Munich, 25. February 2026 – innoscripta SE (ISIN: DE000A40QVM8, the “Company”) expects an increase in revenue and earnings for the 2026 financial year based on current business development and continued high demand.

The Company’s Management Board currently expects the following for the 2026 financial year:

consolidated revenue of at least EUR 140 million and

EBIT of at least EUR 80 million

The guidance is based on the current order situation, the scalability of the business model, and stable regulatory conditions.

This guidance represents an expected +36% sales growth for 2026 (vs. + 60% in 2025) and +27% EBIT growth (vs. +70% in 2025). The implied 2026 EBIT margin is 57% against 61%.

Overall, despite the slow down in growth rates, these are still very impressive numbers. The stock trades currently at around 14x 2026 P/E. Still, investors don’t seem to be convinced that this is a good investment.

Maybe the “AI fear” is the driver here. To be honest, I find it very difficult for now, to get the conviction to invest into the currently very negative share price momentum, but I will keep watching and hopefully be able to attend the AGM in Munich in person.

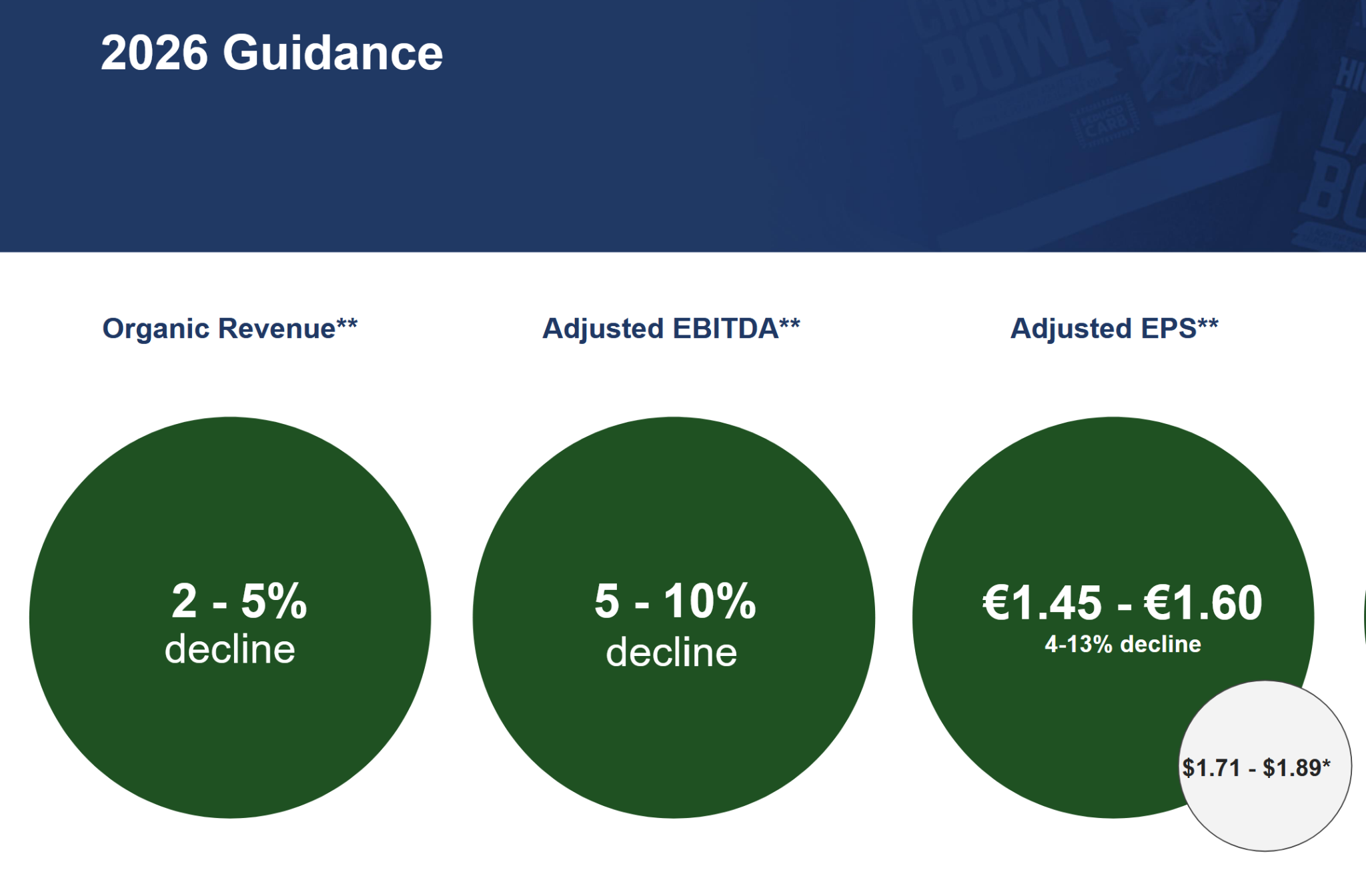

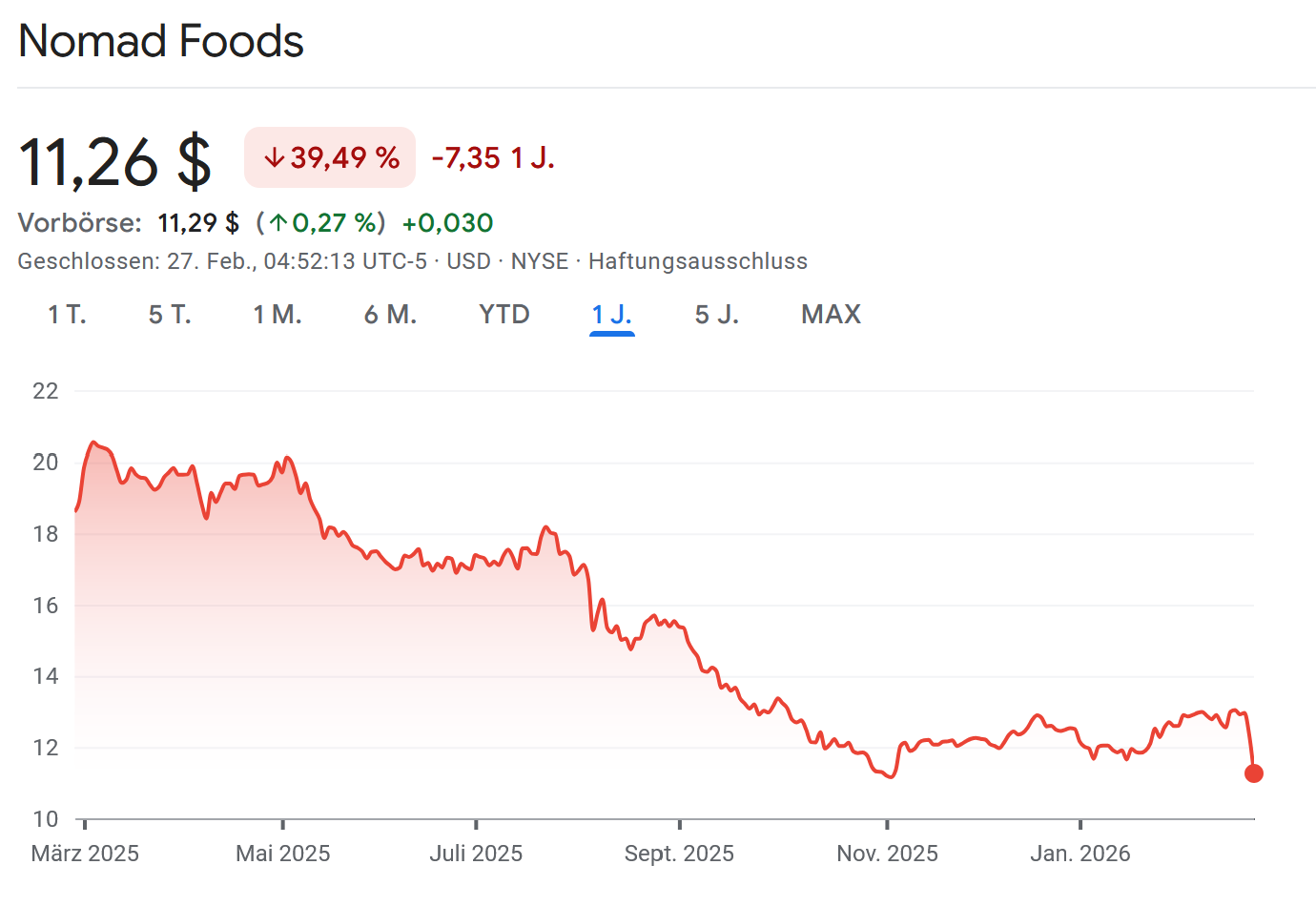

The picture was not pretty at all. Sales down, margins down, earnings down. Unadjusted they actually made a GAAP loss in Q4.

The guidance for 2026 doesn’t look much better either, but rather worse:

If we compare this to Frosta who have increased sales double digits, improved gross margins and only have shown lower net margins because of higher advertising spend, it is pretty clear that Nomad Food and especially the Iglo brand seems to be losing market share.

My gut feeling is that in Nomad’s case, the focus on Cash generation and share buy backs has maybe led to underinvestment into the brand which is not so easy and quick to reverse. Pretty much the same “playbook” and issues like Kraft-Heinz or Anheuser-Busch.

In the consumer space, the safer long term bets are those guys who invest long term into the brand and not the spreadsheet jockeys.

With a further EBITDA decline and current Debt/EBITDA of 3,8x, I am not sure for how long they can continue to pay dividends and buy back shares.

This one looks really vulnerable. For Frosta, there could be a msall risk that if Nomad gets really desperate and needs cash, that they start to dump their products into the market. So I think it makes sense to look at Nomad updates as a Frosta shareholder in any case.

No one has asked for it, but here it is, the next episode of my Private Equity series. Previous episodes of the Private Equity series can be found here:

Everyone in the alternative (non-listed) investment space has been talking about the Blue Owl Private Debt “redemption gating” event lately, but in my personal opinion, another story which has not been so widely reported is much more interesting.

The case of the first Stonepeak Infrastructure Flagship fund is at least equally interesting for the whole Private Equity sector and I will try to explain why.

Traditionally, the Private Equity business model can be summarized from the the perspective of the Asset Manager or General Partner (“GP”) as follows:

GPs take a big junk out of any upside (usually 20% ,sometimes more) but themselves have very little downside risk as they charge a hefty 2% p.a. fee in any case and only, if at all, invest relatively little money themselves into the funds they manage.

So let’s look at Stonepeak. Stonepeak is one of the leading Alternative Infrastructure Equity Asset Managers in the world and has 89 bn USD Assets under Management. It is still privately owned.

Although the dividing line between Infrastructure and Private Equity is a little bit blurry, Infrastructure investments are often “capital heavy” and considered more safe despite usually significant leverage. Typical assets are ports, Airports, railways, toll roads but also stuff like container leasing, warehouses etc. (among others Stonepeak bought the Canadian Port Operator Logistec which I owned)

Target returns for Infrastructure funds are usually a bit lower than for Private Equity (usually maybe 10-15% p.a. vs. 15-20%) and fund duration is often a bit longer. But infrastructure should be also be more robust, i.e. have less downside than a PE fund.

Stonepeak was founded in 2011 and launched its inaugural “Flagship” fund in 2012.

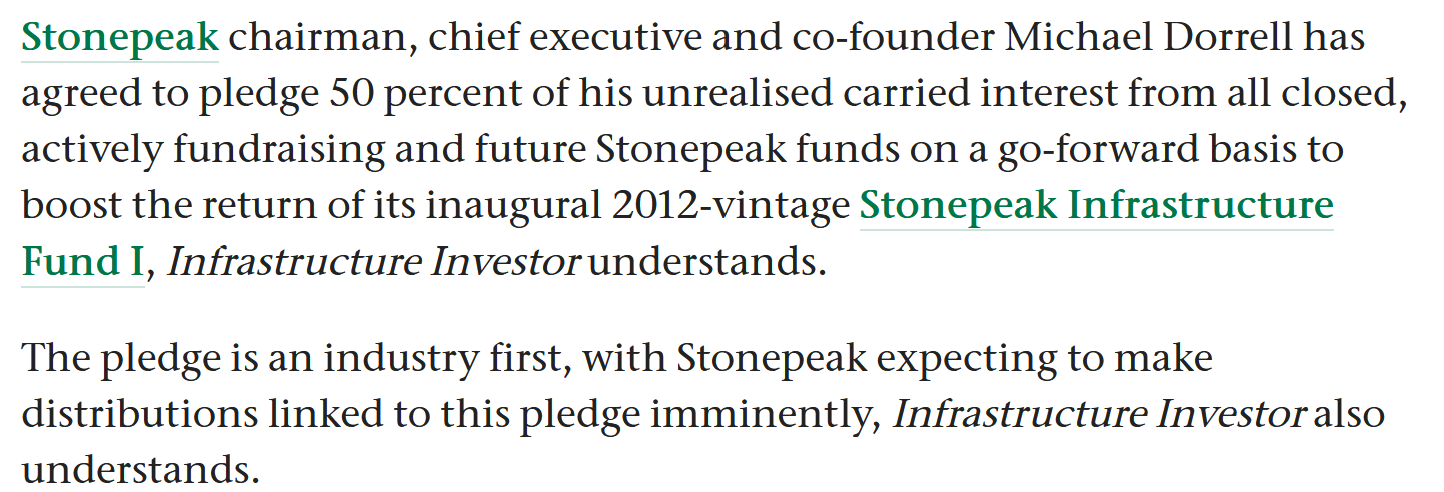

Although it is not unusual that Alternative Assetmanagers might maybe reduce fees going forward if a fund performs really badly, this is the first time that I have actually seen that an owner actually puts in personal money to make good on the not so great performance of the investors. Here is how it should work:

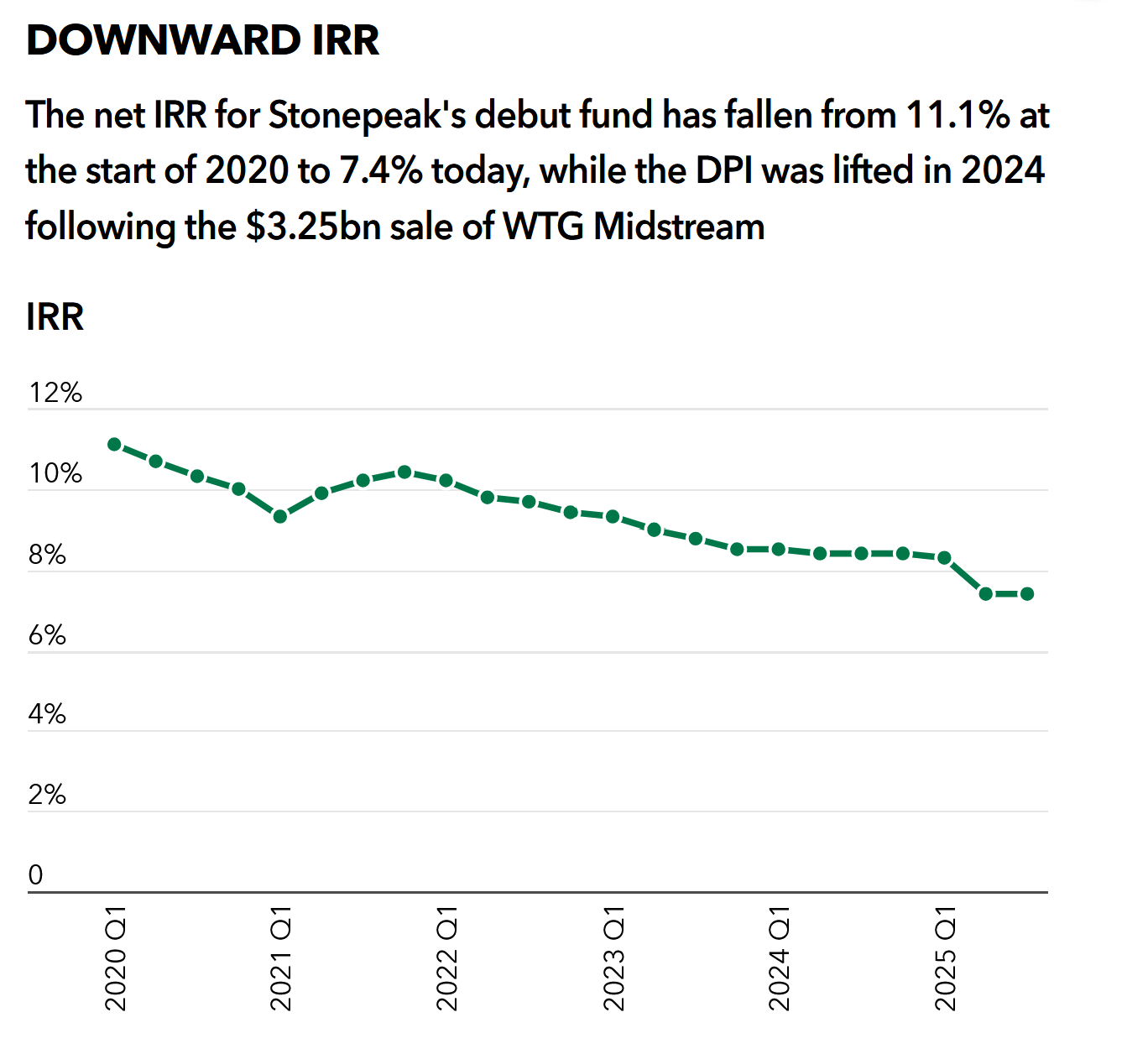

According to the article, the initial fund had “promised” 12% net IRR to investors at launch but currently, after 14 years it only shows an IRR of 7,4%. Not a catastrophy at first glance but also not great either for such a vintage that should have benefitted from a significant decline in interest rates which was especially beneficial for “long duration” infrastructure assets.

What is also really interesting is that graph that shows how calculated IRRs have developed in the last years from the perspective of investors in this fund:

Until 2020, i.e. for the first 7-8 years everything looked fine. But what happened then ? And why is this relevant ?

I guess it’s now time to tell you a little bit about a “dirty secret” of the Private Equity (and Private Infrastructure) world.

Whenever a new firm gets created and launches an initial fund, it takes a long time until investors can see actual results. On average, in the infrastructure space, investment are sold maybe 6-10 years after they have been bought.

However, Asset Managers don’t want to wait until then to raise a new fund. They want to raise funds more frequently in order to earn more fees. Normally the “fund raising” cycle is ~ 3-4 years.

Even professional investors invest mostly based on past performance, often just simply extrapolating those past numbers in the future.

So what do you do when you have no exits to show ? Of course, you just mark up your portfolio yourself based on some loosely defined metrics which often is coincidently very close to the target return. So just to say this again: In the beginning, almost all PE/Infrastructure funds are marking up their investments “at will” to show a decent performance, of course with the hope that later on, they will actually realize those returns or even more.

You then can present this (unrealized) return to investors and they happily invest into the next fund and the next etc.

In Stone Peak’s case they were quite busy and raised another 3 funds during the time when performance was looking still OK for the initital fund in 2020 as we can see here:

The funds got bigger and bigger, Fund III was ~7 bn and Fund IV 14 bn. And they are currently raising fund V with a target size of 15 bn,

Most of that money got raised with investors looking at the track record and saying: Fund I looks good at 11% p.a. (or maybe even more in the beginning) and I guess Stonepeak was telling them that this was marked “conservatively” (GPs always say that about unrealized values).

But it turned out to be wrong and clearly overvalued. And this is clearly embarrassing for Stonepeak.

If I were a potential Stonepeak investor doing Due Dilligence, I would ask: “How can I trust all the other performance numbers of your funds when the only one which is almost realised seems to have been significantly overvalued ?”

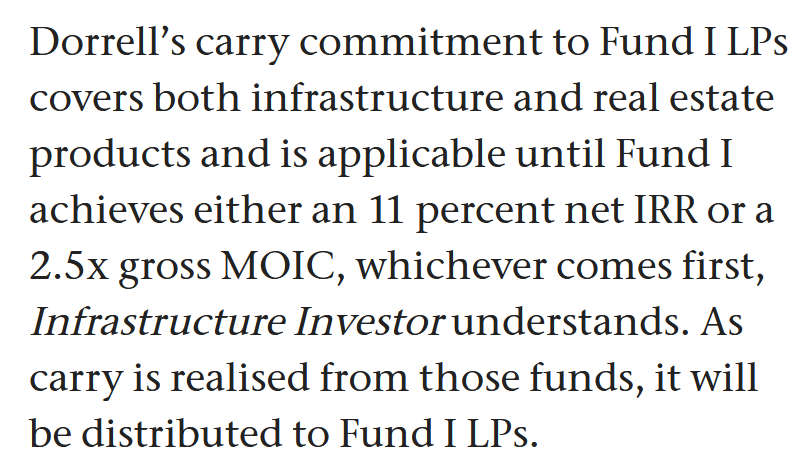

I guess that’s why Dorrell wants to make those investors “whole” with personal money:

As the first fund is significantly smaller than the follow up funds, this will not bankrupt him, but anyway, this is an industry first.

The industry relevance in my opinion is the following:

We can expect a lot more such cases where the initial, very positive performance will turn out not so positive at all or even funds may lose money (2019 to 2021 vintages for instance).

So far, this has always been the sole problem of the investor, never for the GP.

Michael Dorrell now created a high profile precedent that will be taken up with gusto by many disappointed investors.

The smart LPs will use the Stonepeak precedent to ask their GPs for the same “Commitment” to make good on their initial promise.

Otherwise they will not invest into a subsequent fund. Some GPs, especially the very big ones will resist, some will maybe just close up shop, but I guess a lot of GPs will get under a lot of pressure.

Overall, this might be a first step to change the relationship between GPs and LPs going forward. If you are an investor in any listed Alternative Asset manager, I think you should really pay attention to this. It could be that in the future, results might get even more volatile and in general lower if funds underperform.

Another relevant point is the following:

This case also puts a spotlight on how arbitrary especially early valuations are for these investments. Already last year, I heard rumors that auditors have begun to challenge valuations of PE funds as they see secondary transactions with large discounts.

I could also imagine that investors want better disclosure of unrealized return figures during Due Diligence and how those seemingly great early performance numbers got cooked up, or maybe not 😉

In any case, I am sure that there willl be a lot of interesting discussions already going on between disappointed investors and GPs, that’s for sure.

Timing wise, this comes at a pretty inconvenient time for most PE firms anyway. As this chart shows, the last year was not so good for the share price performance of the big shops:

Maybe we will see a turn-around at some point in the future, but for the moment I see more headwinds than tailwinds for the industry overall. If more GPs are forced to compensate investors, then valuations for those guys would need to come down significantly.

This post does not contain any actionable investment advice but rather some personal ramblings on Vibe coding and the attempt to analyze a specific Software company (Guidewire) according to a Template of 10 Moats for Software companies and their vulnerability to the AI threat.

Introduction:

My track record as a Software investor is to put it mildly, very poor. My best Software Investment so far is Chapters Group which I bought as a net-net before it even became a VMS Serial Acquirer. My blog and portfolio archive also tell me that I sold Microsoft in 2011 at ~25$ per share with a 4% gain because I thought that the Office products had no future. So please take everything I say about Software with a grain of salt or even better, just ignore it.

I do have a background in Software development. Although I would not call it Software development but “Code butchering”. It started as a teenager on a C64 with Basic and Assembler and ended in the late 1990s with Cobol/PLSQL working for a large US Consulting Company (yes, I was young and needed the money). Knowing the speed of financial institutions, I would not be surprised if some of my Spaghetti code would still be running somewhere….

Why am I saying this ? Because of course, Software stocks have been doing quite poorly over the past weeks/months. In addition, I also had the opportunity to play around with Claude Code first hand.

This week was quite busy, with (at least) 5 of my companies releasing 2025 numbers, some more preliminary than others. Overall it was a “mixed bad”. Some good, some not so good. Let’s jump in:

“One important thing to understand with Frosta is that they don’t try to smooth earnings much, at least not to the upside. So you might always be in for some surprise either at the 6 month mark or annual report. Their guidance is usually very wide. Sometimes they decide to increase marketing expenses significantly which lowers profit in the current year but boosts revenues in the next year. In the long run, this has turned out very well for shareholders but for “weak hands” this can be a little bit unnerving.”

I guess this was once again such an event. Net income actually declined -12% in 2025. On the other side, growth of the Frosta Brand with ~16% and the ready made meals with almost 18% in 2026 is far above the market growth. So Frosta is taking significant market share. The dividend will remain at 2,40 EUR. They guide towards overall growth between 4-9% and a net margin of 4-8% in 2026 which is of course again very wide but implies that growth will continue for the Brand.

Disclaimer: This is not Investment advice. The stock discussed is very illiquid and trades at the unregulated market (Freiverkehr). If you want to buy this stock, work very carefully with strict limits. The author owns the stock and might buy/sell it without giving prior notice. And as always: PLEASE DO YOUR OWN RESEARCH !!

After having two (relatively) exciting stocks in the last two weeks with Rocket Internet and Innoscripta, I decided to tune down the exitement a little bit and focus on a very boring, family run German small cap this time. In order to not fall asleep, you might want to listen to the Soundtrack while reading:

Elevator Pitch:

This write-up is special in two ways. For one, I have privately bought the stock already a few months ago. Secondly, I base this write-up on another write-up from my friend Jon from abilitato.de. So please read that one before you read my “mini-writeup” where I only focus on a few specific aspects.

In a nutshell, Frosta is a boring, under-the-rader German family owned and run frozen Food company that does not do a lot of investor relations but runs a very convincing strategy focusing on additive-free ready made frozen meals. Inventing this category more than 20 years ago, the main Frosta brand is now growing with solid “mid teens” percentage rates p.a., has succesfully managed to enter and grow in neighbouring countries and with profitability that is steadily increasing. For the quality of the company and the potential growth prospects, the stock is still relatively cheap in my opinion at around 12×2025 P/E (ex net cash).

Here ist the write-up. Best read it after having a decent “Chicken Paella” from Frosta 😉

My timing of my Innoscripta write-up was a little bit unfortunate. Just a day later, Innoscripta held a conference call explaining the 2025 numbers. I think I need to better check the calenders of the companies I write about in the future….

I listened to the Call on Quartr. My main (and of course subjective) take-aways:

as a relatively new initiative, they develop a “safe storage” for R&D data

the arguments about LLMs and their limitations did not overly convince me. The arguments rely on today’s abilities of LLMs, but the question is how this will develop in 1,3 or 5 years. Especially I do not see that the LLM in the hand of a client itself is the competitor but competitors (especially other consultants) using AI to rapidly develop (cheaper) alternatives

Cash conversion (to EBIT) is currently around ~60% but they try to improve cash collection

They are bullish on the Government increasing the programs in general (regulatory tailwinds)

They claim that they see increasing revenue from the same clients which I find quite surprising. They didn’t however provide any concrete numbers

The clarified that the overall proces from application to cash collection is 9-12 months (3 months for innovation approval, 6-9 months for tax credits)

They claim that the “front loading” of 4 year applications seems not so significant

There is a clear seasonality that companies hand in filings mostly in Q4 in order not to lose credits for T-4 projects

Revenue in Q1 2026 should look good (whatever that means, not sure if they compare this to Q4 2025 or Q1 2025)

The currently do not consider M&A for international expansion but try to grow organically in 4 different countries (UK & US was mentioned)

The question if the 40% growth for 2026 is relevant was somehow confirmed but very indirectly. A “real” guidance should be expected for the AGM in April

Interestingly, the overall growth in the German Tax Credit market was +60% in 2025 which means Innoscripta’s growth is in line with the market and they want to grow with the market. More details again shall be provided at the AGM. The analyst mentioned that the market will grow less than 40% in 2026

The question how big the “4 year front loading effect” actually is, they were quite evasive. They mentioned that there will be growth internationally and through “Software” and Tax Credits is described as a “Milestone” or “trojan horse” to get other business.

Cash usage: No additional cash is needed for growth. Buy backs limited due to limited liquidity but rather distributions.

Overall my impression is that at least 2026 should look pretty Ok, but further out it gets a little bit vague. International expansion is clearly more risky than increasing market share in Germany.

But overall it remains a very interesting and dynmaic company and I am looking forward to the Annual Shareholder Meeting which I hopefully can attend.

Innoscripta, a young German “SaaS company” which IPOed in 2025 came to my attention because it is extremely profitable (EBIT margin 60%) and growing like crazy (10x in sales since 2020). However, because of the unique revenue model (success fee instead of software fees) and a rapid decrease in quarterly growth in 2025, I am currently not investing, although the stock is not super expensive at 21x trailing P/E. But I will keep a close watch.

The 2025 IPO

Innoscripta was one of the few “official” IPOs in Germany in 2025. If we look at the share price, it was not a very successful one: