Fundsmith 6M letter – Active vs. passive, Momentum & Style change

Management Summary:

In this post, out of pure self-interest, I looked a little bit deeper into Terry Smith’s controversial 6M Fundsmith report and focus on the “Active vs. Passive” debate, how Fundsmith’s Buys and Sells look under my own Momentum scoring and some thoughts on changes in investment management styles.

Intro & Background

Terry Smith, the outspoken Boss of UK “Quality Value” Fund Manager Fundsmith dropped a quite unexpected 6M letter to investors where he basically communicated a pretty drastic pivot compared to what he said over the past 15 years.

In an “unprecedented” move, he switched ~50% of the portfolio within 6 months which is very unusual for his fund. In previous years, annual turnover of the portfolio was on average less than 10%.

His mantra of “do nothing” was repeated in every letter and often repeated in his talks.

In the most recent letter, he blames, as several times before, “passive ETFs” for market distortions and claims that those active managers that are currently successful are most likely “momentum chasers”.

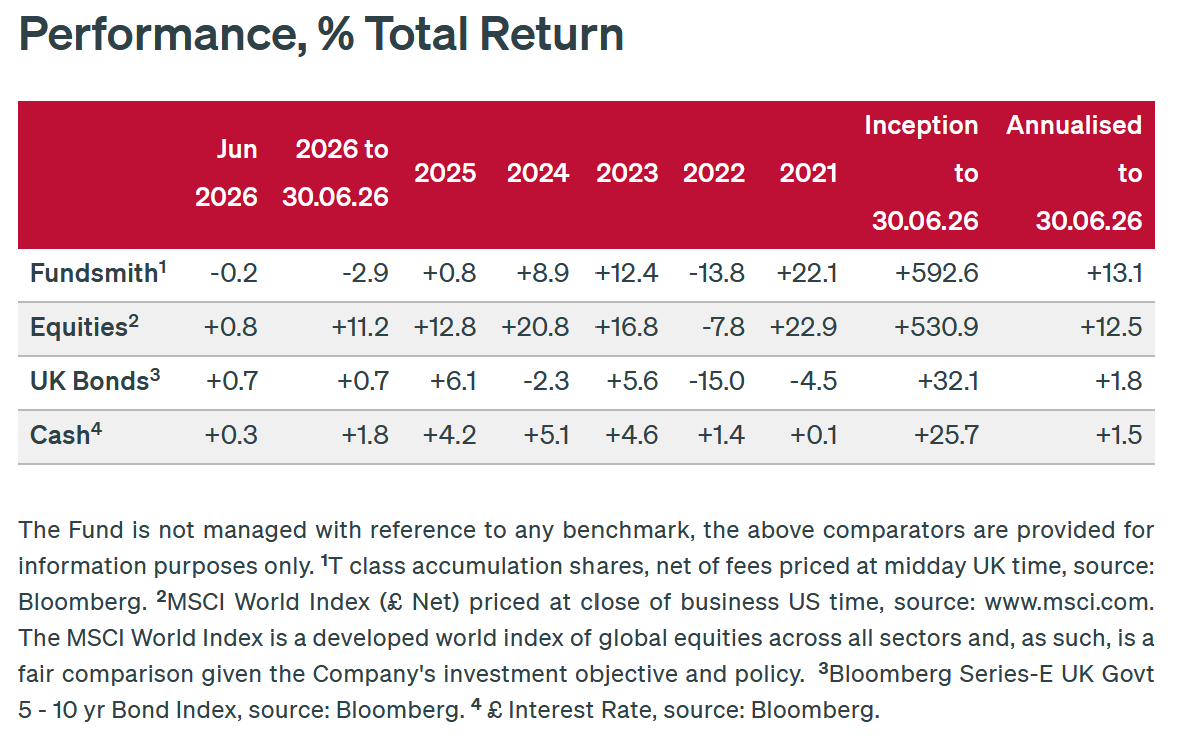

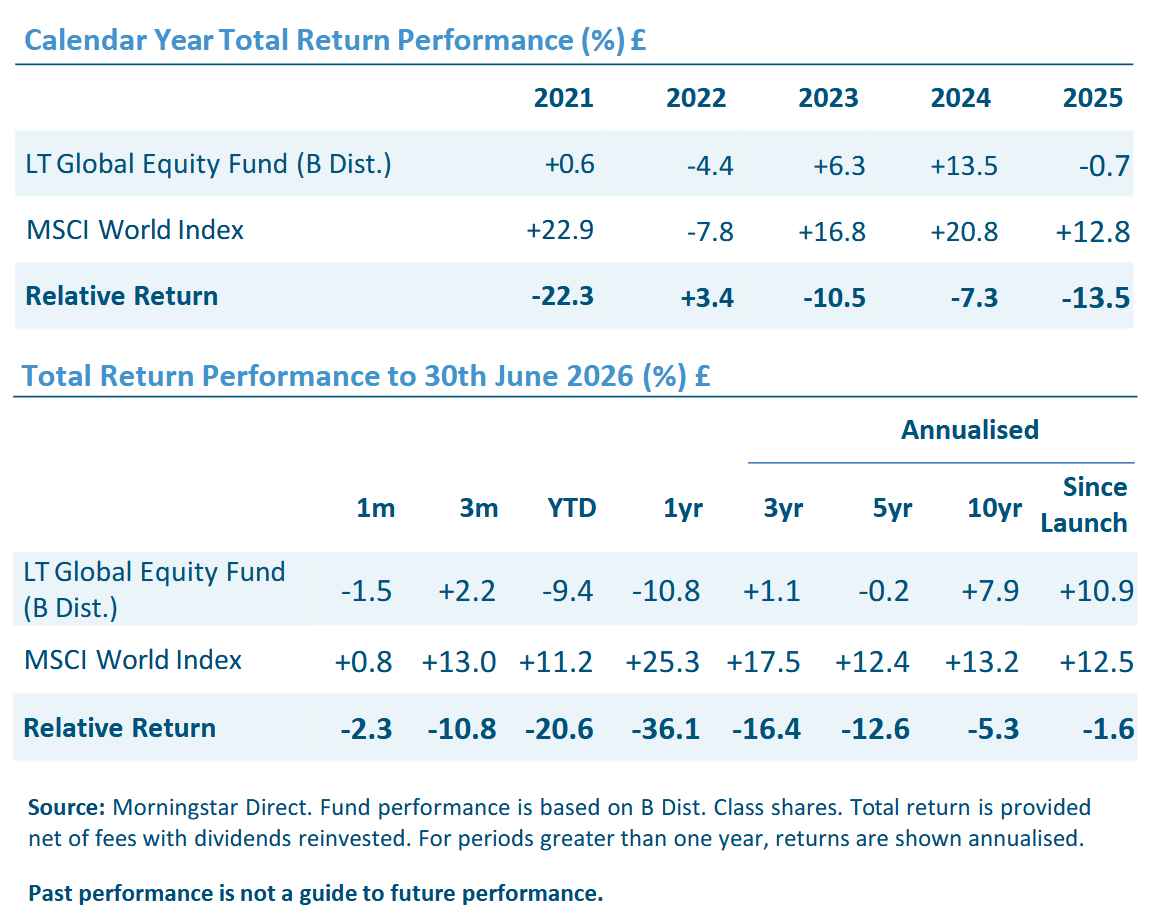

Fundsmith to be clear is not the worst active fund. With a TER of ~1% they are also not on the extremely expensive side and since inception, the track record is still pretty ok. However, a quick look at his recent fund factsheet shows that for the past 4 ½ years, the fund underperformed the MSCI World pretty drastically:

He underperformed both, in up markets and in the down year 2022. So it is clearly not a “low vol” effect.

Nevertheless I found that letter interesting due to the following aspects in which I will dive a little bit more:

- Active vs. Passive

- Smith’s somehow inconsistent treatment of “momentum” which is a factor I have been paying more attention to since some time now

- The question of how to generally shift/pivot/adapt an investment strategy (if at all)

- Active vs. Passive

I actually read the Substack post that Terry Smith referenced which can be found here:

It summarizes quite well the general view from many active managers why too much index investing is very dangerous and might end in a total collapse of the stock market. While there might be a (smallish) probability for this scenario, it sounds a little bit like the typical “Old man shouting to the clouds” cartoon.

On the other hand, the article also doesn’t really cover that as a whole, Active Management just has never really justified its rather significant cost.

In the “good old times”, active funds had been the gate keepers between individual investors and the stock market with the only alternative being stock brokers.

These days however, the ease of buying an ETF and the low cost is clearly a very attractive value proposition compared to “classical” funds where often still an intermediary is clipping an additional fee (and or the bank).

In the US, the largest market for funds globally, ETFs in general are also significantly more tax efficient than (active) Mutual Funds.

Only claiming that there will be Doom with too many passive structures is not so convincing and rather looks like an attempt to scare regulators in protecting the still very profitable business of underperforming asset managers and wealth advisors.

In my opinion, these days an active manager really needs to have a more convincing story than just that one from Mr. Evan-Cook. Your really need to offer something to investors that they can’t get through low cost Index ETFs which is not so easy.

Just a few days ago, FT Alphaville tried to debunk another narrative: That if there are only a few active managers left, there will be a big bounty for those remaining managers.

They argue that the opposite is true: As the remaining ones are the smart ones, there are not enough “patsies” to make the “big hay”:

In any case, it will be interesting to see how the active vs. passive debate continues, but there won’t be a magic turnaround any time soon in my opinion. Index ETFs are here to stay and the Active Management industry really needs to find ways to create actual value for investors in some way.

2) Momentum

In the letter, it almost seems that Terry Smith has written parts without looking at the whole “enchilada”.

On page 3&4 he shows a chart that Momentum is dangerously high as last seen in 1999 before the Dotcom Boom. And then, only a few pages later he writes the following:

We will take more account of momentum — both fundamental and share price — in our investment decisions. In particular, we will be much less willing to deploy the time-honoured technique of buying quality companies when they hit a glitch

As some of my readers might remember, I did start to include momentum into my decision process a year ago. But in a less drastic way than Terry Smith and more “gradual”.

In my comprehensive Scoring system, Momentum is reflected by 4 indicators as part of an overall score that also includes “Quality” and “Valuation”:

For “momentum” my crude assessment looks as follows:

- Current EPS momentum (i.e. EPS LTM is higher than the previous year): 1 Point if Yes, 0 otherwise

- Stock price is above the 200 day moving average 1 Point if Yes, 0 otherwise

- The stock price performance of the last 6 Months (1 Month lag) is positive or negative (1 Point of Performance is > +5%, -1 point if Performance is <-5%, 0 points otherwise)

- The stock price performance of the last 12 Months (1 Month lag) is positive or negative (1 Point of Performance is > +5%, -1 point if Performance is <-5%, 0 points otherwise)

So overall, my “momentum score” can go from minimum of -2 to a maximum of +4 within a total score that can reach, including Quality and Valuation, scores a total score of 18.

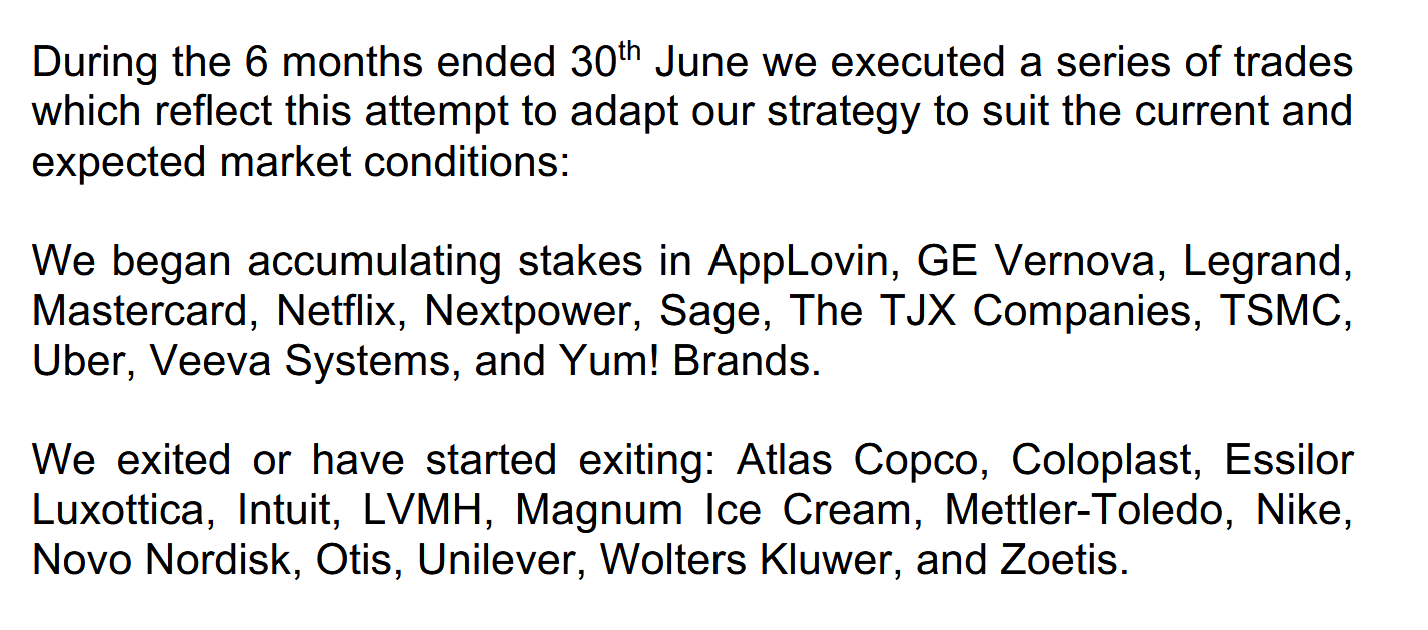

So for fun I just tried to score the stocks that Fundsmith sold and bought. Here is Terry’s summary:

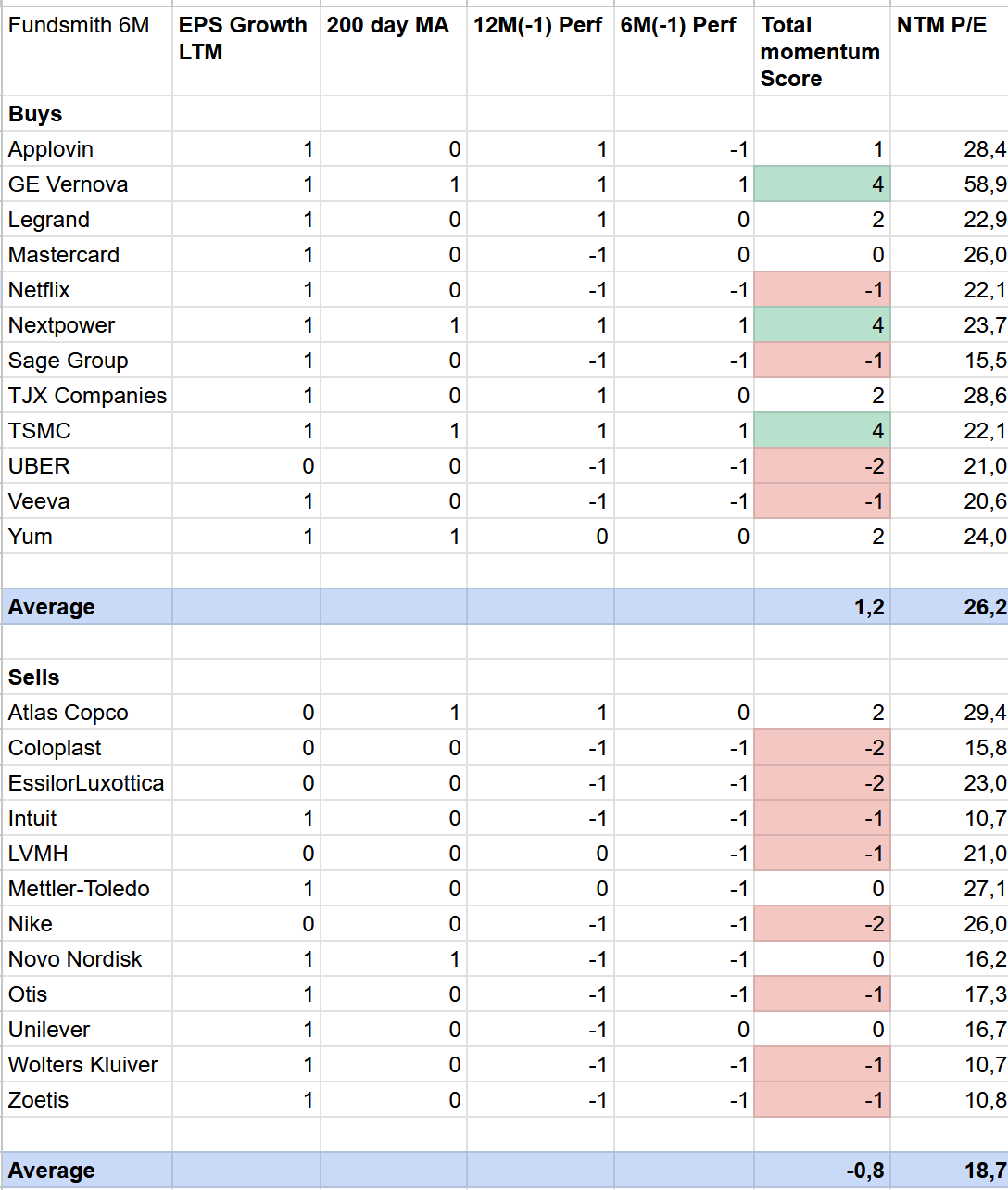

And here is the table scoring Terry’s stocks, both, the buys and sells with my crude momentum measure:

Two things stand out in aggregate:

The stocks that he sold, on average, look indeed worse from a momentum perspective than the ones he bought. And the stocks he sold are a lot cheaper than the ones he bought.

It’s also interesting that only 3 of the stocks he bought would get a maximum Momentum score in my system (GE Vernova, TSMC and Nextpower). Some of the stocks have rather negative Momentum under my definition (Uber, Netflix & Veeva).

It’s also obvious that he wanted to have some exposure to the Datacentre /AI theme via TSMC, GE Veronica, NextPower, Legrand and maybe UBER.

Overall it looks to me that he still focuses on fundamentals but looks for more “positive fundamental momentum”.

One question I have been asking myself is why he didn’t sell some of these stocks earlier. One example which I have looked into under another context is Essilor Luxottica. Here is the chart of the implicit NTM PE over the past 10 years:

We can see that until the end of 2025, the stock was valued at 40x NTM P/E, far above the average.

If we look at the margin and Return on Capital ratios over time we can see that after the merger between Essilor and Luxottica, margins never recovered there previous level and Return on Capital was a depressing mid single digit.

That begs the question why you would want to own such a stock at such a valuation in the first place.

Anyway, Terry Smith clearly now wants to avoid “unloved” stocks and is looking to invest more into stocks that do at least from a fundamental perspective well, even if the new stocks are on average significantly more expensive than the sold ones.

With such an approach, in my opinion, his “do nothing” mantra won’t work, because in the current environment, fundamentals can change ven more quickly than before.

It will be interesting to see if and how fast he will turn over his portfolio going forward.

3) If and how to shift/pivot/adapt an investment strategy

One “peer” to Terry Smith is Nick train from Linsell Train funds who has a similar “quality focused” approach. In his 6M letter (Global Fund) however, he is rather adding to his losers than selling them. One prominent example is Intuit:

But buying a consensus AI loser stock today doesn’t mean arguing no risk from AI (or anything else we haven’t yet seen coming). It means taking a calculated risk, based on

likelihood and the trade-off with price, and accepting the emotional discomfort of appearing unconventionally wrong. To give a pertinent example, Intuit was easily the Fund’s worst performer in June, declining 21% in USD terms, down now nearly two-thirds from last year’s highs. Whilst 2025’s valuation was arguably steep at a c.2.5% free cash flow yield, the collapse to what is now over 10% feels egregious. As above, we think it likely that the prior

bullishness resulted from the general extrapolation of past successes – with, it must be said, some justification: Intuit has grown revenues organically at double-digit rates every year this decade, whilst its EPS is up 4.5-fold versus FY2016. But the forward bearishness, predicated we assume on acute (but typically unsupported) fears of AI disintermediation, feels disproportionate. The non-GAAP multiple on next year’s EPS (which management still guide to grow at c.16-18%!) is now down to 11x. To achieve a normal nominal return (say the US market’s historic 9% p.a.) now implies negative forward earnings growth. As little as a year ago, analyst debate focused on whether Intuit could sustainably hit 20% revenue growth versus the prior mid-teens rates

I think the Nick Train vs. Terry Smith “contest” is an interesting case study on the merits of changing your investment approach abruptly.

One needs to mention that Nick Train’s track record for this fund is even worse than Terry Smith’s, underperforming the MSCI World by a pretty wide margin since inception in 2011:

Overall, I think in every long investment career, it will be necessary to change and adapt one’s approach to investment in order to stay relevant.

The most famous example here is Warren Buffett who changed his approach fundamentally at least 2 times. From Graham Deep Value to Quality to “Full scale take-over conglomerate” investing. With his initial approach, he would never had been able to reach the size that he has reached today. The same with listed-minority investments in general.

From what I have seen, a rapid increase in AUMs for any manager is often in the end much more a curse than a blessing. Yes, you earn a lot more fees but unless a manager significantly adjusts the strategy, returns will suffer after a certain increase almost inevitably.

The question is clearly how to do this in a way that does not create confusion on the investor side and is hopefully constructive for the future results.

In Terry Smith’s case, I am struggling a little bit with his previous mantra that “do nothing” is the one and only thing and then abruptly change that within a 6 month period. My feeling would have been that he should have toned down the language a little bit earlier already, unless he really did this pivot on short notice.

In Nick Train’s case, doing nothing (or not much) after now being down since inception is maybe also not 100% optimal.

For a lot of institutional investors, 3 years are maybe the maximum they can tolerate underperformance before they pull the trigger. Both Fundsmith and Lindsell &Train are clearly past that mark.

From my perspective, every active fund manager should realize that luck is a big part of the game and when things are good, one should give some credit to good luck instead of claiming all the outperformance due to superior skills. I guess that might make things a little bit easier when inevitably things don’t look so great.

In any case, I do think that a shift in strategy should be prepared and executed including relevant and documented changes in process and also personnel.

What you clearly also need is some patience. Don’t expect that a structural change will improve performance on day one. This will need time.

In any case, as mentioned above, Active Equity Management is facing a lot of headwinds any way, which makes it even more difficult to dig yourself out from an “performance hole”.

Summary:

It is obviously too early to tell if and what we can learn from Terry Smith’s recent actions, but on the surface they look a little bit like a “panic move”.

Going forward, Lindsell & Train will be a good comparison because they seem to keep doing what they have been doing and are even doubling down on their losers.

In any case, for me personally it is clearly some kind of evidence that completely ignoring “momentum”, being fundamental or purely stock price driven is not a good idea. “Do nothing” in my opinion is harder than ever and maybe not the dominant strategy going forward. In my opinion, using momentum as an additional factor in stock picking and portfolio management can clearly improve the process to a certain extent.