How to invest into Venture Capital – Listed Vehicles (part 1)

One upfront remark: I do not recommend to invest in Venture Capital right now. The market is clearly overheated and the asset class is known to be very volatile although Warren Buffett’s Todd Combs seems to just have discovered Fintechs.

This post is ment as a “long-term perspective” view on the sector and not a buy recommendation in the current environment.

How to invest into Venture Capital as a Private Investor

Famous VC funds

Venture Capital, i.e. the industry funding (technology) start-ups is known that almost everything depends on relationships.

It is no secret that a few funds like Sequoia or Kleiner Perkins have produced outstanding returns but these funds are “invitation only”, there are little chances even for larger institutions to invest in them and for individuals without direct connections it is more or less impossible to get in.

One remark with regard to the “famous” VC funds: The reason why they are successful is often not just “picking the right one”. The really good ones are very active investors that help their companies in many ways. From opening doors to actually hiring experienced managers for growth etc. etc. This is why the presence of a famous VC is often (but not always) the start of a virtues cycle: The VC lends credibility (and know how) to the start-up, the start-up becomes successful and the famous VC becomes more famous.

Direct investments into start-ups

There are already some market places that offer investments in start-ups. In general they can be divided into 2 types:

- Crowdsourcing (like Companisto or Seedmatch in Germany) where investments are “crowd sourced” via a service provider

- or match-making services like Angellist that try to hook up capital seeking start-ups directly with investors or syndicates of investors

The big problem with all theses services is the following: All the public available services do inherently contain a strong “negative selection” bias.

Almost all founders try to get into “famous” funds as I described above, this has many very positive aspects. There is absolutely no reason to choose not to bring a great VC on board if you can.

I would also recommend not to invest in general in anything within your circle of friends or friends of friends (unless they are professional VCs). Money and friendship in my opinion should be held separately. As both companies have been invested in the same start-ups, it was relatively easy to compare:

Kinnevik has long put more conservative valuations on firms it jointly holds with Rocket. On Wednesday, it cut its NAV figure for furniture site Home24, while lifting the number for other ecommerce businesses Westwing, Linio and Lazada.

However, Kinnevik’s valuations for Home24, Westwing and Linio are still well below those given by Rocket as of March 31

So what is the alternative —> Listed Vehicles ?

Again, within the “Listed” section of the stock market one has two options:

- direct investments into very early companies

- “Listed VC companies” that offer access to a portfolio of Venture companies

With regard to the direct path I would again be very cautious: As mentioned above, companies that go public very early are almost always “anti selected”. Like the Creditshelf example, many of these companies try to capitalize on a specific hype and are often extremely expensive compared to their non-listed peers. Additionally, future funding rounds are much more difficult to manage in a stock market environment.

Listed “Venture Capital” companies

This leaves us with listed companies that themselves invest into start-up companies.

Here is a list of Listed companies that I consider “Venture Capital” companies:

- Softbank

- Kinnevik

- Rocket Internet

- German Startup Group

- Vostok New Ventures

- Vostok Emerging Finance

- Augmentum

Softbank

I covered Softbank a few months ago with two posts (part 1, part 2). My final take away about the company was as follows:

At the end of the day, I think there might be some upside at the current level of the share price but not enough to fully compensate for the risk. So no investment unless it would turn out that the tax issue isn’t an issue at all.

Softbank is clearly doing things differently, however it is quite risky (lots of leverage) and some of the investments look outright stupid like investing 375 mn USD into “Robo Pizza”.

Kinnevik

I wrote about Kinnevik in December last year and started to build up a position last month. For me, Kinnevik is a combination of long-term investor / incubator /VC with a stellar reputation in the market. I consider the Governance to be very good and think that they are a very interesting long term play, despite their current large exposure to a single company (Zalando, which however in my opinion is a very good company).

One thing to watch is that Christine Stenbeck, the heir of the dominant founding family seems to sell some of her Family’s shares lately.

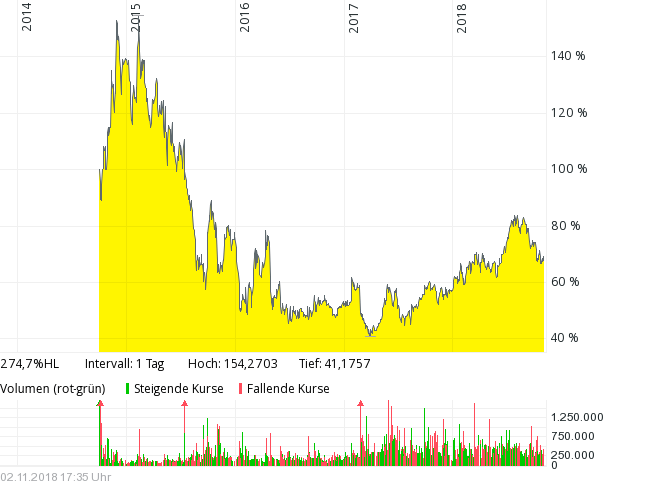

Rocket Internet

Rocket Internet is something like the German Version of Kinnevik, run by the Samwer brothers who made their name with copying business models from the US and rolling them out in high-speed across the globe.

Shareholders who bought the shares at the IPO price of 42,50 EUR are still down a considerable amount despite a rebound this year:

Although Rocket “pivoted” from an incubator to a more traditional VC model some time ago, I still doubt if they stock will ever reach its IPO price.

Interestingly, Rocket and Kinnevik were very close as Kinnevik believed in the future of E-Commerce and Rocket incubated a lot of promising E-Commerce companies including Zalando. Kinnevik actually was a shareholder in Rocket but sold the shares in early 2017.

Why did I not look at Rocket in more detail ? The biggest issue for Rocket in my opinion is that they have burned their reputation significantly over the past few years. There is no doubt that they incubated really good companies, however they also have burned through a lot of unfortunate ones. For instance this story in FT Alphaville is quite telling and there is no lack of stories of founders/employees who claim to have been screwed by the Samwers.

As reputation is almost everything in this business, this also means that Rocket will not have access to the best companies as they will surely avoid Rocket for some time to come. Racket also has to prove that they can do other things than E-Commerce.

Rocket has also a history of valuing its participations much more aggressively than for instance Kinnevik.

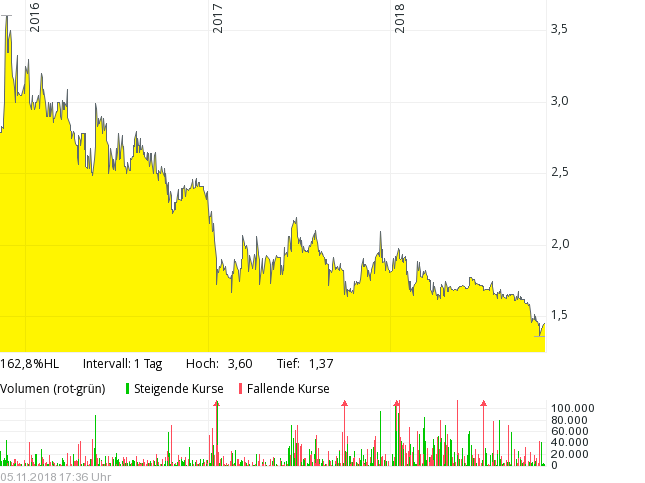

German Startup Group

German Startup Group is a tiny listed VC company which invests as the name says in German start-ups. Looking at the performance since their IPO in 2015, we can see that they did even worse than Rocket:

My impression (without a very deep analysis) is that German Startups is not a value add VC but rather a “spray and pray” kind of investor. They invest more or less randomly across sectors. In their last interim report interestingly they announced a strategy shift from VC investor to a kind of VC asset manager /platform.

In principle, this sounds quite interesting, but I am not sure if they can actually pull this off. They already needed to issue debt earlier this year as they have very little liquidity and the investors clearly have doubts.

To be continued….

Interested to hear your opinion on Vostok New Ventures. Trades at a large discount to NAV (no taxes on capital gains, etc…). Great possibility to invest in Avito, the third largest classifieds business in the world. Biggest shareholder in Vostok New Ventures: Ruane Cunnif Goldfarb. However, macro risk as they primarily invest in emerging markets (Avito / Russia, etc.)

Your question will be answered surprisngly soon 😉

Also take a look at two U.S. closed end VC funds: GSVC and SVVC. No insights to share, but they typically trade at a discount (assuming the NAV is accurate, etc.).

High risk, but have you checked out Vostok Emerging Finance?

My perception of Kinnevik as a “VC” was that Cristina Steinbeck had met the Samwer brothers, was convinced by their spiel and mostly invested alongside them and that given the mixed success of the strategy, she was pushed aside a bit.

Rocket Internet is not a VC per se. it is a copycat factory, launching their own start-ups replicating existing ones.

I am sure that you will have a look at GSV capital and Draper esprit (to be honest I am always a skeptic of permanent capital vehicle, the most efficient ones like Melrose return money to shareholders when they don’t need it).

Kinnevik has incubated companies long before (for instance Telcos) and teamed up with Rocket because they identified E-Commerce as a megatrend long ago.

Rocket by the way has more or less stopped doing copycat companies and has pivoted to a VC in 2017:

Apparently Kinnevik and Rocket want to float Global Fashion Group in 2019:

https://meedia.de/2018/11/22/global-fashion-group-rocket-internet-und-kinnevik-bereiten-milliarden-ipo-fuer-anfang-2019-vor/

I am not really convinced that they can pull this off, but it will depend a lot on the state of the market.

thanks for the heads up. Actaiully I think Global Fashion Group is not that bad. Westwing and Home24 were the harder IPOs in my opinion.

It also depends on the country you live in. The UK for example has Seed Enterprise Investment Scheme (SEIS) which offers great tax efficient benefits to investors in return for investment in small and early stage startup businesses in the UK. These kind of schemes can influence investment results quite a bit.

A listed fund like Woodford Patient Capital in the UK is an option as well.

https://woodfordfunds.com/funds/wpct/

This is arguably one of the worst funds on planet earth! And I read that the guy is heading to the court to defend himself… and that he can’t satisfy redemptions due to „the unlisted and/or illiquid nature of the funds‘ holdings“…and he maintained his high fee structure despite his poor performance….

OK I will stop here, you get the gig.

I’m not a big fan of this Woodford fund either. The investment strategy is so different from his past strategies that performed so well. It shows that even investors with a great track record should stick to their zone of compentence. Yet, the fund isn’t around long enough for me to say it’s “one of the worst funds on planet earth!”. Investing in early stage companies means you lose 8 or 9 and score big 1 time, which often makes up for all the losses. This takes time…. most investors aren’t that patience or cool headed. Plus, the fan boys of mr. Woodford aren’t used to seeing his funds go down 😉

Alternative is to invest in (small) companies around you, that you know and can control…

If you want loose money for sure, invest in VCs or even better in listed VCs.

Very deep insight, thank you so much. This means a lot to me.

Keep analysing; if you have found the golden nugget, let me know.

Why dont you start your own blog? You must be a genius with such reasoning….

@Nihil baxter

I am not smart enough to start my own blog, just smart enough to know that you will loose a lot of money in VC (except if you are tremendously lucky (ever considered playing poker? This will be far more profitable, if you are skilled)). I tend to try to jump over the 1-foot hurdles.

Dear John, discussing with you would be much more interesting if you would substantiate your arguments with data and or sources. However you are just claiming that you and only you know the truth. Such a discussion just doesn’t make Sense in my opinion.

Hey John,

It is not my place to intervene, but I was under the impression that you can lose money anywhere in the market. I checked VC returns over the last 30 years (since 1981) and they do, on aggregate, perform in line with equities in the US and the UK. A good portfolio should match large-cap returns on the long-term whilst offering a „differently“ correlated asset class.

I, for a matter of fact, do not touch a business that has broken even for the simple reason that I hate rights issues. (but I am probably missing out. Check out the softbank and vision fund latest return).

Most importantly, blogs such as this one have a singe purpose of identifying winners. Hence the backlash against your input (or lack of). How about „you are likely to lose money with X for y and z reasons, but why don’t you look at A, B and C instead“? that, I reckon would be better accepted and add to our body of knowhow.

Happy investing!

Interesting; which source did you use? How was the definition of VC (only funds or listed VCs)? Are the results before or after fees? Which geography was covered? How was survivorship bias dealt with? Which was the base currency? How were currency movements dealt with?

If you people do not believe me, may be Howard Marks is able to convince you:

“Probably the activity which could produce the highest expected level of elation for me might be cliff diving. I don’t like the bad outcomes, so I’m not going to engage in cliff diving. And similarly, the highest-returning investment activity might be venture capital investing, and somewhere in the probability distribution for any venture capital fund investment is the possibility that all the investments turn out to be valueless. So, if I’m a conservative investor, I’m not going to do that. And so, we can’t just invest on the basis of the probability distribution and the expected value. We also have to take our own tolerances and predilections into account.”

https://fs.blog/howard-marks/

Do you think Zalando is a good investment or a good company? I just see dodgy accounting and management selling shares as fast as they can.

What kind of dodgy accounting ?

I like it with some good insights for specially VCs

Thanks for that.

You may want to look into SPACs as well. I dwelled in this space a little while ago and understand that early stage investors have started listing vehicles as well….