Quick Updates: DCC (Intertek) & Wise

DCC/Intertek

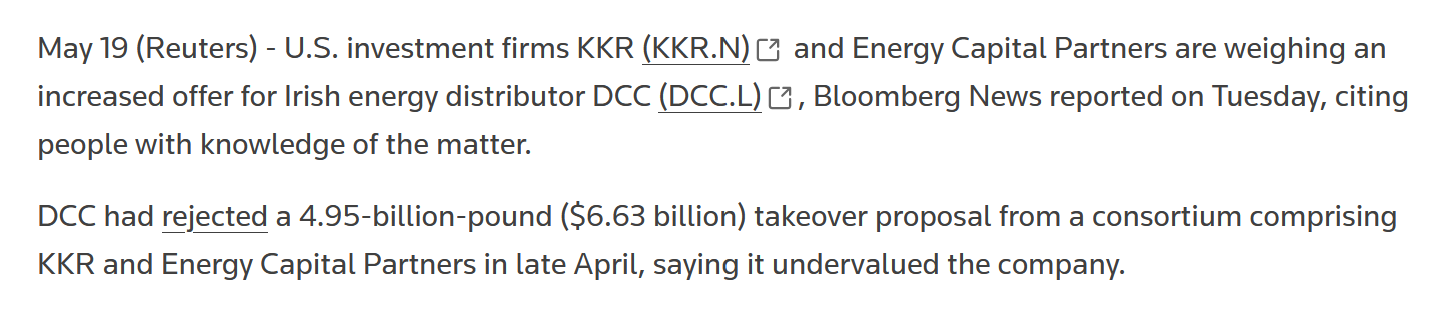

As expected in my post from a month ago, KKR now came back with a better offer after DCC’s board rejected the initial of 58 GBP per share.

This time, KKR offered 65,25 GBP in cash per share, plus a dividend of ~1,47 GBP per share to be received in July.

This is a 12,5% increase (ex dividend) from the initial offer. Less than I expected but it seems the board off DCC is already happy with this:

Having carefully evaluated the Revised Proposal together with its advisers, the Board of DCC considers that the financial terms of the Revised Proposal are at a level which the Board of DCC would be minded to recommend to DCC shareholders should a firm intention to make an offer pursuant to Rule 2.7 of the Irish Takeover Rules be announced by the Consortium on the same financial terms, and subject to the satisfactory agreement of the full terms and conditions of any offer and satisfactory agreement and execution of definitive transaction documentation.

Just to be clear here as a reader asked why the price did not directly jump to the offer price.: KKR hasn’t made a formal offer yet. This is so to say the “pre-discussion”.

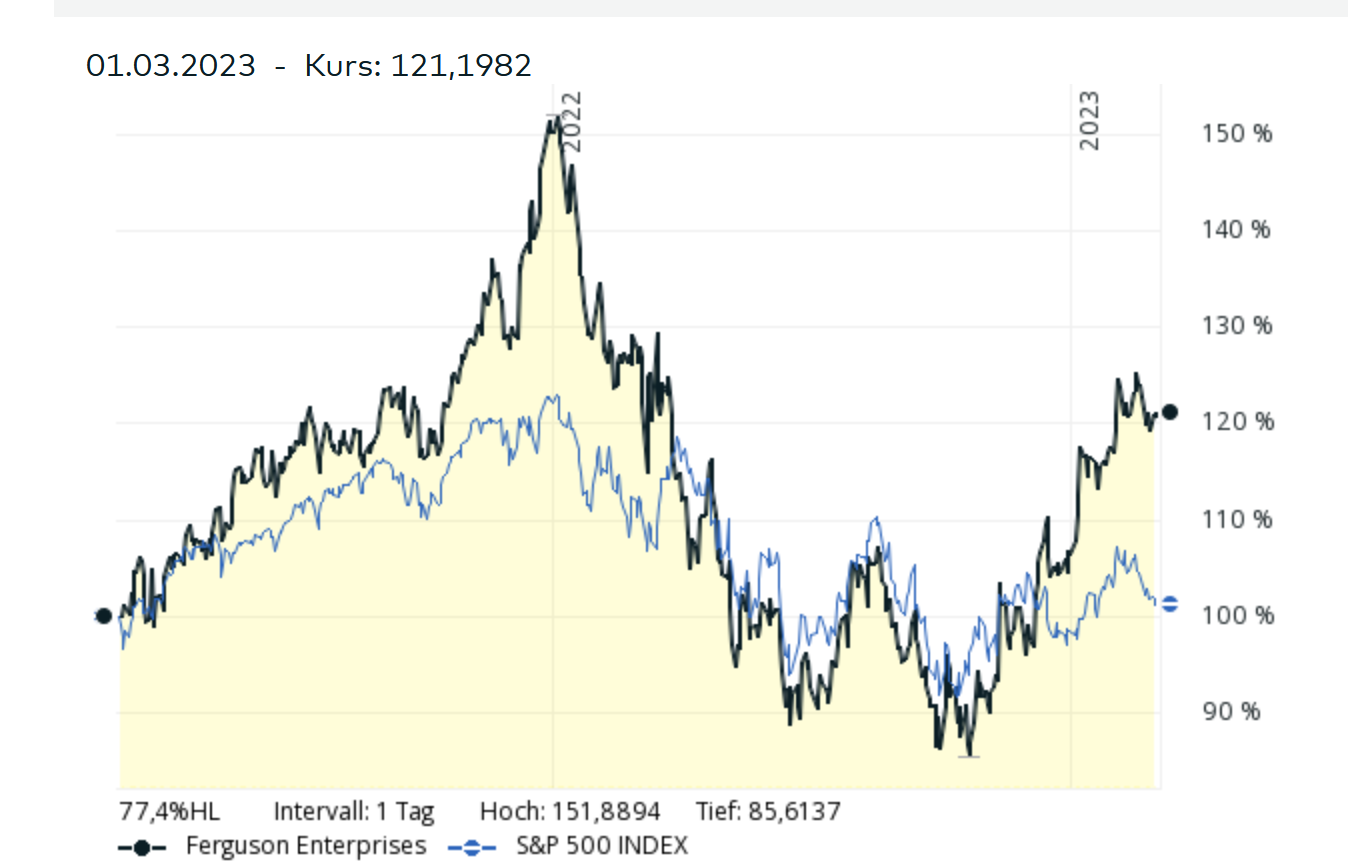

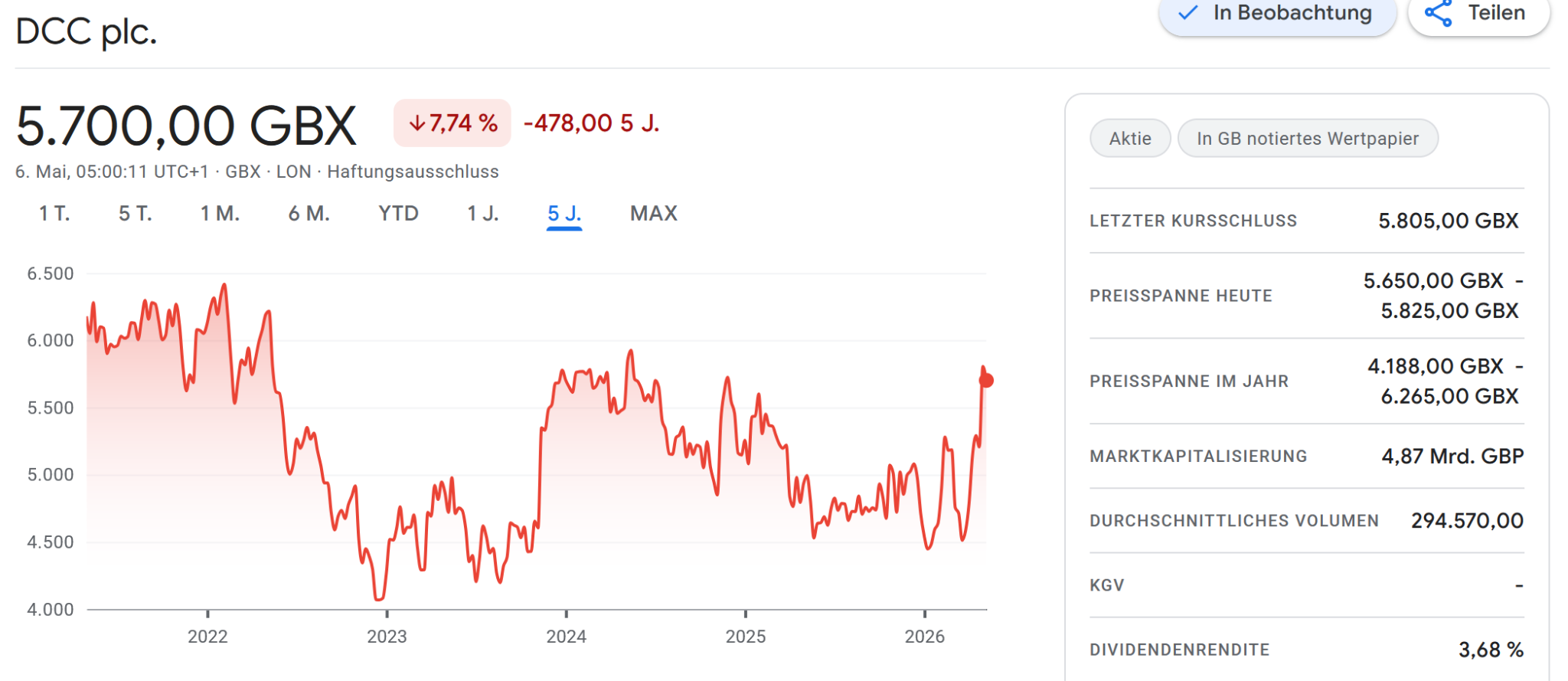

Looking at DCC’s long term share price, the offer price equates roughly the share price DCC had 10 years ago:

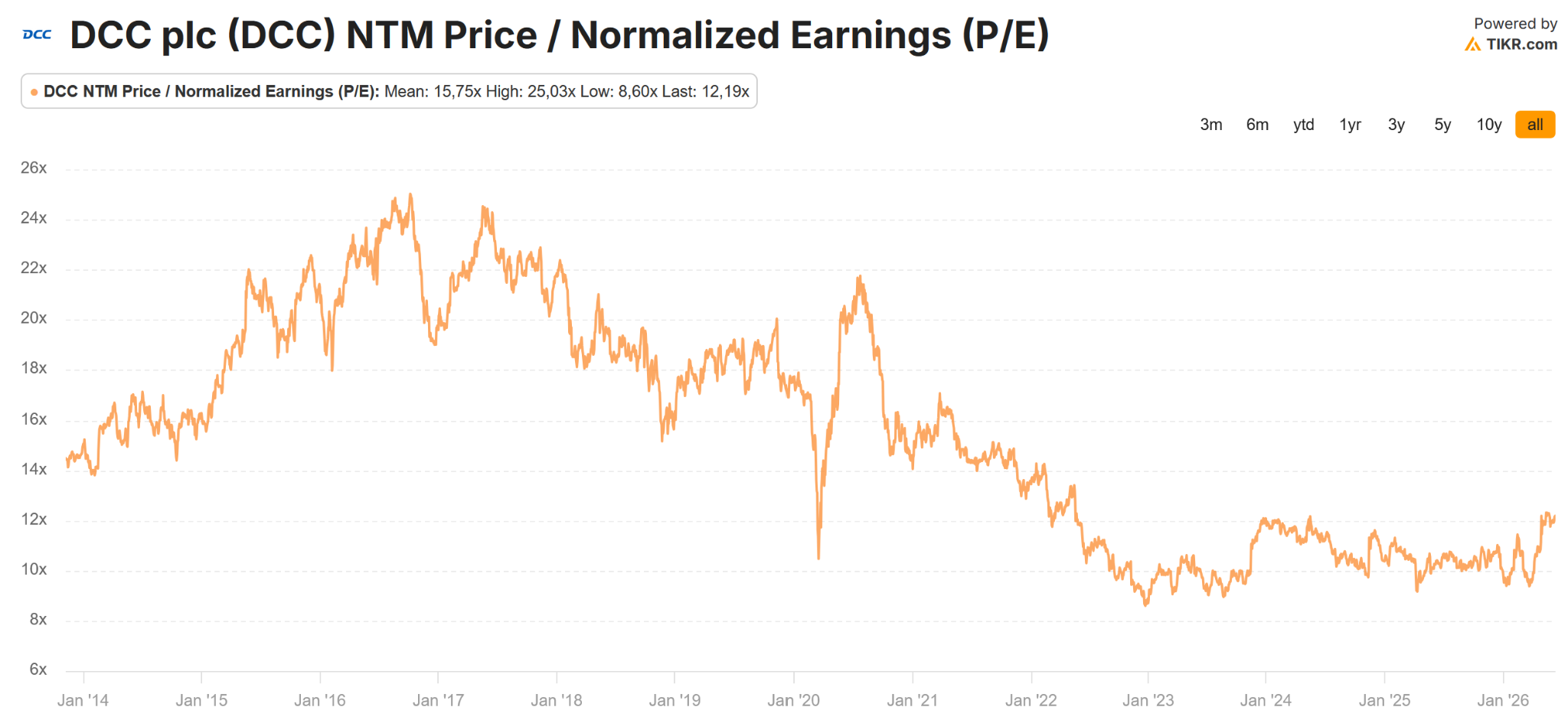

Looking at the historical P/E, we can also see that 2026 was the period in time when people thought that DCC is a 24x NTM P/E business:

As DCC’s board seems to have already accepted the bid, the only further upside would be now a counterbid from another PE fund or a strategic buyer.

I am not sure how probable that is, but maybe not 0% either.

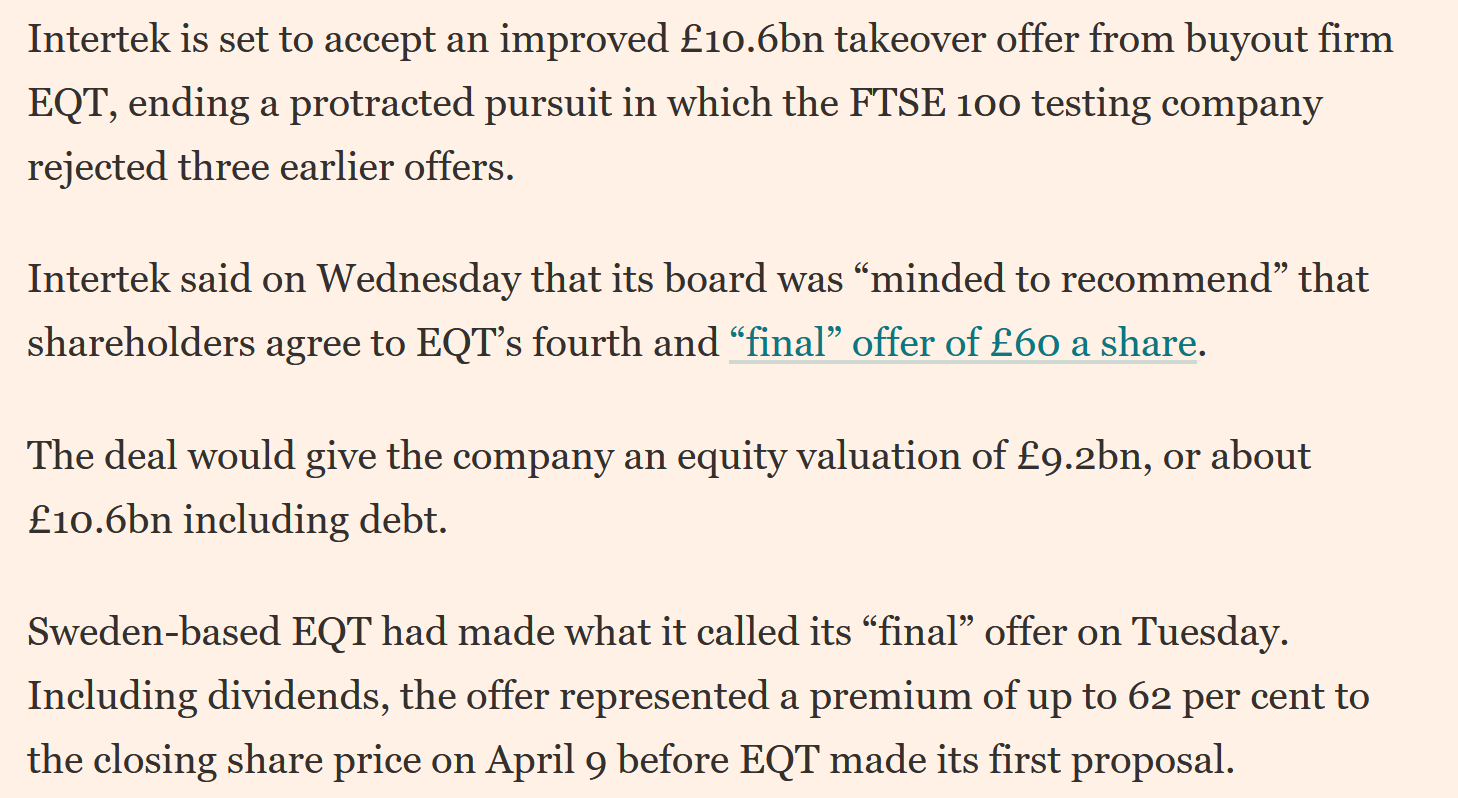

Intertek

As I had mentioned Intertek earlier, it’s spread to the (potential) 60 GBP plus dividend offer from EQT has tightened a little, because there was a rumour that Swiss based testing company SGS would be contemplating a competing offer.

Such rumours are actually not rare in these situations. Sometimes they are launched by hedge funds who might not want to wait until the offer is executed but get out close to the offer price long before that. In other cases, the rumour actually becomes true.

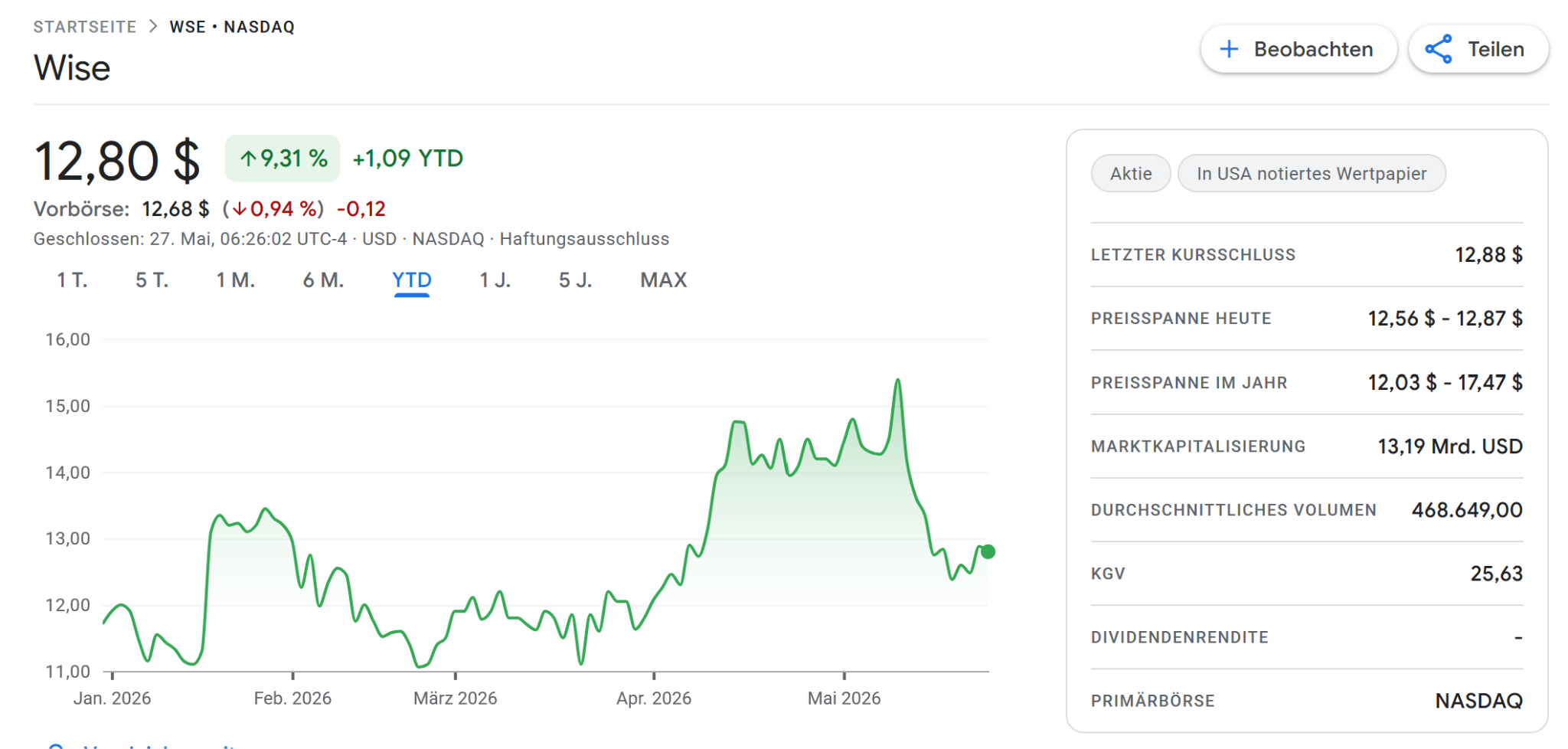

Wise Plc – What is the potential impact of the AML issue

A few days ago, Wise Plc shocked its investors, after it was revealed that authorities in Belgium are investigating Wise with regard to Anti Money Laundering regulations in an amount of 500 mn EUR.

The FT interestingly reported about a similar incident in Belgium in 2024, following the Russian invasion in Ukraine.

I think what is important to know is that the subsidiary in Belgium is not a tiny little subsidiary but basically handling all Euro transactions for WISE. I guess this has regulatory reasons.Unfortunately, Wise doesn’t report what percentage of its volumes have one leg in EUR, but it is clearly a very significant currency.

The size of a potential fine

The question that I had and tried to solve with AI is the following: Suppose Wise is “guilty”, what would be the fine they would have to pay and what or the other consequences ?

In reality, without making this to sound harmless, these kind of AML issues are not that rare, so there are precedents.

Here is what Gemini is saying:

- the maximum charge from a criminal perspective (if guilty) in Belgium is “only” 1,6 mn EUR

- the maximum penalty from an administrative side could be up to 10% of sales or in Wise’s case around 190 mn EUR

- In practice, the fines often seem to be a level of 1% of the volume. So overall, Gemini estimates the fine to be in the range 5-10 mn EUR. Which would be not so much.

Indirect costs: More compliance

The more critical part could be cost increases through additionally required Compliance functions. Gemini estimated that total compliance costs (which the estimate at 260 mn GBP at Wise) could increase by 30%, which would be around 80 mn GBP/100 mn EUR per year, which would be quite significant.

I think that is maybe an over-estimation, as so far, this only concerns the European operations. but still, 10-30 mn EUR per year could be realistic.

Additionally, we have now of course US shareholder litigation and potentially some reputational issues.

A further risk is that more compliance also maybe means less customer satisfaction and slower growth.

If we take May 29th as a reference, where the share price was at 9,35 GBP, as of the time of writing, the share price is down ~1,15 GBP or -12%. In monetary terms, Wise lost more than 1 bn GBP in market cap.

Payment in general has a difficult time in 2026

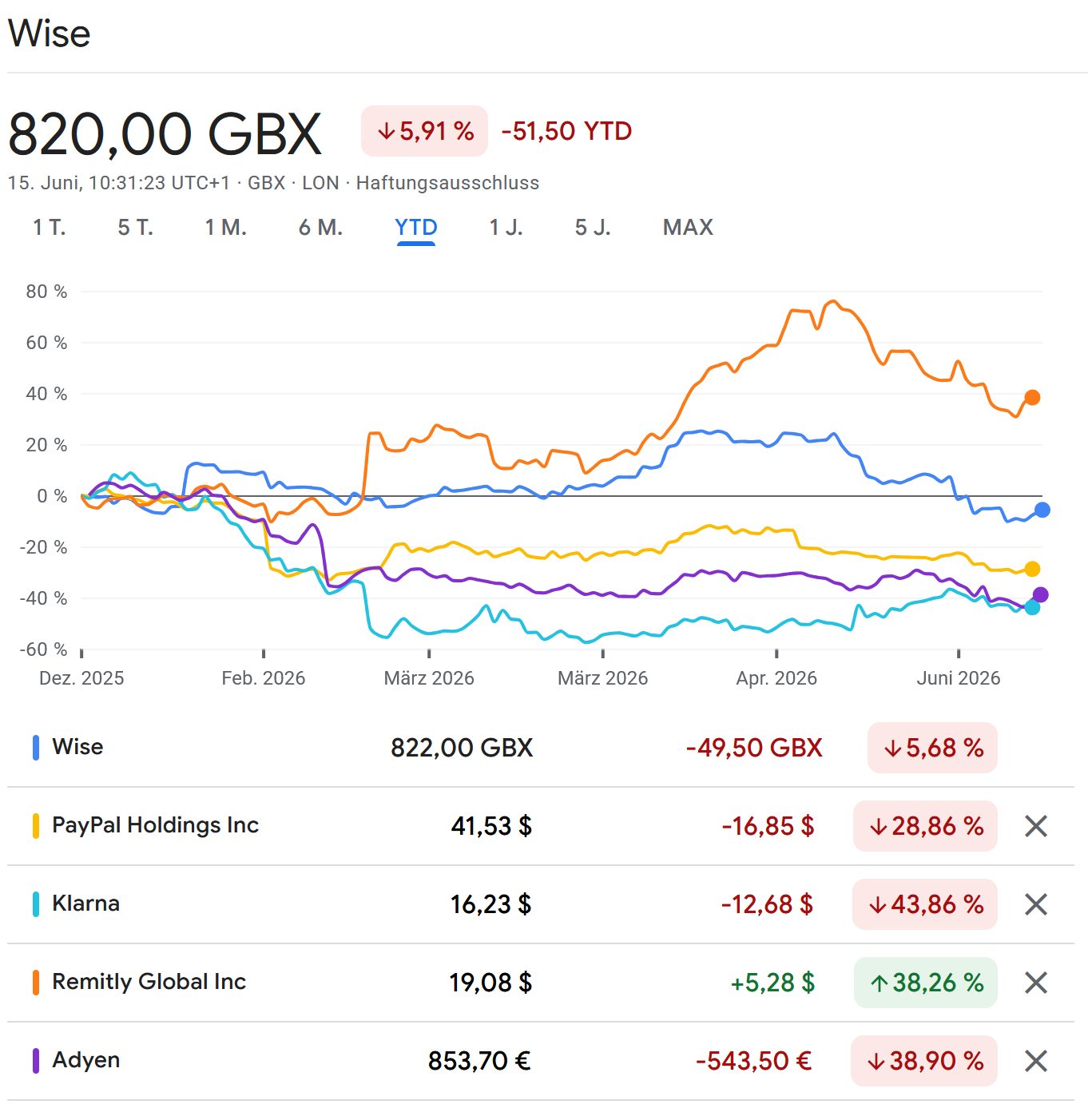

Another aspect is that payments in general are not doing that well in 2026. I have collected a small peer group here where Wise is still one of the better performers:

So where does that leave us with Wise:

For me, it is currently too early to say if and how this could impact Wise in the future. The share price drop clearly prices some pain and AML is always a risk for money transfer businesses, but I am not 100% sure if now is the time to increase the position. So I personally will wait for the next 2 or 3 quarters to see if growth keeps up and maybe add then.

If the share price falls significantly from here, I would rather sell and watch.