All German Shares Part 13 (Nr. 226-250)

Another week, another 25er batch of “fresh” German companies. Again, there is a lot of “Garbage” but also some interesting “watch” positions. One of the candidates is German Startups Group which, in the meantime made it into my portfolio. I publish the “All German stock” Series with a certain time lag and if time allows, I dive deeper into stocks that really interest me a lot. So It can happen that I decide to invest prior to actually publishing the respective post…

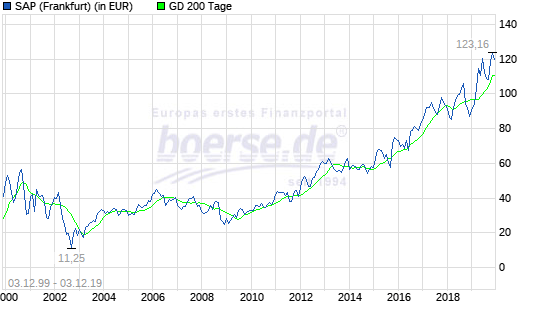

226. SAP AG

With 147 bn EUR the most valuable listed German company, leader in enterprise software with a steady increase in valuation over the last years:

Personally, I don’t like SAP that much,especially the capital allocation under the old CEO was questionable and the current PE of 42 seems to be rich for a large and mature software company. For me a “pass”.

227. VDN VEREINIGTE DEUTSCHE NICKEL-WERKE

Long term insolvent shell company with 20k market cap. Pass.

228. AFKEM AG

1mn EUR market cap nano cap with no observable business. “pass”.

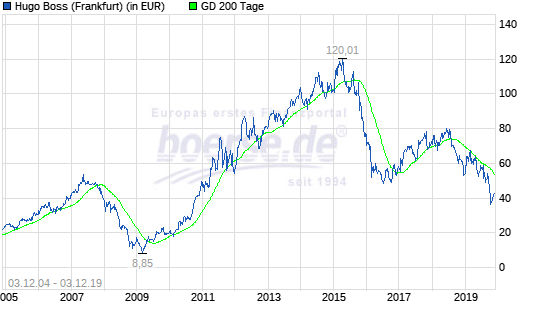

229. Hugo Boss AG

Hugo Boss, the iconic German fashion label, currently has a market cap of 2.9 bn EUR. The company has a quite interesting recent past as can be seen in the stock price:

PE company Permira invested in 2007, but never took the company private. They then managed to exit exactly at the peak in 2015. Since then, the stock lost 2/3 of its value. An iconic brand these days is clearly not a guarantee for profits.

The Q3 report shows that the main problem at the moment is the US, however the reasons given are not really clear (less tourists…). Anyway, as the stock looks cheap (P/E of ~14), I’ll add it to my “watch” list.

230. WKM Terrain und Beteiligungsgesellschaft

1.6 mn market cap company in liquidation. “pass”.

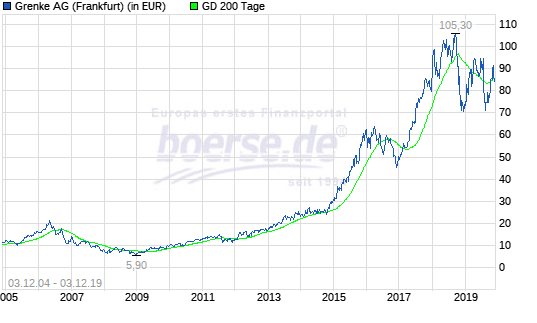

231. Grenke Leasing AG

Shame on me on this one. In 2016 I claimed that I had found the “better Grenke from Australia”, my painful losses on Silver Chef showed that Grenke is still the best Grenke.

Grenke these days has a market cap of around 3.8 bn EUR, but looking at the stock price, the company seems to be stagnating:

EPS for the first 9 months 2019 is more or less unchanged, for a P/E 30 stock this is maybe not enough. Especially “claims” have risen by almost 50% yoy. Not sure what the reason is but normally this is not a good sign. New business is growing strongly, with solid double digit growth but I guess that Grenke is growing now in riskier areas such as Italy and Spain. I was also surprised that Grenke is now also in the Factoring business and is also financing other equipment than the initial IT assets.

Nevertheless, Grenke is clearly a “watch” list candidate,

232. Horizont Holding AG

1.4 mn EUR nano cap. “pass”.

233. Dt. Konsum REIT

492 mn EUR real estate company specializing in retail real estate. the company run by Mr. Elgeti, a very “resourceful” figure in the German capital market. The company is growing through rapid purchases which turn into valuation gains very soon after acquisition. The stock trades at 1.5x NAV. “pass”.

234. OHB

OHB is a 716 mn EUR market cap supplier to the aerospace industry. The company is growing single digits and has EBIT margins of 6-7%. The order book is good for the next 2,5 years or so. ROCE looks okay with 13%, however a PE of ~24 is not so cheap. As I don’t understand much about this industry, for me it is a “pass”.

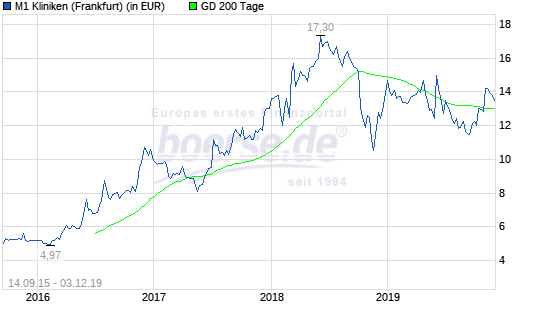

235. M1 Kliniken AG

M1 Kliniken is a 233 mn EUR market cap “health care” provider, specializing on beauty treatments (body, laser, face, dental). The half year report is actually an interesting lecture, I dodn’t know for instance that fat treatment and eye lid corrections are the most common beauty operations done in Germany. The beauty segement within M1 is growing by 40% whereas their “trading” segment is shrinking. Margins are good too, EBIT margins are close to 15%. However reporting is not super transparent. The stock price went up nicely until mid 2018 but is going sideways since then

With a P/E of 25-30, the stock is not cheap but if they would continue to grow by 40%, they would look cheap rather soon. the company seems to belong to the MPH Healthcare “ecosystem” but nevertheless a stock to “watch”:

236. Allgäuer Brauhaus AG

Traditional Bavarian brewery with a 99 mn market cap. Stock price increased significantly over the last few years, however this is not really justified by the operating business which only shows a 1 mn EUR profit for 2018. There seems to be a dominating shareholder and trading is super thin, maybe speculation on a squeeze out ? For me a “pass”.

237. Westgrund AG

714 mn EUR market cap real estate company that trades ~20% below NAV. Majority owned by another listed real estate company, Adler real estate. “pass”.

238. Verianios Real Estate AG

15.7 mn EUR real estate management company. Issued a profit warning a few weeks ago. “Pass”.

239. Luyanta AG

2 mn EUR market cap company without a functioning website. Pass.

240. Windhoff AG

Another 20k market cap Zombie stock. “pass”.

241. Basic Resources AG

1 mn nano cap company, “pass”.

242. Con Value AG

0.5 mn EUR market cap “zombie”. “pass”.

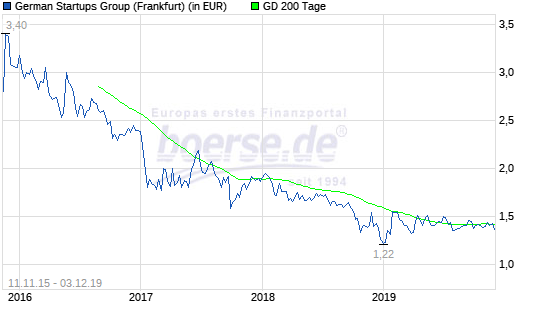

243. German Startups AG

Not a super innovative name for this 16 mn market cap “Listed VC” vehicle. The stock price looks like terminal decline since the company IPOed in 2015 at 2,50 EUR per share.

Initially, the two founders looked like someone I wouldn’t want to shaek hand withs or at least to count my fingers afterward:

In the meantime, the two founders have split and the remaining one is suing the other.

Within GSG, a strategic change has taken place. Investments are sold, debt is payed back and the company has acquired among other a majority stake in a Berlin based IT consulting company. The company looks cheap, therefore a candidate for my “watch” list. UPDATE: In the mean time I bought the stock.

244. UMT United Mobility Technology AG

UMT is a 7 mn EUR smallcap that seems to be active in the mobile payment space, haveing somehow acquired the payment part of the major German loyalty program PAYBACK. However EBITDA is “Pumped up”by capitalizing expenses and overall profitability is low. “pass”.

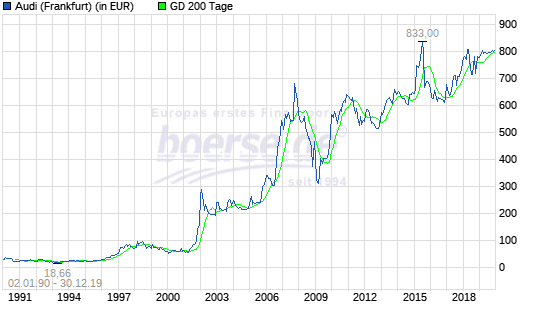

245. Audi AG

Audi AG is the remaining listed part of the Volkswagen subsidiary with a market cap of ~34 bn EUR. As long as I can remember, Audi was always just before being squeezed out a a significantly higher valuation than the one attributed to the tiny free float of 0,34% (the rest is owned by Volkswagen). There is very limited value for minority shareholders as VW has a profit and loss transfer agreement with Audi and Audi shareholders only have the right to a compensation payment of currently 4,80 EUR per share.

Interestingly the stock has shown a fantastic performance over the last years as this chart shows:

My best guess is that the stock is being priced as a bond where 0,5% is still a decent yield these days. However, for me it is a “Pass”.

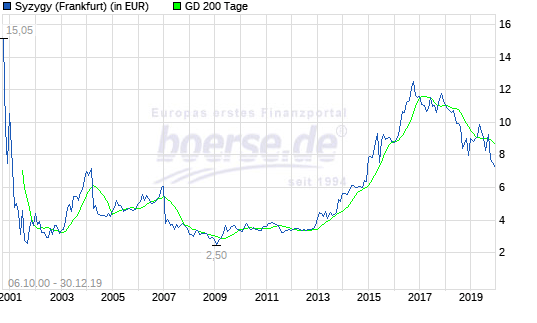

246. Syzygy AG

Syzygy is a 100 mn market cap digital marketing agency that helps its clients to do better advertising or marketing via digital channels.

The company is a “child” of the dot.com boom and ipo’ed at the peak of the mania in 2001. However, inlike others it seems that their business model had legs and the recovered.

In 2015, advertising giant WPP obtained the majority at Sysygy with an offer of 9 EUR per share. However a lot of shareholders thought that this is not enough and WPPP only got ~50,5% of the shares.

Fundamentally, the last years however have not been so good. In the 9M report we can see that 2019 9M top line is now only at the level of 2016 and profit has been declining since then. On that basis, and as the stock is still quite expensive, Syzygy is a “pass”.

247. üstra Hannoversche Verkehrsbetriebe Aktiengesellschaft

üstra is a 148 mn market cap transportation company with a tiny free float of 1,62%. I had never heard of that stock before. The stock is rarely traded.The company seems to be structurally loss making and is majority owned by the Government. “pass”.

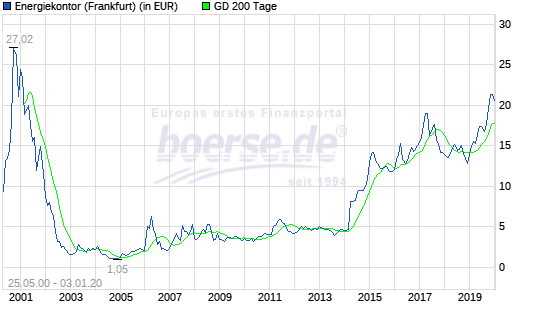

248. Energiekontor AG

300 mn EUR market cap developer of solar and windparks. Energiekontor was IPOes during the Dotcom boom and as we can see in the chart, only 4 years ago the stock started to climb again and has now increased by around 4 times over the last 4 years:

The company is majority owned by two supervisory board members. From the outside, it is not so clear what exactly is the reason for the increase in the stock price. Based on the 6M 2019 numbers, profit has been stagnating since at least 2 years and the company is pretty significantly leveraged. Maybe their own windparks are revalued following the decrease in interest rates ? For me a “Pass”.

249. Fonterelli GmbH & Co KGaA

1.3 mn EUR market cap nano cap active as a “art dealer”. Had to resturcture their debt in 2019. “pass”.

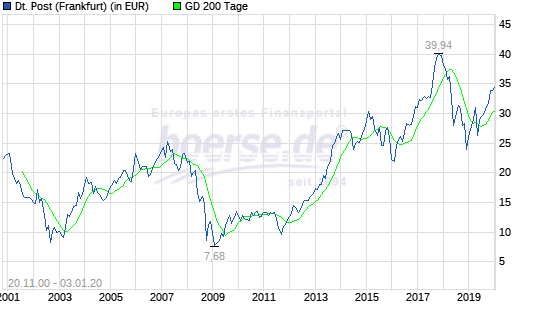

250. Deutsche Post AG

Deutsche Post AG is the 43,5 bn market cap former German postal monopoly that has been privatized in 1995. 20,5% of the shares are still held by a Government owned entity (KFW Bank). As many former monopolists, Deutsche Post combines a highly proftable but shrinking postal business plus a growing parcel delivery business.

The segment reporting doesn’t really reflect the reality and is somehow structured differently. The stock has been doing quite well over the last few years as the chart shows:

9M results 2019 saw a nice increase yoy but that was mainly driven by a de-consolidation effect. For me, Deutsche Post is too large to be interesting and I have no special insights into the sector, so I “pass”.

Some bad news for Grenke today with a short report:

Or maybe good news, as it is a good opportunity to address claims and/or clean up…

and it is happening: VW taking over the final 0,xx% of Audi, for a 50% premium…

https://www.reuters.com/article/us-volkswagen-audi-buyout-idUSKBN23N2M2

German Startups direction want the share price to reach a better price compared to “NAV” before investing in new startups. Seems risky to me – past performance of startups won’t predict performance of their current portfolio. They just wanna buy back shares until then. Not a good startup-oriented company strategy imo… Very risky with potential +100-200% upside but if they mess this up it could go much lower

Zilian, not sure if I understand your comment. German Startups plans a significant strategy shift, i.e. they will not invest any more into minority startup participations. Rather the opposite, they will continue selling their remaining stakes. Their plan is to develop businesses (i.e. a market place for startup shares etc.) around that ecosystem. They also “don’t wait until then”. Of course there is risk in that shift but for the time being the downside risk is limited as the market cap is pretty much covered by cash.

Out of curiosity you should read the Dt. Konsum REIT Annual Report, particularly the Related Party section.

I agree, I am a recent follower of this blog and enjoy the posts a lot.

In the interests of sharing re M1 Kliniken – My take away was they have a very interesting offering in a nascent market which I expect to grow nicely in the future. On the negative side they had surpisingly poor cash conversion and were investing – I am not sure how that has changed over the last year or if the growth from investment met expectations. The biggest thing for me was that I found the ownership structure quite convoluted (M1 owned by MPH owned by family entity Magnum, M1 CEO is also the MPH CEO and his father is in charge of Magnum) and don’t understand why both M1/MPH need to be listed. It feels like (and is) a family business where there might be a clear strategy to take on this interesting market opportunity but it wasn’t clear to me last time I looked.

But maybe you guys discover something I missed…

Thanks, I was hoping for sich high quality comments to thin out my watch list 😉

Keeping on going 🙂

Always interestig to read these.

Will take a look at M1 Kliniken out of curiosity. It sounds interesting as an investment theme.

I have been following Deutsche Post for a while now. While I like how they run their business it’s been too expensive for me.

Just to make my life a little easier I stay away from apparel and agencies.