Short cuts: Provident Financial, Topdanmark

Provident Financial

Wow, that was fast. In November I looked at the stock but luckily dismissed it. This is what I wrote back then:

However for me, despite I do like financial companies, I don’t want to invest into a company which in my opinion runs an ethical questionable business. Some might argue that Lloyds Banking is not much different but I think that there is still a big difference between a well run main street bank and an aggressive subprime lender.

I do belive that in the long run, a company which takes advantage of clients has a higher probability to get into troubles than one which actually benefits the customer.

Although the “Crook” is out, the stock tanked an incredible -70% alone on Tuesday

So what happened ?

According to this Bloomberg article, not only did CEO Crook leave the company, but Provident also announced that most likely they will show a big loss instead of the previously planned modest profit:

The company now expects a “pre-exceptional” loss for the home credit business of between 80 million pounds ($103 million) and 120 million pounds. It predicted a 60 million-pound profit as recently as June, when it issued a profit warning as loan sales and debt collections plunged. Wolstenholme said in the statement that it will take “an elongated period of time” to turn the division around.

The doorstep loan business seems to be in total chaos already since some time.

What’s new is the fact that the UK regulator FCA also seems to have a problem with their growth engine Vanquis Bank. This seems to have started already in 2016 and clearly puts another nail into Provident’s coffin.

Is the stock now interesting ?

When a stock drops that much, many “value investors” think that it is automatically “cheap” as they look on trailing earnings (for the record: 4x 2016 earnings). In Provident’s case I would hesitate.

Firstly, the underlying, 100-year-old doorstep lending business seems to be totally screwed up and it is not clear if and how it comes back.

Secondly, there is no way to understand what is going on with their Vanquis subsidiary.

Thirdly, even without the home-made problems it is not clear how good subprime business will be in the UK going forward.

In the end, I am very happy that my “filter” worked in this case despite the many well-known investors present (Woodford, Marathon, Tweedy). Especially Woodford seems to have a really bad streak this year.

Topdanmark update

In March I wrote a post about Danish Insurer Topdanmark, which was in the process of transforming from a true “Cannibal” stock to one fully distributing its earnings as dividends. This is what I posted back then as summary:

On the other hand, I think the most interesting point will be to see if and how the Topdanmark stock price will react to a change to a dividend stock next week, which seems to be quite likely. This is one of the rare examples where a stock might go from one extreme (Cannibal) to the other (Full distribution). Of course we do not know what is already priced in.

For investors whose income is taxed, this is a clear negative. On the other hand, yield starved investors will find this more attractive.,

From my point of view, Topdanmark clearly has become less attractive. The “special” aspect will be most likely gone and speculating on a Sampo bid is maybe also not so interesting for the time being.

As expected, the AGM decided to switch from Share buy backs to dividends. The dividend policy was changed accordingly:

Future earnings distribution policy

Topdanmark’s Board of Directors has adopted an earnings distribution policy according to which earnings distribution will take place via annual distribution of dividends. Distribution of dividends will take place immediately after the AGM.The dividends will correspond to a pay-out ratio of at least 70%.

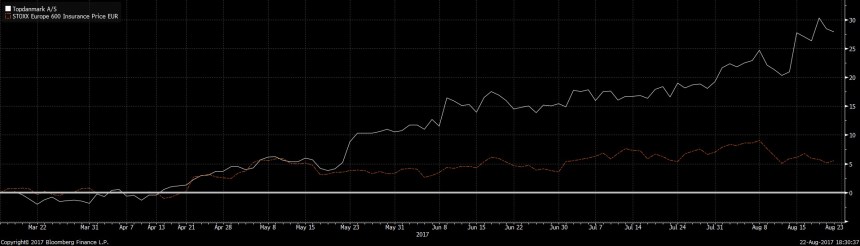

So what happened with the share price ? Let’s look at the chart:

Since end of March, Topdanmark outperformed the European Insurance sector by +25%. !!!

Results in 2017 were quite positive although mostly driven by lower claims but I don’t think that this fully explains the stock price movement.

To me it looks like that in the short term and in the current yield starved environment, investors seem to prefer the dividend yield compared to the ecoenomically better share buy backs which I find very interesting. It will be interesting to see if there will be more such “conversions” towards dividend payouts.

http://www.cityam.com/272483/why-we-bought-provident-financial

to be honest i found this article quite weak in real arguments.

Neil Woodford would disagree with you.

But he also mentioned Provident would make £80m despite the lenders losing £9m per week in sales or over £400m in a year and stating it would make a financial loss for the year. He also projected that in two years, the company would return to pre-tax profits of over £300m by 2019. That might be true, but given he was blatantly lied to by Peter Crook or some senior managers, I can’t understand why he wouldn’t admit his mistake.

Woodford is becoming too trusting of FTSE companies’ management or he doesn’t care about his client’s money.

This would not be the first famous fund manager who disagrees with me 😉

I would counter that ! I would rather say “typically, markets are efficient; however there are anomalies & exceptions”.

Topdanmark for me is just a sign that markets are not efficient in the short term.