Hello Japan – A quick look at Berkshire’s new partner Tokio Marine

Background & Hello Japan

There was a lot of noise around Berkshire’s 10 bn participation in the Alphabet capital increase. However, at the Berkshire AGM, Greg Able mostly singled out the investment of Berkshire into Japanese Insurer Tokio Marine as a great investment.

He also mentioned explicitly that this was Ajit Jain’s idea. Many Berkshire Aficionados know of course that Ajit is behind the rise and success of Berkshires Insurance business.

So when Ajit is brokering a deal with Tokio Marine, I decided to have a first look into this company despite having never looked at a Japanese company more seriously.

Therefore “Hello Japan” for the first time on the blog.

Interestingly, I was not able to find any real write-ups on Substack, just a few very “light” ones mentioning the Berkshire partnership. The “Buffetologists” have ignored that one so far.

The Berkshire deal

The Berkshire Deal with Tokio Marine covers the following “legs” according to Tokio Marine’s webpage:

Strategic Investment: NICO acquired a 2.49% stake in Tokio Marine Holdings for approximately $1.8 billion, with options to increase its holding up to 9.9%. To my understanding, Tokio Marine sold Treasury shares to Berkshire.

Reinsurance Agreement: Berkshire entered a whole-account quota-share reinsurance arrangement, absorbing a portion of Tokio Marine’s globally diversified portfolio to help the Japanese insurer mitigate natural catastrophe and underwriting volatility.

M&A Collaboration: Both companies plan to collaborate on global M&A and strategic investment opportunities.

Technically, the investment is done by NICO (National Indemnity), not Berkshire. The third part is really interesting and unique. It will be interesting to see how this would look in practice.

Tokio Marine overview

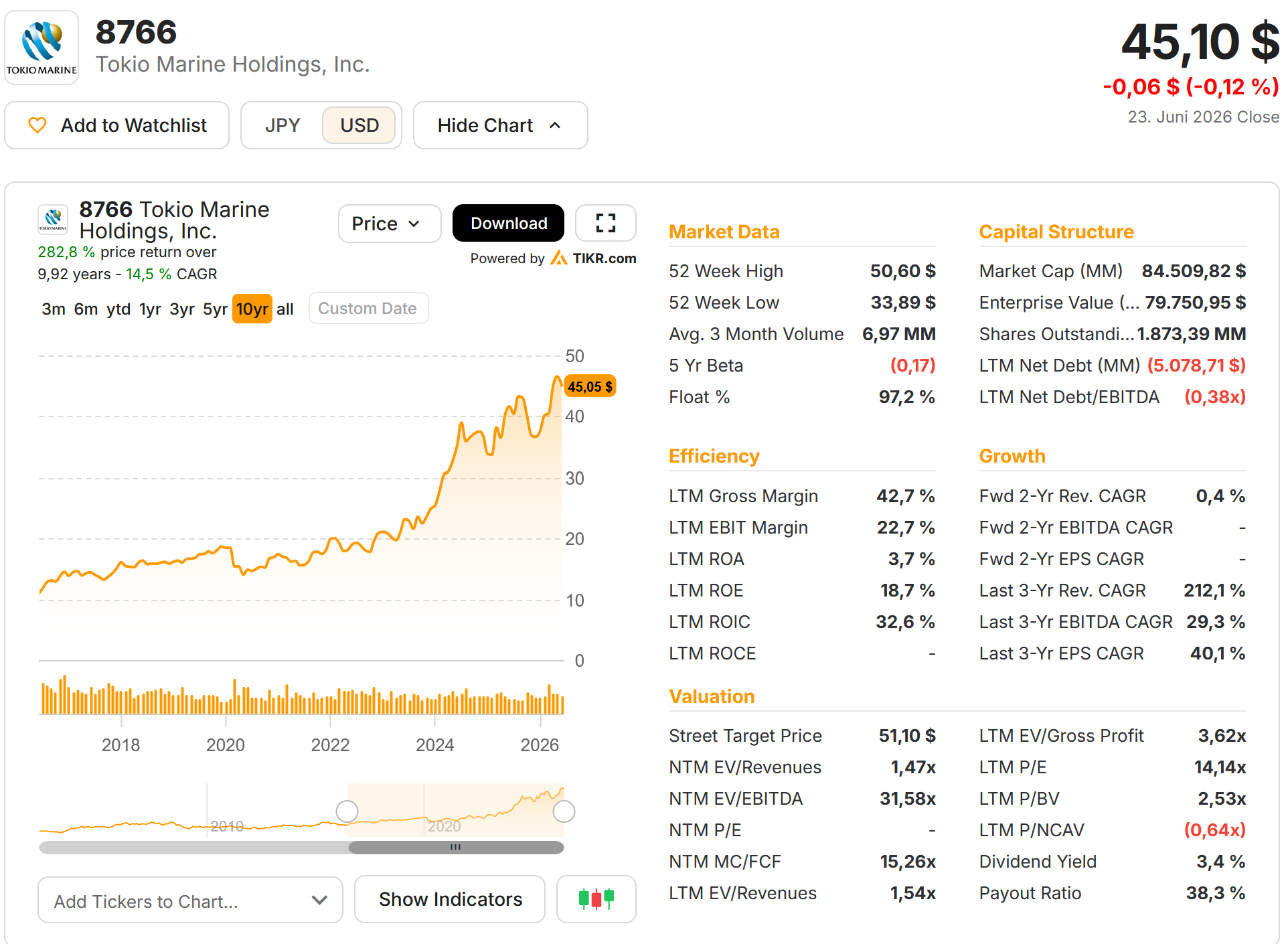

Looking at the TIKR overview, we can see that Tokio Marine has a market cap of around 85 bn USD, is quite profitable and trades at 14x LTM P/E. The 3% dividend yield is quite high for Japanese standards.

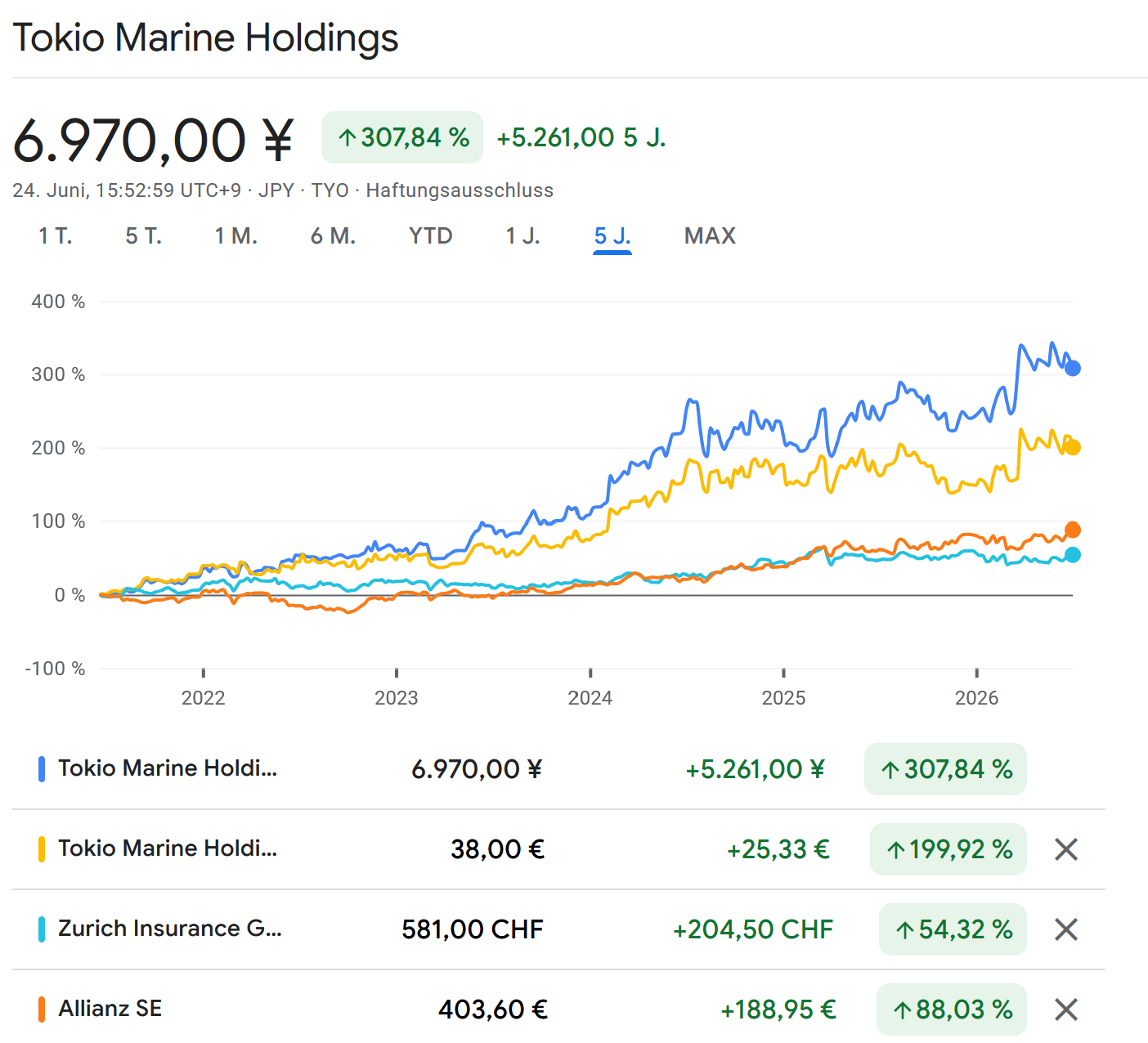

The share price has done very well in Yen. Although as this chart shows, part of the more recent performance is also due to the very weak yen. But the company still easily outperformed the European peers Zurich and Allianz by a wide margin over the past 5 years:

One interesting aspect is that Tokio Marine is widely owned. It was linked to the Mitsubishi Group (Kereitsu in Japanese) but they sold their remaining Mitsubishi shares in 2025.

They also stated a goal to sell all remaining listed equity investments by 2029.

The business

Tokio Marine has a surprisingly comprehensive Investor Presentation on its website.

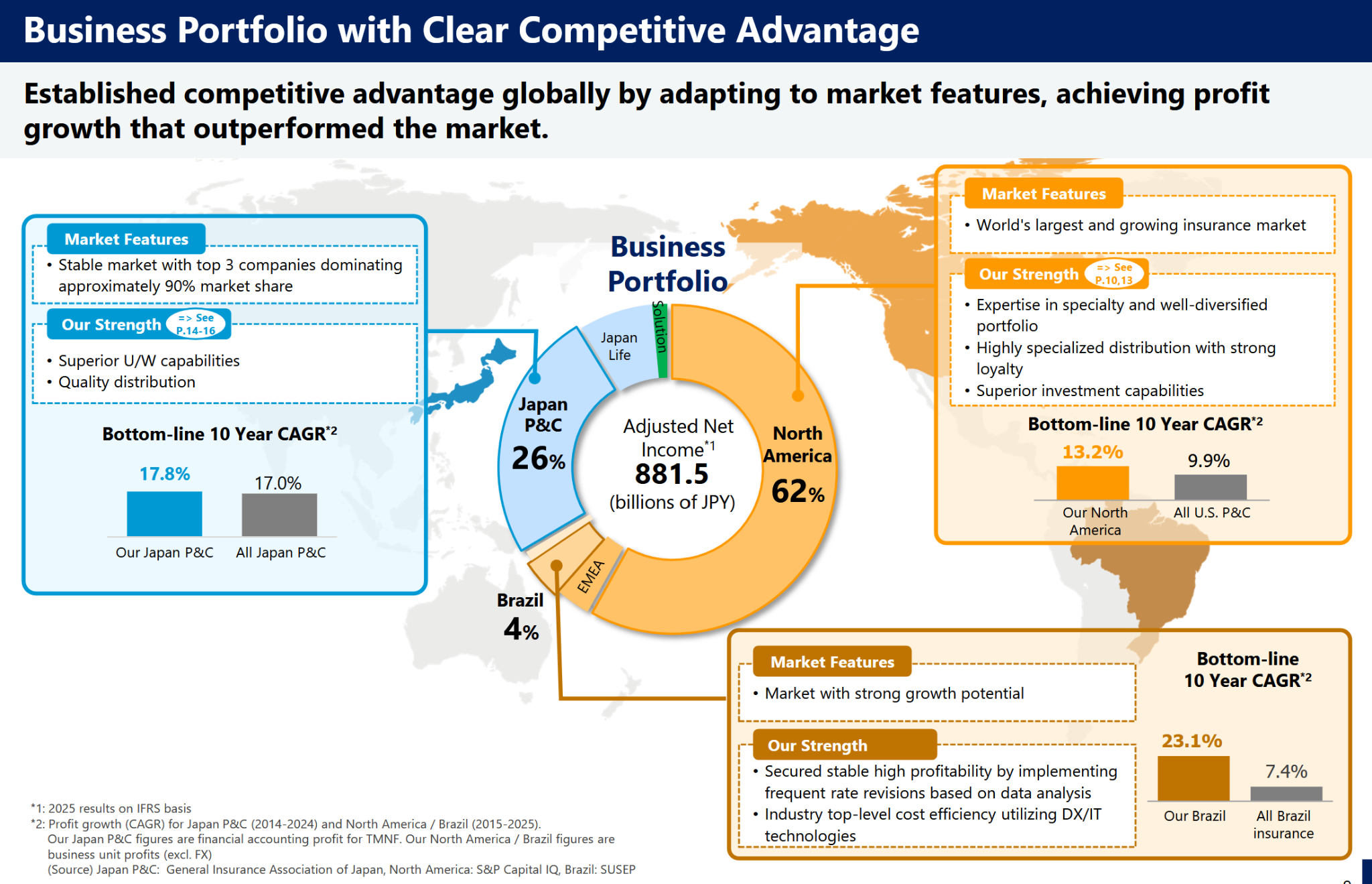

One aspect that really surprised me is that their business seems to be by majority in the US (measured by “adjusted net income”) as this chart shows:

So essentially, Tokio MArine is a US Specialty Insurer with a Japanese business. Looking at the mixed track record of Japanese acquisitions in the US, this looks rather smart in comparison.

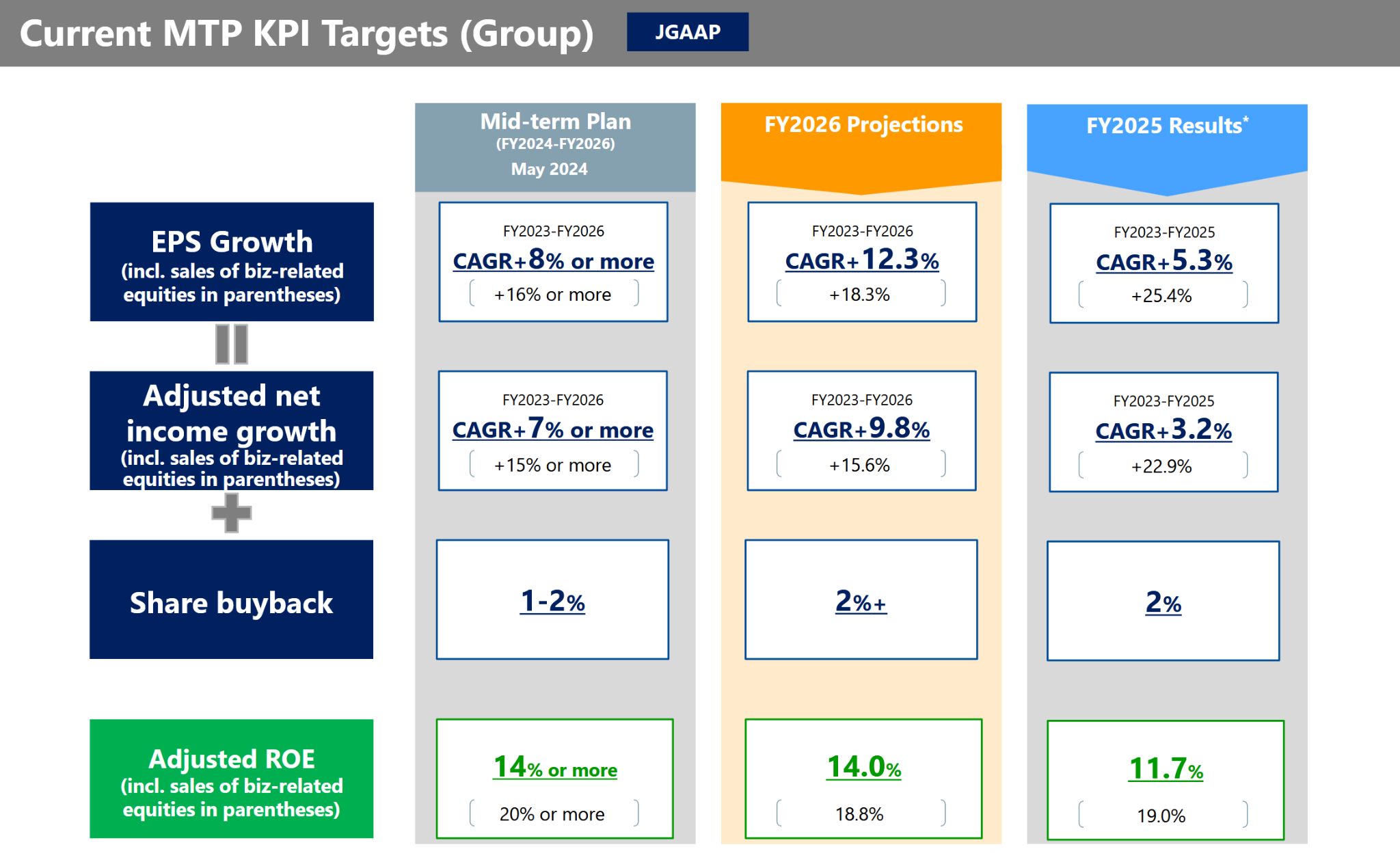

Business plan:

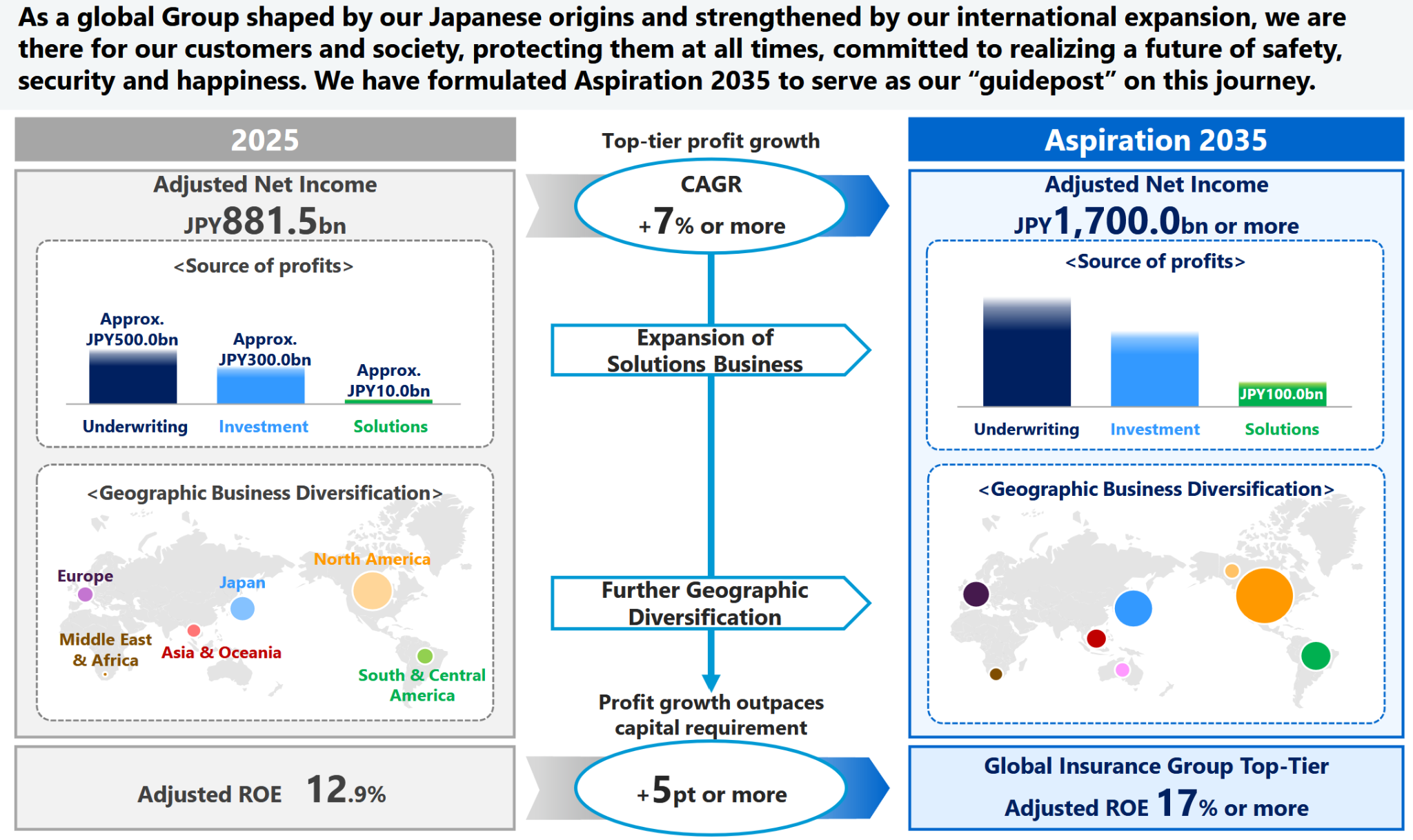

Their plan is to double Net income by 2035:

This is some more detail:

Of course, as insurance is not always predictable, this should be taken with a grain of salt, but putting out a 10 year plan is nevertheless a very positive aspect.

Switch from Japanese GAAP to IFRS

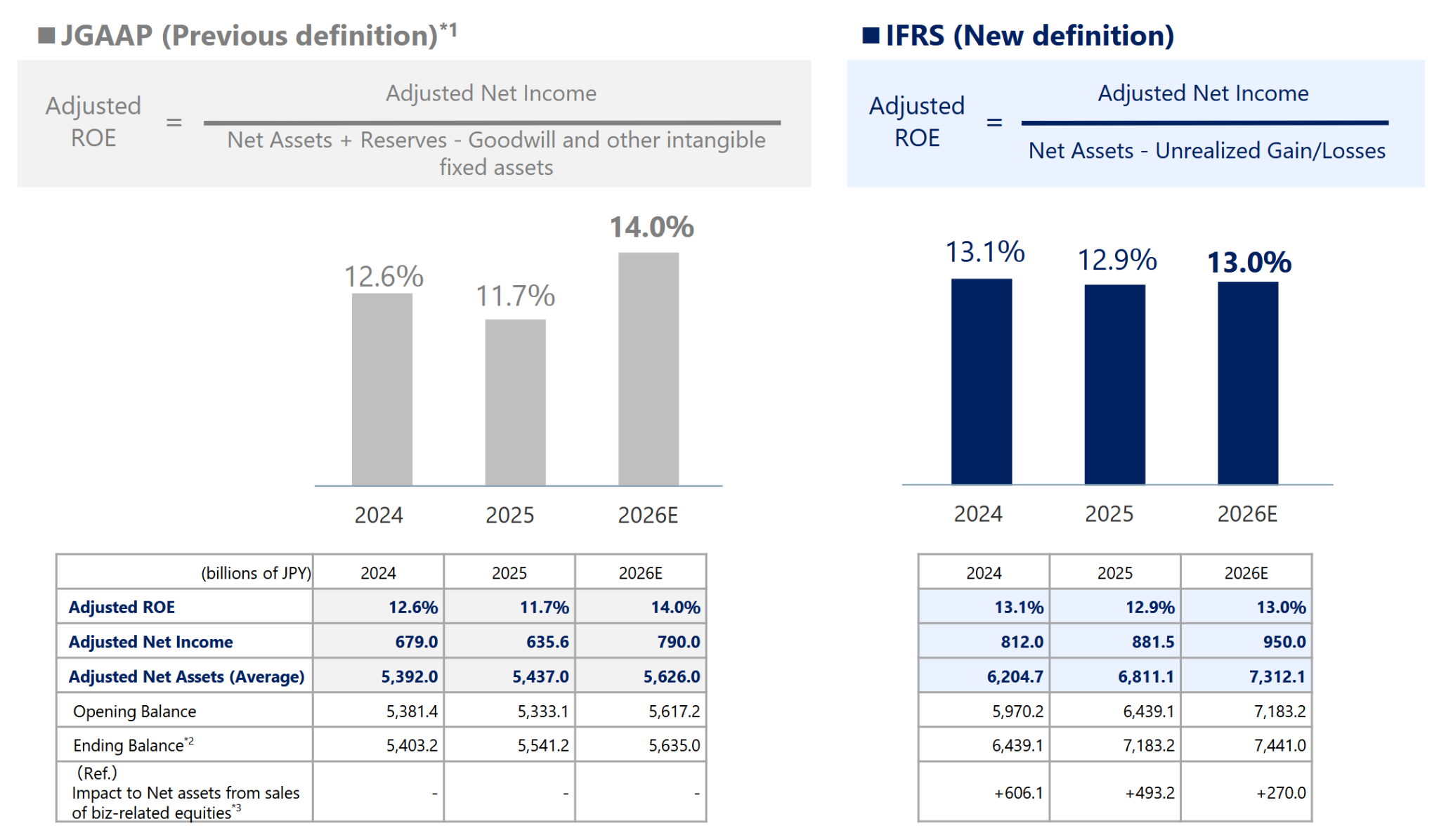

What makes things a little bit more complicated to analyze is the fact, that according to the presentation, Tokio Marine is switching from Japanese GAAP to IFRS in 2026.

They have this table which seems to indicate that IFRS profits are higher, but ROE lower, as net assets (Equity) is jumping after the switch:

Overall; Tokio Marine estimates that profits on an adjusted basis will be higher and less volatile compared to JGAAP.

Buying an Engineering design company

One pretty unique transaction was their purchase of an Engineering design company in 2025. That’s pretty unique among insurers.

I am really curious if and how this will actually develop in the next 2-3 years.

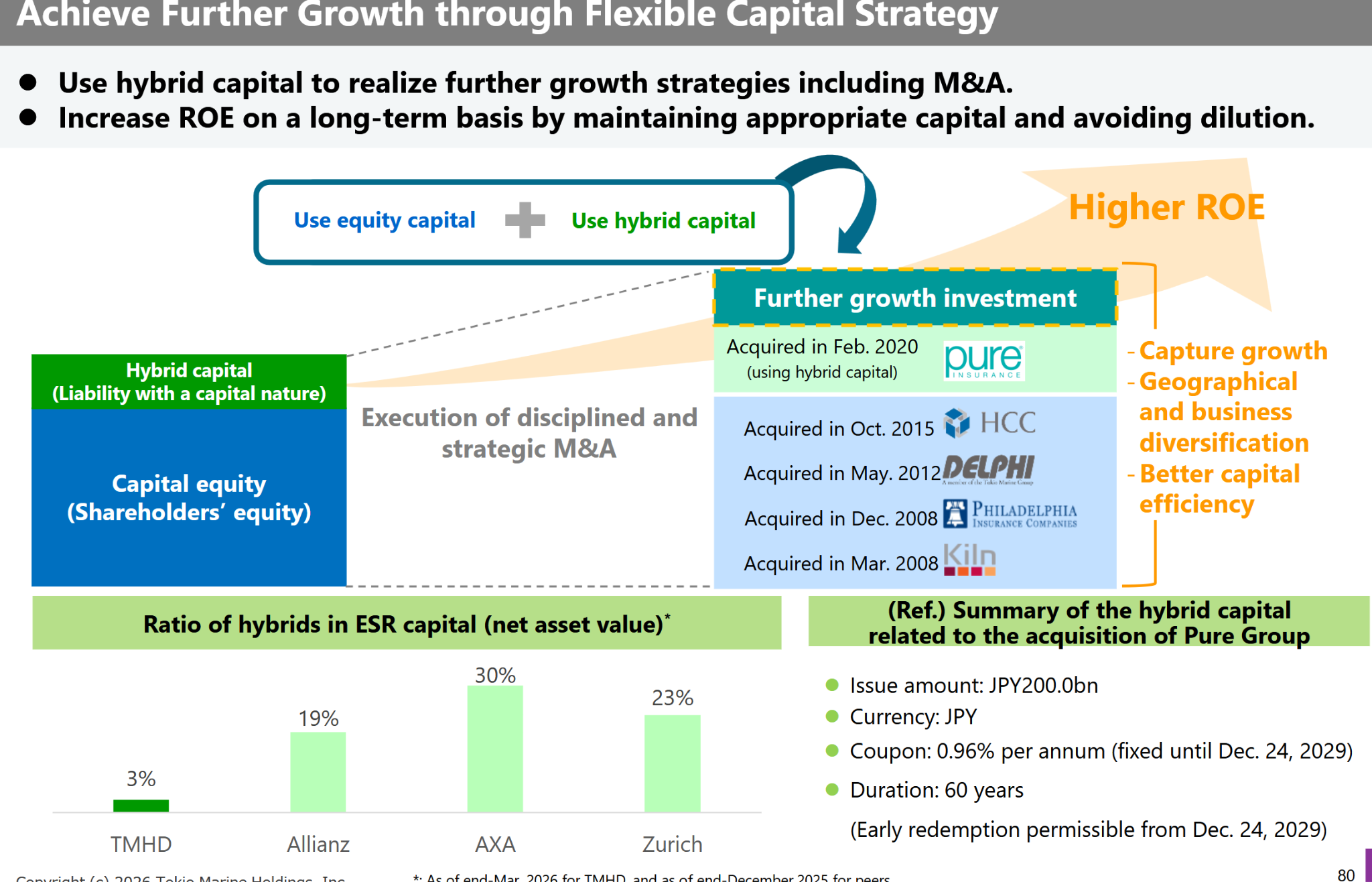

Capital optimisation

One of the “dirty secrets” of Insurance stocks is that a significant part of the Big Insurer’s capital base consists of bonds, so called “hybrid bonds”. Those are significantly cheaper than equity. This is Tokio Marine’s slide that shows that they have made little use of that so far:

Just getting to their competitor’s levels gives them a lot of flexibility with regard to M&A and/or share buybacks.

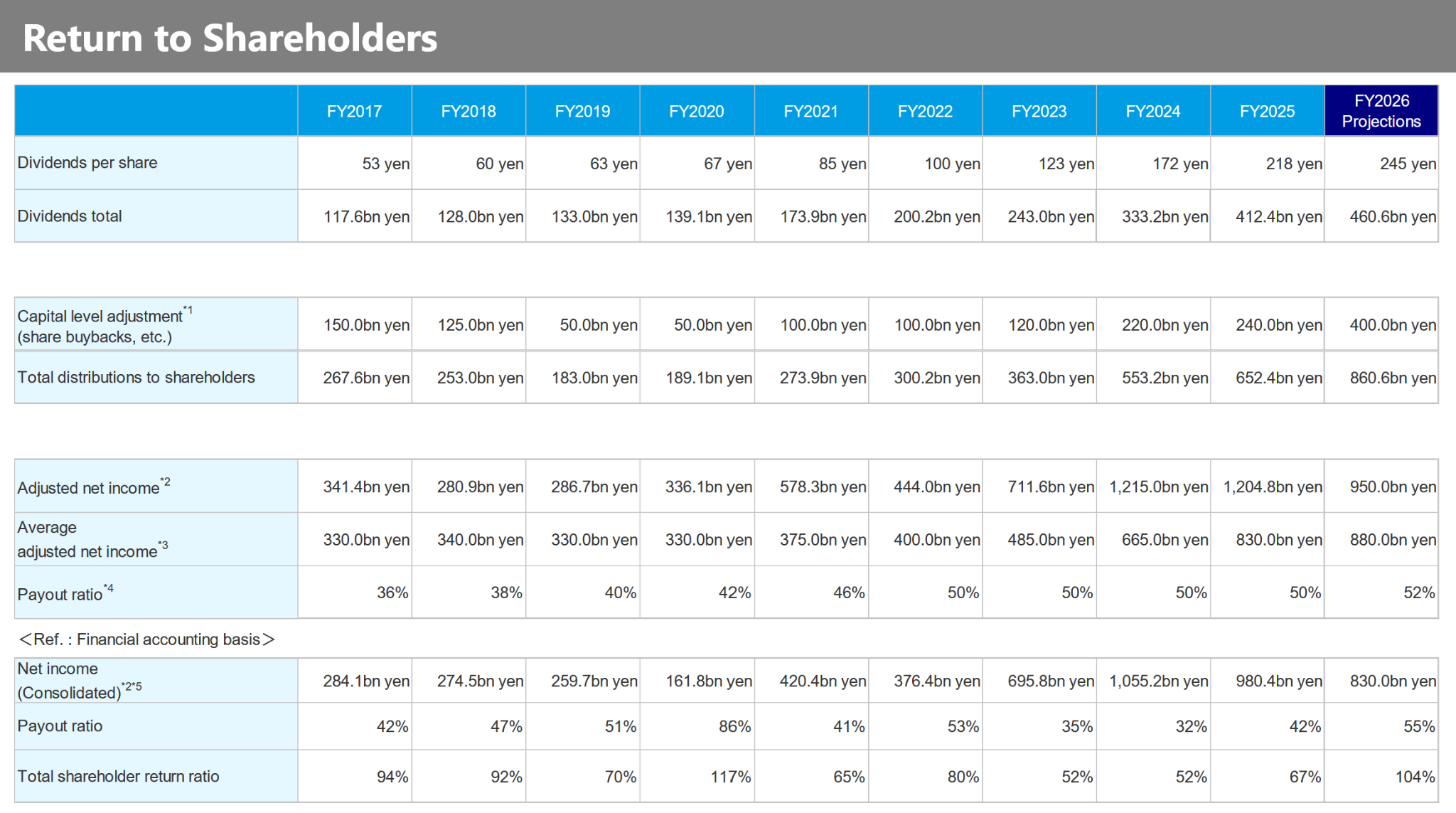

What’s interesting is clearly also how Tokio Marine has increased dividends and share buybacks over the past 10 years which can be seen in this table:

Return expectation:

A simplified return expectation for Tokio MArine would look like this:

Dividend yield + Buyback yield + growth rate

Taking Tokio Marine’s numbers this would result in:

3,1% + 1,5-2% + 7% = 11,6-12,1% p.a. without assuming any multiple expansion

This is not bad, but to be honest, also not super great.

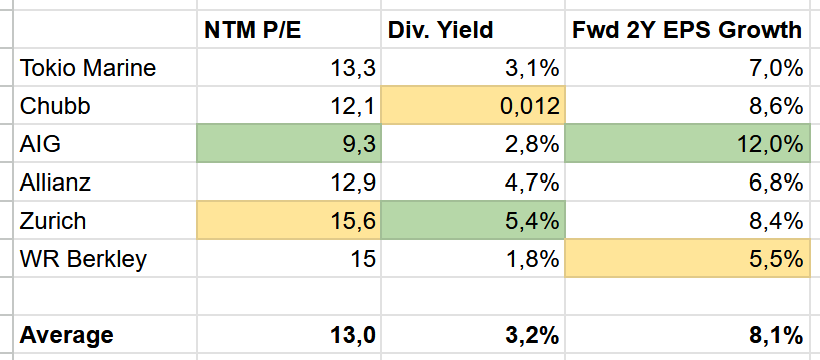

Here is a quick Peer Group table which shows that Tokio Marine enjoys an absolute average valuation in my subjective Peer Group:

The question or upside would be if Tokio Marine is really an “above average” player, then maybe they would deserve an above average multiple. Based on their very conservative capital structure, they should (in theory) be able to grow more than competitors.

To be honest, based on this quick check, I am not yet ready to give them an “above average” rating despite Ajit’s endorsement.

Pro’s/Con’s

As always, a quick summary of Pro’s and Con’s

- Ajit generally knows what he is doing & Berkshire Cooperation

- High capital flexibility

- Good business mix

- Shareholder friendly distribution/buyback strategy

- Good share price /earnings momentum

- Very good historic growth

+/- not super cheap, expected return below my hurdle rate

+/- Japan GAAP to IFRS transition

+/- complex business

+/- USD/JPY risk (as EUR investor)

- General Nat Cat exposure (famous Japanese Earthquake)

Summary:

Tokio Marine looks kind of interesting. Especially the fact that the majority of its profit comes form the US is a big surprise to me.

However, after the Berkshire announcement, the stock is not so cheap anymore.

So for the time being I will put it onto my “focus watch list” but not invest. I think it will be interesting to see how IFRS results will look like in 2026.

In any case, this shift from JGAAP to IFRS seems to be a very interesting item for Japanese insurers.