And on we go. With this post, I have passed the 50% threshold, so I am very optimistic to finish this before year end. This time, two stocks qualified for the preliminary watch list. Let’s go:

136. Norbit

Norbit is a 305 mn EUR market cap company has three distinct segment of which “Oceans delivers tailored technology to global maritime markets, Connectivity provides wireless solutions for identification, monitoring and tracking, while PIR offers R&D services, proprietary products and contract manufacturing.”

The company IPOed in 2019, and contrary to the 2020 IPO vintages, the share price has done quite well:

This has become a quite long and somehow rambling post. If you look for “actionable investment advice”, then you don’t need to read this.

Background: Handelsbankon on the blog since 2015

One of the great things of an Investment Blog/Journal is that one can easily revisit everything that one has written years ago when I want to look at a stock again.

Handelsbanken is a stock that I have covered quite often since 2015. Initially, I compared Handelsbanken to Deutsche Bank in 2015, claiming that Handelsbanken is a much better run “quality bank” compared to Deutsche Bank and that Deutsche Bank, despite the much cheaper valuation, most likely the worse investment. This is how Handelsbanken has performed against Deutsch Bank and the European Banking index.

Govro has already published an excellent post about the situation in his Wintergem Blog here. He estimates that a sale at ~9xEV EBITDA could result in an offer of CAD 76 per share. However, he points out that this is just the start of a process and it could well be that there will be no sale at the end, especially as due to the high interest rates, the infrastructure sector is not super hot at the moment.

The Logistec share price has increased from around 43 CAD per share before the announcement to around 60 CAD at the time of writing. Funnily enough, this is almost exactly half way between the “undisturbed price” and Govro’s sale price estimate.

Disclaimer: This is not investment advice. PLEASE DO YOU OWN RESEARCH !!!

Some days ago, I made the case for a significant increase in demand for insulation in Europe for the next several years. In this post, I want to dig a little bit deeper into the main listed players and which I find more interesting. In general, even only for the German speaking region there are many companies that offer insulation, among them very large, diversified groups such as BASF, Dow Chemical and St. Gobain.

However, the following listed companies are those who do the majority of sales in insulation to my knowledge:

Kingspan, Irleand/UK Rockwool, Denmark Recticel, Belgium Steico, Germany Sto SE, Germany

Sto, Rockwool and Recticel are already in my portfolio with relatively small weights.

Before jumping into the companies, I have compiled a table with a few KPIs that i find interesting. One quick coment upfront: As Recticel is undergoing a signifcant transformation, their numbers are curently not comparable.

Disclaimer: This is not Investment advice. PLEASE DO YOUR OWN RESEARCH !!

Summary:

If you would ask me about the most boring stock of my generally very boring portfolio, I would possibly name Schaffner Group. I had bought a first position back in 2021 during my “All Swiss Stocks” series.

However, I have never written a more detailed write-up despit my annual summaries (2021/2022 ,2022/2023), maybe becasue I always got bored when I started writing about it ? Over time I added to the position and after the most recent 6 months numbers, I decided to increase into a full position. Time to explain the investment case a little bit better.

Disclaimer: As I am an investor and not a Building & Construction specialist, this post might contain a lot of wrong or even misleading information. All I can say is that I do this on a “best effort” basis.DO YOUR OWN RESEARCH !!!!

Time flies. Already more than 7 Months ago, I introduced my “Freedom insulation” basket. Since then I had pruned the basket, mainly because of the contraction in the construction industry and currently I only hold Rockwool (1,1%), Sto (1%) and Recticel (0,6%). Back then, the underlying case for insulation was a very high level one, this time I want to dig a little deeper and substantiate it if possible.

Regulatory background:

Just a few weeks ago, the EU Parlament passed a quite impactful law, basically requiring the “energetic renovation” (and insulation) of old buildings within the next 4-10 years. The most important part is that for each EU country, the worst 15% of buildings must be thoroughly renovated by 2027 (commercial) and 2030 (residential), with even stricter rules after another 3 years.

As this is Europe, the details of this law now need to be discussed with each and every member country and for sure, there will be excemtoptions and delays, but the direction is clear: There will be a strong push towards renovations which in turn will require a lot of insulation. Naturally, with the Green Party in charge, Germany has passed already some laws that require property owners to do something quickly, like for instance baning Oil and gas heating from 2024

What happened to insulation stocks since then ?

Interestingly, this hasn’t helped insulation stocks at all, as the stock charts below show. Over 1 year, insulation stocks significantly underperformed the broad construction index, since my post in September performance was on average “in line” (yellow is Steico):

In the first 3 months of 2023, the Value & Opportunity portfolio gained +4,7% (including dividends, no taxes) against a gain of +11,3% for the Benchmark (Eurostoxx50 (25%), EuroStoxx small 200 (25%), DAX (30%), MDAX (20%), all TR indices).

Links to previous Performance reviews can be found on the Performance Page of the blog. Some other funds that I follow have performed as follows in the first 3M 2023:

Partners Fund TGV: -3,3% Profitlich/Schmidlin: +8,0% Squad European Convictions +5,3% Frankfurter Aktienfonds für Stiftungen 1,3% Squad Aguja Special Situation +3,9% Paladin One +4,9% Alphastars Europe + 4,2%

I have slightly adjusted the Peer Group by eliminating Ennismore as it is actually a long/short Fund and Greiff Special situations. I have added Alphastars Europa, a quite new fund,. What I like about Alphastars is that one has an almost real time view into the portfolio. The Europa funds contains a selection of quite unusual but very interesting selection of European small caps and will be a challenging peer for me going forward.

Performance review:

Overall, the portfolio performance was again more or less in the middle of my peer group. As the peer group is pretty Small cap focused, the relative low returns correspond with the returns of European small cap indices. Looking at the monthly returns, it is not difficult to see that especially January was in relative terms very disappointing.

Disclaimer: This is not investment advice, PLEASE DO YOUR OWN RESEARCH !!!!

For all readers that found my SFS write-up from February as too exciting, I have good news: I have found a stock that looks at least as boring as SFS, maybe even more so: Logistec, a maritime terminal operator from Canada.

Background/Intro:

This is the first investment idea that I initially found on Twitter, a big Hat tip to Sutje who brought this up on my radar and of course to the author of the original write-up “Wintergem Stocks”. The Wintergem Substack has a 3 part write-up that I can only recommend to read first:

And on we go after a short break with another fresh 15 Norwegian stocks, selected by the Google Sheets random generator. This time, I have identified six companies that go onto the preliminary watch list. Let’s go:

106. Instabank

Instabank is a 50 mn EUR market cap “fully digital bank that offers loan products, savings and insurance to consumers in Norway, Sweden and Finland.” The company was IPOed in 2022 and surprisingly trades slightly above its IPO price, a clear exception for the 2020/2021 IPO vintage.

Equally surprising is the fact that a relatively young “digital bank” makes a profit. They seem to lend to more “high yielding” customers but overall, they show decent growth and the stock looks cheap at 8x trailing earnings and ~6,5x 2023 earnings.

Although I am not a big fan of Nordic banks, I think this one is worth to potentially “watch”.

107. GNP Energy

GNP Energy is a 19 mn EUR market cap Energy company that has lost more than 50% since its IPO in 2020. I also found very little tangible information on this one. “Pass”.

108. Wilh. Wilhelmsen

Wilh. Wilhelmsen is a 1 bn EUR market cap “global maritime industrial group offering ocean transportation and integrated logistics services for car and ro-ro cargo. It also occupies a leading position in the global maritime service industry, delivering services to some 200 shipyards and 20 000 vessels annually.”.

Looking at the long term chart, it seems that there is significant cyclicality in Wilhelmsen’s business:

The shares currently trade at a historical high and on avery low P/E multiple. The P&L is not easy to read as the majority of net income comes from non-consolidated JVs. My gut feeling tells me that entering at the top of the cycle might not be a smart idea, however they seem to be very active in supporting the offshore wind industry. Therefore I’ll put them on “watch”.

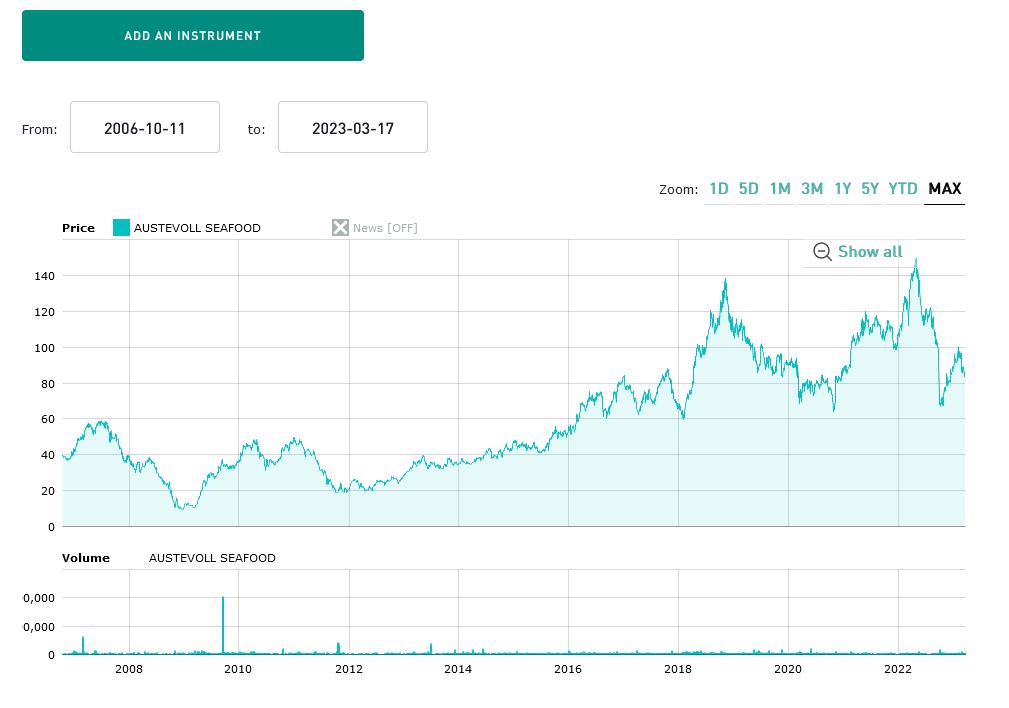

109. Austevoll Seafood

Austevoll is a 1,6 bn EUR fish farmer, which compared to the other fish players so far, is a very established player. Looking at the long term chart we see a relatively good value creation, but quite some volatility:

The stock looks quite cheap at 8x 2023 earnings, but they employ quite some leverage. I think they were also hit by the suprse Norwegian Special tax for Salmon fsih farmers. Overall, this could be one of the fish farms where one could learn something, therefore they go on the preliminary “watch” list.

110. Tysnes Sparebank

Tysnes is a 20 mn EUR local savings bank, which, not surprisingly is located in Tysnes near Bergen. The stock looks cheap, but regional savings banks are not my specialty, therefore I’ll “pass”.

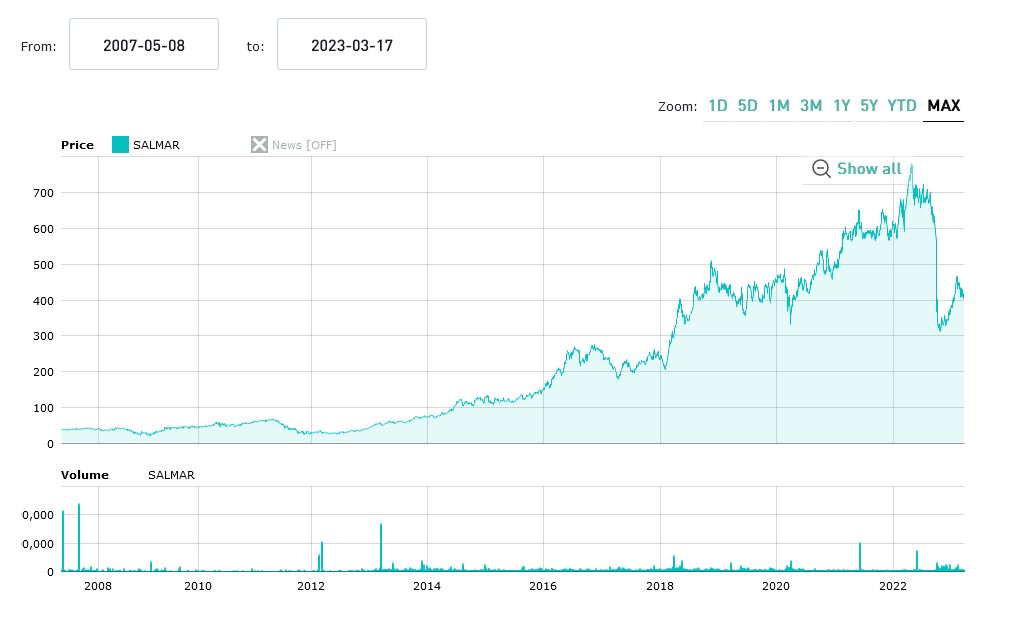

111. Salmar

Salmar, with 5,5 bn EUR market cap seems to be one of the “larger fish” among the Norwegian fish farms. The long term share chart looks impressive, despite the obvious hit from the special tax:

However, the valuation at 17,5x 2023 earnings seems to reflect this already to a certain extent. Interestingly, Salmar holds a 71% interest in another listed Norwegian company called Froy which seems to be a specialist in servicing fish farms. According to the Q4 report, they seem to contemplate selling Froy

Overall, Salmar is also a company which could be interesting to “watch” as their track record seems to be really god.

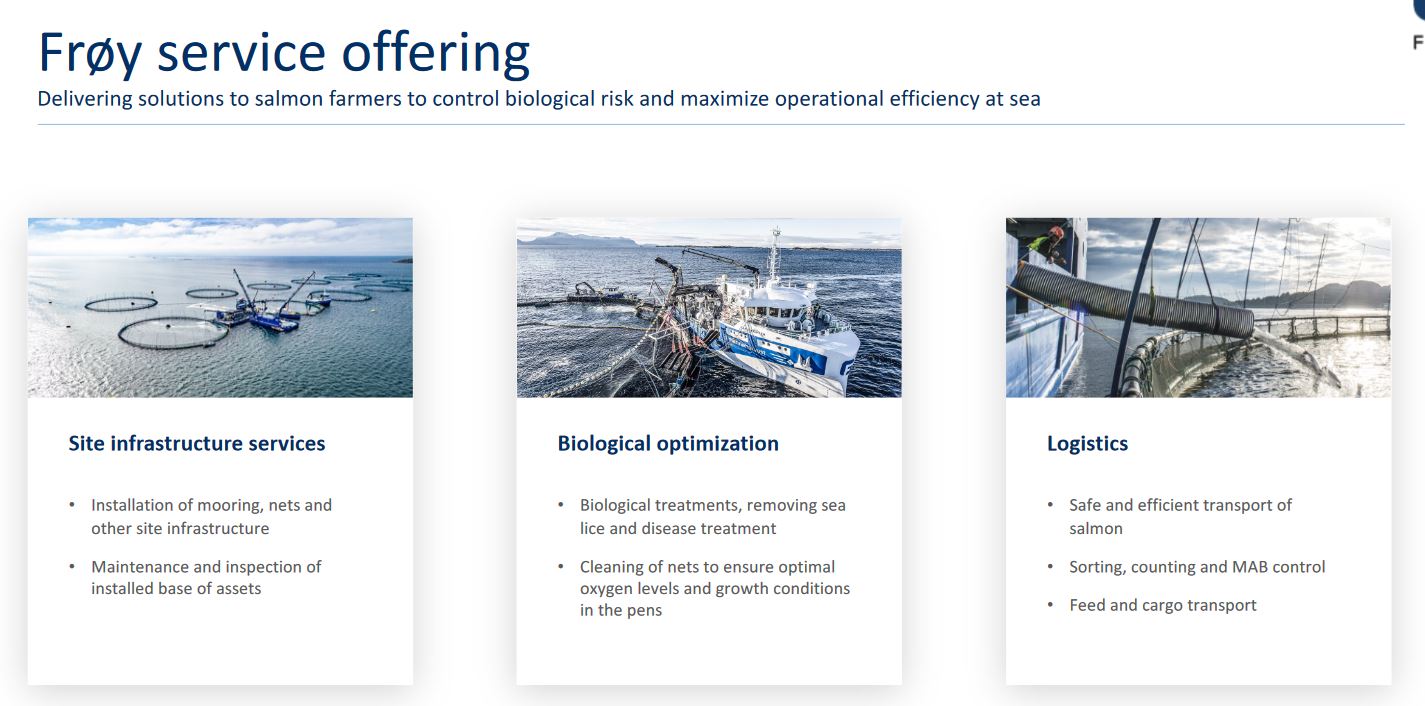

112. Froy

As a one time excepion, I follow up with Froy, a 475 mn market cap stock in which Salmar holds a 72% stake. Froy was IPOed in 2021 and its share price went on a pretty wild ride:

According to their initial investor presentation, Froy seems to be a very important service provider to the fish farming industry, providing all kind of essential services with a focus on Norway:

I guess that their focus on Norway led to the significant loss in the share price follwoing the surpise tax on Norwegian Slamon farming last years.

As mentioned in the Salmar write-up, Salmar seems to be considering “strategic options” for Froy whatever that means. In any case, I find Froy interesting, despite the fact that it is not cheap at 18,5x 2022 earnings. “Watch”.

113. Okea

Okea is a 250 mn EUR market cap company that owns minority interest in several Norwegian off shore oil fields.

They seem to specialize on mature oil fields and try to extend the life of these fields.

The company was IPOed in 2020 and the share price has been fluctuation widly between 10 andf 70 NOKs:

As many oil stocks, the stock looks ridicuolosly cheap at around 2,4x trailing P/E and a big juicy dividend. However there seems to be clearly a strong leverage to oil prices which are now declining for some months. Somehow I still find them interesting bexause of their foucs on Norway, therefore they go on “watch”.

114. Techstep

Techstep is a 37 mn EUR market cap company that seems to hav had its best time in the early 2000s, although the current business model seems to have impmented only in 2016. The company seems to offer some mobile services, but only achieved to have a positive operating result in 2 out of the last 6 years. “Pass”.

115. Sparebanken 1 Helgeland

This is a 324 mn EUR market cap regional savings bank that looks quite profitable- The stock has performed quite welll since the GFC and is not too expensive (P/E ~10,5). However. local banks are out of scope for me, “pass”.

116. Agilyx

Agilyx is a 228 mn EUR market cap company that is active in chemical plastics recycling. As a 2020 IPO, the stock trades around the IPO price, which can be considered a succes for this vintage.

As one can expect from a young cleantech company, they are loss making, although they do have sales, currently a run rate of 15-20 mn EUR. However gross margins are negative for the time being and they are burning cash.

The main shareholder is a fund called “Saphron Hill Ventures” and as many such companies they have an impressive list of strategic partners (Exxon etc.). They seem to operate a JV with Exxon in the US called Cyclix, that recycles plasticand another project seems to be in construction in Japan

Plastic recycling is an interesting topic, however a negativ gross margin really turns me off, therefore I’ll “pass”.

117. Aurskog Sparebanken

Aurskog is a small, 89 mn EUR market cap local savings banklocated in Aurskog near Oslo with no specific aspects at a first glance. “Pass”.

118. SATS

SATS is a 110 mn EUR market cap fitness chain that is active across Scandinavia. The company IPOed in 2020 and lost around -75% since then, indicating that not all is great.

The main reason might be that since their IPO, they have not been able to genrate a profit. The company has significant debt, although they managed to lower the debt burden over the past 3 years.

Because of loan covenants, the company is not allowed to distribute dividends and Q4 2022 was not great, most likely due to electricty and heating costs.

At an EV/EBITDA of ~5,5 this might be interesting for turnaround specialists, but for me the risk is much too high, therfore I’ll “pass”.

119. Nykode Therapeutic

Nykode is 570 mn EUR market cap “clinical-stage biopharmaceutical company, dedicated to the discovery and development of vaccines and novel immunotherapies for the treatment cancer and infectious diseases. Nykode’s modular platform technology specifically targets antigens to Antigen Presenting Cells.” Nykode was only profitable in its IPO year 2020 and has been making losses in 2021 and 2022.

As far as I understand, they are using a different technology to MRNA, but they have some interesting cooperations and Cash should last for a couple of years. However, Biotech is far out of my circle of competence, therefore I’ll “pass”.

120. Wallenius Wilhelmson

By coincidence, this 3 bn EUR market cap company has been selected in the same part of the series as Wilhelm Wilhemsen. And indeed, the companies are related as Wallenius Wilhelmsen seems to be a JV between Wallenius and Wilhelmsen, specialising in owning and operating ships that transport cars.

As other shipping companies, the stock did quite well, doing ~11x since the bottom in MArch/April 2020. The stock looks really cheap at a P/E < 5, but buying cyclical stocks at the margin peak is rarely a good entry point. As I have Wilhelm Wilhelmson already on watch, I’ll “pass” here.

In between, the bank run accellerated and SVB was then closed and rescued by the FDIC. In the age of social media, there is now a lot of coverage on this event available, personally I found this Odd Lots Podcast Episode helpful as well as Matt Levin’s take. Matt Levin also has an answer on why SVB was not sold over the weekend: In the wake of the GFC, many of the banks who bought failing lenders were then punished with lawsuits and it seems that something like this could happen to SVB as well.

Current consensus is that SVB failed both, because of very unwise interest rate bets on its asset side as well as an unhealthy concentration of its depositor base connected by a few big VCs on its liability side. According to many stories, SVB was a very active member of the Silicon Valley VC ecosystem and somehow the VCs (and startups) basically killed the Goose who laid them golden eggs with this bankrun. In the current difficult funding environment, It would have made more sense fot the VCs to support the bank but I guess they were all in panic mode.

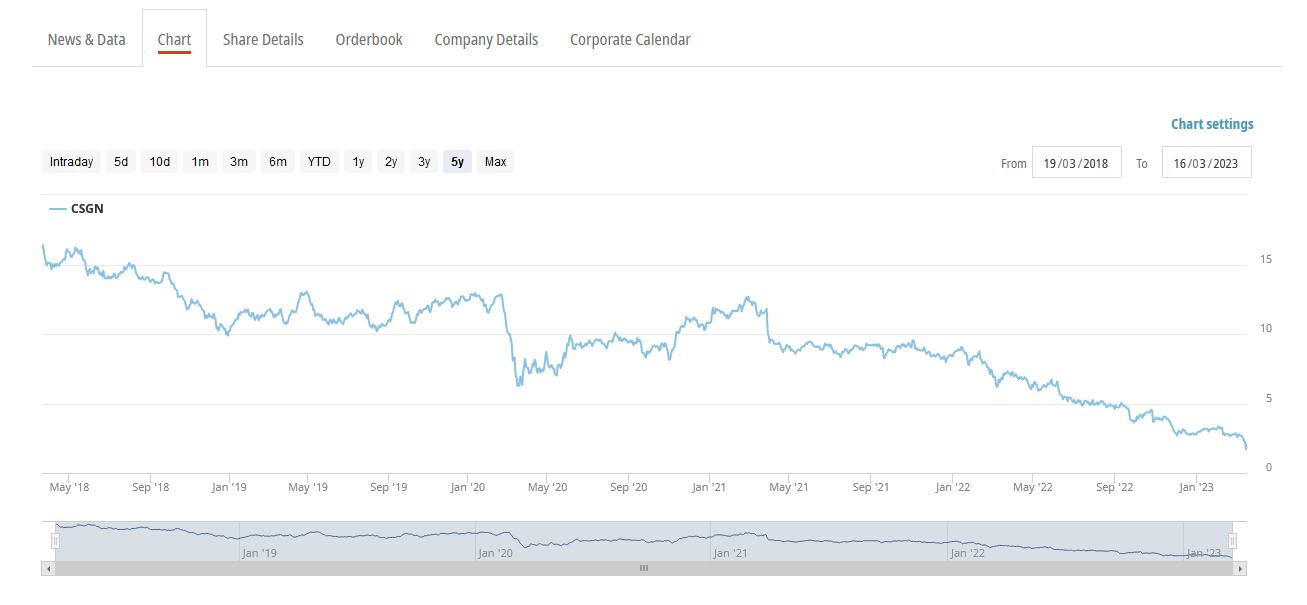

CS was a slow moving train wreck ever since the former McKinsey “Wunderkind” Tidjane Tiam took over as CEO in 2015. When he was fired in 2020, not only it was revealed thaty he used private investigators to spy on fellow board members, but more importantly, Credit Suisse was involved in almost every major fuck-up in the last few years. A few examples:

Looking at the CS share price, it is pretty obvious that there is literally no bottom:

Although it is always very difficult to make predictions, I personally think that a true and lasting turn-around for CS is very unlikely. There are very few cases in banking history where a financial institution survived such a “clusterfuck”. Credit Suisse would not be the first big name in Banking that just disappears. Besides Leahman and Bear Stearns, who remembers Salomon Brothers, DLJ, Bankers Trust, Barings, Smith Barney, Chemical Bank, Dresdner Bank and all the others ?

The most likely scenario in my opinion will be that the ring-fenced Swiss operation will somehow survive. What that means for Bondholders and shareholders on Group level is open, but in my opinion the CS shares are at best a “far out of the money option” on a very optimistic scenario. Of course anything can be traded profitably in the short term, but mid- to longterm, a complete loss of capital is very likely for CS shareholders.

Today: First Republic Bank

First Republic, a “mid sized” 200 bn plus US bank with ~21 that banks to “High net worth clients in costal regions” continued its plunge and said it would be open to almost anything, including a fire sale in order to survive.

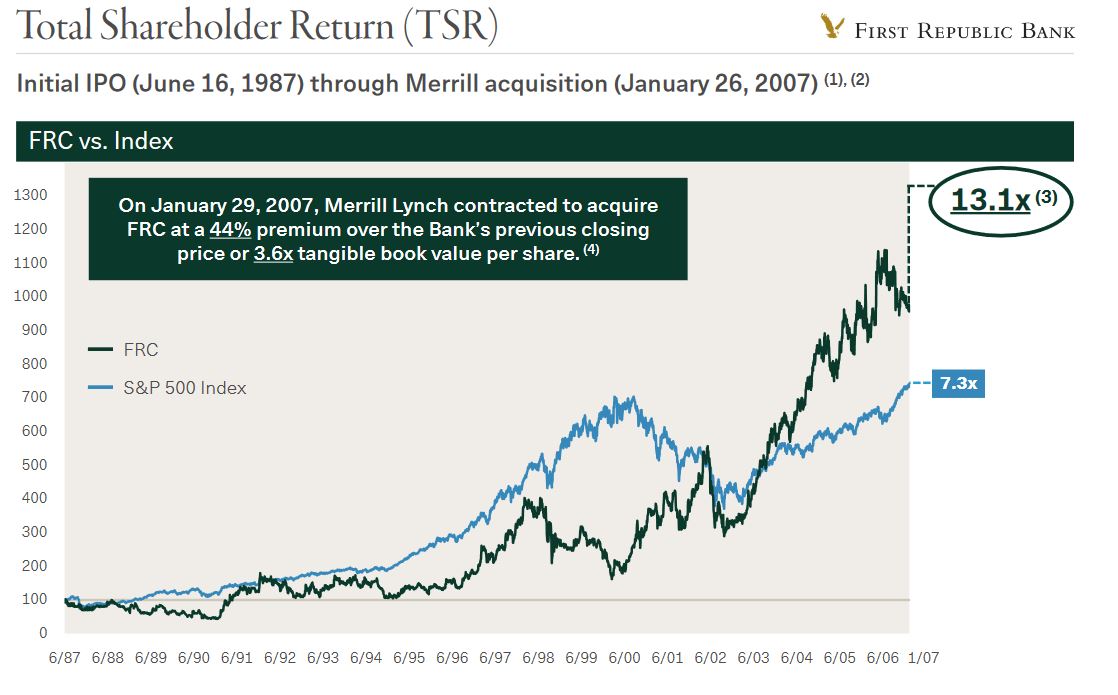

When reading the January invetsor presentation, First Republic looks like an absolute success story, among others, their share price went up 13x since 1987, almost 2x the level of the S&P (i guess ex dividends) which is remarkable for a bank:

However, looking at these slides, it becomes relatively clear where the problems of Republic are: Funding is mostly via deposits:

The deposits are mostly business accounts and larger size:

And, the Asset side consists mostly of “coastal real estate loans” and business loans to venturec Capital funds, both assets that might be in trouble:

To be honest, If I would have known about First Republic earlier and read the investor presentation, I might have considered it as a potential investment. The bank also traded at unusual high P/E multiples in the range of 20-30 earnings, so very few investors

Next week and thereafter: Whatcould be the more lasting effects of this episode ?

I guess that for the next two or more weeks, the market is “hunting” for further weak players and all of them will be backstopped by their respective Governments and Central Banks. A “Lehman moment” in my opinion still remains a very low probability scenario. However it is also clear that this whole development might have wider consequences.

For the banks, it will be even more difficult to transform short term deposits into longer term assets, which by definition is one of the main function of the banking system. For the US, more and tougher regulation is already on the way.

Among other side effects, overall the current development will most likely increase funding cost and limit borrowing capacity for the banking sector. This in turn will make it more difficult for borrowers to obtain or roll over bank loans. And if borrowers are able to obtain bank loans, they will need to pay higher credit spreads. A certain increase in Corporate Credit spreads was already observable in the past few days.

Overall this could have a siginficant impact on business activity as the availability of bank loans is a leading indicator for economic activity. This in turn could then lead to the second part of the cycle, the real credit cycle with more defaults etc.

Depending on how inflation rates are developing, the central banks might counter with lower interest rates, which however, do little to make lending easier for the banks. Of course, Governements and Central banks will try to counter a big credit squeeze, however without tighter credit conditions it is unlikely that inflation will cool off quickly.

I need to emphasize here that I am not a Macro guy at all, but overall, I think the probability for a real credit cycle has increased significantly. As a consequence, in my opinion one should limit exposure to exposed financial companies as well as businesses with near or mid term funding requirements.