Camellia Plc (ISIN GB0001667087) -Exotic assets at a deep discount ?

Background:

Camellia Plc is a pretty odd company for UK standards. It is a conglomerate with interest in plantations around the world, as well as some engineering businesses, a UK cold storage business, a fish trader in the Netherlands and a private bank plus an art collection, a stock portfolio and other stuff.

Some UK blogs have covered Camellia like Richard Beddard and Expecting Value.

Camellia seems to be a favourite among deep value or “assets at a discount” investors and as I do like strange companies (and conglomerates) , I decided to take a deeper look at it. Also as it is in the same sector as ACOMO makes it easier to get “into it”.

The stock:

The company has a market cap of currently 260 mn GBP . The stock hasn’t done much for the last 10 years or so

The stock trades below book value (0,8x) and Bloomberg tells me that EV/EBITDA is 1.

I usually start with cross reading annual reports and then making bullets what I found positive and negative

Positive:

+ new CEO, slightly more transparent reporting

+ long-term focus, decentralized structure

+ exclude biological asset gains in presentation

+ have a lot of “extra assets”

Negative

– pension deficit 40 mn net, 200 mn gross liability. Current economic pension deficit ~90-100 mn (my estimate)

– want to invest more in banking despite really bad track record

– “diworsification”, all other 3 segments have produced cumulative losses over the last 10 years

– Dividend increase from 2.23 mn GBP in 2002 to 3,56 mn in 2016 (+64%), Director Compensation from 0,7 mn in 2002 to 2.6 mn in 2015 (+271%) –> alignment ??

– Comprehensive income over the last 8 years only ~50% of net income

– very volatile Comprehensive income (pension, FX)

Quick & Dirty Valuation / Extra Assets

The valuation for Camellia is really difficult. They do have better disclosure now with regard to the extra assets plus what part of the cash is actually corporate cash outside the bank (the EV/EBITDA of 1 includes Banking cash).

One also has to adjust for the pension fund. Especially for UK pension funds, IFRS values are usually too low. As a rule of thumb adding 20% to the liabilities is reasonable. Since year and 2015, interest rates dropped (~-50bps) so that I would estimate the current economic deficit at around 90-100 mn GBP 40+(0,2*200) +(0,1*200).

One remark on pension in the UK: Other than for instance in Germany, there is a funding requirement in the UK. Every 3 years (?) there will be a review and the sponsor has to come up with a funding plan which normally should close the gap within 10 years. As a basis, they use actuarial values which are mostly at least 10-15% higher than IFRS values. So in the UK, a higher deficit will lead to higher cash outflows relatively soon. Depending on when they do thr review, one should not be surpirsed to see increasing pension contributions at Camellia pretty soon.

| Extra Assets Camellia | |

|---|---|

| Associates | 49,8 |

| Stock portfolio | 30,5 |

| Heritage Assets | 9 |

| Investment prop. | 15,6 |

| Corp. Cash | 65,6 |

| Total Extra Assets | 170,5 |

| minus Pension deficit | -100 |

| Net Extra Assets | 70,5 |

So my quick and dirty valuation would leave a valuation of (260-70) = 190 mn for the “operating” businesses.

Based on the historical numbers, I would value banking, engineering and logistics with zero.

The big problem now is: How much is the plantation business worth ? Over the last 10 years, the plantations had around 30 mn trading profit per year on average. However after accounting for FX fluctuations the profit was often a lot lower. Also the operating cashflow doesn’t reconcile well with headline numbers.

So if I use 20 mn as normal trading profit and deduct 25% tax I would end up with 15 mn normalized profit p.a. and in implicit valuation of (190/15) 12,7 times earnings for the plantation which looks fair.

Even if I use the stated 30 mn, I would end up with an implicit valuation of 8,4 times normalized earnings which is cheap but not super cheap for such a cyclical, capital-intensive business. Plus, in a structure like Camellia, a discount compared to a “pure play” of 15-25% would not be a surprise

Siegfried Holding AG

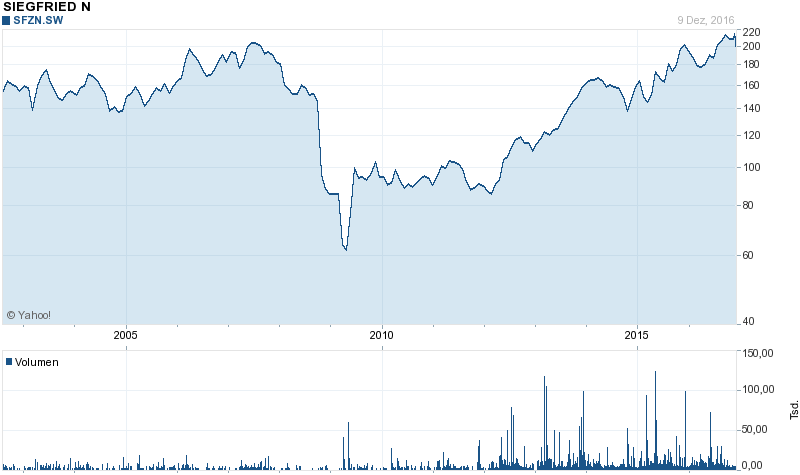

When I read the Camellia annual reports, I was surprised that Camellia used to hold ~1/3 of the shares of Siegfried Holding AG, a company I was invested in a long time ago as well. I don’t know when they bought the stake, but they sold it in full in early 2010. Looking at the Siegfried Holding stock price, this doesn’t look like such a smart move, especially if you call yourself a “long-term oriented” investor:

Overall, I am not really impressed with the asset allocation abilities of the Management. Maybe the new CEO is better, but for a Conglomerate like Camellia, capital allocation is key and I am not impressed at all.

Comparison Acomo – Tea trading

In 2010. Acomo bought a tea trading company (Van Rees) which I find interesting as Camellia’s main product is growing tea. They are buying tea in most of the countries where Camillia has plantations. In contrast to Camillia, they generated relatively stable net profits of between 3,5 and 4,5 mn EUR with net assets of around 20 mn EUR.

To me, trading tea looks much more interesting than growing tea from a business perspective. I wonder why they want to invest in Banking instead of going more “vertical” in their core business.

Summary:

Overall, Camellia is an interesting company but not an investment for me.

Based on my assumptions, the stock is valued relatively cheap but not super cheap. The main issue is in my opinion however the lack of observable capital allocation skills. Only a small amount of the plantation profit is distributed and the rest is reinvested in a quite intransparent and not very successful way, at least for the last 10 years or so. However, for a holding company /conglomerate without any “catalyst” on the horizon, good capital allocation is the main driver for value creation, which I don’t see at Camellia.

Maybe the new CEO is able to change that, but until further proof, I will watch this from the side lines. In comparison, I think Acomo is the better business and has the better management and business model.

Interesting and very posiitve news at Camellia: Banking will be sold:

Click to access 6475b8e9-d326-4f51-8718-3786228314d4.pdf

Have a look at Kakuzi

Thanks for the write-up. I had a cursory look at Camellia a few years back. The valuation looked as compelling as it does today, but then as now there was no real plan to unlock that value. The majority owner is a charitable foundation, which does not seem to be in a hurry. Any thoughts on whether that might be changing?

I don’t think that the setup with the foundation will change. Although I did not do any deep research into it. I don’t know who is behind the foundation. Maybe some of the readers know morr ?

From a quantitative only not business analysis standpoint, it is interesting to note that Camellia has 9 Piotroski score using TTM financial statements.

I guess the Pietroski score uses net income, not Comprehensive income. Which are 2 very different things for Camellia.