years, a real increase in inflation was experienced the last time around the date of the reunification in the late 80ties and early 90ties as this chart shows:

It should be clear from the past that not all company can simply pass inflation to customers and maintain (or even grow) profits. In my opinion, especially those companies with large pension liabilities have vulnerable business models, especially capital-intensive companies like Thyssen and Lufthansa. Software Companies like SAP for instance will be able to pass most of their cost increases to customers, but they don’t have an issue with pension liabilities anyway. Especially vulnerable in my opinion are utilities, where power prices in inflationary periods are often capped by regulators, whereas input costs often rise quickly

Inflation and interest rates

In the past, high inflation risks often went along with high interest rates, especially in the 70ties and 80ties. The relationship was mostly: Inflation spiked and central banks then had to increase interest rates in order to reduce economic activity and get inflation under control. This time however it might be different. Central banks all over the world have made it clear that the want higher inflation AND low interest rates in order to lower Sovereign debt burdens. It is not clear if they do achieve this, but I think it is also optimistic to assume automatically higher interest rates in the future if inflation picks up.

Quantifying inflation risk pragmatically:

If we look at all the points above, it should be clear that having a liability which will increase with increasing inflation is worse than having for instance a senior bond liability with fixed payments. Even if we use and adjust for current break even rates, there is always the risk that inflation increases above that, especially now, with the Central banks clearly targeting higher levels. As we have seen above, companies with a very strong competitive position and low capital intensity, we can assume that they will be able to earn their margins even under increased inflation. A company which is very asset intensive (i.e. depreciation will be too low in an inflationary scenario), will however get a “double whammy” via increasing pension liabilities.

My proposal to quantify inflation risk would be the following:

– company where inflation has no impact (or even positive) on profit: No adjustment necessary

– company where inflation impact is unclear: 5%-10% “risk adjustment”

– company where inflation impacts business negatively: 10%-20% “risk adjustment”

Those adjustments are very rough proxies for the amounts which would be calculated by a fully fledged risk model but I think as a rough indication this is better than nothing.

Summary:

So summing it up: In order to reflect inflation risks in a typical inflation linked DBO pension plan correctly, one should make the following adjustments for a prudent valuation:

1. Check if assumed inflation rate is close to relevant “Break even” inflation rates implied in traded inflation linked bonds. If not adjust with the difference multiplied with duration.

2. If there is a minimum inflation “guarantee”, further adjust with a 2-3% upwards adjustment for the liability

3. Determine if the underlying business is negatively effected from inflation. In doubt, use a 5%-10% mark up, if there is a clear negative relationship, use a 10%-20% mark up to reflect the uncertainty compared to a fixed liability

Again, I know that this are very rough proxies and you don’t need to do that. But for a prudent valuation, especially for companies with large pension liabilities, it would be very optimistic not to make adjustemnts for inflation risk.